148

d. Days’ Sales in Receivables:

Gross Receivables

=

$50,000

=

4.56 days

Net Sales/365

$4,000,000/365

e. Days’ Sales in Inventory:

Ending Inventory

=

$400,000

=

81.11 days

Cost of Goods Sold/365

$1,800,000/365

f. The days’ sales in receivables and the days’ sales in inventory are understated based

on the year-end figures because the receivables and inventory numbers are

Anne Elizabeth Corporation is using a natural business year; therefore, at year-end,

the receivables and the inventory are below average for the year.

PROBLEM 6-17

a. First-In, First-Out (FIFO):

Ending Inventory

August 1, Purchase 200 @ $7.00

$1,400

November 1, Purchase 200 @ $7.50

1,500

$2,900

b. Last-In, First-Out (LIFO):

Ending Inventory

149

c. Average Cost (Weighted Average):

Average Cost

=

Total Cost

=

$10,900

=

$6.06

Total Units

1,800

d. Specific Identification:

150

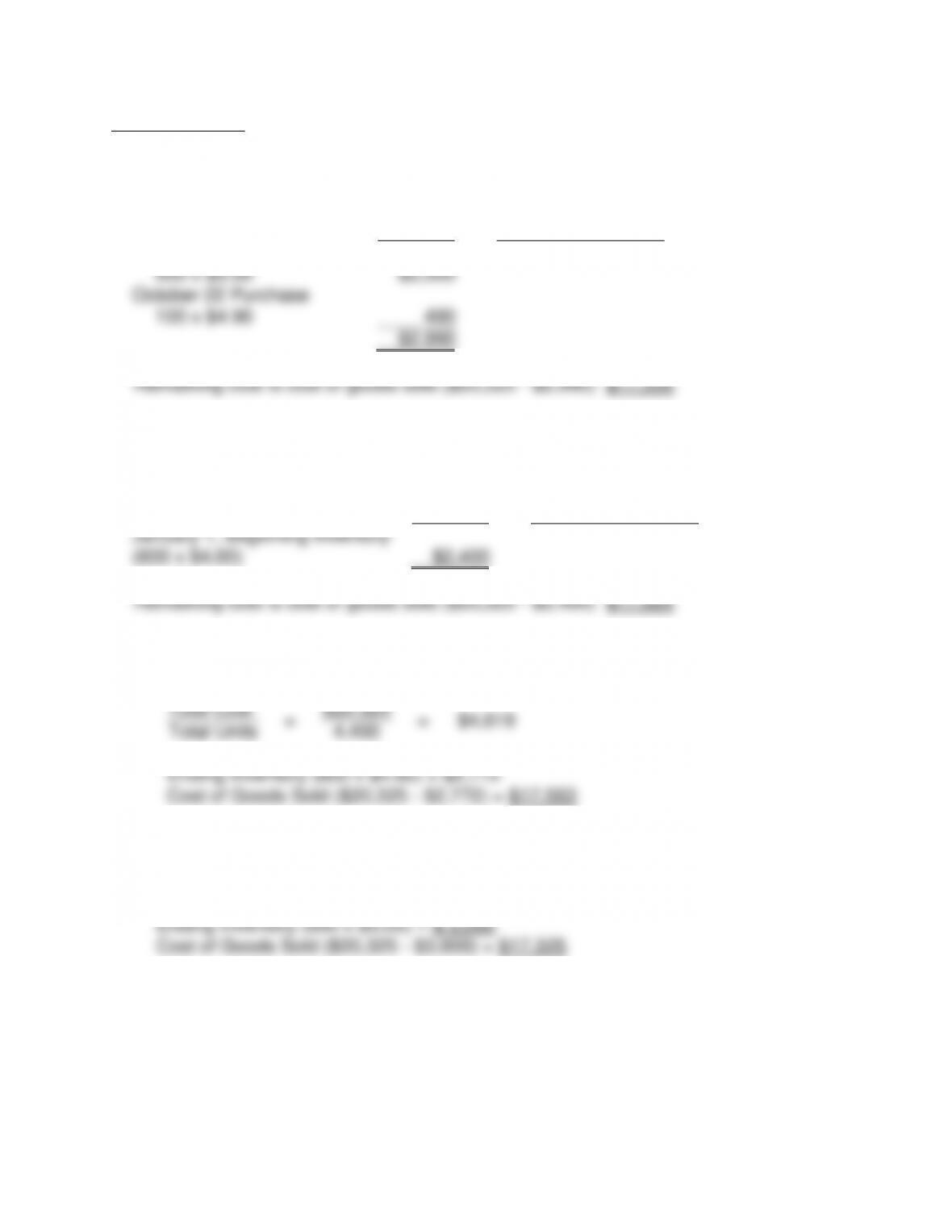

PROBLEM 6-18

a. First-In, First-Out (FIFO):

