Archives

978-1118582558 Appendix A

1 APPENDIX A THE TIME VALUE OF MONEY EXERCISES EA–1 Time Periods (Years) Compound Interest Rates 5 10 15 5% $150 1.27628 $150 1.62889 $150 2.07893 = $191.44 = $244.33 = $311.84 EA–2 Time Periods (Years) Compound […]

978-1118582558 Appendix B

1 APPENDIX B QUALITY OF EARNINGS CASES: A COMPREHENSIVE REVIEW CASE 1: LIBERTY MANUFACTURING The analysis that can be done on Liberty is limited because there is no access to macroeconomic information, industry data, or the company’s financial statements from […]

978-1118582558 Chapter 1

1 CHAPTER 1 FINANCIAL ACCOUNTING IN AN ECONOMIC CONTEXT ISSUES FOR DISCUSSION ID1–1 Security analysts and stockholders: These users would use financial statements to try to estimate the future earnings and cash flow potential of the company, which would be […]

978-1118582558 Chapter 10 Part 1

1 CHAPTER 10 INTRODUCTION TO LIABILITIES: ECONOMIC CONSEQUENCES, CURRENT LIABILITIES, AND CONTINGENCIES BRIEF EXERCISES BE10–1 a. Dividends declared during a year and the actual cash paid for dividends during the year may be different because dividends declared includes dividends that […]

978-1118582558 Chapter 10 Part 2

P10–6 Concluded b. Ending balance = Beginning balance + Promotional expense – Refund payments P10–7 a. Restructuing Expense (E, –SE) …………………………………………………………. 425 Assets (-A) ………………………………………………………………………………. 364 Severance Liability (+L) …………………………………………………………….. 61 b. The $364 million expense was subtracted from earnings […]

978-1118582558 Chapter 11 Part 1

1 LONG-TERM LIABILITIES: NOTES, BONDS, AND LEASES BRIEF EXERCISES BE11–1 a. During 2012 Radio Shack paid down $88.1 million of notes payable (long-term debt) and borrowed $175.0 million of other long-term debt. Further, the reduction in the unamortized discount reflects […]

978-1118582558 Chapter 11 Part 2

would reduce net income by a total of $11,179.56 [from part (b)] for the interest expense associated with the lease and for the depreciation associated with the capitalized asset. Future obligations under operating leases are not disclosed in a company’s […]

978-1118582558 Chapter 11 Part 3

P11–10 Concluded c. Ginny and Bill Eateries is required to make an interest payment on June 30, 2015 under the terms of the debt agreement. The entry to record this payment would be: Interest Expense (E, –SE) ………………………………………………………………… 15,378a Premium […]

978-1118582558 Chapter 12 Part 1

1 CHAPTER 12 STOCKHOLDERS’ EQUITY BRIEF EXERCISES BE12–1 a. 38.4% of net income was paid in dividends during the year ($1,743/$4,535). b. The issuance of common stock affected the basic accounting equation by increasing assets (cash) and BE12–2 a. The […]

978-1118582558 Chapter 12 Part 2

P12–7 Concluded Stockholders’ equity: Common stock ($3 par value, 1,300,000 shares authorized, P12–8 a. 2011 Dollar Amount / Shares = Average price Exercised stock options $312.5 17.3 $ 18.06 Sale of common stock 19.1 0.5 $ 38.20 Repurchase of stock […]

978-1118582558 Chapter 13 Part 1

1 CHAPTER 13 THE COMPLETE INCOME STATEMENT BRIEF EXERCISES BE13–1 To accurately compare a company’s performance from one year to the next, non-recurring items such as debt retirements and accounting changes, as well as the activities of discontinued operations, should […]

978-1118582558 Chapter 13 Part 2

P13–2 a. Bonus = 25% (Income from Operations Before Interest Expense – Interest Expense) = 25% [$1,200,000 – ($1,000,000 8% Interest Rate)] = $280,000 b. Bonus = 25% (Income from Operations Before Interest Expense – Interest […]

978-1118582558 Chapter 14 Part 1

1 CHAPTER 14 THE STATEMENT OF CASH FLOWS BRIEF EXERCISES BE14–1 a. Depreciation expense is shown as an adjustment to net income to calculate cash flow. Depreciation expense is added back to net income because it is a non-cash expense. […]

