232

5.

Operating Income Margin

=

Operating Income

Net Sales

2011

2010

2009

(2) Net sales

$

1,600,000

$

1,300,000

$

1,200,000

Less:

Material and manufacturing

costs of products sold

740,000

624,000

576,000

Research and development

90,000

78,000

71,400

General and selling

600,000

500,500

465,000

$

1,430,000

$

1,202,500

$

1,112,400

(1) Operating income

$

170,000

$

97,500

$

87,600

(1) Divided by (2)

10.63%

7.50%

7.30%

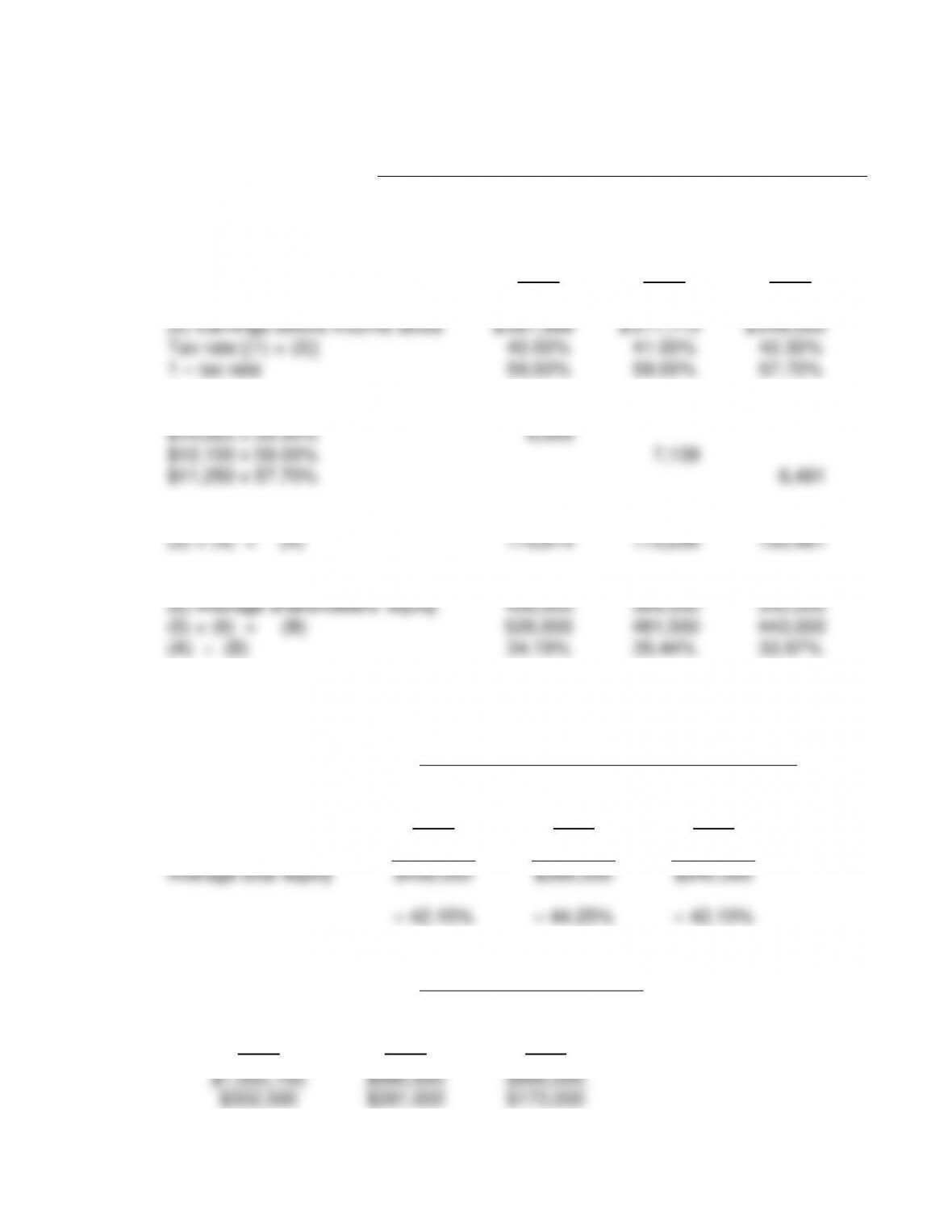

6.

