Archives

978-0324651140 Appendix Solution Manual

A-1 Solutions APPENDIX TIME VALUE OF CASH FLOWS Questions, Exercises, and Problems: Answers and Solutions A.2 The value of cash flows differs over time because cash can earn interest. Extracting, or discounting, the interest element in a future cash flow […]

978-0324651140 Chapter 1 Lecture Note

1-1 Notes CHAPTER 1 INTRODUCTION TO BUSINESS ACTIVITIES AND OVERVIEW OF FINANCIAL STATEMENTS AND THE REPORTING PROCESS I. Learning Objectives 1. Understand four principal activities of business entities: (a) establish goals and strategies, (b) obtain financing, (c) make investments, and […]

978-0324651140 Chapter 1 Solution Manual Part 1

1-1 Solutions CHAPTER 1 INTRODUCTION TO BUSINESS ACTIVITIES AND OVERVIEW OF FINANCIAL STATEMENTS AND THE REPORTING PROCESS Questions, Exercises, and Problems: Answers and Solutions 1.1 The first question at the end of each chapter asks the student to review the […]

978-0324651140 Chapter 1 Solution Manual Part 2

Solutions 1-18 Selling and Administrative Expenses ………….. (4,973) (4,355) (3,921) Other (Income) Expense …………………………… (121) (186) (69) Interest Expense, Net ………………………………. (157) (159) (136) Income Tax Expense ……………………………….. (759) (648) (728) Net Income …………………………………………… $ 1,738 $ 1,354 $ 1,351 […]

978-0324651140 Chapter 10 Lecture Note

10-1 Notes CHAPTER 10 NOTES, BONDS, AND LEASES I. Learning Objectives 1. Develop the skills to compute the issue price, carrying value, and current fair value of notes and bonds payable in an amount equal to the present value of […]

978-0324651140 Chapter 10 Solution Manual Part 1

10-1 Solutions CHAPTER 10 NOTES, BONDS, AND LEASES Questions, Exercises, and Problems: Answers and Solutions 10.2 Generally, accountants initially record assets at acquisition cost and then allocate this amount to future periods as an expense. Changes in the fair value […]

978-0324651140 Chapter 10 Solution Manual Part 2

10–21 Solutions 10.23 d. continued. June 30, 2008 Interest Expense ………………………………………………. 300,000 Cash …………………………………………………………… 300,000 Assets = Liabilities + Shareholders’ Equity (Class.) –300,000 –300,000 IncSt → RE To record interest expense for the first six months. June 30, 2008 Bonds […]

978-0324651140 Chapter 10 Solution Manual Part 3

10–41 Solutions 10.31 continued. g. Carrying Value of Liability: $1,000,000 X 107.1062% ……… $ 1,071,062 h. Interest expense for first six months is $39,535 (= .078/2 X $1,013,711). The carrying value of the liability at the end of the first […]

978-0324651140 Chapter 10 Solution Manual Part 4

10–53 Solutions 10.34 continued. b. Plan (1): Asset—Cash. Plan (2): Operating Lease Method: None. Plan (2): Capital Lease Method Asset—Cash. Asset—Leased Computer System. Asset Contra—Accumulated Depreciation. Liability—Lease Liability. c. $150,000 = $100,000 Depreciation + (.10 X $100,000 X 5) Interest. […]

978-0324651140 Chapter 11 Lecture Note

11– 1 Notes CHAPTER 11 LIABILITIES: OFF-BALANCE-SHEET FINANCING, RETIREMENT BENEFITS, AND INCOME TAXES I. Learning Objectives 1. Understand (a) why and how firms structure financing to keep debt off the balance sheet, and (b) how standard setters have refined the […]

978-0324651140 Chapter 11 Solution Manual Part 1

11-1 Solutions CHAPTER 11 LIABILITIES: OFF-BALANCE-SHEET FINANCING, RETIREMENT BENEFITS, AND INCOME TAXES Questions, Exercises, and Problems: Answers and Solutions 11.2 Using an executory contract to achieve off-balance-sheet financing results in the recognition of neither an asset (for example, leased assets) […]

978-0324651140 Chapter 11 Solution Manual Part 2

11–21 Solutions 11.28 (Woodward Corporation; effect of temporary differences on income taxes.) a. 2008 2009 2010 2011 Other Pre-Tax Income ………….. $ 35,000 $ 35,000 $ 35,000 $ 35,000 Income before Depreciation from Machine ……………………. 25,000 25,000 25,000 25,000 b. […]

