25

Chapter 2

Introduction to Financial Statements and Other

Financial Reporting Topics

QUESTIONS

2- 1. a. Unqualified opinion with explanatory paragraph

b. Unqualified opinion with explanatory paragraph

2- 2. The responsibility for the preparation and integrity of financial statements

conformity with GAAP, and consistency.

2- 3. The basic purpose of the integrated disclosure system is to achieve

companies reporting.

2- 4. The explanatory paragraphs explain important considerations that the

concern.

2- 5. A review consists principally of inquiries of company personnel and

standards.

2- 6. No. The accountant’s report will indicate that they are not aware of any

accounting principles. The accountant does not express an opinion on

reviewed financial statements.

with a compilation.

2- 8. No. Some statements have not been audited, reviewed, or compiled.

accountant’s report.

26

2- 9. Balance Sheet

Income Statement

accounting period.

Statement of Cash Flows

a specified period of time.

2-10. Notes to the financial statements increase the full disclosure of the

2-11. Contingent liabilities depend on the outcome of a future event that

outcome of the case.

2-12. a, c

2-13. A proxy is the solicitation sent to stockholders for the election of directors

2-14. A summary annual report is a condensed annual report that omits much of

2-15. The firm must include a set of fully audited statements and other required

is also available to the public.

2-16. There is typically a substantial reduction in non-financial pages and

pages.

2-17. Cash flows from operating activities, cash flows from investing activities,

and cash flows from financing activities.

2-18. The income statement and the statement of cash flows. The income

27

dates.

2-19. Assets, liabilities, and owners’ equity.

and the retained earnings account.

2-21. Notes are an integral part of financial statements. A detailed review of

statements.

2-22. APB Opinion No. 22 requires disclosure of accounting policies as the first

2-23. They are interchangeable terms referring to ideals of character and

distinguishing between right and wrong.

2-26. The scheme of the double-entry system revolves around the accounting

equation:

(including the temporary accounts).

2-27. a. Assets, liabilities, and stockholders’ equity accounts are referred to as

forward to the next accounting period.

They are referred to as temporary accounts.

2-28. Because the employee worked in the period just ended, the salary must be

employee.

2-29. Adjusting entries are necessary to match revenues with the expenses that

28

2-30. Companies use a number of special journals to improve record keeping

2-31. Filing deadline for Form 10-K follow:

2-32. Sole Proprietorship

Partnership

Corporation

is evidenced by shares of stock.

2-33. Even an efficient market does not have access to “inside” information;

2-34. In an efficient market, the method of disclosure is not as important as

whether or not the item is disclosed.

2-35. Abnormal returns could be achieved if the market does not have access to

2-36. With the purchase method the firm doing the acquiring records the

2-37. Consolidated statements reflect an economic, rather than a legal, concept

of the entity.

2-38. The financial statements of the parent and the subsidiary are consolidated

rest with the majority owner.

2-39. The SEC requires that a copy of the companies code of ethics be made

company’s Internet Web Site.

29

2-40. Treadway Commission is the popular name for the National Commission on

and effective internal controls.

2-41. The Sarbanes-Oxley Act requires the auditor to present a report on the

2-42. Audit Report

Report on the firm’s internal controls

2-44. Reasons why some private companies elect to follow the law follow:

2-45. 1. The subsidiary’s accounts are shown separately from the parent’s.

2-46. Control can be gained by means other than obtaining majority stock

and the primary beneficiary.

2-47. Some countries do not consolidate. Other countries use consolidation with

different rules.

