277

Chapter 9

For the Investor

QUESTIONS

stock during an accounting period.

earnings per share for nonpublic companies.

applies to corporate income statements.

9- 4. Earnings per share is a concept that only applies to common stock. The

ratio.

9- 5. Since earnings pertain to an entire year, they should be related to the common

of the year that if converted those shares would be outstanding during the year

9- 6. Less preferred dividends will be subtracted from net income in the numerator

used to retire the preferred stock in relation to the dividend decrease.

9- 7. Stock dividends and stock splits do not provide the firm with more funds; they

9- 8. Many firms try to maintain a stable percentage because they have a policy on

9- 9. Financial leverage is the use of financing with a fixed charge. Financial

disadvantageous when a firm obtains a lower return on the resources obtained

than the rate of interest expense.

9-10. If the interest rate rises, the degree of financial leverage will rise. For

example, suppose the firm has the following pattern of earnings with

279

9-14. Book value is based on a mixture of valuation basis, such as historical costs.

9-15. Stock options are a form of potential dilution of earnings. With the requirement

will reduce earnings each year.

9-16. A relatively small number of stock appreciation rights can prove to be a

9-17. If the stock price decreases in relation to the prior year, then the estimate of

total compensation expense related to the stock appreciation rights will

280

PROBLEMS

PROBLEM 9-1

Degree of Financial Leverage

=

Earnings Before Interest, Tax, Noncontrolling

Interest, Equity Income and Nonrecurring Items

Earnings Before Tax, Noncontrolling Interest,

Equity Income, and Nonrecurring Items

$975,000 + $70,000

=

$1,045,000

=

1.07

$975,000

$975,000

PROBLEM 9-2

a.

Degree of Financial Leverage

=

Earnings Before Interest, Tax

Noncontrolling Interest, Equity Income,

and Nonrecurring Items

Earnings Before Tax, Noncontrolling

Interest, Equity Income, and

Nonrecurring Items

=

$1,000,000

$800,000

=

1.25

b.

Prior earnings before interest and tax

$

1,000,000

10% increase

100,000

Adjusted income before interest and tax

$

1,100,000

Interest

200,000

Income before tax

$

900,000

Tax (50% rate)

450,000

Net income

450,000

Earnings will increase by 12.5% to $450,000

($400,000 x 112.5% = $450,000)

c.

