Archives

978-1133188797 Chapter 1 Thomson ONE Solution

Thomson One; Chapter 1 Page 1 of 2 Thomson ONE solutions Gibson, Financial Reporting & Analysis: Using Financial Accounting Information, 13e Chapter 1 THOMSON ONE This chapter’s Thomson ONE exercise introduces the Merck & Company in terms of business description, […]

978-1133188797 Chapter 1 To the Net

Chapter 01 1 TO THE NET 1. a. The Mission of the Financial Accounting Standard Board (FASB) The mission of the FASB is to establish and improve standards of financial accounting and reporting that foster financial reporting by nongovernmental entities […]

978-1133188797 Chapter 10 Thomson ONE Solution

Thomson One; Chapter 10 Page 1 of 2 Thomson ONE solutions 13e Chapter 10 THOMSON ONE This Thomson ONE exercise, using the Merck & Company, provides for the review of cash flow and cash flow ratios. Chapter 10 I. Enter […]

978-1133188797 Chapter 10 To the Net

Chapter 10 TO THE NET 1. a. Item 1 Business History space and into cyberspace. b. Direct Method The principle advantage of the direct method is that it shows the operating cash receipts and payments. Knowledge of where operating cash […]

978-1133188797 Chapter 11 Thomson ONE Solution

Thomson One; Chapter 11 Page 1 of 2 Thomson ONE solutions Gibson, Financial Reporting & Analysis: Using Financial Accounting Information, 13e Chapter 11 THOMSON ONE ratios and Worldscope ratios. Chapter 11 I. Enter MRK in “Companies” (Merck & Company, Inc.). […]

978-1133188797 Chapter 11 To the Net

Chapter 11 TO THE NET 1. a. “Kimberly-Clark Corporation was incorporated in Delaware in 1928. We are a global company focused on leading the world in essentials for a better life b. December 31, 2010 December 31, 2009 (In millions) […]

978-1133188797 Chapter 12 Thomson ONE Solution

Thomson One; Chapter 12 Page 1 of 2 Thomson ONE solutions 13e Chapter 12 THOMSON ONE This Thomson ONE exercise uses Fifth Third Bancorporation to address a “special industry”. Chapter 12 I. Enter FITB in “Companies”. Look up “Fifth Third […]

978-1133188797 Chapter 12 To the Net

Chapter 12 409 TO THE NET 1. a. Item 1 Business Market Area Competition b. Table 7 – Nonperforming Assets Loans past due 90 days or more but still accruing These loans peaked in 2007 and then materially declined. Loans […]

978-1133188797 Chapter 13 To the Net

Chapter 13 TO THE NET 1. The following questions can be discussed using “Facts About GASB”: a. What is the GASB? 2. The following can be discussed using the “Summary of the Plan”: a. Vision b. Mission c. Core values […]

978-1133188797 Chapter 2 Thomson ONE Solution

Thomson One; Chapter 2 Page 1 of 5 Thomson ONE solutions 13e Chapter 2 THOMSON ONE This Merck & Company exercise uses the proxy statement to review the directors, board committees, and executive officers. Students find the Executive Officers compensation […]

978-1133188797 Chapter 2 To the Net

Chapter 02 TO THE NET 1. COSO was originally formed in 1985 to sponsor the National Commission on Fraudulent Financial Reporting, an independent private sector initiative which studied the casual factors that can lead to fraudulent financial reporting and developed […]

978-1133188797 Chapter 3 Thomson ONE Solution

Thomson One; Chapter 3 Page 1 of 1 Thomson ONE solutions 13e Chapter 3 THOMSON ONE This Thomson ONE exercise provides for a review of key balance sheet data for the Merck & Company. The trend will change as Thomson […]

978-1133188797 Chapter 3 To the Net

Chapter 03 TO THE NET 1. a. $523,050,000 b. Goodwill $3,681,645,000 Intangible assets, net $255,870,000 c. Intangibles are recorded at historical cost and amortized over their useful lives or their legal lives, whichever is shorter. Goodwill is a type of […]

