48

Chapter 3

Balance Sheet

QUESTIONS

3-1. Assets – Resources of the firm

3-2.

3-3.

3-4. They are listed in order of liquidity, which is the ease with which they can be

converted to cash.

3-5. Marketable securities are held as temporary investments or idle cash. They

higher return.

3- 6. Accounts receivable represents the money that the firm expects to collect;

3-7. A retailing firm will have merchandise inventory and supplies. A

and supplies.

3-8. Depreciation represents the allocation of an asset’s cost over the period it is

3-9. Straight-line depreciation is better for reporting, since it results in higher

profits than does accelerated depreciation. Double-declining balance is

a.

L

d.

A

g.

L

j.

E

m.

L

p.

A

s.

A

b.

L

e.

A

h.

A

k.

E

n.

L

q.

A

c.

A

f.

A

i.

A

l.

A

o.

A

r.

A

a.

TA

c.

IA

e.

IA

g.

TA

i.

TA

k.

IV

b.

CA

d.

CA

f.

CA

h.

CA

j.

CA

l.

TA

49

3-10. The rent is treated as a liability because it is unearned. The rental agency

covered by the rent.

there were a great deal of risk involved.

b. The discount is shown as a reduction of the liability.

interest expense on the income statement.

3-13. Historical cost causes difficulties in analysis because cost does not measure

3-14. At the option of the bondholder (creditor), the bond is exchanged for a

specified number of common shares (and the bondholder becomes a

When the common stock price increases sufficiently, the bondholder will

convert the bond to common stock.

3-15.

a.

CA

f.

CA

k.

CL

p.

NA

b.

CA

g.

E

l.

NL

q.

CA

c.

CL

h.

NA

m.

CL

r.

CL

d.

CL

i.

CA

n.

CA

s.

CA

e.

E

j.

E

o.

E

3-16. a. With the cumulative feature, if a corporation fails to declare the usual

dividend on the cumulative preferred stock, the amount of past

50

c. Convertible preferred stock contains a provision that allows the

preferred stockholders, at their option, to convert the share of

corporation.

d. Callable preferred stock may be retired (recalled) by the corporation at

its option.

3-17. The account “unrealized exchange gains or losses” is an shareholders’

combination, or the equity method of accounting.

3-18. Treasury stock represents the stock of the company that has been sold,

as inventory if they are not sold.

3-20. These subsidiaries are presented as an investment on the parent’s balance

sheet.

3-21. Noncontrolling interest is presented on a balance sheet when an entity in

3-22. If DeLand Company owns 100% of Little Florida, Inc., it will not have a

noncontrolling interest. Little Florida would not be consolidated when control

3-23. The account “unrealized decline in market value of noncurrent equity

unrealized losses on long-term equity investments.

51

3-24. Redeemable preferred stock is subject to mandatory redemption

3-25. Fair value is the price that a company would receive to sell an asset (or

the date of measurement.

3-27. Level 3 valuation can be very subjective.

3-28. A quasi-reorganization is an accounting procedure equivalent to an

3-29. An ESOP is a qualified stock-bonus, or combination stock-bonus and

securities.

3-30. These institutions are willing to grant a reduced rate of interest because they

3-31. Some firms do not find an ESOP attractive because it can result in a

dilute the control of management.

compensation deduction within stockholders’ equity.

3-33. Depreciation is the process of allocating the cost of building and machinery

depletion.

3-34. The three factors usually considered when computing depreciation are asset

from service.

3-35. A firm will often want to depreciate slowly for the financial statements

3-36. Over the life of an asset, the total depreciation will be the same, regardless

52

of the depreciation method selected.

3-38. Conceptually, this account balance represents retained earnings from other

comprehensive income.

3-39. Donated capital results from donations to the company by stockholders,

creditors, or other parties.

3-40. The land account under assets would be increased and the donated capital

3-41. 1. Those that require retroactive recognition (those require balance sheet

and income statement recognition).