Return on Operating Assets

=

Operating Income

Average Operating Assets

2011

2010

2009

Operating Income

$170,000

$97,500

$87,000

Average Operating Assets

$1,390,200

$1,160,000

$1,090,000

= 12.23%

= 8.41%

= 7.98%

7.

Operating Asset Turnover

=

Net Sales

Average Operating Assets

2011

2010

2009

Net Sales

$1,600,000

$1,300,000

$1,200,000

Average Operating Assets

$1,390,200

$1,160,000

$1,090,000

= 1.15 times

= 1.12 times

= 1.10 times

8. DuPont Analysis with operating ratios

Return on

Operating Assets

=

Net Profit Margin

x

Total Asset Turnover

2011:

12.22%*

=

10.63%

x

1.15

2010:

8.40%*

=

7.50%

x

1.12

2009:

8.03%

=

7.30%

x

1.10

233

9.

Return on Investment

=

Net Income Before Minority Share of Earnings and

Nonrecurring Items + [(Interest Expense) x (1 – Tax Rate)]

Average (Long-Term Liabilities) + Equity

Estimated tax rate:

2011

2010

2009

(1) Provision for income taxes

$

62,049

$

35,731

$

32,659

(2) Earnings before income taxes and

minority equity

$

159,100

$

87,150

$

77,760

(1) ÷ (2)

39.00%

41.00%

42.00%

1 – tax rate

61.00%

59.00%

58.00%

(3) Interest expense x (1 – tax rate)

$19,000 x 61.00%

11,590

$18,200 x 59.00%

10,738

$17,040 x 58.00%

9,883

(4) Earnings before minority equity

97,051

51,419

45,101

(3) + (4) (A)

108,641

62,157

54,984

(5) Total long-term debt

211,100

121,800

214,000

(6) Total stockholders’ equity

811,200

790,100

770,000

(5) + (6) = (B)

1,022,300

911,900

984,000

(A) ÷ (B)

10.63%

6.82%

5.59%

10.

Return on Total Equity

=

Net Income Before Nonrecurring Items –

Dividends on Redeemable Preferred Stock

Average Total Equity

2011

2010

2009

Net income etc.

$

86,851

$

42,919

$

37,001

Average total equity

$

811,200

$

790,100

$

770,000

=10.71%

= 5.43%

= 4.81

b. All ratios computed indicate a significant improvement in profitability.