30

PROBLEMS

PROBLEM 2-1

Cash

Sales

Dec 6 2,500

Dec 14 3,000

Dec 24 1,200

Dec 10 500

Dec 17 6,000

Dec 28 700

Dec 2 4,000

Dec 6 2,500

Accounts Receivable

Office Salaries

Dec 2 4,000

Dec 21 900

Dec 24 1,200

Dec 10 500

Land

Gain on Sale of Land

2,200 original cost

Dec 14 2,200

Dec 14 800

Equipment

Services

Dec 17 6,000

Dec 21 900

Accounts Payable

Dec 28 700

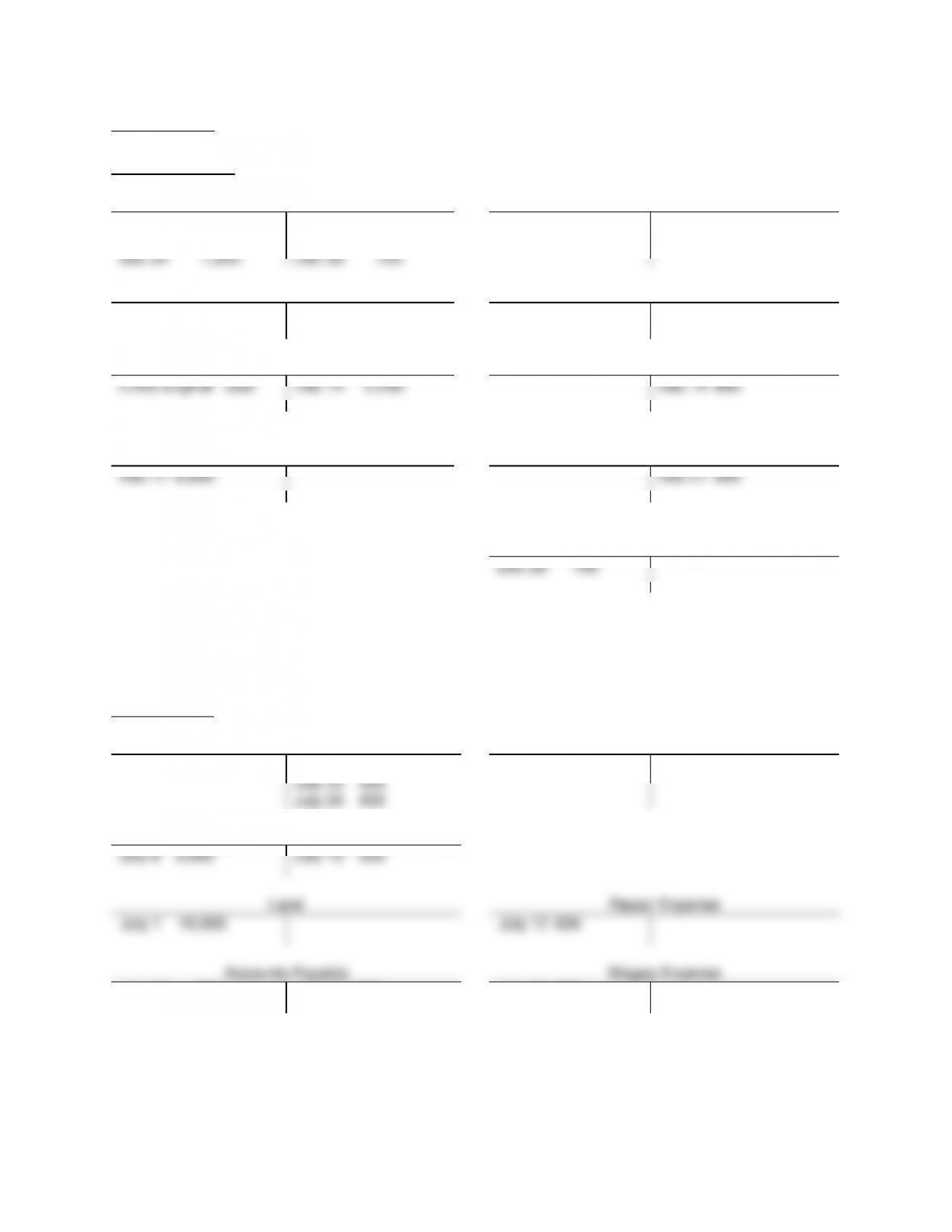

PROBLEM 2-2

Cash

Revenue

July 15 500

July 1 10,000

July 20 300

July 24 400

July 8 3,000

Accounts Receivable

July 8 3,000

July 15 500

Land

Repair Expense

July 1 10,000

July 12 600

Accounts Payable

Wages Expense

July 20 300

July 12 600

July 24 400

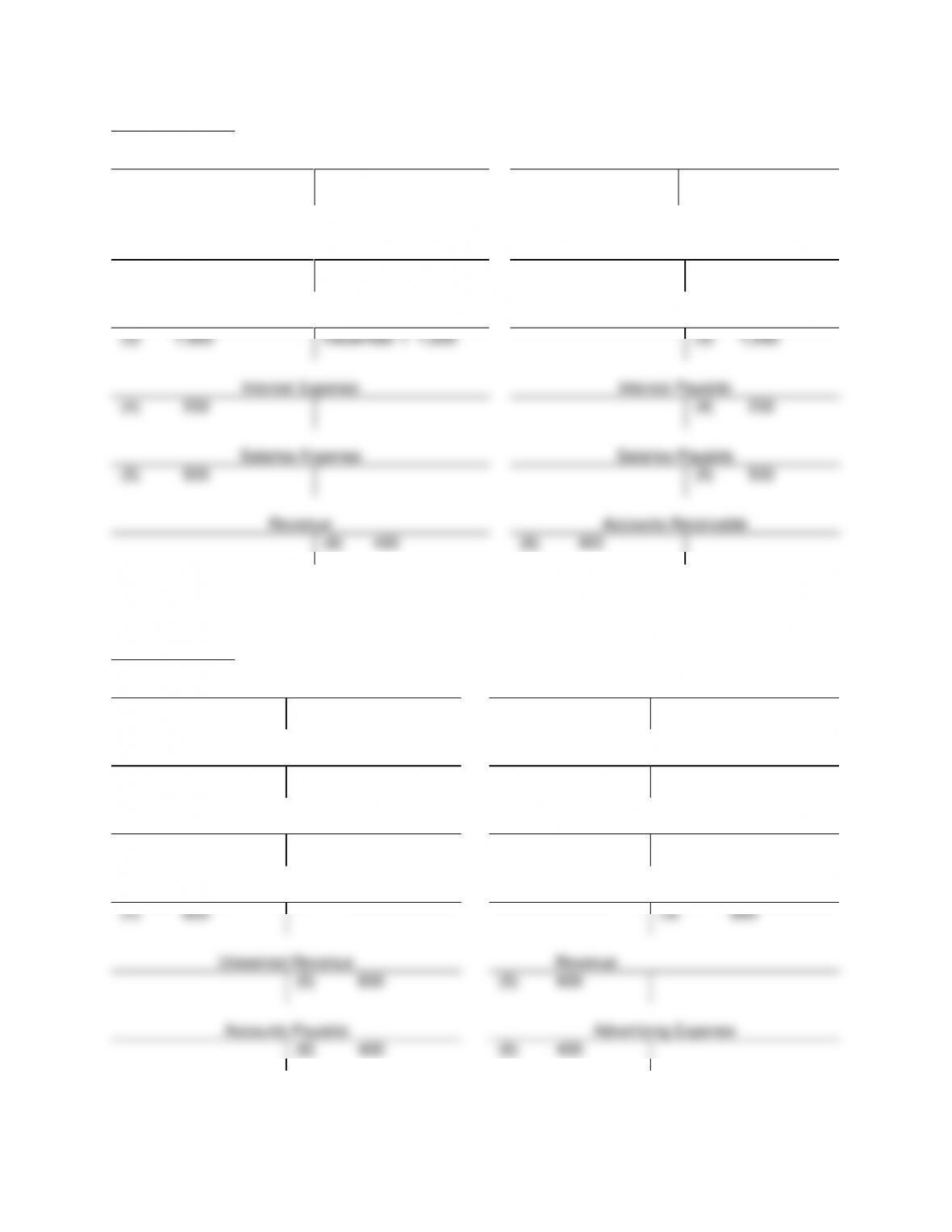

PROBLEM 2-3

Insurance Expense

Prepaid Insurance

(1)December 31 600

July 1 1,200

(1) December 31

600

Supplies Expense

Supplies

(2) 300

September 10 500

(2) 300

Revenue

Unearned Revenue

(3) 1,000

December 1 1,000

(3) 1,000

(4) 200

(4) 200

(5) 500

(5) 500

Revenue

(1) 640

May 1 960

(1) 640

(2) 100

December 1 400

(2) 100

(4) 800