978-1133188797 Chapter 4 Thomson ONE Solution

Thomson One; Chapter 4 Page 1 of 1 Thomson ONE solutions 13e Chapter 4 THOMSON ONE This Thomson ONE exercise provides for a review of key income statement data for Merck & Company. The trend will change as Thomson ONE […]

978-1133188797 Chapter 4 To the Net

Chapter 04 77 TO THE NET c. Equity earnings (losses) are the investor’s proportionate share of the investee’s earnings (losses). 2. a. Net sales $34,204,000,000 (2010); $24,509,000,000 (2009); $19,166,000,000 (2008) b. Income from operations $1,406,000,000 (2010); $1,129,000,000 (2009); $842,000,000 (2008) […]

978-1133188797 Chapter 5 Thomson ONE Solution

Thomson One; Chapter 5 Page 1 of 2 Thomson ONE solutions 13e Chapter 5 THOMSON ONE 1. This Thomson ONE exercise provides for a review of common-size balance sheet and income statement of the Merck & Company. 2. This Thomson […]

978-1133188797 Chapter 5 To the Net

Chapter 05 1 To The Net 1. ALEXANDER & BALDWIN, INC. CONSOLIDATED STATEMENTS OF INCOME (In millions, except per-share amounts) Years Ended December 31 In Millions 2010 2009 2008 (In millions) Operating revenue: Ocean transportation $1,040 $887 $1,021 Logistics services […]

978-1133188797 Chapter 6 Thomson ONE Solution

Thomson One; Chapter 6 Page 1 of 2 Thomson ONE solutions Chapter 6 THOMSON ONE 1. This Thomson ONE exercise provides for a comment on the trend in selected liquidity ratios for the Boeing Company. 2. This Thomson ONE exercise […]

978-1133188797 Chapter 6 To the Net

Chapter 06 128 TO THE NET 1. a. 1. Quaker develops, produces, and markets a broad range of formulated services (“CMS”). 2. Current ratio December 31 2010 2009 Total current assets (a) $215,482,000 $199,174,000 Total current liabilities (b) $101,191,000 $100,180,000 […]

978-1133188797 Chapter 7 Thomson ONE Solution

Thomson One; Chapter 7 Page 1 of 2 Thomson ONE solutions 13e Chapter 7 THOMSON ONE 1. This Thomson ONE exercise provides for comments on debt ratios for Merck & Company, Inc. from the SEC ratios. 2. This Thomson ONE […]

978-1133188797 Chapter 7 To the Net

Chapter 07 188 TO THE NET 1. a. Item 1. Business The Walt Disney Company, together with its subsidiaries, is a diversified and Interactive Media. b. Reporting Period The Company’s fiscal year ends on the Saturday closest to September 30 […]

978-1133188797 Chapter 8 Thomson ONE Solution

Thomson One; Chapter 8 Page 1 of 2 Thomson ONE solutions Chapter 8 THOMSON ONE 1. This Thomson ONE exercise, using Merck & Company, provides for comments on several profitability ratios for the SEC Ratios. 2. This Thomson ONE exercise, […]

978-1133188797 Chapter 8 To the Net

Chapter 08 222 TO THE NET 1. a. Item 1 business Google is a global technology leader focused on improving the ways people connect with information. b. 2008 2009 2010 Revenue 100.0 108.5 134.5 Income from operations 100.0 125.3 156.5 […]

978-1133188797 Chapter 9 Thomson ONE Solution

Thomson One; Chapter 9 Page 1 of 3 Thomson ONE solutions Chapter 9 THOMSON ONE 1. This Thomson ONE exercise, using the Merck & Company, provides for comments on several market factors. These factors include earnings per share forecasts, forward […]

