419

b. The operating ratio decreased, indicating improved efficiency. Funded debt to

Percent earned to operating property increased, indicating improved profitability.

profitability.

be considered to be positive.

PROBLEM 12-5

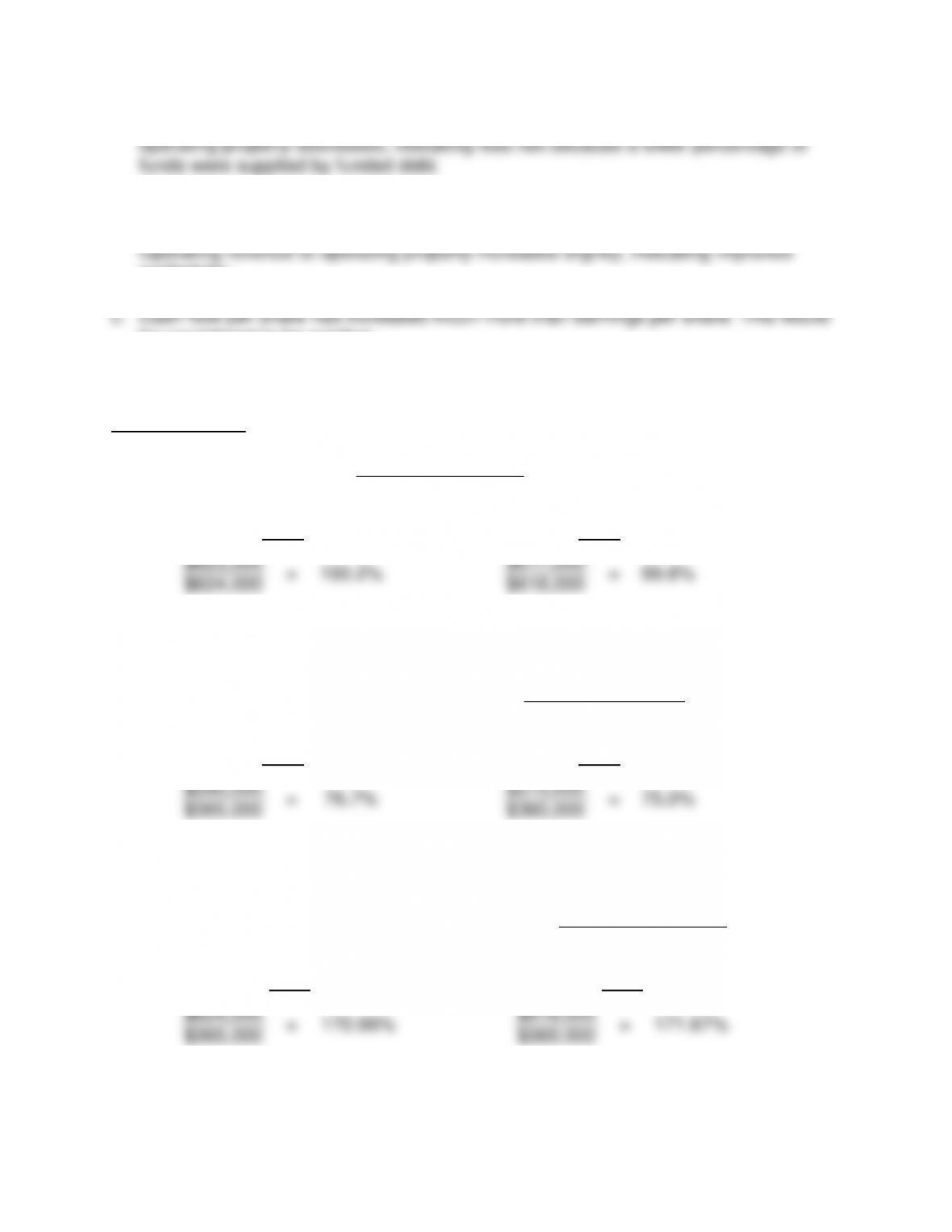

a.

Operating Ratio

=

Operating Expense

Operating Revenue

2011

2010

$625,000

=

100.2%

$617,000

=

99.8%

$624,000

$618,000

This firm is having profit problems. Expenses have increased faster than revenues.

b.

Long-Term Debt to Operating Property

=

Long-Term Debt

Operating Property

2011

2010

$280,000

=

76.7%

$270,000

=

75.0%

$365,000

$360,000

This firm is using more debt in absolute terms and in relation to operating property.

c.

