354

Chapter 11

Expanded Analysis

QUESTIONS

11– 1. Based on the study reported in the text, liquidity and debt ratios are regarded

11– 2. (a) Debt/equity, current ratio

(b) Debt/equity, current ratio

11– 3. The dividend payout ratio does not primarily indicate liquidity, debt, or

bank is paid, the dividend payout ratio can be used as an effective ratio.

11– 4. Based on the study reported in the text, financial executives do regard

profitability ratios as the most significant ratios.

11– 5. 1) Earnings per Share – profitability 2) Debt/Equity – debt

11– 6. The CPAs gave the highest significance rating to two liquidity ratios. These

rated debt ratio was debt/equity.

11– 7. According to the study reported in this book, financial ratios are not used

that interpretations and explanations can be made more effectively in a

annual report, except for earnings per share.

11– 8. (a) Financial summary (b) Management highlights

11– 9. Profitability ratios and ratios related to investing are the most likely to be

included in annual reports.

355

11–10. Earnings per share is the only ratio that is required to be disclosed in the

11–11. Presently, no regulatory agency such as the Securities and Exchange

Commission or the Financial Accounting Standards Board accepts

There are many practical and theoretical issues related to the computation of

financial ratios. As long as each individual is allowed to exercise his/her opinion

11–12. Accounting policies that result in the slowest reporting of income are the most

conservative.

11–13.

Conservative

Yes

No

(a)

X

(b)

X

(c)

X

(d)

X

(e)

X

(f)

X

(g)

X

(h)

X

(i)

X

(j)

X

(k)

X

11–14. Substantial research and development will result in more conservative earnings

which they are incurred.

11–15. Such a model could be used by management to take preventive measures.

accounts receivable. An auditor could use such a model to aid in the

11–16. There are many definitions or descriptions of financial failure. Financial failure

356

11–17. (a) Cash flow/Total debt

11–19. Firms that scored below 2.675 are assumed to have similar characteristics of

past failures.

11–20. Variable X4 in the model requires that the market value of the stock be

11–22. The abnormally low turnover for accounts receivable indicates that a very

11–23. A proposed comprehensive budget should be compared with financial ratios

achieve the corporate objectives.

11–24. 1. Line

11–25. 1. Not extending the vertical axis to zero

2. Having a broken vertical axis

11–27. The surveyed analysts gave the highest significance ratings to profitability

ratios.

357

11–29. a. The proper use of estimates and judgments to prepare financial

statements.

manipulate financial statements.

cash flow, and price-to-sales.

11–33. From the Barker study – (analysts and fund managers)

heart of investment decision-making.”

11–34. Traditional financial statements are important when using fundamental

11.35. In an August, 2006 correspondence, the GAO made this comment related to

358

PROBLEMS

PROBLEM 11-1

a.

5

An incorrect presentation in the financial statements should be corrected.

b.

4

Collection of accounts receivable would increase cash but would not

increase working capital.

c.

3

From the expense side, writing off expenditures reduces income and

reduces assets. From the revenue side, not recognizing revenue reduces

income and assets.

d.

4

This type of situation would have high expenses in relation to revenue.

The plant expansion and start-up costs would increase financing

requirements.

e.

3

A high turnover of net working capital would indicate good management

of working capital.

PROBLEM 11-2

a.

1

A decline in the number of days’ sales outstanding will indicate tighter

credit policies. Lower prices might cause more sales and receivables as

would better credit terms. Lower sales would give lower sales per day,

not an overall decline in days’ sales.

b.

2

Financial leverage causes magnification of changes in earnings and is

only good strategy when earnings are stable.

c.

1

This is basically the same as current assets – inventory.

d.

2

The times interest earned ratio measures long-term borrowing ability and

the risk inherent therein.

e.

3

Net income plus income taxes and bond interest expense by annual

bond interest expense would be a reasonable computation of times bond

interest earned.

359

PROMLEM 11-3

a.