Ending

Inventory

Cost of Goods Sold

December 10 Purchase

500 x $5.00

$2,500

October 22 Purchase

100 x $4.90

490

$2,990

b. Last-In, First-Out (LIFO):

Ending

Inventory

Cost of Goods Sold

January 1, Beginning Inventory

(600 x $4.00)

$2,400

c. Average Cost (Weighted Average):

Total Cost

=

$20,325

=

$4,619

Total Units

4,400

d. Specific Identification:

July 1 purchase cost $5.00

151

PROBLEM 6-19

a. Sales to Working Capital:

2011

2010

2009

$650,000

=

2.41

$600,000

=

2.31

$500,000

=

2.08

$270,000

$260,000

$240,000

Industry

Average

4.10

4.05

4.00

ratio each year.

PROBLEM 6-20

and after the transactions.

b. 2 This would increase current assets and current liabilities by the same amount.

d. 4 A write-off of inventory would decrease the numerator in the current ratio.

e. 2 The liquidation of a long-term note would reduce the numerator in both the

quick ratio and the current ratio, but it would reduce the numerator of the quick

152

PROBLEM 6-21

a.

2

Cash Equivalents + Marketable Securities + Net Receivables

Current Liabilities

$2,100,000 + 7,200,000 + $50,500,000

=

1.76

$34,000,000

b.

1

The collection of accounts receivable does not change the total

numerator or the denominator of the current ratio formula, nor does the

collection change total current assets or total current liabilities.

PROBLEM 6-22

a.

1

Net Sales

Average Gross Receivables

$1,500,000

=

20.0 times per year

($8,000 + $72,000 + $10,000 + $60,000)/2

b.

2

December 31 represents a date when the accounts receivable would be low

and unrepresentative; thus, the accounts receivable turnover computed on

December 31 will be overstated.

153

PROBLEM 6-23

a.

3

Cash Equivalents + Marketable Securities + Net Receivables

Current Liabilities

$8,000 + $32,000 + $40,000

=

$80,000

=

0.89

$60,000 + $30,000

$90,000

b.

1

Net Sales (use only credit sales when available)/Average Gross Receivables

(only net receivables in this problem)

Net Sales

Average Gross Receivables

Note: Use only credit sales when available.

$600,000

=

$600,000

=

8.00 times

($40,000 + $110,000)/2

$75,000

c.

1

Cost of Goods Sold

Average Inventory

$1,260,000

=

$1,260,000

=

11.45 times

($80,000 + $140,000)/2

$110,000

d.

4

Current Assets

Current Liabilities

$8,000 + $32,000 + $40,000 + $80,000

=

$160,000

=

1.78 times

$60,000 + $30,000

$90,000

e.

2

As long as the current ratio is greater than 1 to 1, any payment will increase

the current ratio because the current liabilities go down more in proportion than

do the current assets.

154

PROBLEM 6-24

a.

1

An increase in inventory would increase the current ratio. To the extent that

the increase in inventory used current funds available, this would decrease the

acid-test.

b.

4

LIFO would result in a lower inventory figure. This would decrease the current

ratio and increase inventory turnover.

c.

3

Current Assets

=

X

=

3.0

Current Liabilities

$600,000

Current Assets – Inventory

=

$1,800,000 – Y

=

2.5

Current Liabilities

$600,000

Cost of Sales

=

$500,000

=

1.67

Inventory

$300,000

d.

2

The most logical reason for the current ratio to be high and the quick ratio low is

that the firm has a large investment in inventory.

e.

5

Low default risk, readily marketable, and a short-term to maturity is a proper

description of investment instruments used to invest temporarily idle cash

balances.

f.

1

A proper management of accounts receivable should achieve a combination of

sales volume, bad debt experience, and receivables turnover that maximizes the

profits of the corporation.

g.

5

Any of the four items could be used to cover payroll expenses.

