198

3.

Debt/Equity Ratio

=

Total Liabilities

Stockholders’ Equity

$193,000

=

47.4%

$407,000

4.

Debt to Tangible Net Worth Ratio

=

Total Liabilities

Tangible Net Worth

$193,000

=

49.9%

$407,000 – $20,000

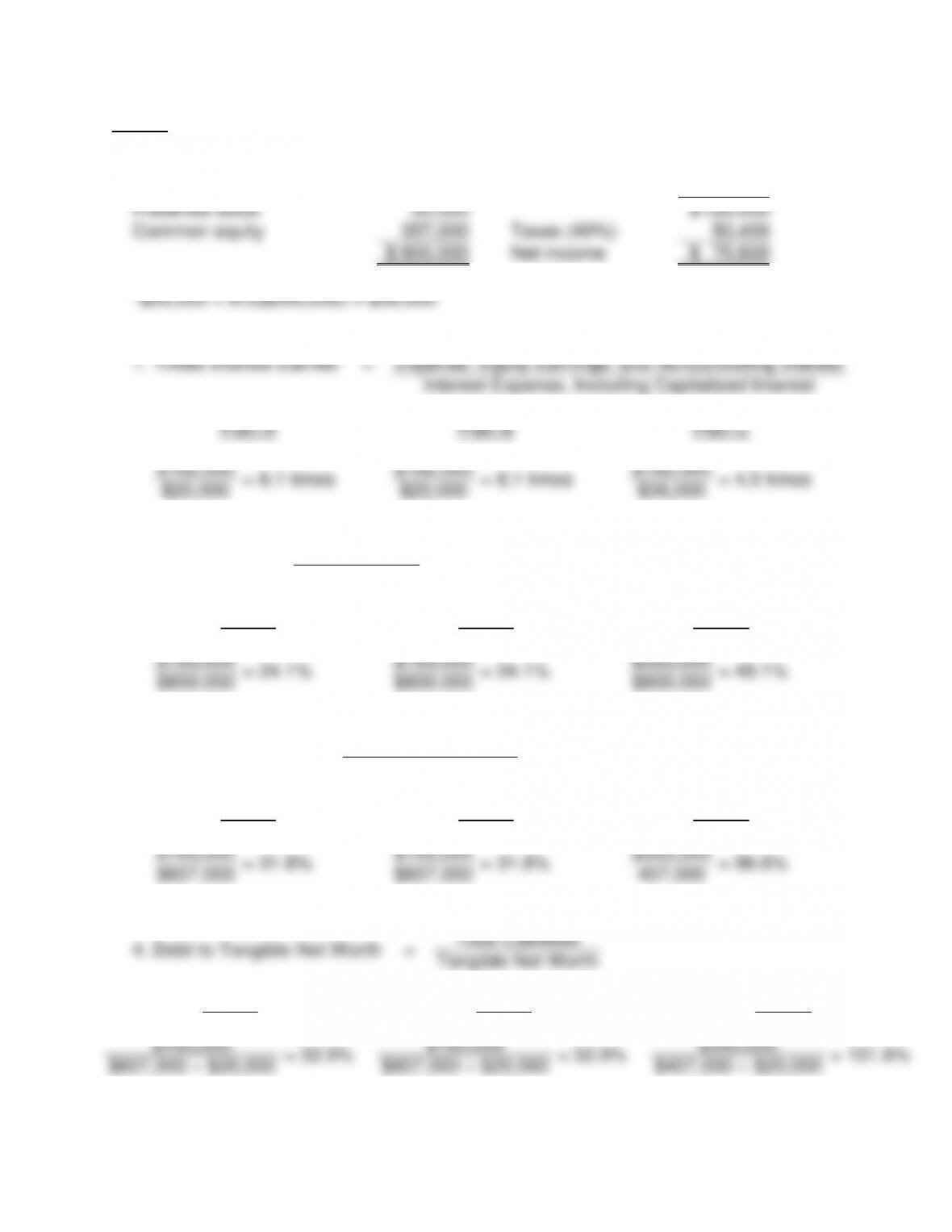

b. New asset structure for all plans:

