384

c. No. Return on average assets before interest and taxes (third goal) is equal to return

on sales before interest and taxes (first goal) times turnover of average assets

(second goal). If Calcor Company achieved the first two goals, the return on

PROBLEM 11-13

a. A Company Z Score

X1

=

Working Capital

X1

=

$90,000

=

30.00

Total Assets

$300,000

X2

=

Retained Earnings

X2

=

$80,000

=

26.67

Total Assets

$300,000

X3

=

E.B.I.T.

X3

=

$70,000

=

23.33

Total Assets

$300,000

X4

=

Market Value of Equity

X4

=

$180,000

=

600.0

Book Value of Total Debt

$30,000

X5

=

Sales

X5

=

$430,000

=

143.33

Total Assets

$300,000

Z = 0.012 x 30.00

+ 0.014 x 26.67

Z = 0.36 Z = 6.53

+ 0.37

385

B Company Z Score

X1

=

Working Capital

X1

=

$120,000

=

42.86

Total Assets

$280,000

X2

=

Retained Earnings

X2

=

$90,000

=

32.14

Total Assets

$280,000

X3

=

E.B.I.T.

X3

=

$60,000

=

21.43

Total Assets

$280,000

X4

=

Market Value of Equity

X4

=

$168,750

=

337.50

Book Value of Total Debt

$50,000

X5

=

Sales

X5

=

$400,000

=

142.86

Total Assets

$280,000

Z = .012X1 + .014X2 + .033X3 + .006X4 + .010X5

Z = 0.012 x 42.86

+ 0.014 x 32.14

Z = 0.51 Z = 5.13

+ 0.45

C Company Z Score

X1

=

Working Capital

X1

=

$150,000

=

60.00

Total Assets

$250,000

X2

=

Retained Earnings

X2

=

$60,000

=

24.00

Total Assets

$250,000

X3

=

E.B.I.T

X3

=

$50,000

=

20.00

Total Assets

$250,000

X4

=

Market Value of Equity

X4

=

$148,500

=

185.63

Book Value of Total Debt

$80,000

X5

=

Sales

X5

=

$200,000

=

80.00

Total Assets

$250,000

386

Z = 0.012 x 60.00

+ 0.014 x 24.00

financial failure.

PROBLEM 11-14

a.