1

Multiperiod discounted earnings models is not an example of the use of a

multiple when valuing common equity.

b.

1

Discounted abnormal earnings and residual income.

c.

2

Shareholders of acquired companies are often big winners of “receiving

on average a 20 percent premium in a friendly merger.”

d.

1

Overuse of conventional financial statements was not given as a reason

for acquirers paying too much in an acquisition.

e.

1

The authors referenced in the book maintain that the correct way to value

dot.coms is by using the classic discounted-cash-flow (DCF) approach to

valuating.

PROBLEM 11-4

b. Financial leverage is the extent to which fixed costs of financing are used, namely

debt. The greater the financial leverage, the greater the magnification of changes in

c. The fixed asset turnover has risen, generally indicating either a rise in sales or a

360

PROBLEM 11-5

a. 1. Rate of Return on Total Assets: Return on Assets

Net Income Before

Noncontrolling Interest

– $0.2

(-1.0%)

and Nonrecurring Items

=

=

Average Total Assets

($19.7 + 19.4)/2

Negative

income figure.

2. Acid-Test Ratio:

Cash Equivalents + Marketable

Securities + Net Receivables

=

$13.5 – $2.8 – $0.6

=

1.09

Current Liabilities

$9.3

3. Return on Sales: Net Profit Margin

Net Income Before

Noncontrolling Interest

and Nonrecurring Items

=

– $0.2

=

(–0.8%) Negative

Net Sales

$24.9

4. Current Ratio:

Current Assets

=

$13.5

=

1.45

Current Liabilities

$9.3

5. Inventory Turnover:

Cost of Goods Sold

=

$18.0

=

6 times per year

Average Inventory

($3.2 + $2.8 )/2

b. 1. Rate of Return on Total Assets:

2. Return on Sales:

Unfavorable. The rate is low and has been declining.

361

3. Acid-Test Ratio:

adequate.

4. Current Ratio:

Unfavorable. The decline has been sharp, and the ratio is probably too low.

5. Inventory Turnover:

6. Equity Relationships:

liquidity problems.

7. Asset Relationships:

Neutral. The reduction in the proportion of assets that are current could indicate

that the firm is working its current assets harder. The reduction in the proportion

c. The facts available from the problem are inadequate to make final judgment;

additional information as listed in Part D would be necessary. However, the facts

1. Cash and securities are declining.

The operations of the company also show unfavorable trends:

1. Cost of goods sold is increasing as a percent of sales.

362

3. Recognizing that prices have risen, it appears that physical volume at D. Hawk

might have actually decreased.

controlled and monitored conditions.

d. Additional information would be:

1. Quality of management of D. Hawk Company

2. The locations of the D. Hawk stores

not inventories

8. Normal ratios for the industry

363

PROBLEM 11-6

a. Liquidity Ratios:

1.