Operating Revenue to Operating Property

=

Operating Revenue

Operating Property

2011

2010

$624,000

=

170.96%

$618,000

=

171.67%

$365,000

$360,000

The turnover has remained relatively constant.

420

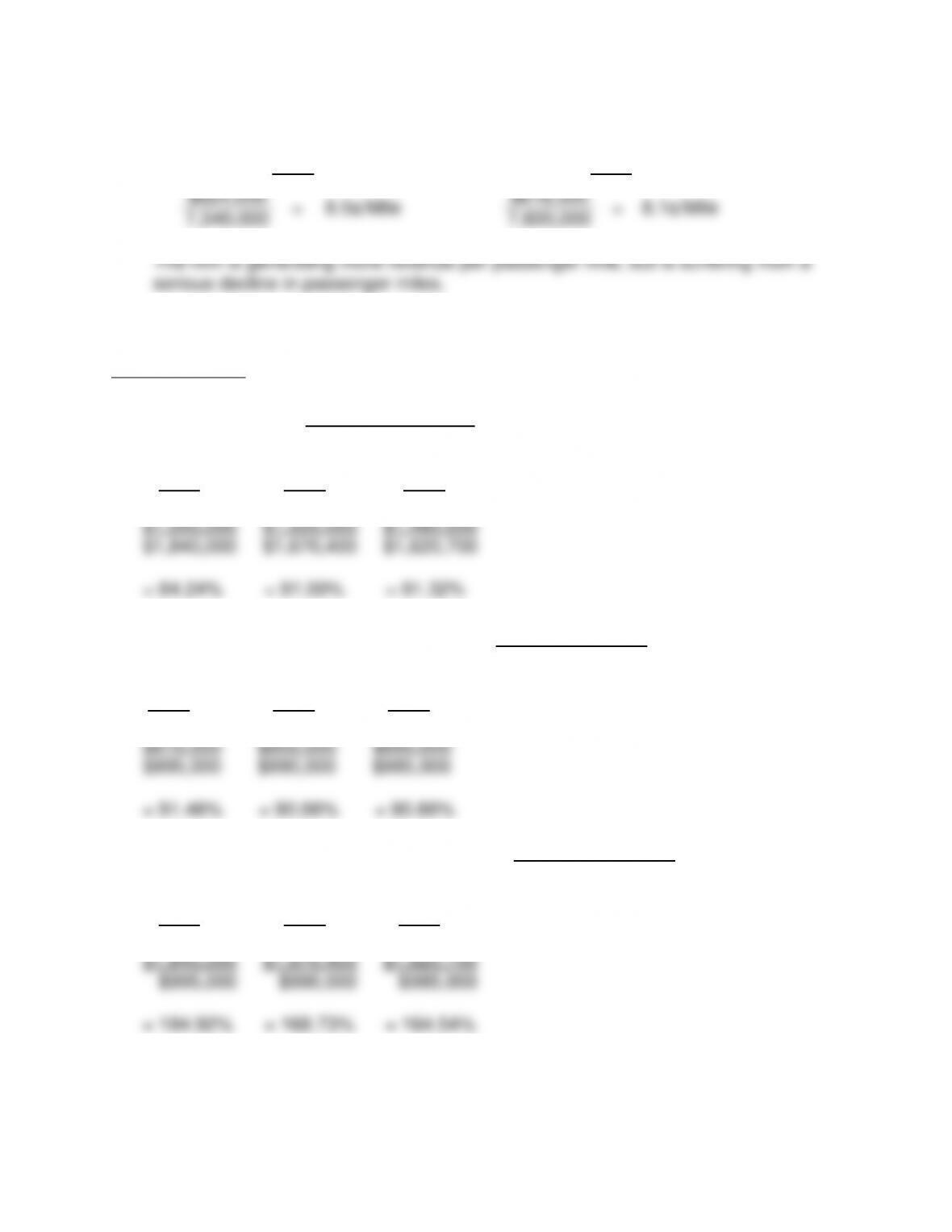

d. Revenue per Passenger Mile:

2011

2010

$624,000

=

8.5¢/Mile

$618,000

=

8.1¢/Mile

7,340,000

7,600,000

PROBLEM 12-6

a. 1. Operating Ratio = Operating Expenses

Operating Revenues

2011 2010 2009

2. Long-Term Debt To Operating Property = Long -Term Debt

Operating Property

2011 2010 2009

3. Operating Revenue to Operating Property = Operating Revenue

Operating Property

2011 2010 2009

b. The operating ratio decreased significantly, indicating improved profitability.

profitability.

c. The passenger load factor increased materially, indicating improved profitability.