155

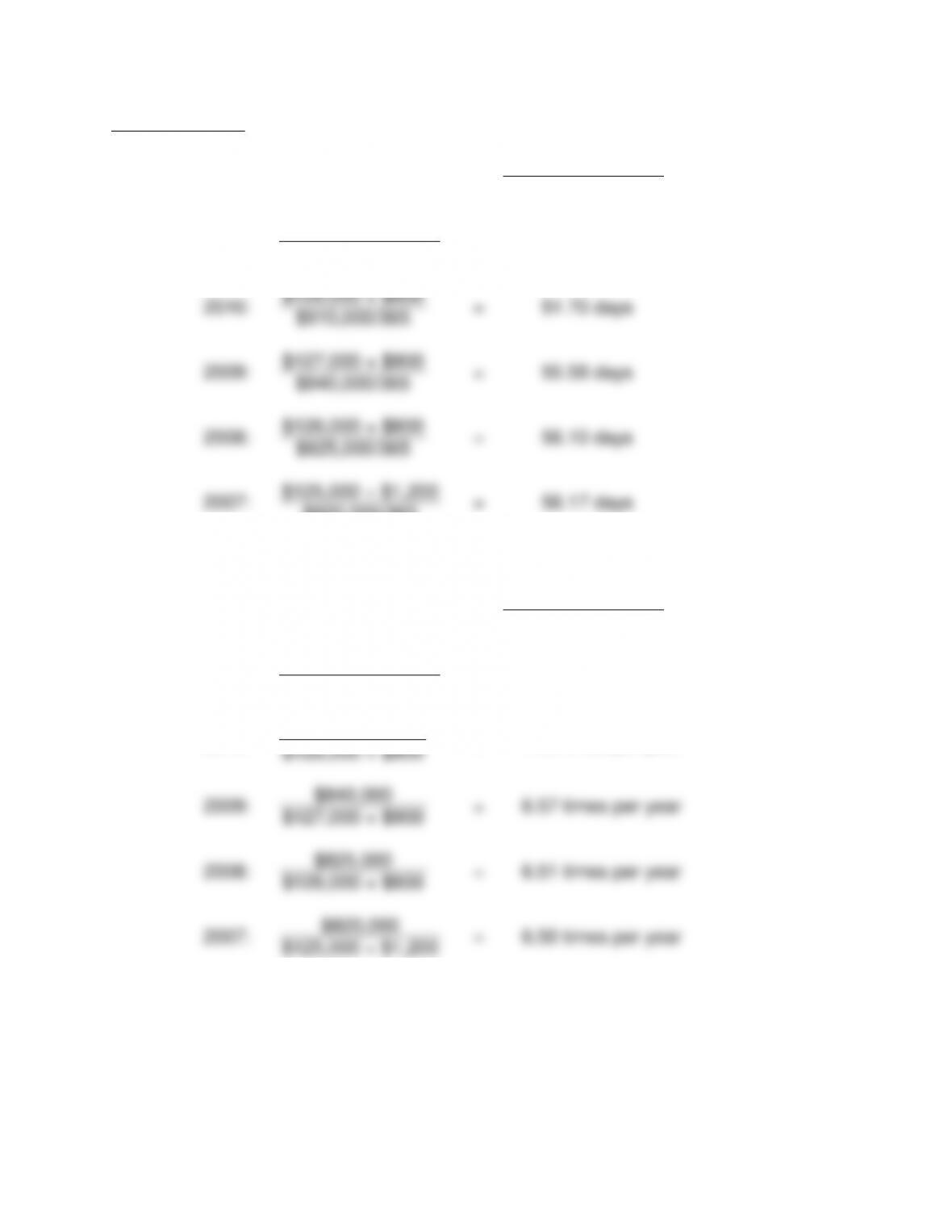

PROBLEM 6-25

a.

1.