978-0324651140 Chapter 11 Solution Manual Part 3

Solutions 11–34 11.33 continued. e. A recognized pension liability or health care liability suggests that a firm has recognized more pension or health care expense than the firm f. GAAP requires firms using the accrual basis of accounting to recognize […]

978-0324651140 Chapter 12 Lecture Note

12– 1 Notes CHAPTER 12 MARKETABLE SECURITIES AND DERIVATIVES I. Learning Objectives 1. Understand why firms acquire securities of other firms and how the purpose of the investment governs the accounting for that investment. 2. Develop skills to account for […]

978-0324651140 Chapter 12 Solution Manual Part 1

12-1 Solutions CHAPTER 12 MARKETABLE SECURITIES AND DERIVATIVES Questions, Exercises, and Problems: Answers and Solutions 12.2 a. Debt securities that a firm intends to hold to maturity (for example, to lock in the yield at acquisition for the full period […]

978-0324651140 Chapter 12 Solution Manual Part 2

12–21 Solutions +2,700 OCInc → AOCInc To revalue Security T to market value. Solutions 12–22 12.16 continued. 2/15/2010 Assets = Liabilities + Shareholders’ Equity (Class.) +14,900 +2,900 IncSt → RE –15,200 –3,200 OCInc → AOCInc To record sale of Security […]

978-0324651140 Chapter 12 Solution Manual Part 3

12–41 Solutions 2008 ………………………. $ 2,300 $ 3,300 $ 3,300 end of 2009 appears in income if these securities are trading securities but in a separate shareholders’ equity account if these securities are se– 2009 ………………………… 5,700 (300) (300) Total […]

978-0324651140 Chapter 12 Solution Manual Part 4

Solutions 12–56 of the note payable at the beginning of the year tractual interest rate of 6% on the face amount of the note ($3,000 = .06 X $50,000), and the increase in the carrying value of the note payable […]

978-0324651140 Chapter 13 Lecture Note

13– 1 Notes CHAPTER 13 INTERCORPORATE INVESTMENTS IN COMMON STOCK I. Learning Objectives 1. Understand why firms invest in the common stock issued by other entities and how the purpose of the investment determines the method of accounting for those […]

978-0324651140 Chapter 13 Solution Manual Part 1

13-1 Solutions CHAPTER 13 INTERCORPORATE INVESTMENTS IN COMMON STOCK Questions, Exercises, and Problems: Answers and Solutions 13.2 Control is present when one entity has sufficient ownership interest or contractual rights to make both strategic and operating decisions for another entity. […]

978-0324651140 Chapter 13 Solution Manual Part 2

13–21 Solutions 13.22 continued. (5) Advance from Joyce Company …………………………… 4,000 Assets = Liabilities + Shareholders’ Equity (Class.) –4,000 –4,000 To record repayment of advance. (6) Retained Earnings …………………………………………….. 20,000 Cash ……………………………………………………………. 20,000 Assets = Liabilities + Shareholders’ Equity (Class.) […]

978-0324651140 Chapter 13 Solution Manual Part 3

13–37 Solutions $20,000/10. Solutions 13–38 13.30 continued. d. and e. Peak Valley Company Company Consolidated Assets Cash ……………………………. $ 13,000 $ 6,000 $ 19,000 Accounts Receivable ……… 42,000 20,000 54,000 Investment in Valley Company (Using the Sales Revenue ……………… $ […]

978-0324651140 Chapter 14 Lecture Note

14-1 Notes CHAPTER 14 SHAREHOLDERS’ EQUITY: CAPITAL CONTRIBUTIONS, DISTRIBUTIONS, AND EARNINGS I. Learning Objectives 1. Understand the different priority claims of common and preferred shareholders on the assets of a firm and the disclosure of those claims in the shareholders’ […]

978-0324651140 Chapter 14 Solution Manual Part 1

14-1 Solutions CHAPTER 14 SHAREHOLDERS’ EQUITY: CAPITAL CONTRIBUTIONS, DISTRIBUTIONS, AND EARNINGS Questions, Exercises, and Problems: Answers and Solutions 14.2 The three provisions provide different benefits and risks to the issuing firm and the investor and should sell at different prices. […]