978-1118582558 Chapter 14 Part 2

E14–17 Concluded L.L. Beeno Operating Section – Statement of Cash Flows (Indirect Method) For the Year Ended December 31, 2015 Cash flows from operating activities: Net income …………………………………………………………………. $ 5,500 Adjustments: Depreciation expense ………………………………………………. $ 3,300 E14–18 Martland Stores Operating […]

978-1118582558 Chapter 14 Part 3

P14–14 Concluded c. Working capital = Current assets – Current liabilities = ($25,000 + $23,200 + $11,200 + $4,000) – ($10,000 + d. Working capital = ($63,400 – $10,000 cash) – ($14,000 – $10,000 accounts payable) = $53,400 – $4,000 […]

978-1118582558 Chapter 14 Part 4

P14–19 Continued Prepaid Insurance Land Fixed Assets B.B. 0 B.B. 0 B.B. 0 (7) 80,000 (4) 40,000 (2) 750,000 (b) 20,000 B.B. 0 B.B. 0 B.B. 0 (11) 100,000 (3) 20,000 (12) 140 (3) 9,200 E.B. 100,000 E.B. 20,000 E.B. […]

978-1118582558 Chapter 2 Part 1

CHAPTER 2 THE FINANCIAL STATEMENTS BRIEF EXERCISES BE2–1 2012 2012 2012 Beginning Ending Retained 2012 2012 2012 Retained Earnings + Revenues – Expenses – Dividends = Earnings $40.3 + $65.5 – $59.3 – X = $43.2 X = $3.3 2012 […]

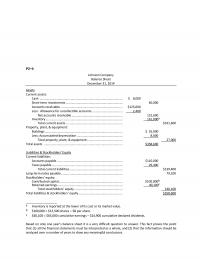

978-1118582558 Chapter 2 Part 2

P2–4 Johnson Company Balance Sheet December 31, 2014 Assets Current assets: Total current assets ………………………………………………………… $331,600 Property, plant, & equipment: Buildings ……………………………………………………………………………… $ 35,000 Less: Accumulated depreciation …………………………………………….. 8,000 Total property, plant, & equipment ………………………………….. 27,000 Total assets ………………………………………………………………………………. $358,600 […]

978-1118582558 Chapter 3 Part 1

CHAPTER 3 THE MEASUREMENT FUNDAMENTALS OF FINANCIAL ACCOUNTING BRIEF EXERCISE BE3–1 1. Fiscal period 6. Materiality 2. Economic entity 7. Matching 3. Conservatism 8. Objectivity 4. Consistency 9. Objectivity 5. Revenue recognition 10. Stable dollar EXERCISES E3–1 At the beginning […]

978-1118582558 Chapter 3 Part 2

14 P3–8 a. Book value on 12/31/14 = Total book value of assets – Total value of liabilities = $124,000 – ($8,000 + $20,000) = $96,000 b. The economic value of Myers and Myers equals its future cash flows discounted […]

978-1118582558 Chapter 4 Part 1

122 Chapter 4 CHAPTER 4 THE MECHANICS OF FINANCIAL ACCOUNTING BRIEF EXERCISES BE4–1 Transaction Assets = Liabilities + Stockholders’ Equity Paid $11,027 to purchase + 11,027 property, plant and equip. – 11,027 b. The transaction to purchase property, plant and […]

978-1118582558 Chapter 4 Part 2

associated with operating activities. Similarly, the company will recognize expenses when it has an outflow of assets or an inflow of liabilities associated with operating activities. E4–16 Concluded Consider the revenues being generated when the company is entitled to cash. […]

978-1118582558 Chapter 4 Part 3

Purchased Supplies. (5) Accounts Payable (–L)……………………………………………………….. 3 (6) Interest Payable (–L) …………………………………………………………. 3 Cash (–A)…………………………………………………………………….. 3 Paid interest accrued in previous period. (7) Cash (+A) …………………………………………………………………………. 9 Accounts Receivable (+A) ………………………………………………….. 9 Sales (R, +SE)……………………………………………………………….. 18 Rendered services. (8) Long-term […]

978-1118582558 Chapter 4 Part 4

P4–17 Continued e. Closing entries are posted to the T–accounts in Part (a). (A) Sales ………………………………………………………………………………. 1,700,000 Interest Revenue …………………………………………………………….. 1,620 Gain on Sale of Investment ……………………………………………….. 7,000 Depreciation Expense—Machinery ……………………………….. 47,500 Closed revenues and expenses into Income Summary. (B) […]