Days’ Sales in Receivables

=

Gross Receivables

Net Sales/365

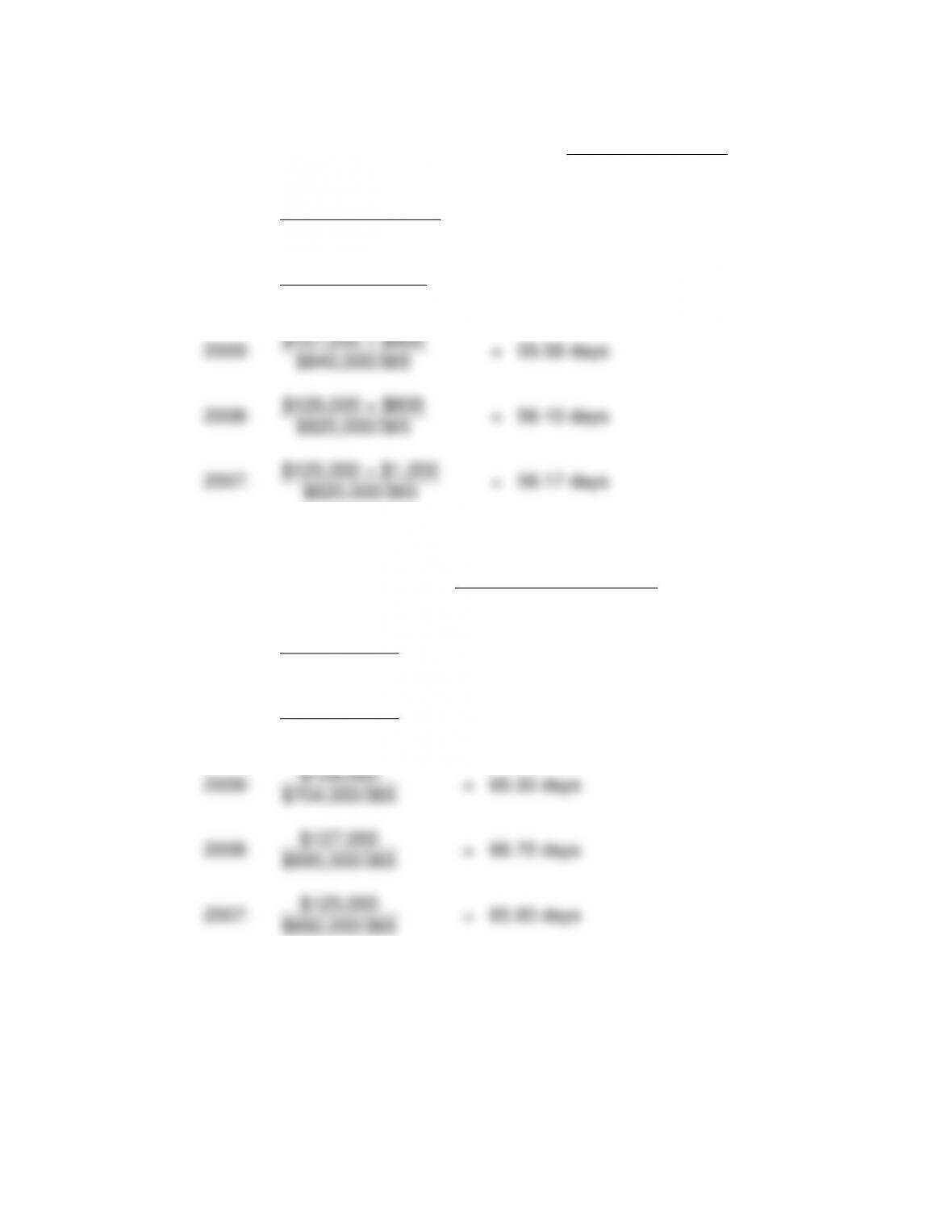

2011:

$131,000 + $1,000

=

54.75 days

$880,000/365

2010:

$128,000 + $900

=

51.70 days

$910,000/365

2009:

$127,000 + $900

=

55.58 days

$840,000/365

2008:

$126,000 + $800

=

56.10 days

$825,000/365

2007:

$125,000 + $1,200

=

56.17 days

$820,000/365

2.

Accounts Receivable Turnover

=

Net Sales

Gross Receivables

2011:

$880,000

=

6.67 times per year

$131,000 + $1,000

2010:

$910,000

=

7.06 times per year

$128,000 + $900

2009:

$840,000

=

6.57 times per year

$127,000 + $900

2008:

$825,000

=

6.51 times per year

$126,000 + $800

2007:

$820,000

=

6.50 times per year

$125,000 + $1,200

156

3.

Accounts Receivable Turnover in Days

=

Gross Receivables

Net Sales/365

2011:

$131,000 + $1,000

=

54.75 days

$880,000/365

2010:

$128,000 + $900

=

51.70 days

$910,000/365

2009:

$127,000 + $900

=

55.58 days

$840,000/365

2008:

$126,000 + $800

=

56.10 days

$825,000/365

2007:

$125,000 + $1,200

=

56.17 days

$820,000/365

4.

Days’ Sales in Inventory

=

Ending Inventory

Cost of Goods Sold/365

2011:

$122,000

=

60.18 days

$740,000/365

2010:

$124,000

=

59.55 days

$760,000/365

2009:

$126,000

=

65.33 days

$704,000/365

2008:

$127,000

=

66.70 days

$695,000/365

2007:

$125,000

=

65.93 days

$692,000/365

157

5.

Inventory Turnover

=

Cost of Goods Sold

Ending Inventory

2011:

$740,000

=

6.07 times per year

$122,000

2010:

$760,000

=

6.13 times per year

$124,000

2009:

$704,000

=

5.59 times per year

$126,000

2008:

$695,000

=

5.47 times per year

$127,000

2007:

$692,000

=

5.54 times per year

$125,000

6.

Inventory Turnover in Days

=

Ending Inventory

Cost of Goods Sold/365

2011:

$122,000

=

60.18 days

$740,000/365

2010:

$124,000

=

59.55 days

$760,000/365

2009:

$126,000

=

65.33 days

$704,000/365

2008:

$127,000

=

66.70 days

$695,000/365

2007:

$125,000

=

65.93 days

$692,000/365