X1

=

Working Capital

X1

=

$152,800

=

30.90

Total Assets

$494,500

X2

=

Retained Earnings

X2

=

$248,000

=

50.15

Total Assets

$494,500

X3

=

E.B.I.T

X3

=

$84,000

=

16.99

Total Assets

$494,500

X4

=

Market Value of Equity

X4

=

$690,000

=

344.14

Book Value of Total Debt

$200,500

X5

=

Sales

X5

=

$860,000

=

173.91

Total Assets

$494,500

Z = .012X1 + .014X2 + .033X3 + .006X4 + .010X5

Z = 0.012 x 30.90

+ 0.014 x 50.15

387

+ 0.70

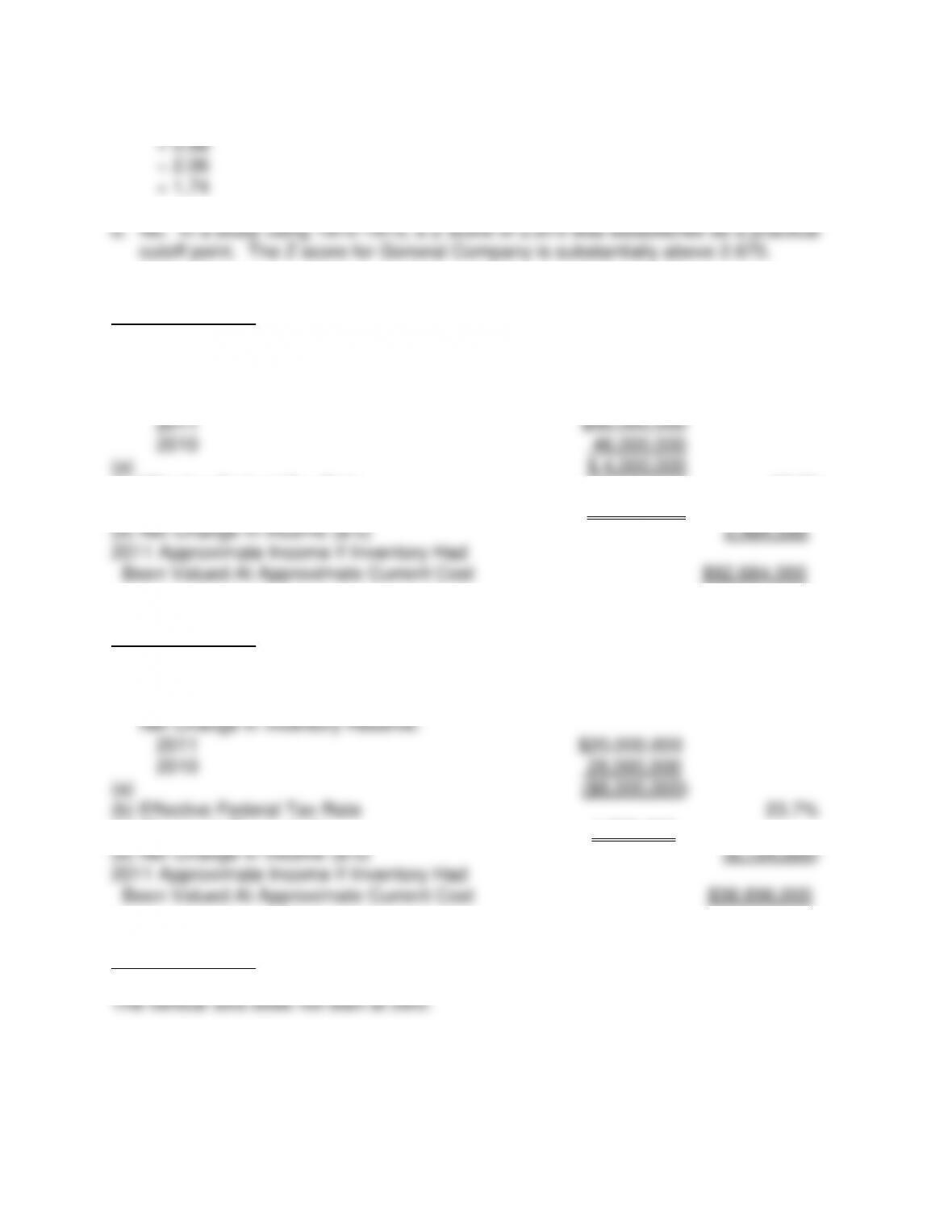

PROBLEM 11-15

2011 Net Income as Reported $90,200,000

Net Change in Inventory Reserve:

(b) Effective Federal Tax Rate 37.9%

(c) Change In Taxes (a x b) $ 1,516,000

PROBLEM 11-16

2011 Net Income as Reported $45,000,000

(c) Change in Taxes (axb) 1,896,000

PROBLEM 11-17

388

PROBLEM 11-18 PROVISION FOR OBSOLETE INVENTORY – ETHICAL

b. No. The inventory will be reduced and the reserve account will be reduced.

a. This promotion appears to be ethical and likely does not require special disclosure.

b. This promotion may not be ethical without special disclosure describing the

promotion and the risk. There needs to be a sales cutoff at December 31 not

389

CASES

CASE 11-1 SMOKE AND SMOKELESS

earnings and stock split.)

a. 1. 2010 Net earnings (in millions): $1,113

Net increase in inventory reserve:

2010

$197

2009

190

$7

3. Change in Taxes

4. Net increase in Income

[1 – 3]

5. Estimated Adjusted Income

2010 Net Earnings

$

1,113.00

Net Increase in Income

4.24

$

1,117.24

b.

