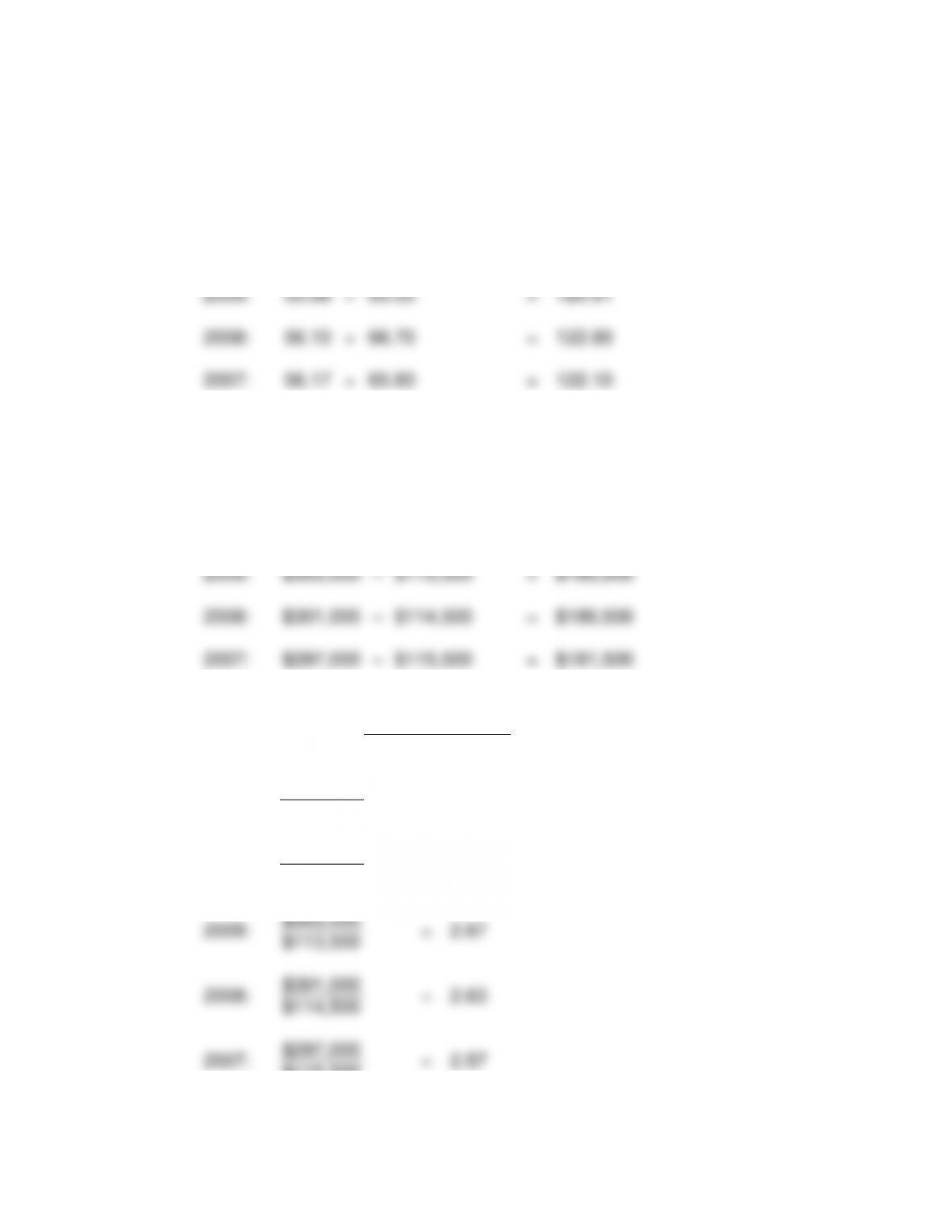

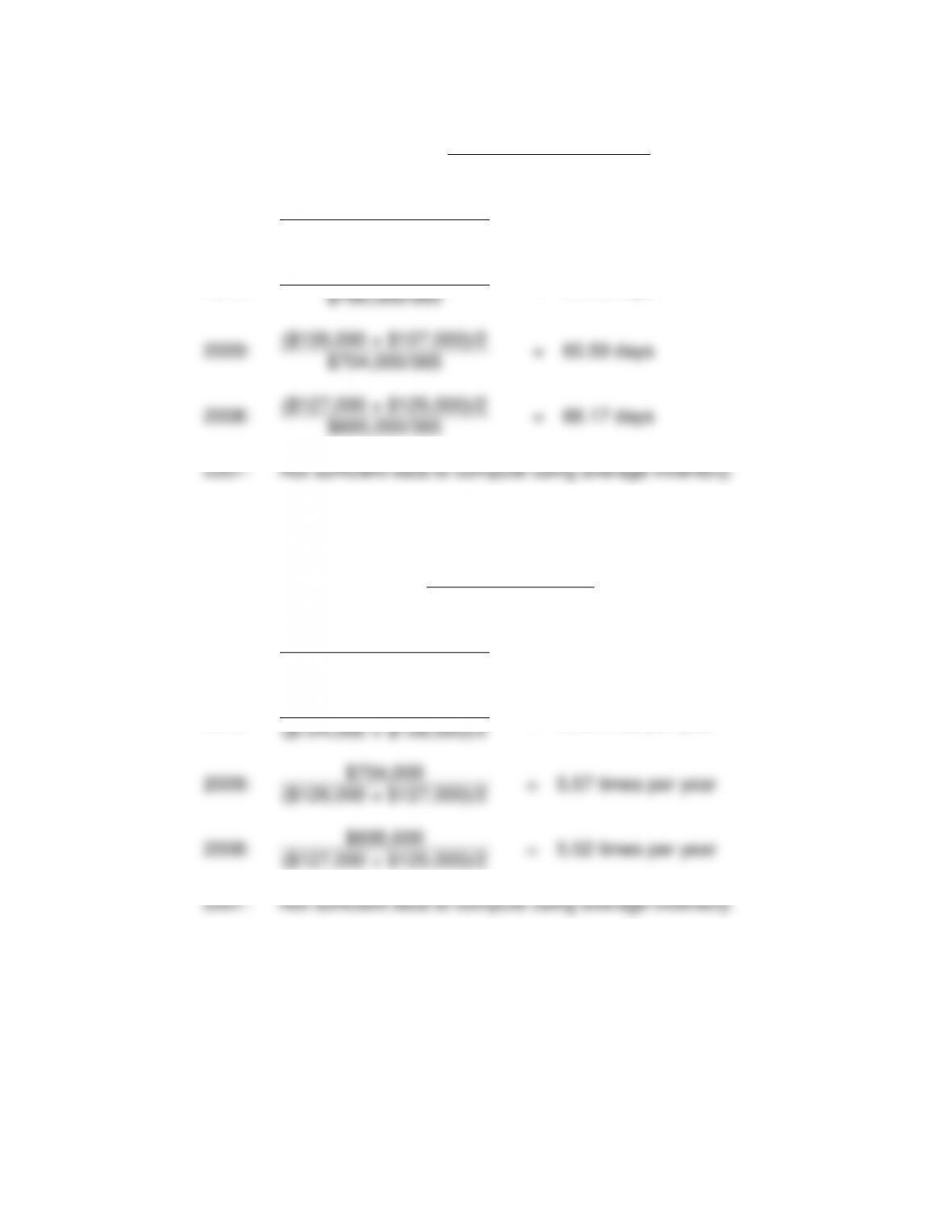

7.

Operating Cycle

=

Accounts Receivable

Turnover in Days

+

Inventory Turnover

in Days

2011:

54.75

+

60.18

=

114.93

2010:

51.70

+

59.55

=

111.25

2009:

55.58

+

65.33

=

120.91

2008:

56.10

+

66.70

=

122.80

Current Assets

2011:

2010:

2009:

2008:

2007:

159

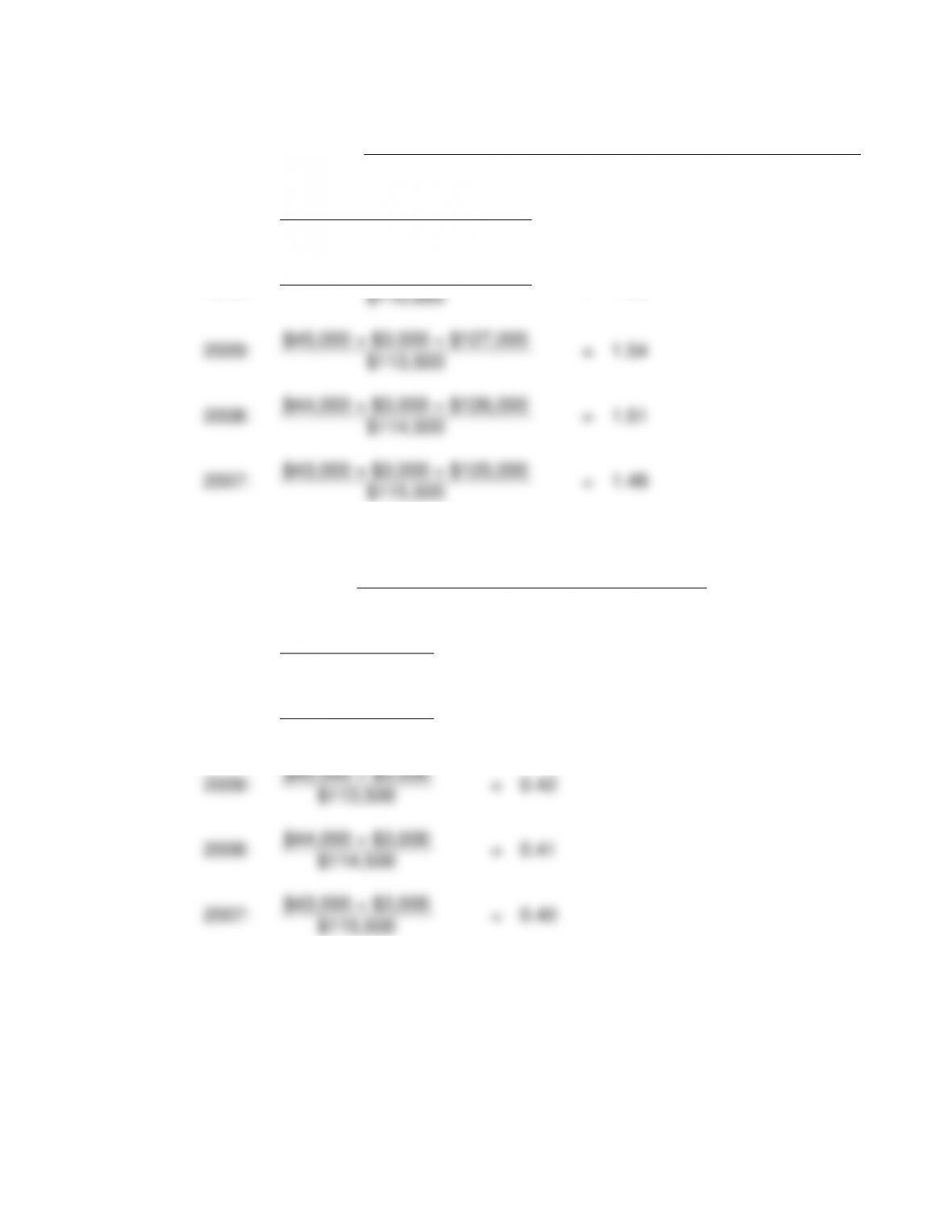

10.

Acid-Test Ratio

=

Cash Equivalents + Marketable Services + Net Receivables

Current Liabilities

2011:

$47,200 + $2,000 + $131,000

=

1.65

$109,500

2010:

$46,000 + $2,500 + $128,000

=

1.60

$110,000

2009:

$45,000 + $3,000 + $127,000

=

1.54

$113,500

2008:

$44,000 + $3,000 + $126,000

=

1.51

$114,500

2007:

$43,000 + $3,000 + $125,000

=

1.48

$115,500

11.

Cash Ratio

=

Cash Equivalents + Marketable Securities

Current Liabilities

2011:

$47,200 + $2,000

=

0.45

$109,500

2010:

$46,000 + $2,500

=

0.44

$110,000

2009:

$45,000 + $3,000

=

0.42

$113,500

2008:

$44,000 + $3,000

=

0.41

$114,500

2007:

$43,000 + $3,000

=

0.40

$115,500

160

12.