Assets

Current Assets

$

226,000

Property, plant and equipment

554,000

Intangibles

20,000

Total assets

$

800,000

Liabilities and Equity

Plan A

Current Liabilities

$

93,000

Long-term debt

100,000

Preferred stock

250,000

Common equity

357,000

No change in net income

$

800,000

Plan B

Current Liabilities

$

93,000

Long-term debt

100,000

Preferred stock

50,000

Common stock

120,000

Premium on common stock

300,000

Retained earnings

137,000

No change in net income

$

800,000

199

Plan C

Current liabilities

$

93,000

Operating income

$

162,000

Long-term debt

300,000

Interest expense

36,000

*

Preferred stock

50,000

$

126,000

Common equity

357,000

Taxes (40%)

50,400

$

800,000

Net income

$

75,600

1.

Times Interest Earned

=

Recurring Earnings, Excluding Interest Expense, Tax

Expense, Equity Earnings, and Noncontrolling Interest

Interest Expense, Including Capitalized Interest

Plan A

Plan B

Plan C

$162,000

=

8.1 times

$162,000

=

8.1 times

$162,000

=

4.5 times

$20,000

$20,000

$36,000

2.

Debt Ratio

=

Total Liabilities

Total Assets

Plan A

Plan B

Plan C

$193,000

=

24.1%

$193,000

=

24.1%

$393,000

=

49.1%

$800,000

$800,000

$800,000

3.

Debt/Equity Ratio

=

Total Liabilities

Stockholders’ Equity

Plan A

Plan B

Plan C

$193,000

=

31.8%

$193,000

=

31.8%

$393,000

=

96.6%

$607,000

$607,000

407,000

4.

