394

CASE 11-4 BOOKS UNLIMITED (Part 1)

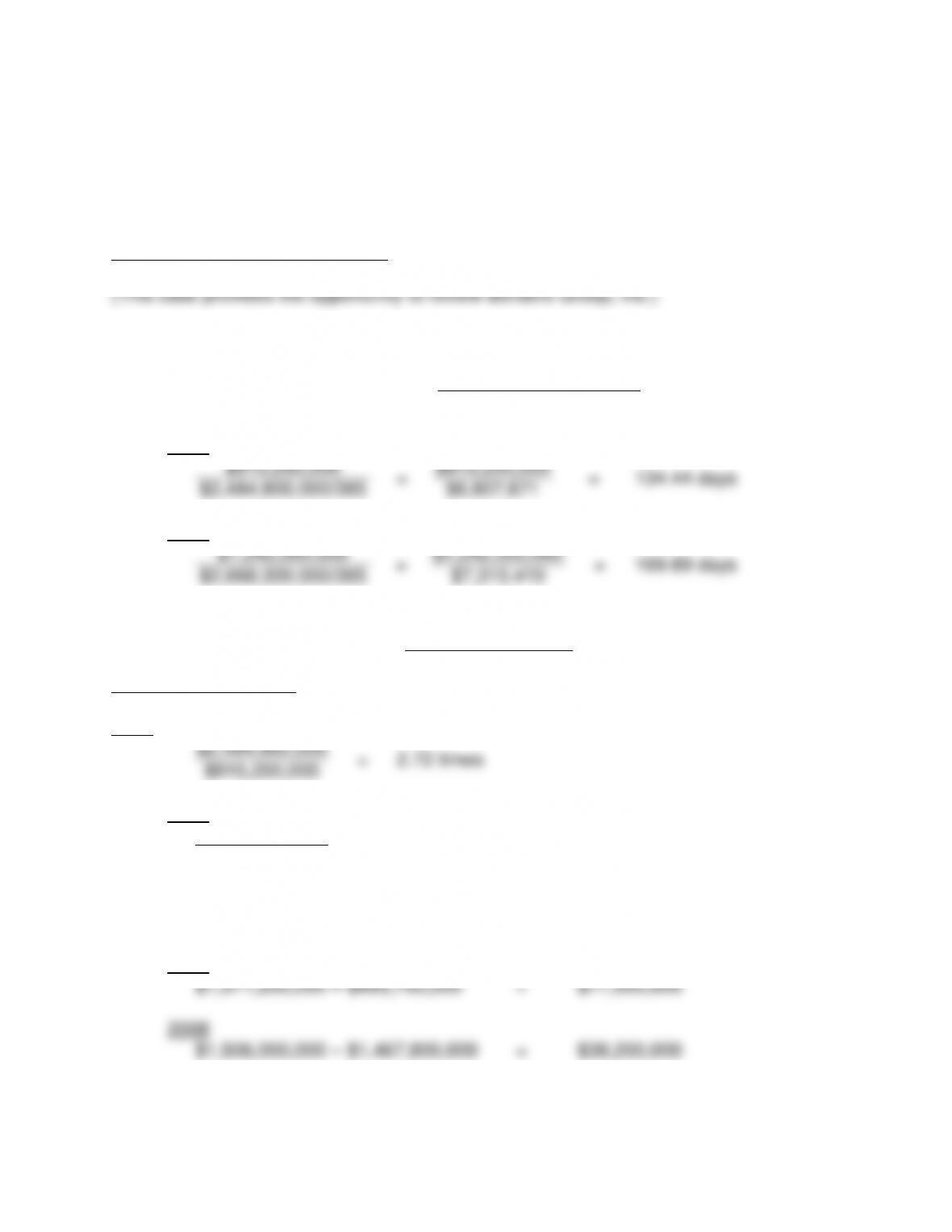

a. Liquidity Ratios

1.