53

PROBLEMS

PROBLEM 3-1

Airlines International

Balance Sheet

December 31, 2012

ASSETS

Current assets:

Cash

$

28,837

Marketable securities

10,042

Accounts receivable

$

67,551

Less: Allowance for doubtful accounts

248

67,303

Inventory

16,643

Prepaid expenses

3,963

Total current assets

$

126,788

Investment and special funds

11,901

Property, plant, and equipment:

Property, plant and equipment

$

809,980

Less: Accumulated depreciation

220,541

589,439

Other assets

727

Total assets

$

728,855

LIABILITIES AND STOCKHOLDERS’ EQUITY:

Current Liabilities:

Accounts payable

$

77,916

Accrued expenses

23,952

Unearned transportation revenue

6,808

Current installments of long-term debt

36,875

Total current liabilities

$

145,551

Long-term debt, less current portion

393,808

Deferred income taxes

42,070

Stockholders’ equity:

Common stock (par $0.50, authorized 20,000

shares, issued and authorized 14,304)

$

7,152

Capital in excess of par

72,913

Retained earnings

67,361

Total stockholders’ equity

147,426

Total liabilities and stockholders’ equity

$

728,855

54

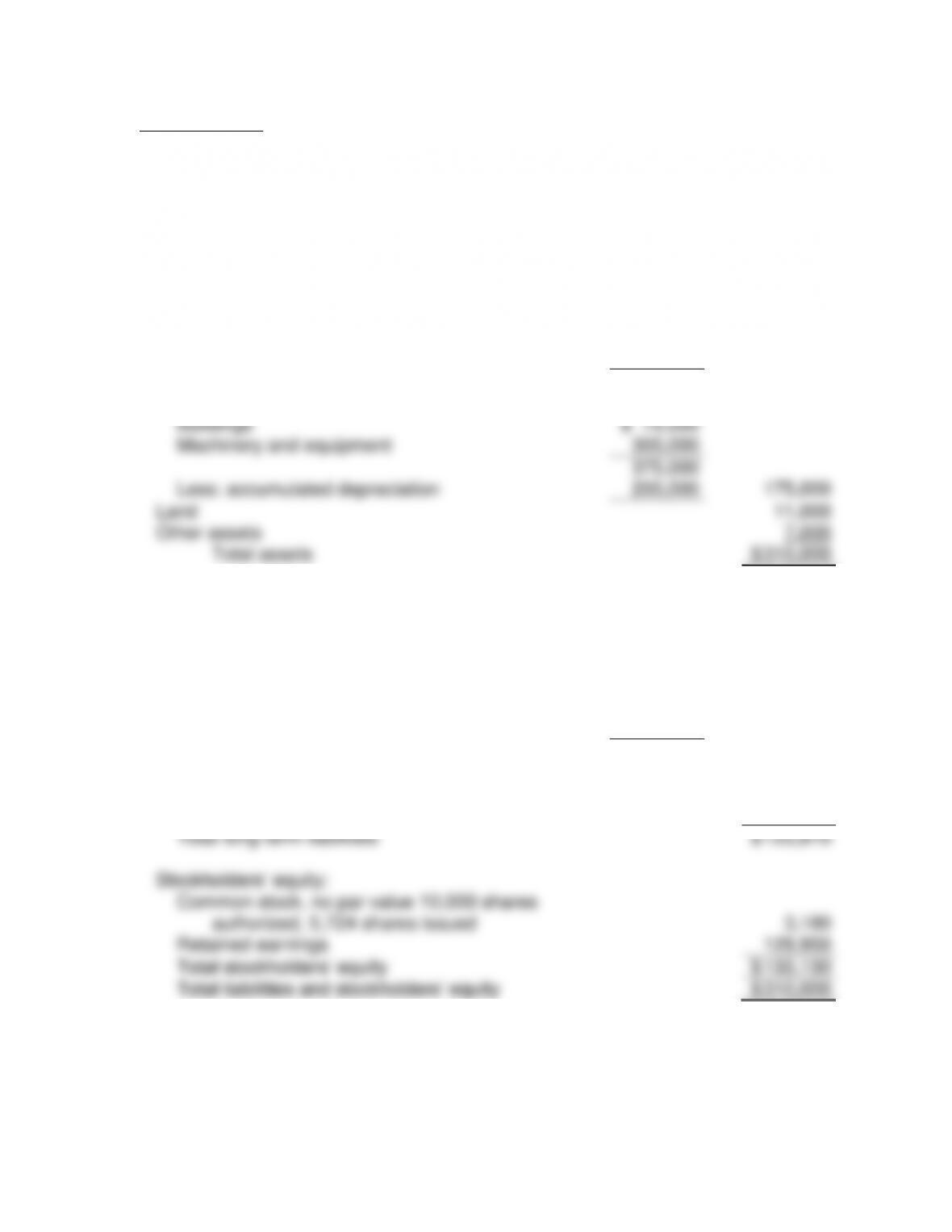

PROBLEM 3-2

Lukes, Inc.

Balance Sheet

December 31, 2012

ASETS

Current assets:

Cash

$

3,000

Receivables, less allowance of $3,000

58,000

Inventories

54,000

Prepaid expenses

2,000

Total current assets

$

117,000

Plant and equipment:

Buildings

$

75,000

Machinery and equipment

300,000

375,000

Less: accumulated depreciation

200,000

175,000

Land

11,000

Other assets

7,000

Total assets

$

310,000

LIABILITIES AND STOCKHOLDERS’ EQUITY

Current liabilities:

Accounts payable

$

35,000

Accrued income taxes

3,000

Other accrued expenses

8,000

Current portion of long-term debt

7,000

Total current liabilities:

$

53,000

Long-term liabilities:

Long-term debt, less current portion

99,870

Deferred income tax liability

24,000

Total long-term liabilities

$

123,870

Stockholders’ equity:

Common stock, no par value 10,000 shares

authorized, 5,724 shares issued

3,180

Retained earnings

129,950

Total stockholders’ equity

$

133,130