Debt to Tangible Net Worth

=

Total Liabilities

Tangible Net Worth

Plan A

Plan B

Plan C

$193,000

=

32.9%

$193,000

=

32.9%

$393,000

=

101.6%

$607,000 – $20,000

$607,000 – $20,000

$407,000 – $20,000

200

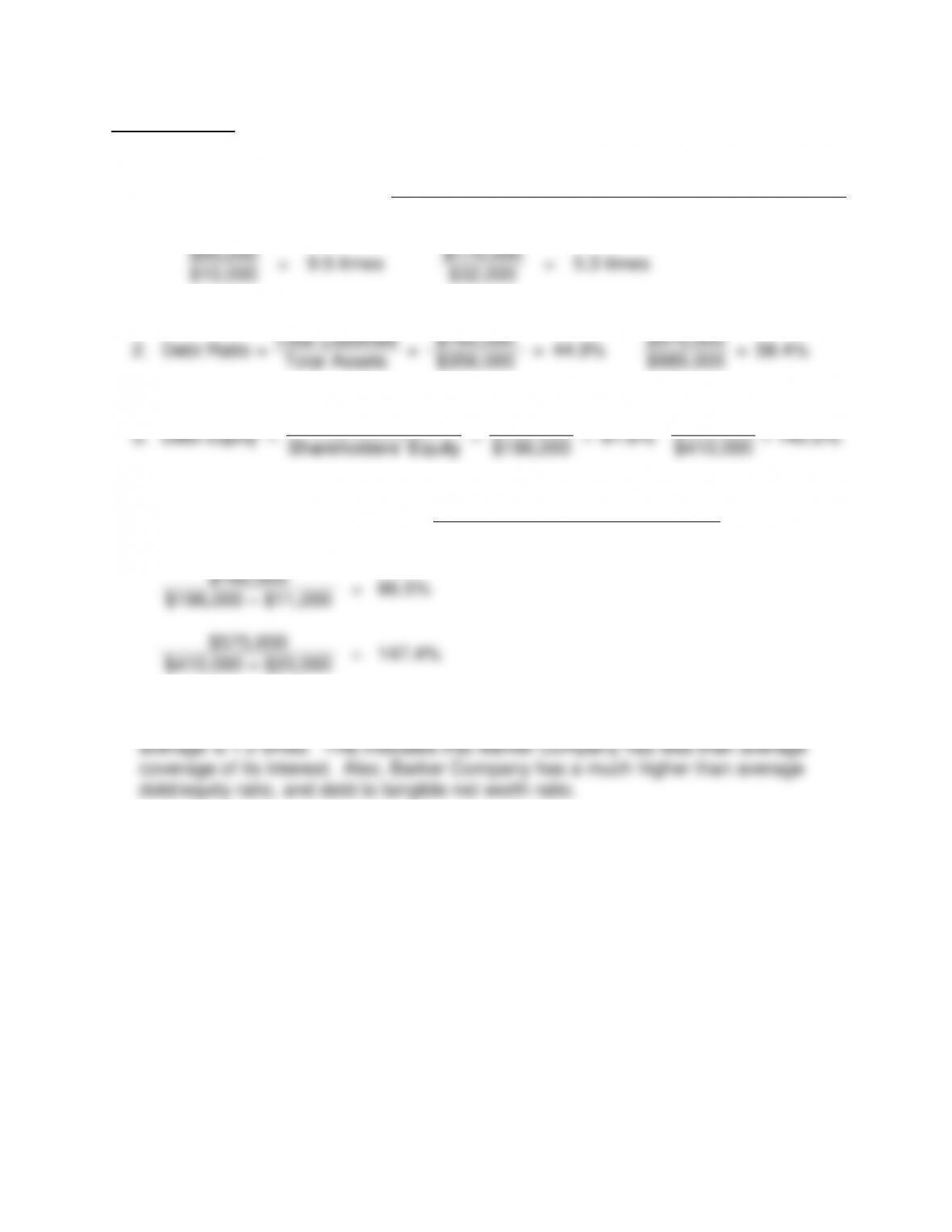

c. Preferred Stock Alternative:

Advantages:

2. Not the absolute reduction in earnings that accompanied the debt alternative.

Debt to Tangible Net Worth Ratio.

of issuing long-term debt.

Disadvantage:

any dividends can be paid to common stockholders.

Common Stock Alternative:

Advantages:

1. No increase in fixed obligations.

3. Not the absolute reduction in earnings that accompanied the debt alternative.

of issuing long-term debt.

Disadvantage:

Long-Term Bonds Alternative:

Advantage:

Disadvantages:

1. Material decline in Times Interest Earned.

Tangible Net Worth Ratio.

201

3. Absolute reduction in earnings.

interest is tax deductible and, therefore, the after-tax cost is 4.8% [8% x (1-.40)(1–

the corporate tax rate)].

necessarily be true with changed assumptions.

PROBLEM 7-8

a.

Times Interest Earned

=

Recurring Earnings, Excluding Interest Expense, Tax

Expense, Equity Earnings, and Noncontrolling Interest

Interest Expense, Including Capitalized Interest

Earnings from continuing operations before

income taxes and equity earnings

Add back interest expense

$

74,780,000

Adjusted earnings

(1) $

37,646,000

(2) $

112,426,000

Times interest earned: [(2) + (1)] 2.99 times per year

b.

Adjusted earnings (see a, above)

$

112,426,000

Plus equity earnings

27,749,000

Interest expense

(1) $

140,175,000

(2) $

37,646,000

interest payments.

202

PROBLEM 7-9

a.

1.

Times Interest Earned

=

Recurring Earnings, Excluding Interest Expense, Tax

Expense, Equity Earnings, and Noncontrolling Interest

Interest Expense, Including Capitalized Interest

$95,000

=

9.5 times

$170,000

=

5.3 times

$10,000

$32,000

2.

Debt Ratio

=

Total Liabilities

=

$160,000

=

44.9%

$575,000

=

58.4%

Total Assets

$356,000

$985,000

3.

Debt Equity

=

Total Liabilities

=

$160,000

=

81.6%

$575,000

=

140.2%

Shareholders’ Equity

$196,000

$410,000

4.