$

800,000

Earnings before interest and tax

200,000

Interest

600,000

Earnings before tax

300,000

Tax

$

300,000

Net Income

281

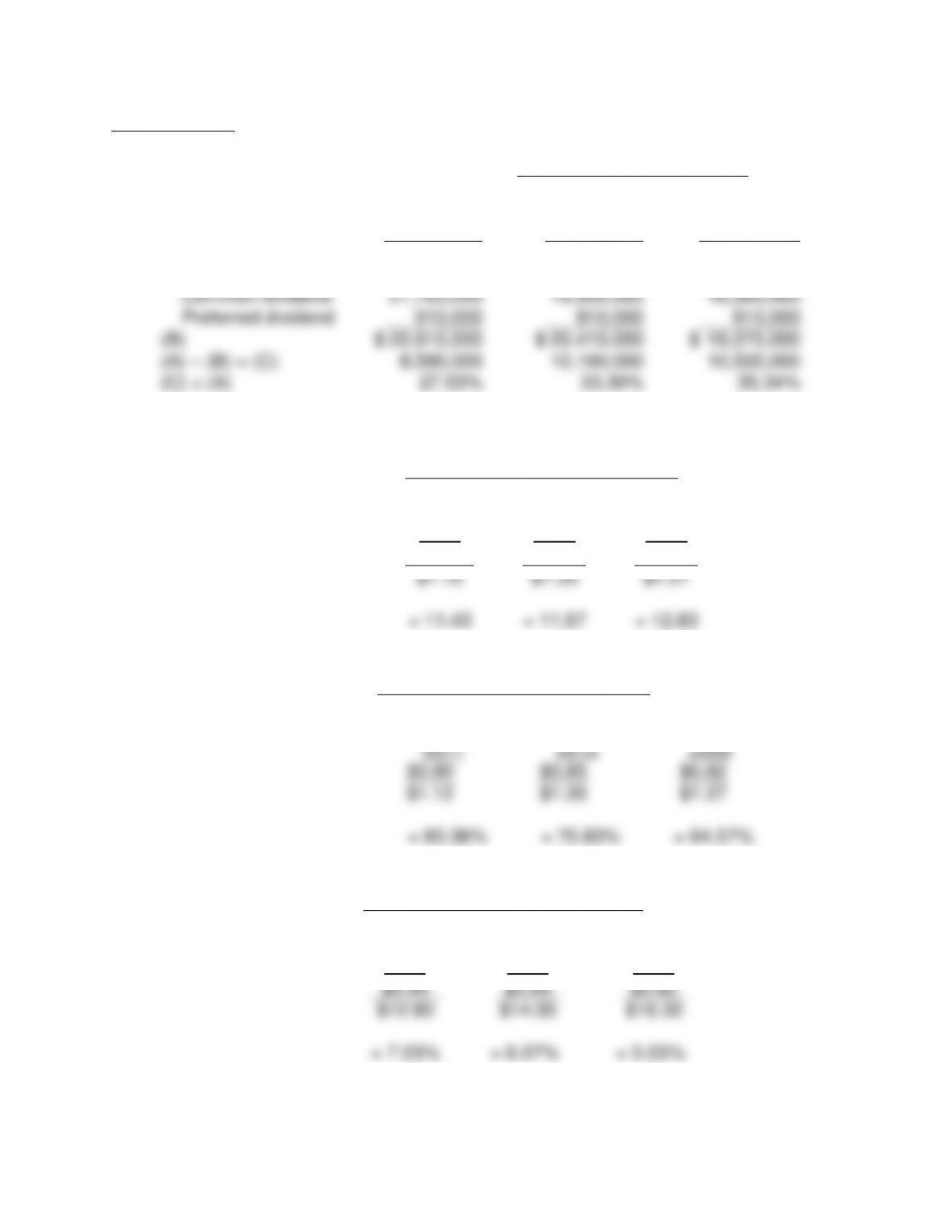

PROBLEM 9-3

a.

1.

Percentage of Earnings Retained

=

Net Income – All Dividends

Net Income

2011

2010

2009

Net income (A)

$

31,200,000

$

30,600,000

$

29,800,000

Less:

Common dividend

21,700,000

19,500,000

18,360,000

Preferred dividend

910,000

910,000

910,000

(B)

$

22,610,000

$

20,410,000

$

19,270,000

(A) – (B) = (C)

8,590,000

10,190,000

10,530,000

(C) ÷ (A)

27.53%

33.30%

35.34%

2.

Price/Earnings Ratio

=

Market Price Per Share

Fully Diluted Earnings Per Share

2011

2010

2009

$12.80

$14.00

$16.30

$1.12

$1.20

$1.27

= 11.43

= 11.67

= 12.83

3.

Dividend Payout

=

Dividends Per Common Share

Fully Diluted Earnings Per Share

2011

2010

2009

$0.90

$0.85

$0.82

$1.12

$1.20

$1.27

= 80.36%

= 70.83%

= 64.57%

4.