Sales to Working Capital

=

Net Sales

Working Capital

2011:

$880,000

=

4.50

$195,700

2010:

$910,000

=

4.72

$193,000

2009:

$840,000

=

4.43

$189,500

2008:

$825,000

=

4.42

$186,500

2007:

$820,000

=

4.52

$181,500

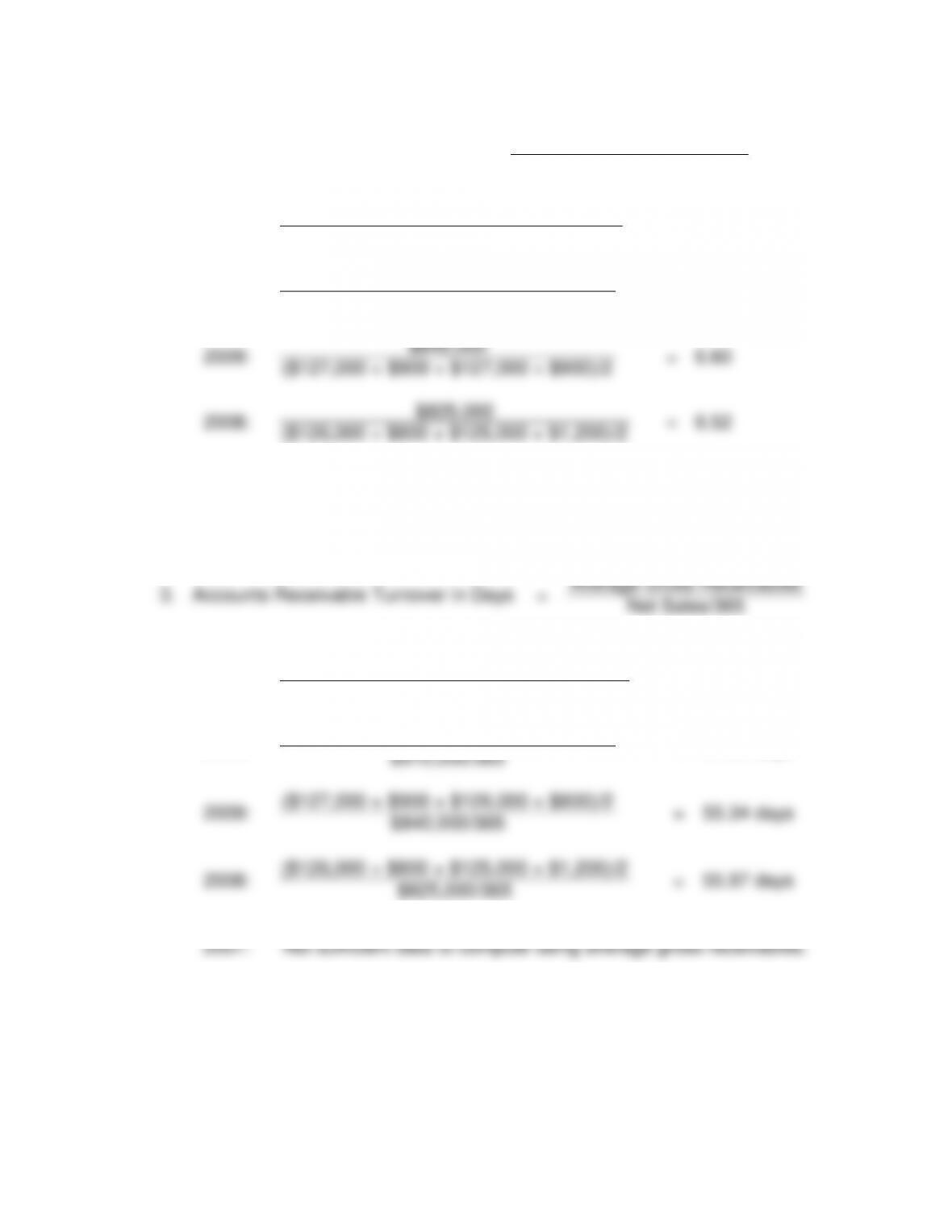

b.

1.

Days’ Sales in Receivables

=

Average Gross Receivables

Net Sales/365

2011:

($131,000 + $1,000 + $128,000 + $900)/2

=

54.11 days

$880,000/365

2010:

($128,000 + $900 + $127,000 + $900)/2

=

51.50 days

$910,000/365

2009:

($127,000 + $900 + $126,000 + $800)/2

=

55.34 days

$840,000/365

2008:

($126,000 + $800 + $125,000 + $1,200)/2

=

55.97 days

$825,000/365

2007:

Not sufficient data to compute using average gross receivables.