234

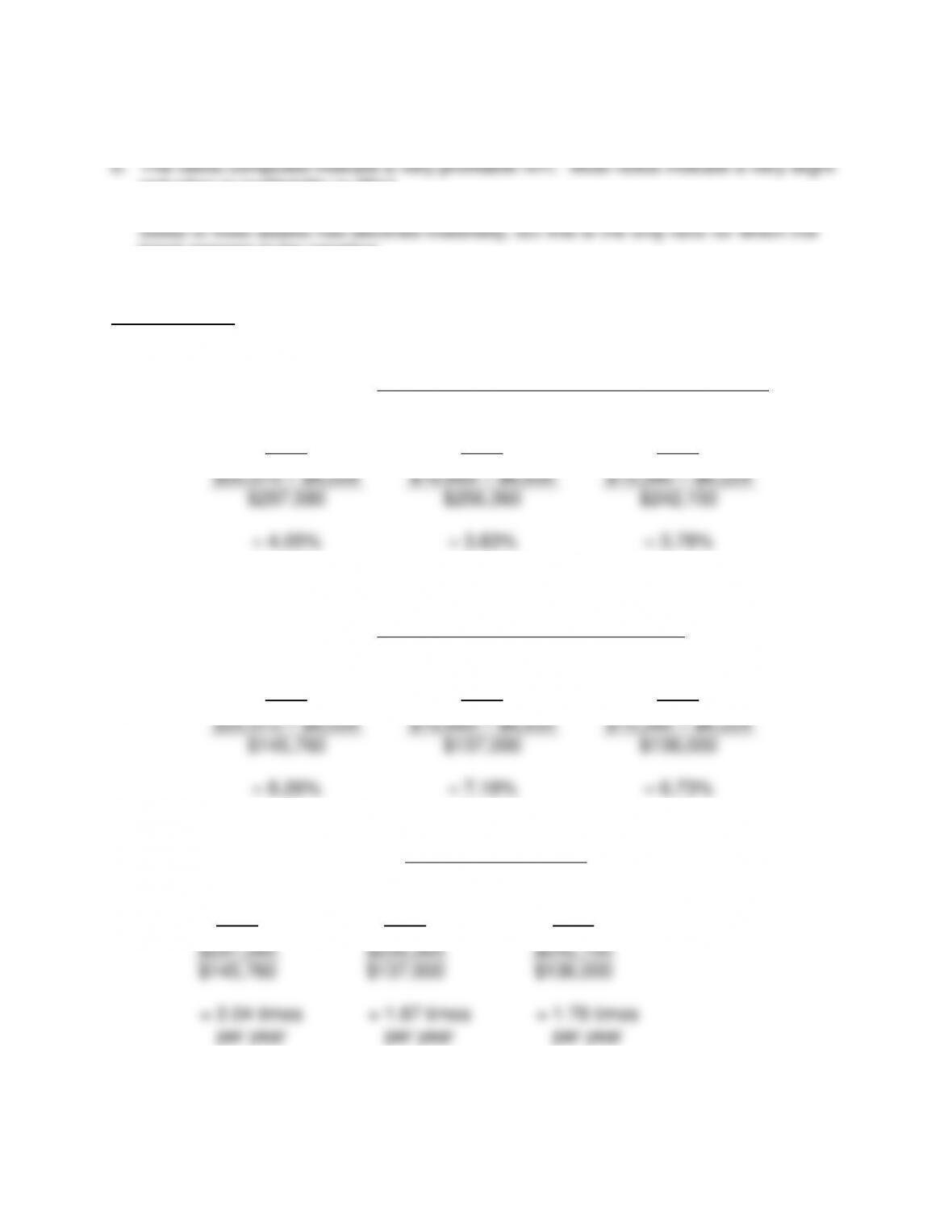

PROBLEM 8-7

a.

1.

Net Profit Margin

=

Net Income Before Noncontrolling Interest,

Equity Income and Nonrecurring Items

Net Sales

2011

2010

2009

$171,115

$163,497

$143,990

$1,002,100

$980,500

$900,000

= 17.08%

= 16.67%

= 16.00%

2.

Return on Assets

=

Net Income Before Noncontrolling

Interest and Nonrecurring Items

Average Total Assets

2011

2010

2009

$171,115

$163,497

$143,990

$839,000

$770,000

$765,000

= 20.40%

= 21.23%

= 18.82%

3.

Total Asset Turnover

=

Net Sales

Average Total Assets

2011

2010

2009

$1,002,100

$980,500

$900,000

$839,000

$770,000

$765,000

= 1.19 times

per year

= 1.27 times

per year

= 1.18 times

per year

4. DuPont Analysis

Return on

Assets

=

Net Profit

Margin

x

Total Asset

Turnover

2011:

20.33%*

=

17.08%

x

1.19 times per year

2010:

21.17%*

=

16.67%

x

1.27 times per year

2009:

18.88%*

=

16.00%

x

1.18 times per year

235

5.