(4) 800

Revenue

(5) 600

(6) 400

(6) 400

32

PROBLEM 2-5

liabilities plus stockholder’s equity.

permanent account.

e. 3 Insurance expense is an income statement account and therefore a

temporary account.

debit.

PROBLEM 2-6

b. 1 An unqualified opinion usually has the highest degree of reliability.

f. 2 Form 10-K is the annual financial report submitted to the Securities

and Exchange Commission.

33

PROBLEM 2-7

statements

fairly, in all material respects, the financial position, results of

complete set of financial statements

e. 1 Financial statements of legally separate entities may be issued to

PROBLEM 2-8

Permanent (P)

or Temporary (T)

Normal Balance

Dr. (Cr.)

Cash

P

Dr.

Accounts receivable

P

Dr.

Equipment

P

Dr.

Accounts payable

P

Cr.

Common stock

P

Cr.

Sales

T

Cr.

Purchases

T

Dr.

Rent expense

T

Dr.

Utility expense

T

Dr.

Selling expenses

T

Dr.

PROBLEM 2-9 PROBLEM 2-10

c 1 c 1

34

PROBLEM 2-11

Prepaid Insurance

Insurance Expense

December 31, 2011 180,000

320,000

X 320,00

Amount paid 310,000

December 31, 2011 170,000