161

2.

Accounts Receivable Turnover

=

Net Sales

Average Gross Receivables

2011:

$880,000

=

6.75

(131,000 + $1,000 + $128,000 + $900)/2

2010:

$910,000

=

7.09

($128,000 + $900 + $127,000 + $900)/2

2009:

$840,000

=

6.60

($127,000 + $900 + $127,000 + $900)/2

2008:

$825,000

=

6.52

($126,000 + $800 + $125,000 + $1,200)/2

2007:

Not sufficient data to compute using average gross receivables.

3.

Accounts Receivable Turnover in Days

=

Average Gross Receivables

Net Sales/365

2011:

($131,000 + $1,000 + $128,000 + $900)/2

=

54.11 days

$880,000/365

2010:

($128,000 + $900 + $127,000 + $900)/2

=

51.50 days

$910,000/365

2009:

($127,000 + $900 + $126,000 + $800)/2

=

55.34 days

$840,000/365

2008:

($126,000 + $800 + $125,000 + $1,200)/2

=

55.97 days

$825,000/365

2007:

Not sufficient data to compute using average gross receivables.

162

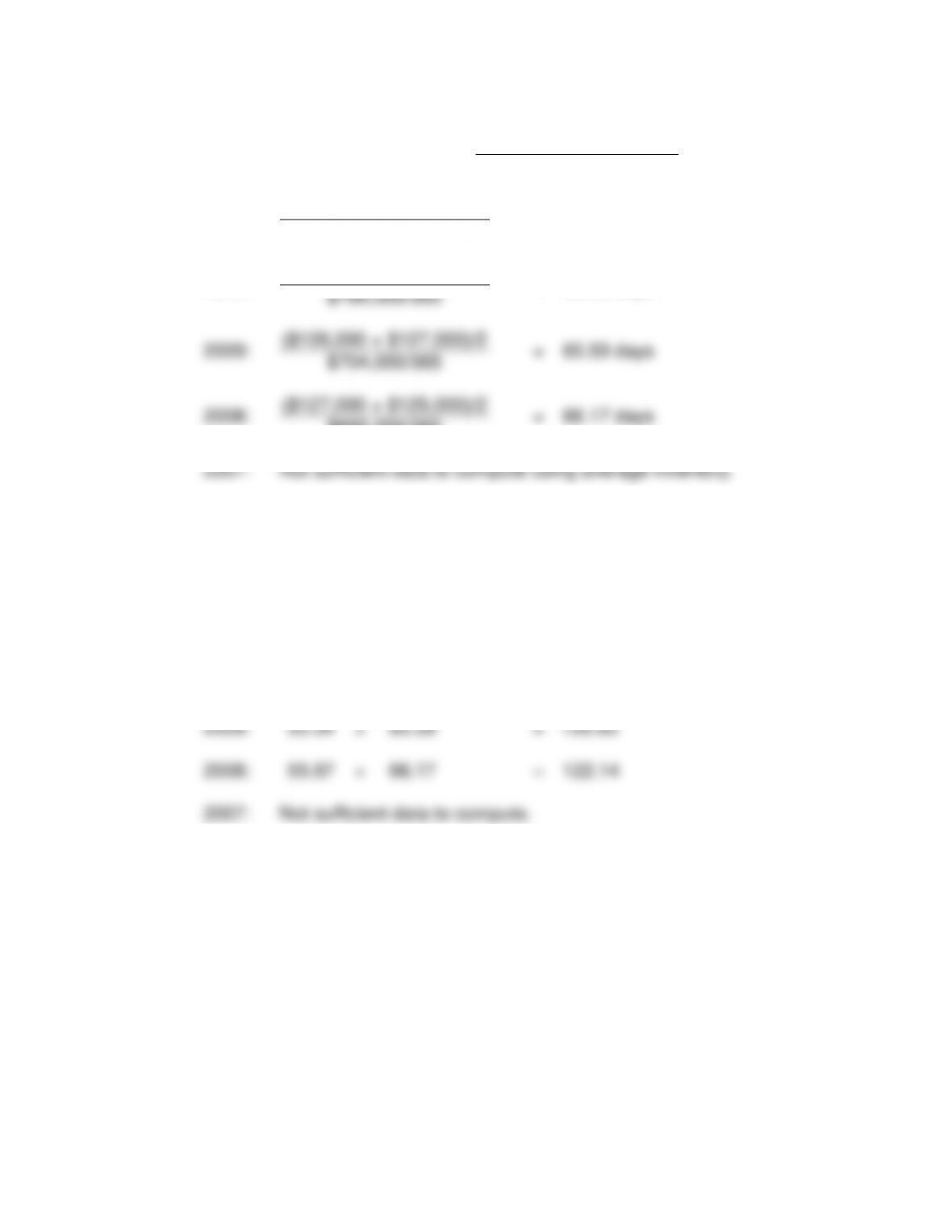

4.

Days’ Sales In Inventory

=

Average Inventory

Cost of Goods Sold/365

2011:

($122,000 + $124,000)/2

=

60.67 days

$740,000/365

2010:

($124,000 + $126,000)/2

=

60.03 days

$760,000/365

2009:

($126,000 + $127,000)/2

=

65.59 days

$704,000/365

2008:

($127,000 + $125,000)/2

=