Return on Investment

=

Net Income Before Noncontrolling Interest and

Nonrecurring Items + [(Interest Expense) x (1 – Tax Rate)]

Average (Long-Term Liabilities) + Equity

Estimated tax rate:

2011

2010

2009

(1) Provision for income taxes

$

116,473

$

113,616

$

105,560

(2) Earnings before income taxes

$

287,588

$

277,113

$

249,550

Tax rate [(1) + (2)]

40.50%

41.00%

42.30%

1 – tax rate

59.50%

59.00%

57.70%

(3) Interest expense x (1 – tax rate)

$14,620 x 59.50%

8,699

$12,100 x 59.00%

7,139

$11,250 x 57.70%

6,491

(4) Net earnings

171,115

163,497

143,990

(3) + (4) = (A)

179,814

170,636

150,481

(5) Average long-term debt

120,000

112,000

101,000

(6) Average shareholders’ equity

406,000

369,500

342,000

(5) + (6) = (B)

526,000

481,500

443,000

(A) ÷ (B)

34.19%

35.44%

33.97%

6.

Return on Total Equity

=

Net Income Before Nonrecurring Items –

Dividends on Redeemable Preferred Stock

Average Total Equity

2011

2010

2009

Net earnings

$171,115

$163,497

$143,990

Average total equity

$406,000

$369,500

$342,000

= 42.15%

= 44.25%

= 42.10%

7.

Sales to Fixed Assets

=

Net Sales

Average Net Fixed Assets

2011

2010

2009

$1,002,100

$980,500

$900,000

$302,500

$281,000

$173,000

236

= 3.31

= 3.49

= 5.20

reduction in profitability in 2011.

trend appears to be negative.

PROBLEM 8-8

a.

1.

Net Profit Margin

=

Net Income Before Noncontrolling Interest,

Equity Income and Nonrecurring Items

Net Sales

2011

2010

2009

$20,070 – $8,028

$16,660 – $6,830

$15,380 – $6,229

$297,580

$256,360

$242,150

= 4.05%

= 3.83%

= 3.78%

2.

Return on Assets

=

Net Income Before Minority Share of

Earnings and Nonrecurring Items

Total Assets

2011

2010

2009

$20,070 – $8,028

$16,660 – $6,830

$15,380 – $6,229

$145,760

$137,000

$136,000

= 8.26%

= 7.18%

= 6.73%

3.

Total Asset Turnover

=

Net Sales

Total Assets

2011

2010

2009

$297,580

$256,360

$242,150

$145,760

$137,000

$136,000

= 2.04 times

per year

= 1.87 times

per year

= 1.78 times

per year

237

4. DuPont Analysis

Return on

Assets

=

Operating Income

Margin

x

Total Asset

Turnover

2011:

8.26%

=

4.05%

x

2.04 times

2010:

7.16%*

=

3.83%

x

1.87 times

2009:

6.73%

=

3.78%

x

1.78 times

*Rounding difference from the 7.18% computed in (2).

5.

Operating Income Margin

=

Operating Income

Net Sales

2011

2010

2009

$26,380

$22,860

$20,180

$297,580

$256,360

$242,150

= 8.86%

= 8.92%

= 8.33%

6.

Return on Operating Assets

=

Operating Income

End of Year Operating Assets

2011

2010

2009

$26,380

$22,860

$20,180

$89,800 + $45,850

$84,500 + $40,300

$83,100 + $39,800

= 19.45%

= 18.32%

= 16.42%

7.

Operating Assets Turnover

=

Net Sales

End of Year Operating Assets

2011

2010

2009

$297,580

$265,360

$242,150

$89,800 + $45,850

$84,500 + $40,300

$83,100 + $39,800

= 2.19 times

per year

= 2.13 times

per year

= 1.97 times

per year

238

8. DuPont Analysis

Return on

Operating Assets

=

Operating Income

Margin

x

Operating Asset

Turnover

2011:

19.40%*

=

8.86%

x

2.19 times

2010:

18.29%*

=

8.92%

x

2.05 times

2009:

16.41%*

=

8.33%

x

1.97 times

*Rounding difference from the 19.45%, 18.32%, and 16.42% computed in (6).