978-1118582558 Chapter 5 Part 1

1 CHAPTER 5 USING FINANCIAL STATEMENT INFORMATION BRIEF EXERCISE BE5–1 Coke Pepsi (a) ROE = Net Income/Average Stockholders’ Equity 27.7% 28.5% ROA = (Net Income +[Interest Expense (1-Tax Rate)])/ Average Total Assets 11.2% 9.3% Common Equity Leverage = Net Income/(Net […]

978-1118582558 Chapter 5 Part 2

21 industry averages, it is difficult to conclude whether the company is really effective in managing the owners‘ capital. 22 P5–4 Continued (2) Return on equity measures a company’s effectiveness at managing owners’ investments, while return on assets measures a […]

978-1118582558 Chapter 5 Part 3

37 P5–12 Continued Alternative 2 EPS: $7,050,000 ÷ 2,000,000 shares = $3.53 ROE: $7,050,000 ÷ ($45,000,000 + $7,050,000) = .1354 Alternative 3 EPS: $7,275,000 ÷ (2,000,000 shares + 100,000 shares) = $3.46 ROE: $7,275,000 ÷ ($45,000,000 + $2,500,000* + $7,275,000) […]

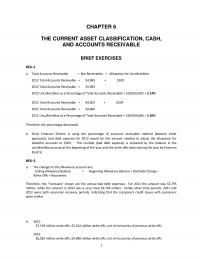

978-1118582558 Chapter 6 Part 1

1 CHAPTER 6 THE CURRENT ASSET CLASSIFICATION, CASH, AND ACCOUNTS RECEIVABLE BRIEF EXERCISES BE6–1 a. Total Accounts Receivable = Net Receivables + Allowance for Uncollectibles 2012 Total Accounts Receivable = $4,983 + $109 2012 Total Accounts Receivable = $5,092 b. […]

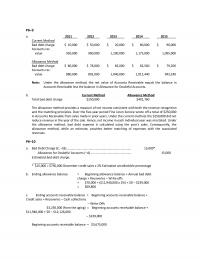

978-1118582558 Chapter 6 Part 2

P6–9 a. 2011 2012 2013 2014 2015 Current Method Bad debt charge $ 10,000 $ 50,000 $ 20,000 $ 80,000 $ 90,000 Accounts rec. Accounts Receivable less the balance in Allowance for Doubtful Accounts. b. Current Method Allowance Method Total […]

978-1118582558 Chapter 7 Part 1

1 CHAPTER 7 MERCHANDISE INVENTORY BRIEF EXERCISES BE7–1 The inventory purchases made by Hewlett-Packard during 2012 can be calculated as follows: Beginning inventory $ 7.5 billion BE7–2 a. From the footnote it is apparent that Johnson & Johnson is a […]

978-1118582558 Chapter 7 Part 2

For the Year Ended December 31, 20XX FIFO Averaging LIFO Sales $ 55,000 $ 55,000 $ 55,000 Cost of goods sold 38,900 36,891 34,900 P7–5 a. Cost of Goods Available for Sale = Cost of Goods in Beginning Inventory + […]

978-1118582558 Chapter 8 Part 1

CHAPTER 8 INVESTMENTS IN EQUITY SECURITIES BRIEF EXERCISES BE8–1 a. Comprehensive income includes all non-owner changes in shareholder equity that do not already appear on the income statement. For example, the change in value of assets that have been sold […]

978-1118582558 Chapter 8 Part 2

P8–5 a. 6/15/14 Trading Securities (+A) …………………………………………………. 7,500 Cash (–A) ……………………………………………………………… 7,500 12/31/14 Trading Securities (+A) …………………………………………………. 1,500 Unrealized Price Increase (Ga, +SE) …………………………. 1,500 Trading Securities (–A) …………………………………………… 3,600 b. The entries would remain the same except the following: […]

978-1118582558 Chapter 9 Part 1

1 CHAPTER 9 LONG-LIVED ASSETS BRIEF EXERCISES BE9–1 a. The new method, straight-line depreciation, will increase net income in the early years and reduce income in the later years versus using an accelerated method. An accelerated method of depreciation increases […]