Debt to Tangible Net Worth

=

Total Liabilities

Shareholders’ Equity – Intangibles

$160,000

=

86.5%

$196,000 – $11,000

$575,000

=

147.4%

$410,000 – $20,000

b. No, Barker Company has a times interest earned of 5.3 times while the industry

c. Allen Company has a better times interest earned, debt ratio, debt/equity ratio, and

debt to tangible net worth.

203

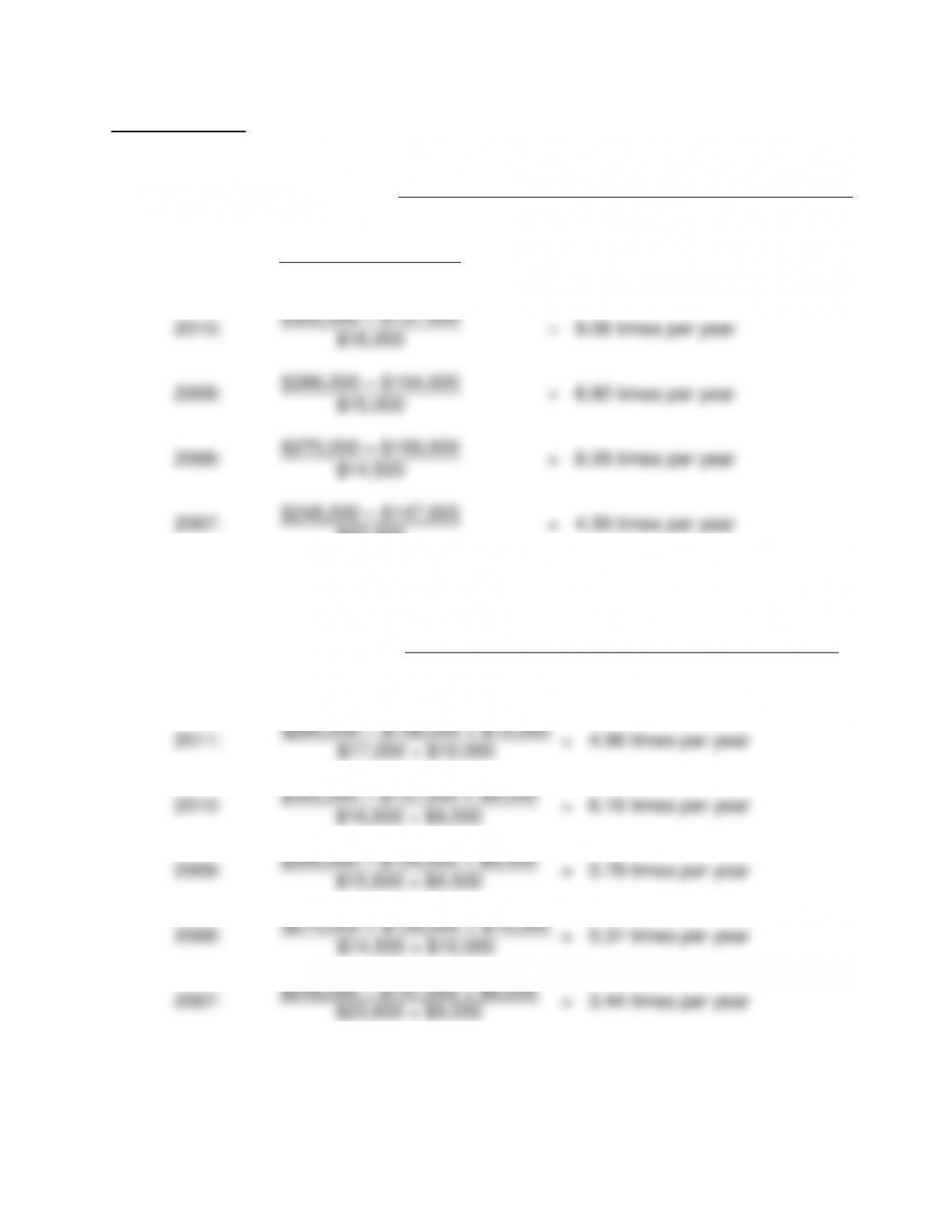

PROBLEM 7-10

a.