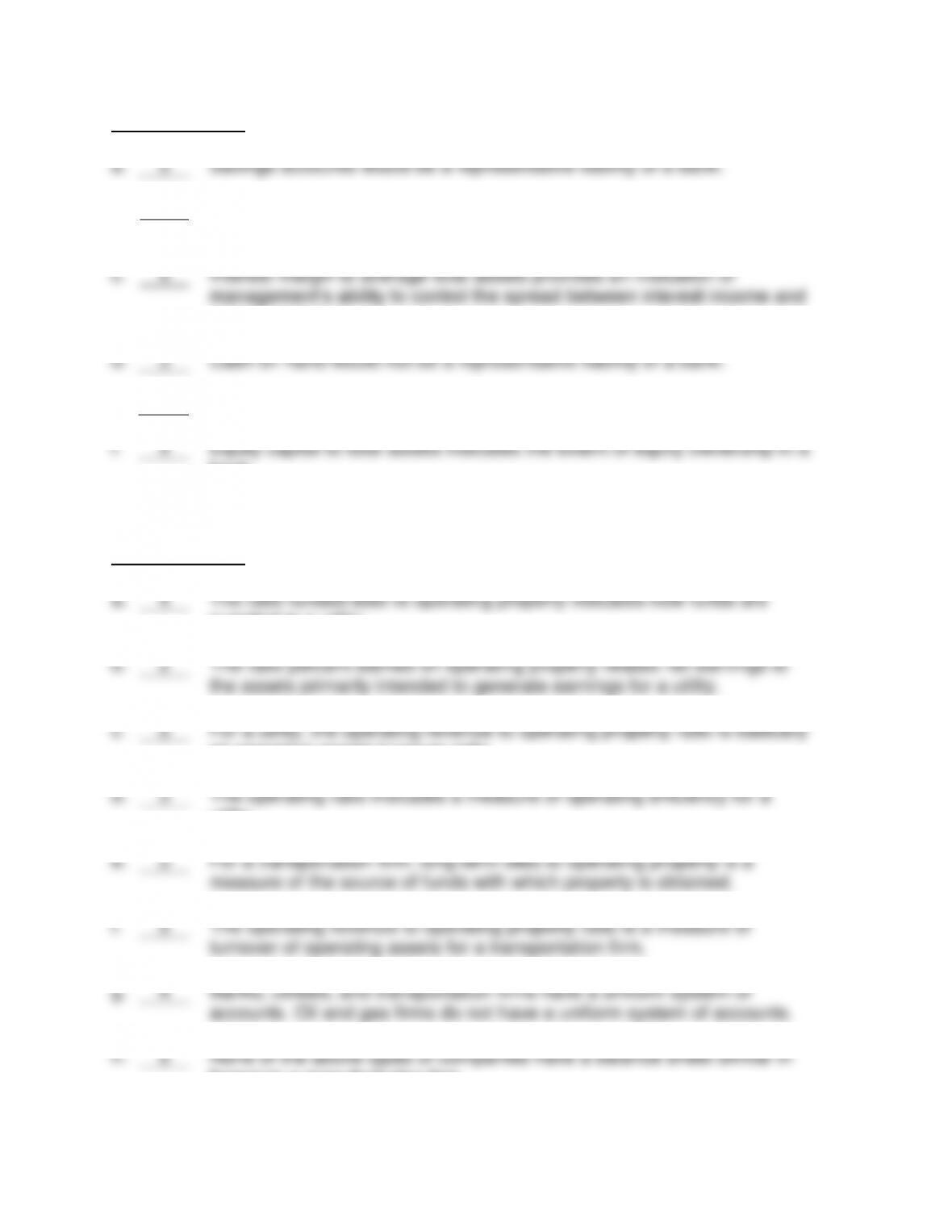

PROBLEM 12-7

a.

2

Bond companies do not represent a basic type of insurance organization.

b.

1

For insurance financial reporting, the balance sheet is not a class.

c.

1

Investment gains/losses are not part of the quantification process when

estimating the reserves.

d.

5

For investment contracts, termination fees are not booked as revenue

over the period of the contract.

e.

3

After the annual reports are files with the individual state insurance

departments, a testing process is conducted by the NAIC. If a

company’s ratio is outside the prescribed limit, the NAIC brings that to the

attention of the state insurance department.

f.