Dividend Yield

=

Dividends Per Common Share

Market Price Per Common Share

2011

2010

2009

$0.90

$0.85

$0.82

$12.80

$14.00

$16.30

= 7.03%

= 6.07%

= 5.03%

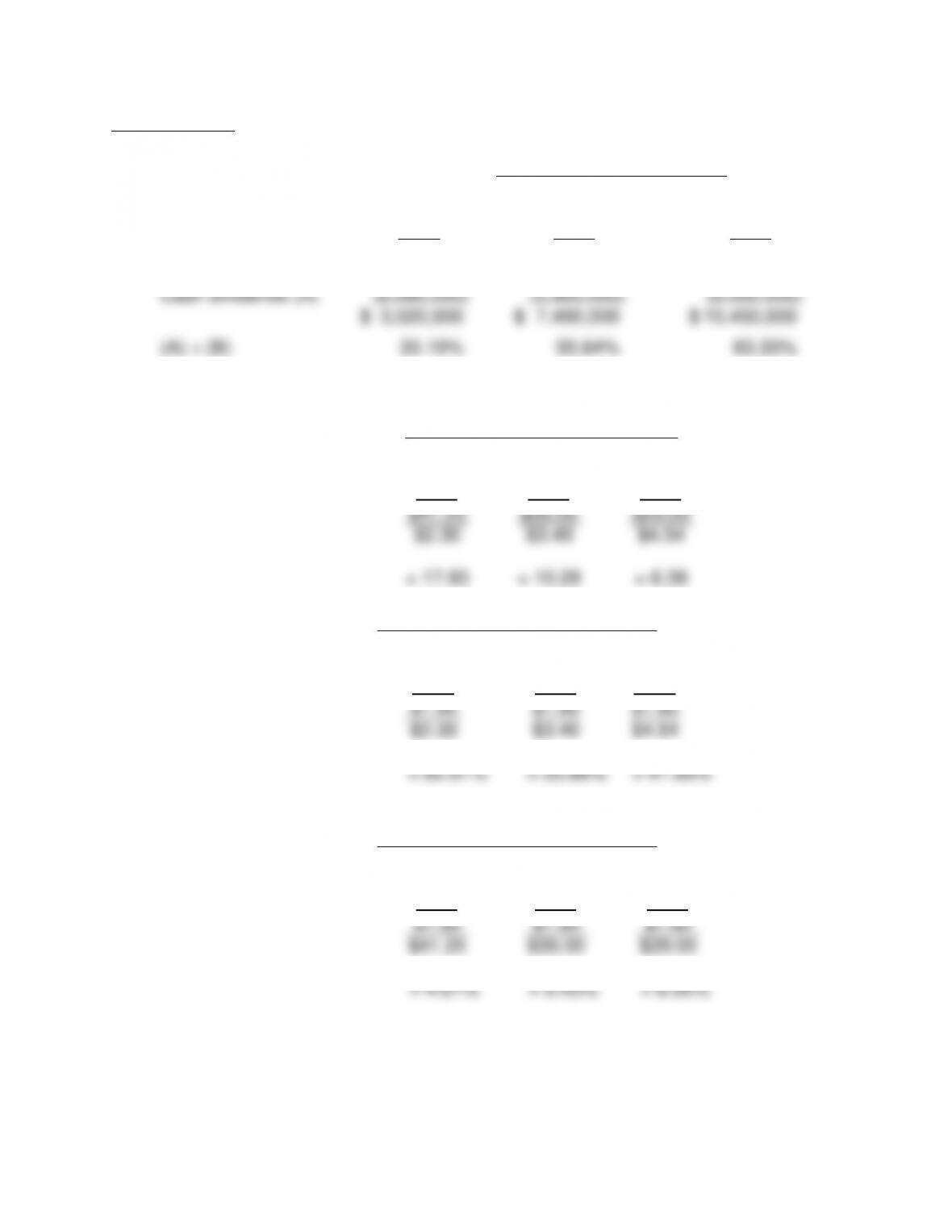

282

5.

Book Value Per Share

=

Total Stockholders’ Equity – Preferred Stock Equity

Number of Common Shares Outstanding

2011

2010

2009

Total assets:

$

$1,280,100,000

$

$1,267,200,000

$

1,260,400,000

Less:

Liabilities

(800,400,000)

(808,500,000)

(799,200,000)

Stockholders’ Equity

479,700,000

458,700,000

461,200,000

Less:

Nonredeemable

preferred stock

(15,300,000)

(15,300,000)

(15,300,000)

(A) Common stock

equity

$

$464,400,000

$

$443,400,000

$

$445,900,000

(B) Shares

outstanding end

of year

24,280,000

23,100,000

22,500,000

(A) ÷ (B)

$

$19.13

$

$19.19

$

$19.82

payout, is therefore increasing.

The price/earnings ratio has been relatively stable. The dividend yield has increased

283

PROBLEM 9-4

a.

1.

Percentage of Earnings Retained

=

Net Income – All Dividends

Net Income

2011

2010

2009

Net income (B)

$

9,100,000

$

13,300,000

$

16,500,000

Less:

Cash dividends (A)

(6,080,000)

(5,900,000)

(6,050,000)

$

3,020,000

$

7,400,000

$

10,450,000

(A) ÷ (B)

33.19%

55.64%

63.33%

2.

Price/Earnings Ratio

=

Market Price Per Share

Fully Diluted Earnings Per Share

2011

2010

2009

$41.25

$35.00

$29.00

$2.30

$3.40

$4.54

= 17.93

= 10.29

= 6.39

3.

Dividend Payout

=

Dividends Per Common Share

Fully Diluted Earnings Per Share

2011

2010

2009

$1.90

$1.90

$1.90

$2.30

$3.40

$4.54

= 82.61%

= 55.88%

= 41.85%

4.

Dividend Yield

=

Dividends Per Common Share

Market Price Per Common Share

2011

2010

2009

$1.90

$1.90

$1.90

$41.25

$35.00

$29.00

= 4.61%

= 5.43%

= 6.55%

284

5.

Book Value Per Share

=

Market Price Value

Ratio of Market Price to Book Value

2011

2010

2009

$41.25

$35.00

$29.00

120.5%

108.0%

105.0%

= $34.23

= $32.41

= $27.62

payout, materially increased.

The price earnings ratio materially increased, which is difficult to explain, considering

The increase in market price and the increase in price earnings ratio appears to be

285

PROBLEM 9-5

Simple Earnings Per Share

=

Net Income – Preferred Dividends

Weighted Average Number of

Common Shares Outstanding

Year 1

Year 2

$40,000 – $22,500

$42,000 – $27,500

38,000

38,000

$0.46

$0.38

The decline in earnings per share is caused mainly by the issuance of preferred

stock.