978-1133188797 Chapter 9 To the Net

Chapter 09 TO THE NET 1. Belden a. Earnings per common share (basic and diluted) 2010 2009 2008 Basic income (loss) per share: Continuing operations $ 1.48 $ (0.16) $ (7.09) Discontinued operations (.11) (.37) (1.01) Disposal of discontinued operations […]

978-1133188797 Solution Manual Gibson_Ch01_SM_13e Part 1

1 Chapter 1 Introduction to Financial Reporting QUESTIONS 1- 1. a. The AICPA is an organization of CPAs that prior to 1973 accepted the primary responsibility for the development of generally accepted Accounting Oversight Board was established in 2002. b. […]

978-1133188797 Solution Manual Gibson_Ch01_SM_13e Part 2

11 CASES CASE 1-1 STANDARD-SETTING: “A POLITICAL ASPECT“ (This case provides an opportunity to view some of the political aspects of standard setting.) a. The hierarchy of accounting qualities in SFAC No. 2 includes neutrality as one of the verifiable, […]

978-1133188797 Solution Manual Gibson_Ch02_SM_13e Part 1

25 Chapter 2 Introduction to Financial Statements and Other Financial Reporting Topics QUESTIONS 2- 1. a. Unqualified opinion with explanatory paragraph b. Unqualified opinion with explanatory paragraph 2- 2. The responsibility for the preparation and integrity of financial statements rests […]

978-1133188797 Solution Manual Gibson_Ch02_SM_13e Part 2

35 CASES CASE 2-1 THE CEO RETIRES Teaching Note: The CEO Retires (Teaching note prepared by the American Accounting Association) PURPOSE: This case is meant to illustrate that the accounting choices available can be used by management to manipulate the […]

978-1133188797 Solution Manual Gibson_Ch03_SM_13e Part 1

48 Chapter 3 Balance Sheet QUESTIONS 3-1. Assets – Resources of the firm 3-2. 3-3. 3-4. They are listed in order of liquidity, which is the ease with which they can be converted to cash. 3-5. Marketable securities are held […]

978-1133188797 Solution Manual Gibson_Ch03_SM_13e Part 2

58 PROBLEM 3-8 b. The noncontrolling interest share of earnings will be 20% of $50,000, or $10,000. PROBLEM 3-9 a. Preferred Common Year 1 0 0 Year 2 Preferred Cumulative from year 1 10,000 shares x $100 par value = […]

978-1133188797 Solution Manual Gibson_Ch03_SM_13e Part 3

66 CASES CASE 3-1 CONVENIENCE FOODS sheet.) a. 1. The financial statements of the parent and the subsidiary are consolidated. A subsidiary is a company controlled by another company. 2. No. There is noncontrolling interest presented. b. 1. No. Only […]

978-1133188797 Solution Manual Gibson_Ch04_SM_13e Part 1

77 Chapter 4 Income Statement QUESTIONS 4- 1. Extraordinary items are events or transactions that are distinguished by their before extraordinary items. 4- 2. d, f 4- 3. Examples include sales of securities, write-down of inventories, disposal of a product […]

978-1133188797 Solution Manual Gibson_Ch04_SM_13e Part 2

87 PROBLEM 4-13 a. 1. Receipt of cash: Sales, 210,000 ounces x $300 = $ 63,000,000 Cost of goods sold (1), 210,000 ounces x $250 = (52,500,000) Gross profit $ 10,500,000 Selling expenses (2,000,000) Administrative expenses (1,250,000) Profit before taxes […]

978-1133188797 Solution Manual Gibson_Ch05_SM_13e Part 1

100 Chapter 5 Basics of Analysis QUESTIONS 5 – 1. A ratio is a fraction comparing two numbers. Ratios make the comparisons in 5 – 2. a. Liquidity is the ability to meet current obligations. Short-term creditors such as banks […]

978-1133188797 Solution Manual Gibson_Ch05_SM_13e Part 2

110 Problem 5-3 Continued (In Percentage) Liabilities and Stockholders’ Equity 2010 2009 Current liabilities: Short-term borrowings and current portion of long- term debt 5.8 6.1 Accounts payable and accrued liabilities 13.3 13.9 Accrued payroll and related taxes 17.8 15.9 Accrued […]