66.17 days

$695,000/365

2007:

Not sufficient data to compute using average inventory.

5.

Inventory Turnover

=

Cost of Goods Sold

Average Inventory

2011:

$740,000

=

6.02 times per year

($122,000 + $124,000)/2

2010:

$760,000

=

6.08 times per year

($124,000 + $126,000)/2

2009:

$704,000

=

5.57 times per year

($126,000 + $127,000)/2

2008:

$695,000

=

5.52 times per year

($127,000 + $125,000)/2

2007:

Not sufficient data to compute using average inventory.

6.

Inventory Turnover In Days

=

Average Inventory

Cost of Goods Sold/365

2011:

($122,000 + $124,000)/2

=

60.67 days

$740,000/365

2010:

($124,000 + $126,000)/2

=

60.03 days

$760,000/365

($126,000 + $127,000)/2

$704,000/365

($127,000 + $125,000)/2

$695,000/365

8.

Working Capital

=

Average Current Assets

–

Average Current Liabilities

2011:

($305,200 + $303,000)/2

–

($109,500 + $110,000)/2

$304,100

–

$109,750

=

$194,350

2010:

($303,000 + $303,000)/2

–

($110,000 + $113,500)/2

$303,000

–

$111,750

=

$191,250

2009:

($303,000 + $301,000)/2

–

($113,500 + $114,500)/2

2008:

($301,000 + $297,000)/2

–

($114,500 + $115,500)/2

$299,000

–

$115,000

=

$184,000

2007:

Not sufficient data to compute.