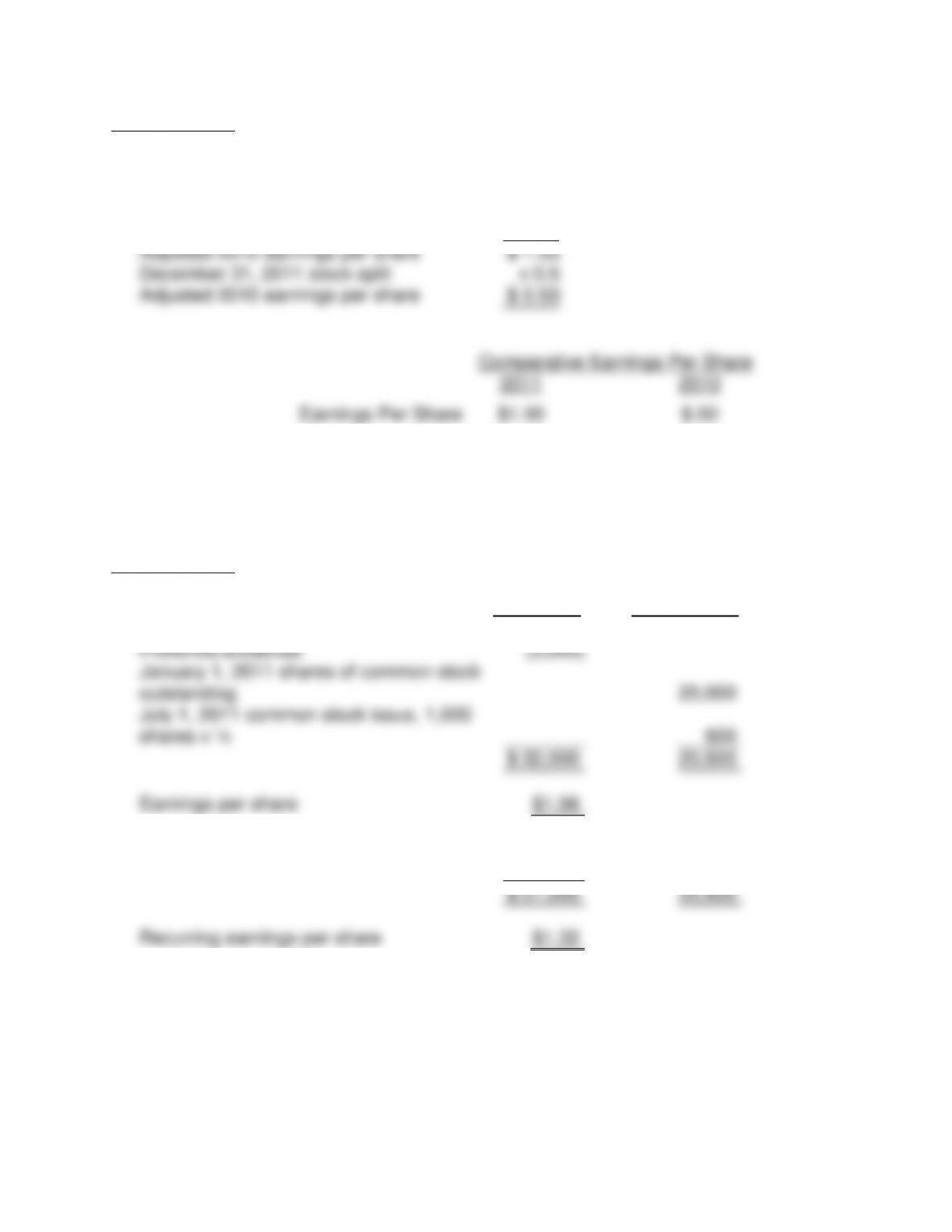

PROBLEM 9-6

January 1, shares outstanding

50,000

shares

July 1, two-for-one stock split

2

Adjusted shares outstanding for the year

(A)

100,000

October 1 stock issue

10,000

shares

Proportion of year that the new shares were

outstanding

0.25

Weighted average for the new shares on an annual

basis

(B)

2,500

Denominator of the earnings per share

computation for the current year

(A) + (B)

102,500

PROBLEM 9-7

Revision of 2010 earnings per share:

2010 reported earnings per share

$

2.00

July 1, 2011 stock split

x 0.5

Adjusted 2010 earnings per share

$

1.00

December 31, 2011 stock split

x 0.5

Adjusted 2010 earnings per share

$

0.50

Earnings Per Share

Numerator

Net income

$

35,000

Preferred dividends

Earnings per share

$1.56

$

27,000

20,500

Recurring earnings per share

$1.32