978-1133188797 Solution Manual Gibson_Ch06_SM_13e Part 1

128 Chapter 6 Liquidity of Short-term Assets: Related Debt-Paying Ability QUESTIONS 6- 1. In the very short run, the procedure of making more funds available by slowing creditors would demand payment and they may refuse to sell to our firm […]

978-1133188797 Solution Manual Gibson_Ch06_SM_13e Part 2

138 PROBLEM 6-5 a. 365 days = 365 = 10.14 times per year Accounts receivable turnover in days 36 b. 365 days = 30.42 days 12.0 times per year c. Gross Receivables = $280,000 = 47.36 days Net Sales/365 $2,158,000/365 […]

978-1133188797 Solution Manual Gibson_Ch06_SM_13e Part 3

148 d. Days’ Sales in Receivables: Gross Receivables = $50,000 = 4.56 days Net Sales/365 $4,000,000/365 e. Days’ Sales in Inventory: Ending Inventory = $400,000 = 81.11 days Cost of Goods Sold/365 $1,800,000/365 f. The days’ sales in receivables and […]

978-1133188797 Solution Manual Gibson_Ch06_SM_13e Part 4

7. Operating Cycle = Accounts Receivable Turnover in Days + Inventory Turnover in Days 2011: 54.75 + 60.18 = 114.93 2010: 51.70 + 59.55 = 111.25 2009: 55.58 + 65.33 = 120.91 2008: 56.10 + 66.70 = 122.80 158 2007: […]

978-1133188797 Solution Manual Gibson_Ch06_SM_13e Part 5

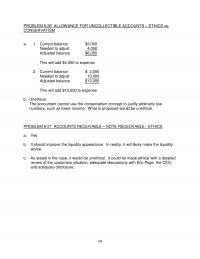

168 CONSERVATISM a. 1. Current balance $2,000 Needed to adjust 4,050 Adjusted balance $6,050 This will add $4,050 to expense 2. Current balance $ 2,000 Needed to adjust 10,000 Adjusted balance $12,000 This will add $10,000 to expense b. Unethical […]

978-1133188797 Solution Manual Gibson_Ch06_SM_13e Part 6

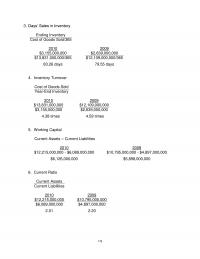

176 3. Days’ Sales in Inventory Ending Inventory Cost of Goods Sold/365 2010 2009 $3,155,000,000 $2,639,000,000 $13,831,000,000/365 $12,109,000,000/365 83.26 days 79.55 days 4. Inventory Turnover Cost of Goods Sold Year-End Inventory 2010 2009 $13,831,000,000 $12,109,000,000 $3,155,000,000 $2,639,000,000 4.38 times 4.59 […]

978-1133188797 Solution Manual Gibson_Ch07_SM_13e Part 1

188 Chapter 7 Long-Term Debt-Paying Ability QUESTIONS 7- 1. Yes, profitability is important to a firm’s long-term, debt– paying ability. ability of the entity to meet its long-run obligations, the major emphasis when determining the long-term, debt-paying ability is on […]

978-1133188797 Solution Manual Gibson_Ch07_SM_13e Part 2

198 3. Debt/Equity Ratio = Total Liabilities Stockholders’ Equity $193,000 = 47.4% $407,000 4. Debt to Tangible Net Worth Ratio = Total Liabilities Tangible Net Worth $193,000 = 49.9% $407,000 – $20,000 b. New asset structure for all plans: Assets […]

978-1133188797 Solution Manual Gibson_Ch07_SM_13e Part 3

207 CASES CASE 7-1 OUTSOURCED SERVICES (This case provides an opportunity to review capitalized interest.) a. 2010 2009 Income statement interest expense $ 40,707,000 $ 28,518,000 Capitalized interest 4,100,000 4,900,000 Total interest $ 44,807,000 $ 33,418,000 b. 2010 2009 2008 […]