978-1118582558 Chapter 9 Part 2

P9–2 a. 1/1/14 Relative Purchase Cost Asset FMV FMV Price = Allocation Building $ 300,000 300/1,200 $1,000,000 $ 250,000 Office equip. 150,000 150/1,200 1,000,000 125,000 b. Depreciation Expense—Building (E, –SE) ………………………………………….. 8,750a Depreciation Expense—Office Equipment (E, –SE) …………………………..… 30,000b […]

978-1118582558 Test Bank Chapter 1 Part 1

1. The balance sheet communicates a. proof to the investor that the company is profitable. b. assets, liabilities, and shareholders’ equity with all transactions reflected through the year. c. assets, liabilities, and shareholders’ equity as of a certain date. d. […]

978-1118582558 Test Bank Chapter 1 Part 2

Test Bank – Chapter 1 – Financial Accounting and Its Economic Context 1-19 64. Which of the following groups make up a company’s audit committee? a. Auditors. b. Outside directors from the Board. c. Company officers. d. All of the […]

978-1118582558 Test Bank Chapter 10 Part 1

1. The recognition of a deferred tax liability that results from the use of straight-line depreciation on financial statements and double-declining balance on tax returns will a. increase the current ratio. b. increase the debt/equity ratio. c. increase the quick […]

978-1118582558 Test Bank Chapter 10 Part 2

Test Bank – Chapter 10 – Introduction to Liabilities: Economic Consequences, Current Liabilities, & Contingencies 10-21 62. The following information was taken from the annual report of Jones Inc. 2015 2014 BALANCE SHEET Deferred income tax liability $29,700 $28,300 INCOME […]

978-1118582558 Test Bank Chapter 10 Part 3

Test Bank – Chapter 10 – Introduction to Liabilities: Economic Consequences, Current Liabilities, & Contingencies 10-35 13. Porter Products recognizes expenses for wages, interest and rent when cash payments are made. The following related cash payments were made during December […]

978-1118582558 Test Bank Chapter 11 Part 1

1. Which one of the following will result from receiving cash upon issuing long-term debt? a. Increase of the company’s indebtedness b. Decrease of the current ratio c. Increase of retained earnings d. Increase of total shareholders’ equity Ans: A […]

978-1118582558 Test Bank Chapter 11 Part 2

Test Bank – Chapter 11 – Long-Term Liabilities: Notes, Bonds, and Leases 11-21 63. Duncan Industries sold $100,000 of 12 percent bonds on January 1, 2011, when the market interest rate was 10 percent and received $107,732 for them. The […]

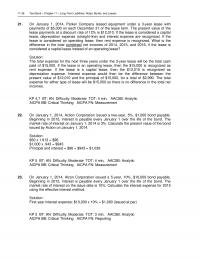

978-1118582558 Test Bank Chapter 11 Part 3

11–36 Test Bank – Chapter 11 – Long-Term Liabilities: Notes, Bonds, and Leases 21. On January 1, 2014, Parker Company leased equipment under a 3-year lease with payments of $5,000 on each December 31 of the lease term. The present […]

978-1118582558 Test Bank Chapter 12 Part 1

1. A corporation issued common stock instead of debt to finance the purchase of non– depreciable property. Which statement is true? a. Ownership by existing shareholders will be diluted. b. The company’s debt/equity ratio will be higher. c. Income tax […]

978-1118582558 Test Bank Chapter 12 Part 2

55. The shareholders’ equity section of the Jason Company as of December 31, 2015 is as follows: Common stock $180,000 Additional paid-in capital (Common stock) 110,000 Retained earnings 160,000 Total shareholders’ equity $450,000 On January 15, the company repurchased 1,500 […]

978-1118582558 Test Bank Chapter 12 Part 3

Test Bank – Chapter 12 – Shareholders’ Equity 12–37 AICPA BB: Critical Thinking AICPA FN: Reporting 15. On January 23, Bayshore Corporation, for the first time in its short history, purchased 200 shares of its own common stock for $40 […]

978-1118582558 Test Bank Chapter 13 Part 1

1. Which one of the following events is an operating transaction? a. Purchase of equipment b. Payment for equipment rental c. Purchase of land d. Issuing bonds for cash Ans: B KP 2 BT: C Difficulty: Easy TOT: 1 min. […]