Days’ Sales in Inventory

=

Ending Inventory

Cost of Goods Sold/365

2009

$915,200,000

=

$915,200,000

=

134.44 days

$2,484,800,000/365

$6,807,671

2008

$1,242,000,000

=

$1,242,000,000

=

169.89 days

$2,668,300,000/365

$7,310,410

2.

Inventory Turnover

=

Cost of Goods Sold

Average Inventory

(use ending inventory)

2009

$2,484,800,000

=

2.72 times

$915,200,000

2008

$2,668,300,000

=

2.15 times

$915,200,000

3.

Working Capital

=

Current Assets – Current Liabilities

2009

$1,071,200,000 – $993,700,000

=

$77,500,000

2008

$1,506,000,000 – $1,467,800,000

=

$38,200,000

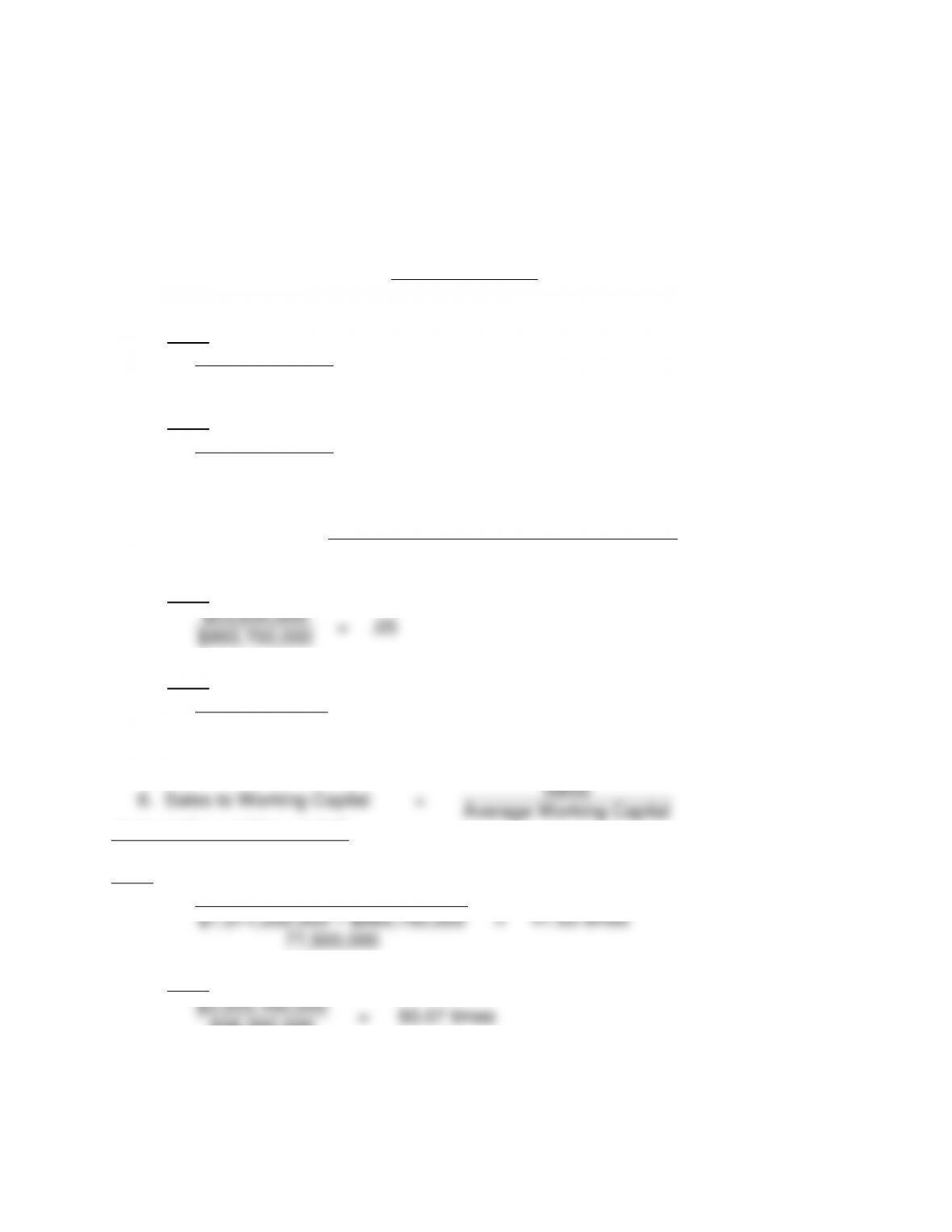

395

4.

Current Ratio

=

Current Assets

Current Liabilities

2009

$1,071,200,000

=

1.08

$993,700,000

2008

$1,506,000,000

=

1.03

$1,467,800,000

5.

Cash Ratio

=

Cash Equivalents + Marketable Securities

Current Liabilities

2009

$53,600,000

=

.05

$993,700,000

2008

$58,500,000

=

.04

$1,467,800,000

6.

Sales to Working Capital

=

Sales

Average Working Capital

(use ending working capital)

2009

$3,242,100,000

=

41.83 times

$1,071,200,000 – $993,700,000

77,500,000

2008

$3,555,100,000

=

93.07 times

$38,200,000

7. Operating Cash Flow / Current Maturities of Long-Term Debt and Current Notes

Payable

396

2009

$233,600,000

=

70.83%

$329,800,000

$105,000,000

=

19.14%

$548,600,000

b. Long-Term Debt-Paying Ability

1.

Debt Ratio

=

Total Liabilities

Total Assets

2009

1,346,400,000

=

83.68%

$1,609,000,000

$1,825,800,000

=

79.29%

$2,302,700,000

2. Operating Cash Flow / Total Debt

2009

$233,600,000

=

17.35%

$1,346,400,000

2008

$105,000,000

=

5.75%

$1,825,800,000

c. Profitability Ratios

1.

Net Profit Margin

=

Net Income Before Noncontrolling Income (loss),

Equity Income and Nonrecurring Items

Net Sales

2009

($184,700,000)

=

Negative

$3,242,100,000

2008

($19,900,000)

=

Negative

$3,555,100,000

2.