978-1133188797 Solution Manual Gibson_Ch08_SM_13e Part 1

222 Chapter 8 Profitability QUESTIONS 8- 1. Profits can be compared to the sales from which they are the residual. They can in different directions, depending on the base. 8- 2. Extraordinary items are by nature nonrecurring. They should be […]

978-1133188797 Solution Manual Gibson_Ch08_SM_13e Part 2

232 5. Operating Income Margin = Operating Income Net Sales 2011 2010 2009 (2) Net sales $ 1,600,000 $ 1,300,000 $ 1,200,000 Less: Material and manufacturing costs of products sold 740,000 624,000 576,000 Research and development 90,000 78,000 71,400 General […]

978-1133188797 Solution Manual Gibson_Ch08_SM_13e Part 3

PROBLEM 8-11 Net Profit Retained Earnings Total Stockholders’ Equity a. A stock dividend is declared and paid. b. Merchandise is purchased on credit. c. Marketable securities are sold above cost. d. Accounts receivable are collected. e. A cash dividend is […]

978-1133188797 Solution Manual Gibson_Ch08_SM_13e Part 4

252 12. Return on Common Equity = Net Income Before Nonrecurring Items – Preferred Dividends Average Common Equity Average Balance Sheet Figures 2011: $72,700 – $6,400 – $6,300 = 13.36% ($520,000 – $70,000 + $518,000 – $70,200)/2 2010: $64,900 – […]

978-1133188797 Solution Manual Gibson_Ch08_SM_13e Part 5

262 5. Return on Operating Assets = Operating Income Year-End Operating Assets 2010 2009 $437,975 $284,349 ($1,161,519 + $1,886,130 + $99,156) ($1,055,380 + $1,897,853+ $91,000) $3,146,805 $3,044,233 13.92% 9.34% 6. Sales to Fixed Assets = Net Sales Year-End Fixed Assets […]

978-1133188797 Solution Manual Gibson_Ch08_SM_13e Part 6

268 CASE 8-6 RETURN ON ASSETS – INDUSTRY COMPARISON Assets.) a. Johnson & Johnson 1. Net Profit Margin = Net Income Before Noncontrolling Interest Equity Income and Nonrecurring Items Net Sales $13,334 = 21.65% $61,587 2. Total Asset Turnover = […]

978-1133188797 Solution Manual Gibson_Ch09_SM_13e Part 1

277 Chapter 9 For the Investor QUESTIONS stock during an accounting period. 9- 2. The Financial Accounting Standards Board suspended the reporting of earnings per share for nonpublic companies. 9- 3. Keller & Fink is a partnership. Earnings per share […]

978-1133188797 Solution Manual Gibson_Ch09_SM_13e Part 2

287 PROBLEM 9-9 a. Numerator Denominator Net income $ 200,000 Preferred dividends (10,000) Common shares outstanding on January 1 20,000 shares Common stock issue on July 1, 5,000 shares 2,500 (5,000 x ½) Weighted average 22,500 Two-for-one stock split on […]

978-1133188797 Solution Manual Gibson_Ch09_SM_13e Part 3

297 Fiscal year ended October 3, 2009 statements – September 27, 2008 $5.78 Fiscal year ended October 2, 2010 statements – September 27, 2008 $5.80 c. September 7, 2008 1. October 2, 2010 statements September 27, 2008 88,454 2. October […]

978-1133188797 Solution Manual Gibson_Ch10_SM_13e Part 1

312 Chapter 10 Statement of Cash Flows QUESTIONS 10– 1. The basic justification for a statement of cash flows is that the balance sheet and the income statement do not adequately indicate changes in cash. obtained this way. The income […]