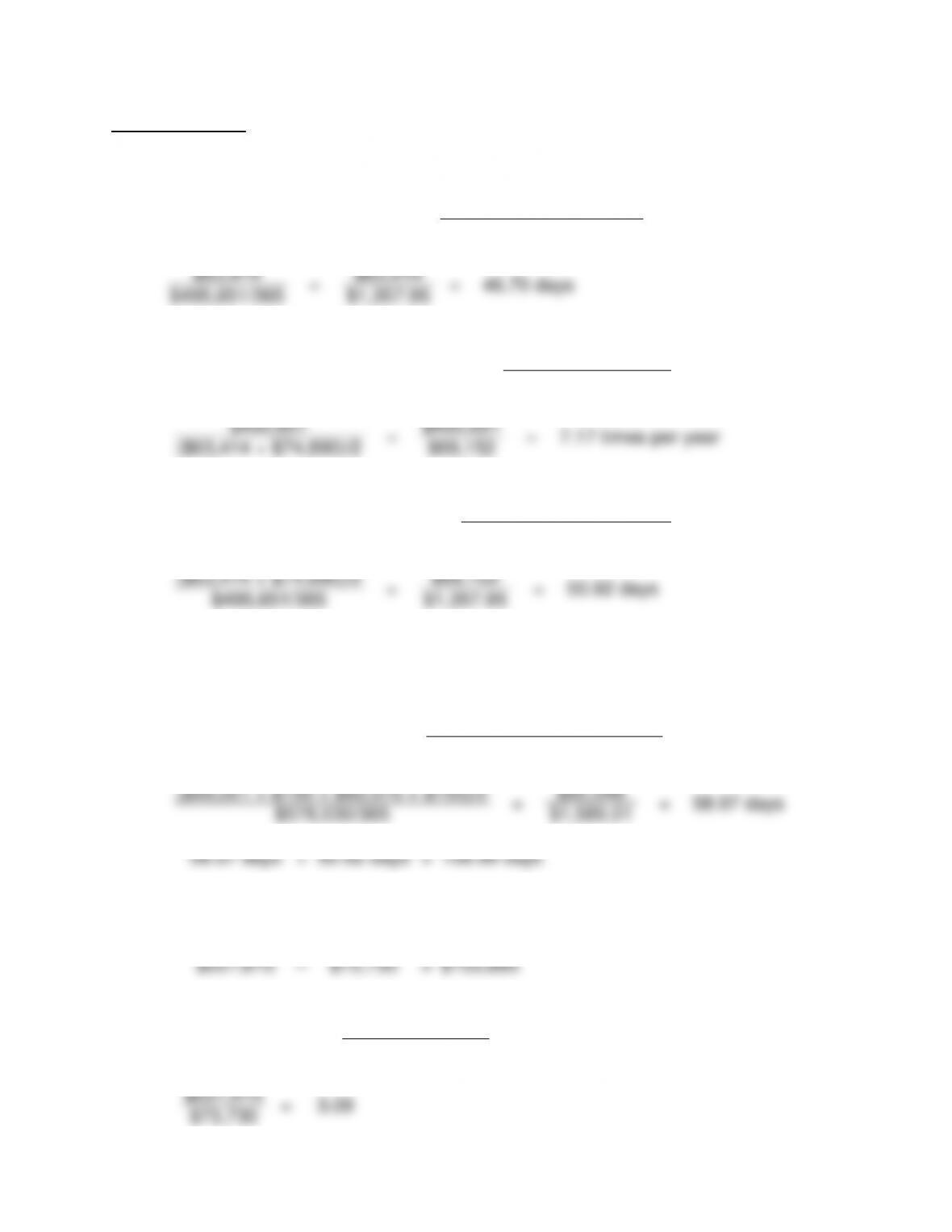

Days’ Sales in Inventory

=

Ending Inventory

Cost of Goods Sold/365

$63,414

=

$63,414

=

46.70 days

$495,651/365

$1,357.95

2.

Merchandise Inventory Turnover

=

Cost of Goods Sold

Average Inventory

$495,651

=

$495,651

=

7.17 times per year

($63,414 + $74,890)/2

$69,152

3.

Inventory Turnover in Days

=

Average Inventory

Cost Of Goods Sold/365

($63,414 + $74,890)/2

=

$69,152

=

50.92 days

$495,651/365

$1,357.95

4.

Operating Cycle

=

Accounts Receivable

Turnover in Days

+

Inventory Turnover

in Days

Accounts Receivable

Turnover in Days

=

Average Gross Receivables

Net Sales/365

($99,021 + $750 + $83,575 + $750)/2

=

$92,048

=

58.07 days

$578,530/365

$1,585.01

58.07 days

+

50.92 days

=

108.99 days

5.

Working Capital

=

Current Assets

–

Current Liabilities

$227,615

–

$73,730

=

$153,885

6.

Current Ratio

=

Current Assets

Current Liabilities

$227,615

=

3.09

$73,730