978-1118582558 Test Bank Chapter 13 Part 2

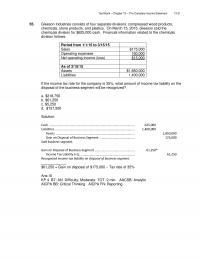

Test Bank – Chapter 13 – The Complete Income Statement 13-21 55. Gleeson Industries consists of four separate divisions: compressed wood products, chemicals, stone products, and plastics. On March 15, 2015, Gleeson sold the chemicals division for $625,000 cash. Financial […]

978-1118582558 Test Bank Chapter 13 Part 3

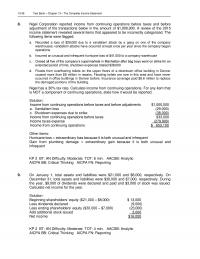

13–36 Test Bank – Chapter 13 – The Complete Income Statement 8. Nigel Corporation reported income from continuing operations before taxes and before adjustment of the transactions below in the amount of $1,000,000. A review of the 2015 income statement […]

978-1118582558 Test Bank Chapter 14 Part 1

1. How will a company classify ‘proceeds received from the issuance of long–term bonds’ on its statement of cash flows? a. Cash provided from operations b. Cash used in operations c. Cash provided from investing activities d. Cash provided from […]

978-1118582558 Test Bank Chapter 14 Part 2

60. The following information was taken from the records of Albert’s Fine Coffee: 2015 2014 Machinery $90,000 $40,000 Accumulated depreciation (30,000) (20,000) Depreciation expense 14,000 12,000 Gain on sale of machinery 4,000 1,000 During 2015, machinery with a cost of […]

978-1118582558 Test Bank Chapter 14 Part 3

15. During 2015, equipment was sold for $57,000. This equipment cost $90,000 and had a book value of $47,000. Accumulated depreciation for equipment was $184,000 at 12/31/15 and $147,000 at 12/31/14. Show how the results of the three items will […]

978-1118582558 Test Bank Chapter 2 Part 1

1. Current assets are: a. all assets except inventory. b. all assets that provide benefits extending beyond one year. c. cash, accounts receivable, and buildings. d. all assets that are expected to be converted to cash in the near future. […]

978-1118582558 Test Bank Chapter 2 Part 2

Test Bank – Chapter 2 – The Financial Statements 2-21 Solution: 1. D 2. E 3. B 4. A 5. G 6. C KP 2 BT: K Difficulty: Easy TOT: 2 min. AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: […]

978-1118582558 Test Bank Chapter 3 Part 1

1. When preparing the financial statements, we assume that the life of the entity will continue beyond the current period. Which assumption are we most likely following? a. Stable dollar theory. b. Going concern assumption. c. Economic entity assumption. d. […]

978-1118582558 Test Bank Chapter 3 Part 2

c $187,500 = ($100,000 ÷ $800,000) $1,500,000 68. Karr Construction built a levee for the state of Mississippi over a three-year period. The contracted price for the levee was $1,500,000. The costs incurred by Karr and the payments from […]

978-1118582558 Test Bank Chapter 4 Part 1

1. The accounting period is the time a. the Controller decides to close the books. b. between selling a product to a customer and collecting the cash from the customer. c. that it usually takes to journalize and post events […]

978-1118582558 Test Bank Chapter 4 Part 2

Test Bank – Chapter 4 – The Mechanics of Financial Accounting 4-21 4-22 Test Bank – Chapter 4 – The Mechanics of Financial Accounting 68. On December 31, 2015, immediately after all the adjustments were made to Gilbert Inc.’s accounting […]

978-1118582558 Test Bank Chapter 4 Part 3

4-40 Test Bank – Chapter 4 – The Mechanics of Financial Accounting 13. Total assets, liabilities, and shareholders’ equity are $22,000, $5,000, and $17,000 before land costing $10,000 is purchased in exchange for a $1,000 note payable and $9,000 cash. […]

978-1118582558 Test Bank Chapter 5 Part 1

1. The current ratio is a. current assets divided by current liabilities. b. current liabilities divided by current assets. c. current assets divided by total liabilities. d. total assets divided by total liabilities. Ans: A KP 5 BT: K Difficulty: […]

978-1118582558 Test Bank Chapter 5 Part 2

Test Bank – Chapter 5 – Using Financial Statement Information 5-21 54. Rudy Company has total assets, liabilities, and shareholders’ equity of $28,000, $21,000, and $7,000, respectively. Assume no material change occurred during the year to totals on the balance […]