978-1133188797 Solution Manual Gibson_Ch10_SM_13e Part 2

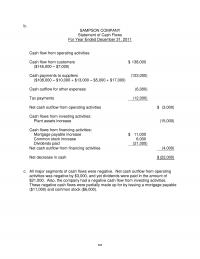

322 b. SAMPSON COMPANY Statement of Cash Flows For Year Ended December 31, 2011 Cash flow from operating activities: Cash flow from customers $ 138,000 ($145,000 – $7,000) Cash payments to suppliers (123,000) ($108,000 – $10,000 + $13,000 – $5,000 […]

978-1133188797 Solution Manual Gibson_Ch10_SM_13e Part 3

PROBLEM 10-11 a. 1 Tightening of credit by suppliers could lead to cash flow problems. b. 5 For a profitable firm, a substantial decrease in receivables would not contribute to bankruptcy. c. 5 Change in notes payable to bands is […]

978-1133188797 Solution Manual Gibson_Ch10_SM_13e Part 4

341 CASE 10-4 THE RETAIL MOVER a. 1. 2007 2008 2011 Total current assets $ 628,408,895 $ 719,478,441 $ 1,044,689,000 Total current liabilities 366,718,656 458,999,682 661,058,000 Working capital 261,690,239 260,478,759 383,631,000 Working capital was fairly constant between 2007 and 2008. […]

978-1133188797 Solution Manual Gibson_Ch11_SM_13e Part 1

354 Chapter 11 Expanded Analysis QUESTIONS 11– 1. Based on the study reported in the text, liquidity and debt ratios are regarded 11– 2. (a) Debt/equity, current ratio (b) Debt/equity, current ratio 11– 3. The dividend payout ratio does not […]

978-1133188797 Solution Manual Gibson_Ch11_SM_13e Part 2

364 7. Acid-Test Ratio = Cash Equivalents + Marketable Securities + Accounts Receivable Current Liabilities $64,346 + $99,021 = 2.22 $73,730 8. Cash Ratio = Cash Equivalents + Marketable Securities Current Liabilities $64,346 = 0.87 $73,730 Debt: 1. Debt Ratio […]

978-1133188797 Solution Manual Gibson_Ch11_SM_13e Part 3

374 (15) Land, Buildings, and Equipment: Let: A = land, buildings, and equipment D = accumulated depreciation N = net fixes assets A – D = N A – [(A/3*)] = $195,000 x 2/3A = $195,000 A = $292,500 *From […]

978-1133188797 Solution Manual Gibson_Ch11_SM_13e Part 4

384 c. No. Return on average assets before interest and taxes (third goal) is equal to return on sales before interest and taxes (first goal) times turnover of average assets (second goal). If Calcor Company achieved the first two goals, […]

978-1133188797 Solution Manual Gibson_Ch11_SM_13e Part 5

394 CASE 11-4 BOOKS UNLIMITED (Part 1) a. Liquidity Ratios 1. Days’ Sales in Inventory = Ending Inventory Cost of Goods Sold/365 2009 $915,200,000 = $915,200,000 = 134.44 days $2,484,800,000/365 $6,807,671 2008 $1,242,000,000 = $1,242,000,000 = 169.89 days $2,668,300,000/365 $7,310,410 […]

978-1133188797 Solution Manual Gibson_Ch11_SM_13e Part 6

400 CASE 11-5 BOOKS UNLIMITED (Part 2) (This case provides the opportunity to review Borders Group, Inc. per the 10-K for the fiscal year ended January 29, 2011.) This comment is included in Note 1: On February 16, 2011 (the […]

978-1133188797 Solution Manual Gibson_Ch12_SM_13e Part 1

409 Chapter 12 Special Industries: Banks, Utilities, Oil and Gas, Transportation, Insurance, Real Estate Companies QUESTIONS 12– 1. Interest income, service charges, and earnings in investments are the main sources of revenue for banks. 12– 2. Loans are assets because […]