1.

Days’ Sales in Inventory

=

Ending Inventory

Cost of Goods Sold/365

$1,055

=

$1,055

=

84.74 days

$4,544/365

12.45

2.

Working Capital

=

Current Assets – Current Liabilities

$4,802 – $4,372

=

$430

3.

Current Ratio

=

Current Assets

Current Liabilities

$7 X 39.4%

=

2.76

$7 – 2.76

=

4.24

390

$4,802

=

1.10

$4,372

4.

Acid-Test Ratio

=

Cash Equivalents + Marketable Securities + Net Receivables

Current Liabilities

$2,195 + $118

=

$2,313

=

.53%

$4,372

$4,372

5.

Debt Ratio

=

Total Liabilities

Total Assets

$4,372 + $3,701 + $518 + $1,668 + $309

=

$10,568

=

61.88%

$17,078

$17,078

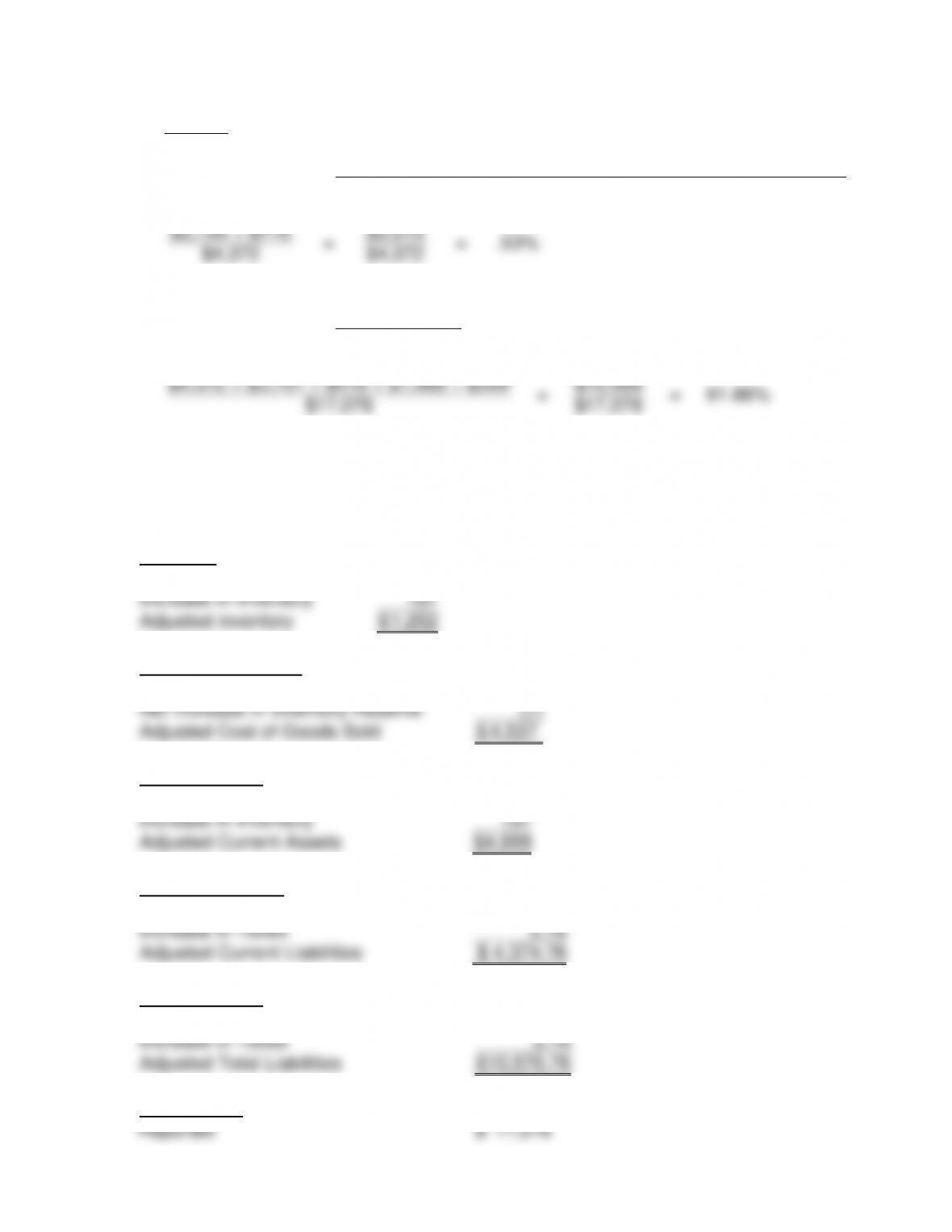

c. 2010, with Adjustment for LIFO Reserve

Computations of Changes

Inventory

Inventory Reported

$

1,055

Increase in Inventory

197

Adjusted inventory

$

1,252

Cost of Goods Sold

Reported

$

4,544

Net Increase in Inventory Reserve

(7)

Adjusted Cost of Goods Sold

$

4,537

Current Assets

Reported

$

4,802

Increase in Inventory

197

Adjusted Current Assets

$

4,999

Current Liabilities

Reported

$

4,372.00

Increase in Taxes

2.76

Adjusted Current Liabilities

$

4,374.76

Total Liabilities

Reported

$

10,568.00

Increase in Taxes

2.76

Adjusted Total Liabilities

$

10,570.76

Total Assets

Reported

$

17,078

391

Increase in Inventory

197

Adjusted Total Assets

$

17,275

1.