978-1118582558 Test Bank Chapter 5 Part 3

10. Washington Company has current assets, current liabilities, and long-term liabilities of $6,000, $2,000, and $5,000, respectively at the end of 2015. How much cash can Washington use to acquire equipment and retain a current ratio of at least 3.0? […]

978-1118582558 Test Bank Chapter 6 Part 1

1. Current assets are assets which a. can be used immediately to retire liabilities. b. are newly acquired. c. have been converted into cash in the previous year. d. are intended to be converted into cash within one year. Ans: […]

978-1118582558 Test Bank Chapter 6 Part 2

58. The following information was taken from the unadjusted trial balance and aging schedule of Diane Company on December 31, 2015. All sales are on account. Accounts and related balances at December 31, 2015 before adjustment: Debit Credit Accounts receivable […]

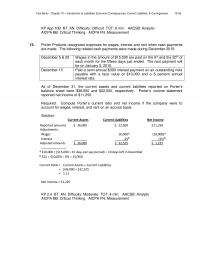

978-1118582558 Test Bank Chapter 6 Part 3

6-32 Test Bank – Chapter 6 – The Current Asset Classification, Cash, and Accounts Receivable KP 5 BT: AN Difficulty: Moderate TOT: 6 min. AACSB: Analytic AICPA BB: Critical Thinking AICPA FN: Measurement Use the information that follows from the […]

978-1118582558 Test Bank Chapter 7 Part 1

1. Portland Supplies Co. mistakenly excluded $3,000 of goods from its December 31, 2015 physical inventory count. Its December 31, 2016 inventory amount was correct. As a result of this error, a. 2015 income is overstated by $3,000. b. 2015 […]

978-1118582558 Test Bank Chapter 7 Part 2

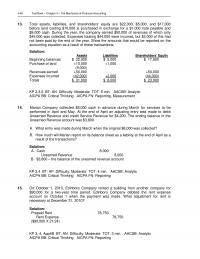

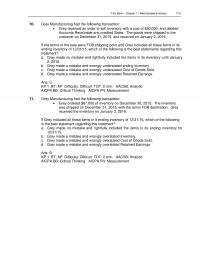

Test Bank – Chapter 7 – Merchandise Inventory 7-21 70. Grey Manufacturing had the following transaction: • Grey received an order to sell inventory with a cost of $50,000, and debited Accounts Receivable and credited Sales. The goods were shipped […]

978-1118582558 Test Bank Chapter 8 Part 1

1. Equity investments are: a. investments in bonds of a corporation. b. investments that pay dividends, not interest. c. classified as long-term liabilities. d. marketed by the SEC to any investor who wishes to buy bonds of a public company. […]

978-1118582558 Test Bank Chapter 8 Part 2

56. The following information related to the marketable security investments of Solo Company. Securities held on December 31, 2014, as described in the table below. AAA and BBB are classified as trading securities and CCC is classified as an available-for- […]

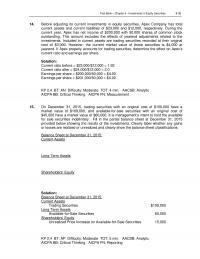

978-1118582558 Test Bank Chapter 8 Part 3

Test Bank – Chapter 8 – Investments in Equity Securities 8-39 14. Before adjusting its current investments in equity securities, Apex Company has total current assets and current liabilities of $23,000 and $12,000, respectively. During the current year, Apex has […]

978-1118582558 Test Bank Chapter 9 Part 1

1. Which one of the following should be classified as land on the balance sheet? a. A shed that houses the company’s equipment. b. Mineral rights representing gold in the soil c. Two tracts of property that houses the company’s […]

978-1118582558 Test Bank Chapter 9 Part 2

Test Bank – Chapter 9 –Long-Lived Assets 9-21 62. The following items represent common post acquisition expenditures incurred on equipment. A. Replacement of defective parts B. Rewiring costs to increase operating speed C. Painting costs D. Repair of the major […]

978-1118582558 Test Bank Chapter 9 Part 3

20. On April 1, Tarpon Co. made the following expenditures on its printing press: Purchase of stapling attachment $8,000 Installation of attachment 2,000 Cleaning and oiling press costs prior to renovation 1,000 Replacement parts for renovation of printing press 1,000 […]