978-1133188797 Solution Manual Gibson_Ch12_SM_13e Part 2

419 b. The operating ratio decreased, indicating improved efficiency. Funded debt to Percent earned to operating property increased, indicating improved profitability. Operating revenue to operating property increased slightly, indicating improved profitability. c. Cash flow per share has increased much more […]

978-1133188797 Solution Manual Gibson_Ch12_SM_13e Part 3

426 b. Horizontal Common-Size For the Years Ended December 31 Total United States Europe Africa Asia and other 2010 Sales and other operating revenues Unaffiliated customers Inter-company Total revenues 100.0 100.0 100.0 26.9 100.0 28.1 26.2 —— 25.7 32.0 —— […]

978-1133188797 Solution Manual Gibson_Ch13_SM_13e Part 1

436 Chapter 13 Personal Financial Statements and Accounting for Governments and Not-For-Profit Organizations QUESTIONS 13– 1. Personal financial statements may be prepared for an individual, a husband and wife, or a larger family group. 13– 3. No. 13– 4. No. […]

978-1133188797 Solution Manual Gibson_Ch13_SM_13e Part 2

446 PROBLEM 13-8 a. City of Toledo Revenues – Business-Type Activities Charge for Services Vertical Common-Size Business-type activities: 2003 2004 2005 2006 2007 2008 2009 2010 Charges for services: Water 36.9 37.5 36.6 35.5 35.2 32.2 32.1 32.9 Sewer 40.0 […]

FC 204 Test 1

1) Accounting policies that result in the fastest reporting of income are the most conservative. 2) The principal of fiduciary funds may be distributed. Answer: F 3) In order to compute gross profit margin, the income statement must be in […]

FC 272 Quiz 2

1) Presently, no regulatory agency, such as the Securities and Exchange Commission or the Financial Accounting Standards Board, accepts responsibility for determining either the content of financial ratios or the format of presentation in annual reports. 2) An adverse opinion […]

FC 390 Test 1

1) Under the allowance method, the charge off of a specific account receivable does not influence the income statement nor the net receivable on the balance sheet at the time of the charge off. 2) Among the many responsibilities of […]

FC 398

1) A profitable utility will maintain a high operating ratio. 2) It would always be conservative to value inventory at market. Answer: F 3) The cash ratio is usually a good indication of the liquidity of the firm. Answer: F […]

FC 408 Test 1

1) Stock appreciation rights give the employee compensation at a future date, based on the market price at the date of exercise in excess of a pre-established dollar market. 2) The stockholders’ equity section of an insurance company will usually […]

FC 492 Quiz 2

1) It is generally perceived that utilities that have cash flow problem will not be increasing their dividend. 2) A service firm will usually have a low amount of inventory, consisting primarily of supplies. Answer: T 3) Interim reports are […]

FC 797 Test 2

1) Relevance and reliability are two primary qualities that make accounting information useful for decision making. 2) Ethics can be a particular problem with financial reports. Answer: T 3) In analysis of income, for purposes of determining a trend, extraordinary […]

FC 838

1) Ideally, a proposed comprehensive budget should be compared with financial ratios that have been agreed upon as part of the firm’s corporate objectives. 2) In practice, some of the required information in the 10-K is incorporated by reference. Answer: […]

FE 163 Test 2

1) Return on investment will typically be lower than return on equity. 2) Dissimilar year ends will have no impact on the results of ratios. Answer: F 3) The rating for an industrial revenue bond represents the probability of default […]

FE 244 Midterm 1

1) The market will not be efficient if it does not have access to relevant information or if fraudulent information is provided. 2) To get a better indication of a firm’s ability to cover interest payments in the long run, […]

FE 419 Midterm 1

1) When preferred stock has a preference as to dividends, the current year’s preferred dividend must be paid before a dividend can be paid to common stockholders. 2) The statement of changes in net worth is presented in terms of […]

FE 587 Test 2

1) The audit opinion of a public company is similar to an opinion for a private company except for the public company comments will be added as to the effectiveness of internal control over financial reporting. 2) Stock appreciation rights […]