9.

Gross Profit Margin

=

Gross Profit

Net Sales

2011

2010

2009

$91,580

$80,060

$76,180

$297,580

$256,360

$242,150

= 30.77%

= 31.23%

= 31.46%

substantial improvement to return on assets.

Operating income margin declined slightly in 2011 after a substantial improvement in

Gross profit margin declined slightly each year.

239

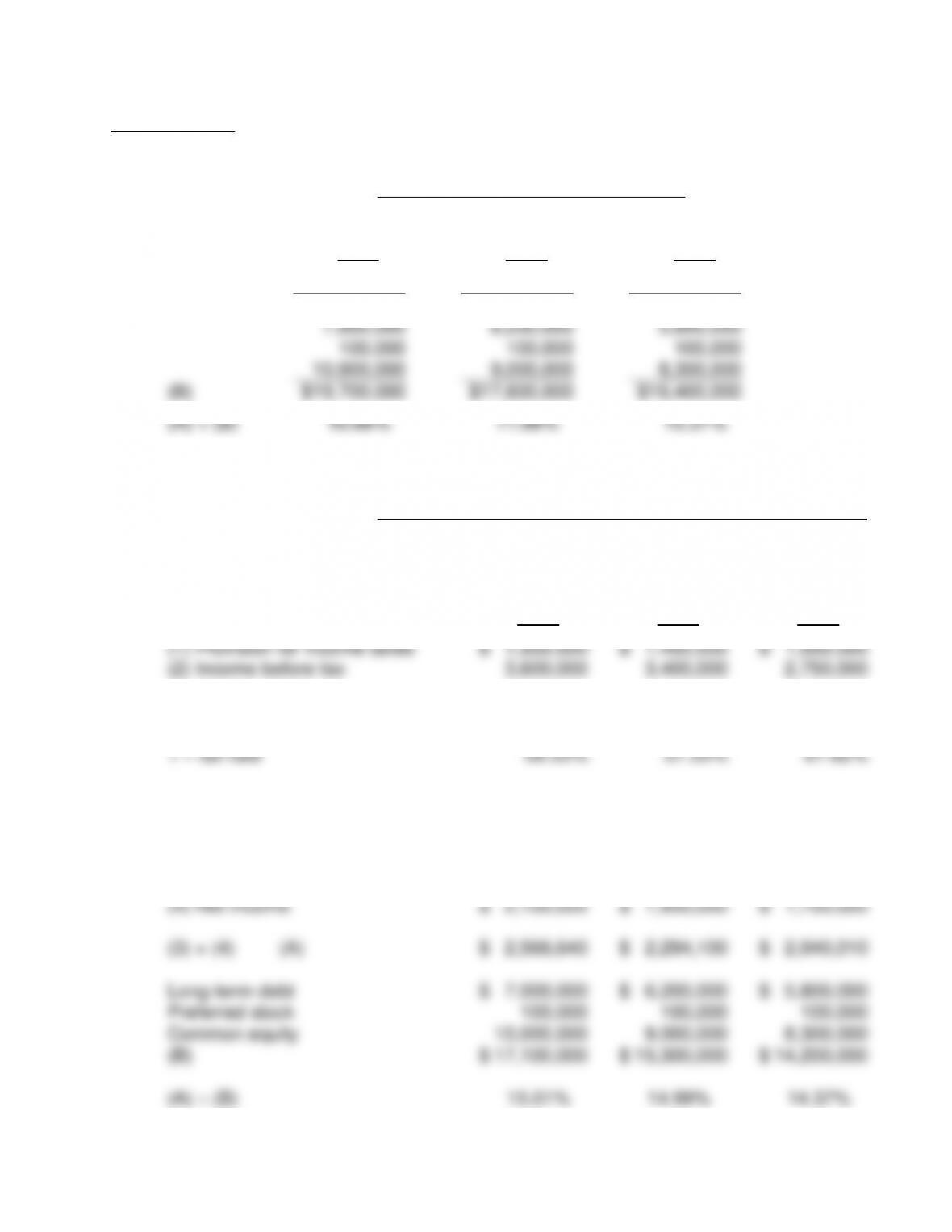

PROBLEM 8-9

a.