Total liabilities and stockholders’ equity

$

310,000

PROBLEM 3-3

Alleg, Inc.

Balance SheetDecember 31, 2012

ASSETS

Current assets:

Cash

Marketable securities

Accounts receivable

Inventories

Total current assets

Plant and equipment:

Land and buildings

Machinery and equipment

Less: Accumulated depreciation

Total plant and equipment

Intangibles:

Current maturities of long-term debt

Total current liabilities

Long-term liabilities:

Mortgages payable

Bonds payable

Deferred income taxes

Total long-term liabilities

Shareholders’ equity:

Common stock

21,000 shares authorized at $1 par value,

10,000 shares issued and outstanding

Additional paid-in capital

$ 13,000

17,000

26,000

30,000

86,000

57,000

125,000

182,000

61,000

121,000

8,000

10,000

26,000

80,000

70,000

18,000

168,000

10,000

38,000

33,000

56

investment.

b. Investment in Subsidiary Company is long-term.

depreciable.

e. Treasury stock should be deducted from stockholders’ equity.

h. For most industries, liabilities should be classified as current and long-term.

i. Preferred and common stock should be separated, as should capital in

excess of par.

PROBLEM 3-5

b. Preferable to disclose allowance for doubtful accounts on face of

disclosed.

e. Short-term U.S. Notes should be classified under current assets.

f. Supplies should be classified under current assets.

payable should be under long-term liabilities.

h. Redeemable preferred stock should be presented before stockholders’

equity.

57

PROBLEM 3-6

b. $10,000 cash should be classified under “other assets” (restricted for

payment of long-term note).

d. Patent should be classified under intangibles.

f. Prepaid insurance should be under current assets.

PROBLEM 3-7

a. The dividends would not be shown on the balance sheet. The dividends

is shown on the balance sheet.

b. You would disclose a contingent liability in note format.

d. This subsequent event requires a note.

f. Securities held for control should be classified as long-term investments.

g. Land must be listed at cost. It will have to be written back down.

from the balance sheet.