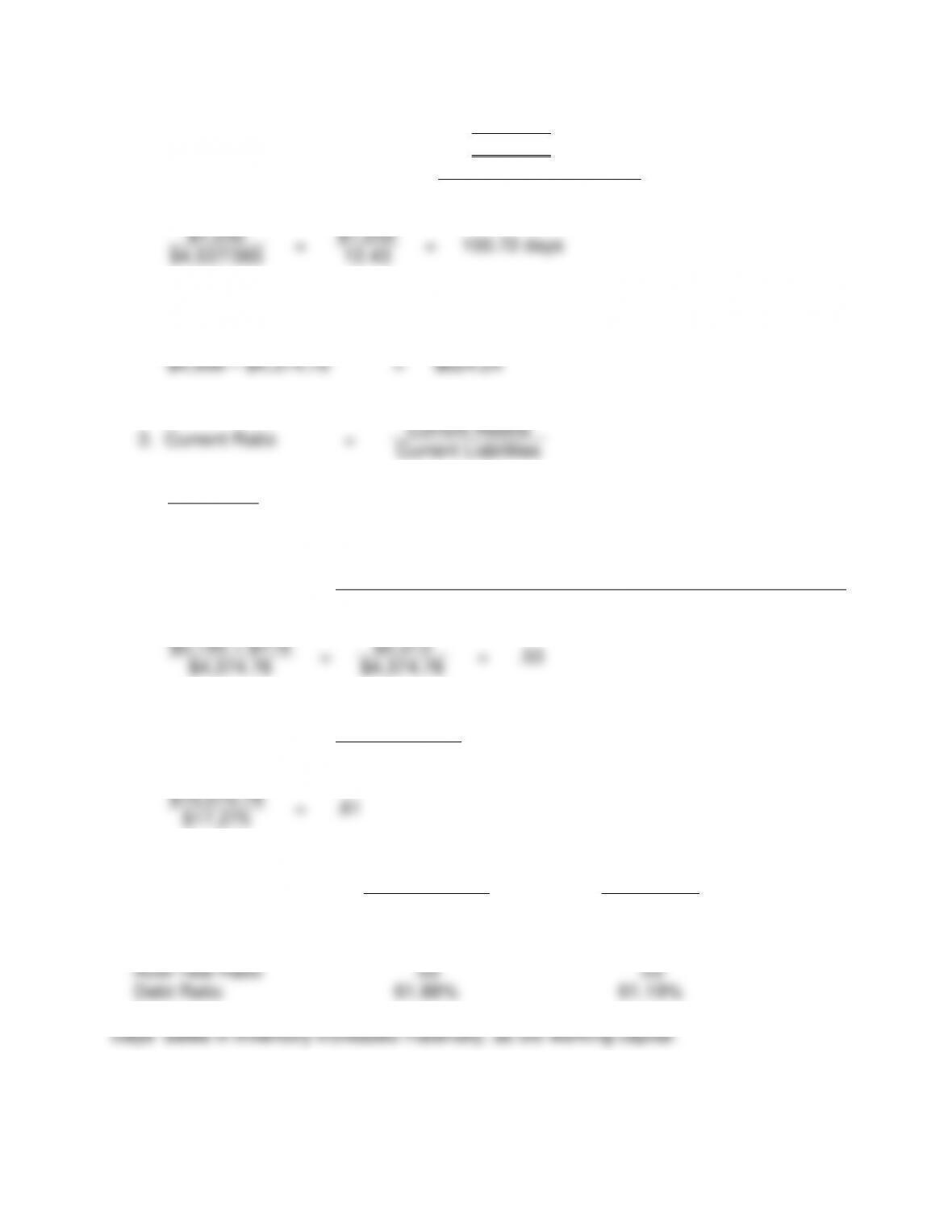

Days’ Sales in Inventory

=

Ending Inventory

Cost of Goods Sold/365

$1,252

=

$1,252

=

100.72 days

$4,537/365

12.43

2.

Working Capital

=

Current Assets – Current Liabilities

$4,999 – $4,374.76

=

$624.24

3.

Current Ratio

=

Current Assets

Current Liabilities

$4,999

=

1.14

$4,374.76

4.

Acid-Test Ratio

=

Cash Equivalents + Marketable Securities + Net Receivables

Current Liabilities

$2,195 + $118

=

$2,313

=

.53

$4,374.76

$4,374.76

5.

Debt Ratio

=

Total Liabilities

Total Assets

$10,570.76

=

.61

$17,275

d.

No Adjustment

Adjustment

Days Sales in Inventory

84.74

Days

100.72

Days

Working Capital

$

430

$

624.24

Current Ratio

1.10

1.14

Acid-Test Ratio

.53

.53

Debt Ratio

61.88%

61.19%

392

e. 2009 Financial Statements

Diluted income per share for 2009 and 2008

2009

$

1.65

2008

$

2.28

f. 125 million

Note: The following is the inventory reserve for 2007 – 2010:

2007

$

51,000,000

2008

112,000,000

2009

190,000,000

2010

197,000,000

CASE 11-2 ACCOUNTING HOCUS-POCUS

Levitt, Securities and Exchange Commission.)

a. “Big Bath”

earnings.

b. In an acquisition, if there is a large write off of “in–process” research and

development, this amounts to a one time charge. This removes the future earnings

drag.

d. A company can account for immaterial items without regard to generally accepted

accounting standards. Thus the company could use “materiality” to improperly

393

CASE 11-3 TURN A CHEEK

second amendment.)

a. Each student will write a different position paper on why the Nike reply should be

viewed under the first amendment.

viewed under the fifth amendment.

Note: In June 2003, the United States Supreme Court declined to hear the case on

procedural grounds.

30, 2003.

In September 2003, Nike settled with California activist Marc Kasky in a deal that

obliges Nike to pay $1.5 million during the next three years to a Washington worker–

rights group. The money will be used “to promote workers’ education, increase training,

“Clouding the muddy-free speech waters is the acknowledgement from justices in both

California and federal courts that Nike’s campaign contained elements of commercial

and noncommercial speech.”