FE 592

1) Current assets are assets that (1) are in the form of cash, (2) will be realized in cash, or (3) conserve the use of cash within the operating cycle of a business or for one year, whichever is shorter. […]

FE 810 Quiz 1

1) For a business combination, the purchase method views the business combination as the acquisition of one entity by another. The firm doing the acquiring records the identifiable assets and liabilities at fair value at the date of acquisition. 2) […]

FE 829

1) Retained earnings always shows a positive balance. 2) Nonrecurring items such as extraordinary income and disposal of a segment require separate earnings per share disclosure. Answer: T 3) Relevance is a quality requiring that the information be timely and […]

FIN 252 Midterm 2

1) Generally accepted accounting principles and the Internal Revenue Code of tax law require that the same depreciation method be used for both the financial statements and the federal tax return. 2) The financial literature and valuation books strongly support […]

FIN 266 Midterm

1) A quasi-reorganization is an accounting procedure equivalent to an accounting fresh start. 2) Contingent liabilities are recorded as a liability only if the loss is considered substantial and the amount is reasonably determinable. Answer: F 3) Working capital is […]

Fin 269 1 Loans to deposits for a

1) Loans to deposits for a bank is a type of debt coverage ratio. 2) Cash flow per share can be viewed as a substitute for earnings per share in terms of a firm’s profitability. Answer: F 3) Cash flow […]

FIN 292 Quiz 1

1) Noncontrolling interest relects income from ownership of noncontrolling shareholders in the equity of consolidated subsidaries less than wholly owned. 2) The principal asset of a merchandising firm will usually be accounts receivable. Answer: F 3) There are three methods […]

FIN 321 Midterm 2

1) In the ratio funded debt to operating property for a utility, construction in progress is a component of operating property. 2) For a public company, the SEC requires that a report be filed annually on its internal control systems. […]

FIN 391

1) Accounting Trends & Techniques is a compilation of data obtained by a survey of annual reports to stockholders undertaken for the purpose of analyzing the accounting information disclosed in such reports. 2) A firm might have a low dividend […]

FIN 463 Quiz 3

1) Some industry practices lead to accounting reports that do not conform to the general theory that underlies accounting. 2) Dividend yield relates dividends per share to market price per share. Answer: T 3) The financial statements of legally separate […]

FIN 535 Homework

1) The accrual basis needs numerous adjustments at the end of the accounting period. 2) In 2007, the Securities and Exchange Commission announced that it would accept financial statements from foreign private issues without reconciliation to U.S. GAAP if they […]

FIN 566 Midterm 2 1 Web sites are

1) Web sites are not very useful when performing analysis. 2) The statement of cash flows should be reviewed for several time periods in order to determine the major sources of cash and the major uses of cash. Answer: T […]

FIN 612 Quiz 2

1) A decline in the acid-test ratio indicates a reduced ability to pay current liabilities with funds from the sale of inventory. 2) To the extent that money does not remain stable, it loses its usefulness as the standard for […]

Fin 612 Test 2

1) Operating assets exclude investments, land, and intangibles from the asset base. 2) The Governmental Accounting Standards Board is a branch of the Financial Accounting Foundation. Answer: T 3) The accrual basis of accounting recognizes revenue when realized (realization concept) […]

Fin 636 Final

1) Gross profit will be a prominent figure on a single-step income statement. 2) If the company closes the year when the activities are at a peak, the number of days’ sales in inventory would tend to be overstated and […]

FIN 731

1) When a firm is expensing an item faster on the tax return than on the financial statements, a deferred tax liability is the result. 2) Accounting standards codification TM reorganizes the accounting pronouncements into approximately 90 accounting topics. Answer: […]

FIN 813 1 Predictive value

1) Predictive value, feedback value, and timeliness are ingredients needed to ensure that the information is reliable. 2) For a statement of financial condition, the figure that will usually be most important is the total asset amount. Answer: F 3) […]