5

All of the above contribute to the relatively low market value of insurance

companies.

422

PROBLEM 12-8

a.

5

Savings accounts would be a representative liability of a bank.

b.

3

Cash is not an earning asset of a bank for the earning assets to total

assets ratio.

c.

4

Interest margin to average total assets provides an indication of

management’s ability to control the spread between interest income and

interest expense.

d.

3

Cash on hand would not be a representative liability of a bank.

e.

5

Typically, the largest expense for a bank will be interest expense.

f.

4

Equity capital to total assets indicates the extent of equity ownership in a

bank.

PROBLEM 12-9

a.

4

The ratio funded debt to operating property indicates how funds are

supplied to a utility.

b.

2

The ratio percent earned on operating property relates net earnings to

the assets primarily intended to generate earnings for a utility.

c.

5

For a utility, the operating revenue to operating property ratio is basically

an operating assets turnover ratio.

d.

3

The operating ratio indicates a measure of operating efficiency for a

utility.

e.

3

For a transportation firm, long-term debt to operating property is a

measure of the source of funds with which property is obtained.

f.

5

The operating revenue to operating property ratio is a measure of

turnover of operating assets for a transportation firm.

g.

4

Banks, utilities, and transportation firms have a uniform system of

accounts. Oil and gas firms do not have a uniform system of accounts.

h.

5

None of the above types of companies have a balance sheet similar in

format to a manufacturing firm.

423

CASES

CASE 12-1 AFUDC EQUITY AND DEBT

that the balance sheet is not presented in the order described in the book.)

a. AFUDC is the estimated cost of debt and equity used to finance regulated plant

additions that can be recorded as part of the cost of construction projects. AFUDC

b. Capitalizing interest on borrowed funds prevents this expense from reducing income

d. Capitalizing allowance for equity funds used during construction increases income

e. Both the capitalization of interest on borrowed funds and the capitalization

flow.

f. 1. Operating ratio

In Millions

2010

2009

Operating expenses (A)

$

11,533

$

11,100

Operating revenues (B)

$

13,841

$

13,399

Operating ratio (A ÷ B)

83.32%

82.84%

424

2. Funded debt to operating property

In Millions

2010

2009

Funded debt* (A)

$809 + $10,906 +

$423 = $12,138

$342 + 10,381 +

$827 = $11,550

Operating property (B)

$31,449

$28,892

Funded debt to operating property

(A ÷ B)

38.60%

39.98%

*Included long-term debt and current maturities of long-term debt.

3. Percent earned on operating property

In Millions

2010

2009

Net income (A)

$1,113

$1,234

Operating property

$31,449

$28,892

Less: Construction in progress

$1,384

$1,888

Operating property adjusted for construction in

progress (B)

$30,065

$27,004

Percent earned on operating property (A ÷ B)

3.70%

4.57%

4. Operating revenue to operating property

In Millions

2010

2009

Operating revenues (A)

$13,841

$13,399

Operating property (B)*

$30,065

$27,004

Operating revenue to operating property (A ÷ B)

46.04%

49.62%

*Excluded construction in progress

425

Comment on the Above Ratios

1. Operating ratio

2. Funded debt to operating property

Decreased slightly

4. Operating revenue to operating property

A substantial decrease

ACTIVITIES

(This case provides the opportunity to view results of operations for oil and gas

producing activities using vertical and horizontal common-size analysis.)

a. Vertical Common-Size

For the Years Ended December 31

Total

United

States

Europe

Africa

Asia

and other

2010

Sales and other operating revenues

Unaffiliated customers

Inter-company

Total revenues

98.4

1.6

100.0

94.2

5.8

100.0

100.0

—–

100.0

100.0

—–

100.0

100.0

—–

100.0

Cost and expenses

Production expenses, including

related taxes

22.0

19.9

32.3

16.5

19.6

Exploration expenses, including dry

holes and lease impairment (b)

9.9

14.8

2.2

5.2

24.0

General administrative and other

expenses

3.2

6.6

2.1

.7

4.0

Depreciation, depletion and

Amortization

25.4

26.5

20.6

28.1

26.2

Asset impairments

6.1

—–

—–

19.3

—–

Total costs and expenses

66.6

67.8

57.2

69.9

73.8

Results of operations before

income taxes

33.4

32.2

42.8

30.1

26.2

Provision for income taxes

18.1

12.4

21.2

21.1

17.1

Results of operations

15.3

19.8

21.6

9.0

9.1