1.

Times Interest Earned

=

Recurring Earnings, Excluding Interest Expense, Tax

Expense, Equity Earnings, and Noncontrolling Interest

Interest Expense, Including Capitalized Interest

2011:

$280,000 – $156,000

=

7.29 times per year

$17,000

2010:

$302,000 – $157,000

=

9.06 times per year

$16,000

2009:

$286,000 – $154,000

=

8.80 times per year

$15,000

2008:

$270,000 – $150,000

=

8.28 times per year

$14,500

2007:

$248,000 – $147,000

=

4.39 times per year

$23,000

2.

Fixed Charge Coverage

=

Recurring Earnings, Excluding Interest Expense,

Tax Expense, Equity Earnings, and Noncontrolling

Interest + Interest Portion of Rentals

Interest Expense, Including Capitalized Interest +

Interest Portion of Rentals

2011:

$280,000 – $156,000 + $10,000

=

4.96 times per year

$17,000 + $10,000

2010:

$302,000 – $157,000 + $9,000

=

6.16 times per year

$16,000 + $9,000

2009:

$286,000 – $154,000 + $9,500

=

5.78 times per year

$15,000 + $9,500

2008:

$270,000 – $150,000 + $10,000

=

5.31 times per year

$14,500 + $10,000

2007:

$248,000 – $147,000 + $9,000

=

3.44 times per year

$23,000 + $9,000

204

3.

Debt Ratio

=

Total Liabilities

Total Assets

2011:

$88,000 + $170,000

=

46.07%

$560,000

2010:

$89,500 + $168,000

=

46.48%

$554,000

2009:

$90,500 + $165,000

=

46.14%

$553,800

2008:

$90,000 + $164,000

=

46.31%

$548,500

2007:

$91,500 + $262,000

=

65.83%

$537,000

4.

Debt/Equity Ratio

=

Total Liabilities

Shareholders’ Equity

2011:

$88,000 + $170,000

=

85.43%

$302,000

2010:

$89,500 + $168,000

=

86.85%

$296,500

2009:

$90,500 + $165,000

=

85.65%

$298,300

2008:

$90,000 + $164,000

=

86.25%

$294,500

2007:

$91,500 + $262,000

=

192.64%

$183,500

205

5.

Debt to Tangible Net Worth

=

Total Liabilities

Shareholders’ Equity – Intangible Assets

2011:

$88,000 + $170,000

=

91.49%

$302,000 – $20,000

2010:

$89,500 + $168,000

=

92.46%

$296,500 – $18,000

2009:

$90,500 + $165,000

=

90.83%

$298,300 – $17,000

2008:

$90,000 + $164,000

=

91.20%

$294,500 – $16,000

2007:

$91,500 + $262,000

=

209.79%

$183,500 – $15,000

The debt ratio, debt/equity ratio, and debt to tangible net worth materially improved

between 2007 and 2008 when long-term debt was reduced and funding shifted to

206

PROBLEM 7-11

a.

4

The times interest earned ratio indicates a firm’s long-term debt-paying ability

from the income statement view.

b.

5

Preferred stock is owned by stockholders.

c.

5

The bonds payable liability will be shown on the balance sheet.

d.

5

The denominator of the debt ratio is total assets. Therefore, none of these

assets are subtracted.

e.

5

The current ratio is considered to be a liquidity ratio.

f.

4

The debt/equity ratio represents a balance sheet view of debt.

g.

5

There is not adequate information to form an opinion on the long-term debt

position.

h.

2

With a times interest earned ratio of .20 to 1, net income is less than the

interest expense.

i.

5

Intangible assets are subtracted in the denominator. Land and bonds payable

are not intangible assets.

j.

2

The ratio fixed charge coverage is an income statement indication of debt–

paying ability.

k.

1

The Employee Retirement Income Security Act calls for a company to be

liable for its pension plan up to 30 percent of its net worth.

l.

1

Capitalized interest should be included with interest expense when computing

times interest earned.

m.

3

Minority shareholders’ interest does not represent a definite commitment to

pay out funds in the future.