Return on Assets

=

Net Income Before Noncontrolling Income

(loss) and Nonrecurring Items

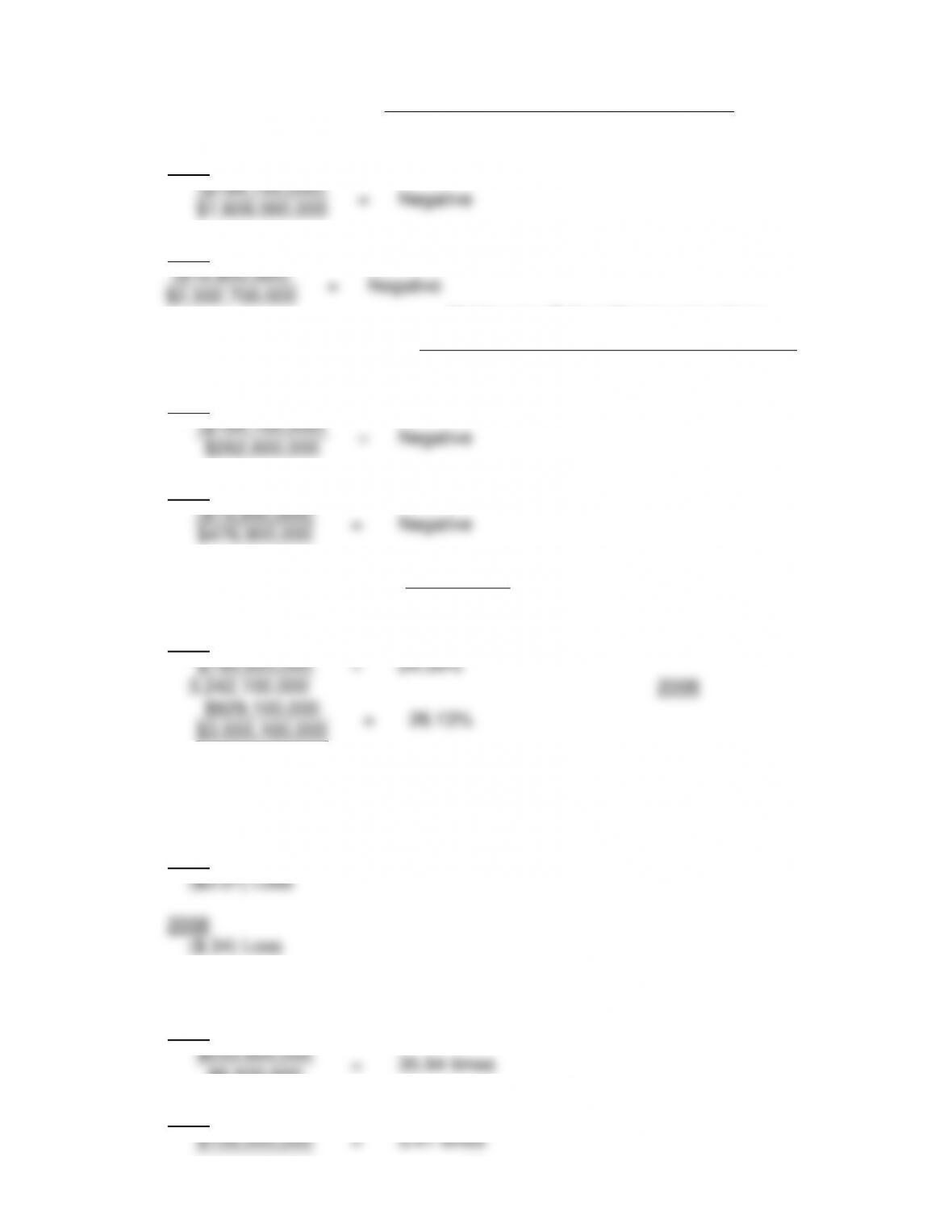

397

Average Total Assets

2009

($184,700,000)

=

Negative

$1,609,000,000

2008

($19,900,000)

=

Negative

$2,302,700,000

3.

Return on Total Equity

=

Net Income Before Nonrecurring Items

– Dividends on Redeemable Preferred Stock

Average Total Equity

2009

($184,700,000)

=

Negative

$262,600,000

2008

($19,900,000)

=

Negative

$476,900,000

4.

Gross Profit Margin

=

Gross Profit

Net Sales

2009

$790,600,000

=

24.39%

3,242,100,000 2008

$929,100,000

=

26.13%

$3,555,100,000

d. Investor Analysis

1. Earnings Per Common Share

2009

2. Operating Cash Flow / Cash Dividends

2009

$233,600,000

=

35.94 times

$6,500,000

2008

$105,000,000

=

5.41 times

398

$19,400,000

e. Liquidity

1. Days’ Sales in Inventory improved materially but still appears to be very high

2. Inventory Turnover improved materially but still appears to be very low

3. Working Capital improved materially

Summary – Liquidity

There were material improvements in liquidity. Several of the areas appear to

Long-Term Debt-Paying Ability

2009

Summary – Long-Term Debt

materially improved in 2009.

Profitability Ratios

1. Net Profit Margin – Negative in both years

Summary – Profitability

Substantial profitability problems.

Investor Analysis

f. Trend in net income (loss) is very negative

399

Net cash provided by operating activities of continuing operations increased

Capital expenditures declined materially each year.

How long can decreasing inventories provide significant cash flow? Can this firm

continue to pay cash dividends?

h. Beaver Study Indicators

1. Cash Flow / Total Debt

2. Net Income / Total Assets

3. Total Debt / Total Assets

came from decreasing inventories.