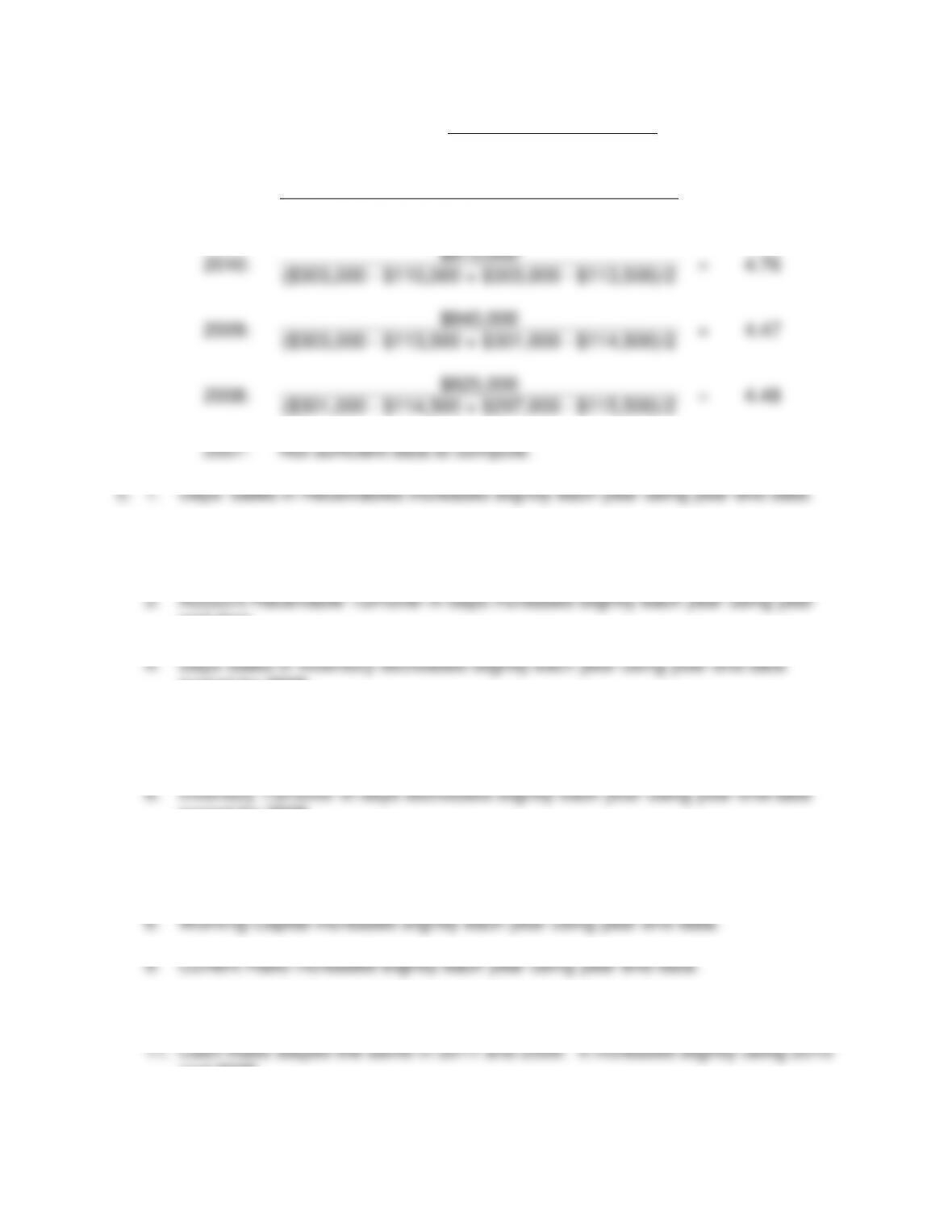

9.

Current Ratio

=

Average Current Assets

Average Current Liabilities

2011:

$304,100

=

2.77

$109,750

2010:

$303,000

=

2.71

$111,750

$302,000

$114,000

$115,000

2007:

Not sufficient data to compute using average inventory.

10.

Acid-Test Ratio

=

Average (Cash Equivalents + Marketable

Securities + Net Receivables)

Average Current Liabilities

2011:

(($47,200 + $2,000 + $131,000) + ($46,000 + $2,500 + $128,000))/2

($109,500 + $110,000)/2

$178,350

=

1.63

$109,750

2010:

(($46,000 + $2,500 + $128,000) + ($45,000 + $3,000 + $127,000))/2

($110,000 + $113,500)/2

$175,750

$111,750

2009:

(($45,000 + $3,000 + $127,000) + ($44,000 + $3,000 + $126,000))/2

($113,500 + $114,500)/2

$174,000

$114,000

2008:

(($44,000 + $3,000 + $126,000) + ($43,000 + $3,000 + $125,000))/2

($114,500 + $115,500)/2

$172,000

=

1.50

$115,000

166

11.

Cash Ratio

=

Average (Cash Equivalents + Marketable Securities)

Average Current Liabilities

2011:

($47,200 + $2,000) + ($46,000 + $2,500)/2

($109,500 + $110,000)/2

$48,850

=

0.45

$109,750

2010:

($46,000 + $2,500) + ($45,000 + 3,000)/2

($110,000 + $113,500)/2

$48,250

=

0.43

$111,750

2009:

($45,000 + $3,000) + ($44,000 + 3,000)/2

($113,500 + $114,500)/2

$47,500

=

0.42

$114,000

2009:

($44,000 + $3,000) + ($43,000 + 3,000)/2

($114,500 + $115,500)/2

$46,500

=

0.40

$115,000

2007:

Not sufficient data to compute using average inventory.

12.

Sales to Working Capital

=

Net Sales

Average Working Capital

2011:

$880,000

=

4.53

($305,200 – $109,500 + $303,000 – $110,000)/2

2010:

$910,000

=

4.76

($303,000 – $110,000 + $303,000 – $113,500)/2

2009:

$840,000

=

4.47

($303,000 – $113,500 + $301,000 – $114,500)/2

$825,000