1.

Return on Assets

=

Net Income Before Noncontrolling

Interest and Nonrecurring Items

End of Year Total Assets

2011

2010

2009

(A)

$

2,100,000

$

1,950,000

$

1,700,000

$

2,600,000

$

2,300,000

$

2,200,000

7,000,000

6,200,000

5,800,000

100,000

100,000

100,000

10,000,000

9,000,000

8,300,000

(B)

$

19,700,000

$

17,600,000

$

16,400,000

(A) ÷ (B)

10.66%

11.08%

10.37%

2.

Return on Investment

=

Net Income Before Noncontrolling Interest and

Nonrecurring Items + [(Interest Expense) x (1 – Tax Rate)]

End of Year (Long-Term Liabilities + Equity)

Estimated tax rate:

2011

2010

2009

(1) Provision for income taxes

$

1,500,000

$

1,450,000

$

1,050,000

(2) Income before tax

3,600,000

3,400,000

2,750,000

Tax rate = (1) ÷ (2)

41.67%

42.65%

38.18%

1 – tax rate

58.33%

57.35%

61.82%

(3) Interest expense x (1 – tax rate)

$800,000 x 58.33%

$

466,640

$600,000 x 57.35%

$

344,100

$550,000 x 61.82%

$

340,010

(4) Net income

$

2,100,000

$

1,950,000

$

1,700,000

(3) + (4) (A)

$

2,566,640

$

2,294,100

$

2,040,010

Long-term debt

$

7,000,000

$

6,200,000

$

5,800,000

Preferred stock

100,000

100,000

100,000

Common equity

10,000,000

9,000,000

8,300,000

(B)

$

17,100,000

$

15,300,000

$

14,200,000

(A) ÷ (B)

15.01%

14.99%

14.37%

240

3.

Return on Total Equity

=

Net Income Before Nonrecurring Items –

Dividends on Redeemable Preferred Stock

Ending Total Equity

2011

2010

2009

$2,100,000

$1,950,000

$1,700,000

$100,000 + $10,000,000

$100,000 + $9,000,000

$100,000 + $8,300,000

= 20.79%

= 21.43%

= 20.24%

4.

Return on Common Equity

=

Net Income Before Nonrecurring

Items – Preferred Dividends

Ending Common Equity

2011

2010

2009

$2,100,000 – $14,000

$1,950,000 – $14,000

$1,700,000 – $14,000

$10,000,000

$9,000,000

$8,300,000

= 20.86%

= 21.51%

= 20.31%

common equity improved and then declined.

2011.

Return on common equity is slightly more than return on total equity, indicating a

benefit from preferred stock.

benefit from long-term debt.

241

PROBLEM 8-10

a.

Sales

$

120,000

Gross profit (40%)

48,000

Cost of goods sold (60%)

$

72,000

Beginning inventory

$

10,000

+ Purchases

100,000

Total available

$

110,000

– Ending inventory

?

Cost of goods sold

$

72,000

Ending inventory ($110,000 – $72,000)

$

38,000

Sales

$

120,000

Gross profit (50%)

60,000

Cost of goods sold (50%)

$

60,000

Beginning inventory

$

10,000

+ Purchases

100,000

Total available

$

110,000

– Ending inventory

50,000

Cost of goods sold

$

60,000

If gross profit were higher, the loss would be higher because ending inventory would