978-0324651140 Chapter 14 Solution Manual Part 2

14–21 Solutions Solutions 14–22 14.25 continued. d. Land ……………………………………………………………….. 540,000 Treasury Stock—Common [= (4,000 X $12) + Assets = Liabilities + Shareholders’ Equity (Class.) +540,000 +348,000 ContriCap +30,000 ContriCap +162,000 ContriCap 14.26 (Treatment of accounting errors, changes in accounting principles, […]

978-0324651140 Chapter 14 Solution Manual Part 3

14–39 Solutions 14.35 continued. (3) Compensation Expense ……………………………………. 889 Assets = Liabilities + Shareholders’ Equity (Class.) –889 IncSt → RE +889 ContriCap (4) Revenues and Gains Net of Expenses and Losses . 14,065 Retained Earnings ………………………………………… 14,065 Assets = Liabilities […]

978-0324651140 Chapter 15 Lecture Note

15-1 Notes CHAPTER 15 STATEMENT OF CASH FLOWS: ANOTHER LOOK I. Learning Objectives 1. Review the rationale for the statement of cash flows, emphasizing why net income differs from cash flows. 2. Review the T-account procedure, introduced in Chapter 5, […]

978-0324651140 Chapter 15 Solution Manual Part 1

15-1 Solutions CHAPTER 15 STATEMENT OF CASH FLOWS: ANOTHER LOOK Problems and Cases: Answers and Solutions 15.1 (Effects of transactions on statement of cash flows.) a. The journal entry to record this transaction is: b. The journal entry to record […]

978-0324651140 Chapter 15 Solution Manual Part 2

15–13 Solutions 15.5 (Metals Company deriving direct method cash flow from operations using data from T-account work sheet.) (All Dollar Amounts in Millions) (Based on financial statements of Alcoa.) (c)–(d) Sum Across Rows to Derive Direct Receipts and Expenditures Indirect […]

978-0324651140 Chapter 15 Solution Manual Part 3

15–27 Solutions Solutions 15–28 15.10 a. continued. Marketable Accounts Securities Receivable—Net Inventories √ 129,200 √ 371,200 √ 124,100 √ 122,600 √ 312,200 √ 255,200 Prepayments Bond Sinking Fund Investment in Subsidiary √ 22,000 √ 63,000 √ 152,000 (13) 1,400 63,000 […]

978-0324651140 Chapter 15 Solution Manual Part 4

Solutions 15–44 15.12 a. continued. Other Current Deferred Liabilities Long-Term Debt Income Taxes 93 √ 1,678 √ 694 √ Common Stock Retained Earnings Treasury Stock 428 √ 1,648 √ √ 15 4 (19) (2) 59 169 (1) 432 √ 1,758 […]

978-0324651140 Chapter 16 Lecture Note

16-1 Notes CHAPTER 16 SYNTHESIS OF FINANCIAL REPORTING I. Learning Objectives 1. Review the conceptual framework underlying the authoritative guidance for financial reporting and potential changes in that framework. 2. Review financial reporting standards discussed in previous chapters, including instances […]

978-0324651140 Chapter 16 Solution Manual Part 1

16-1 Solutions CHAPTER 16 SYNTHESIS OF FINANCIAL REPORTING Exercises and Problems: Answers and Solutions 16.1 (Identifying accounting principles.) a. FIFO cost flow assumption. e. Weighted-average cost flow assumption. f. Effective interest method. g. Cash flow hedge. h. Market value method. […]

978-0324651140 Chapter 16 Solution Manual Part 2

16–21 Solutions 16.4 continued. l. First 6 Months: .025 X $1,104,650.00 ………………………… $ 27,616.25 a$1,104,650.00 – ($30,000.00 – $27,616.25) = $1,102,266.25. m. Interest Expense ………………………………………………. 20,996 Mortgage Payable …………………………………………….. 19,004 Cash ………………………………………………………….. 40,000 Assets = Liabilities + Shareholders’ Equity (Class.) […]

978-0324651140 Chapter 2 Lecture Note

2-1 Notes CHAPTER 2 THE BASICS OF RECORD KEEPING AND FINANCIAL STATEMENT PREPARTION I. Learning Objectives 1. Learn the conventions of recording transactions, including the dual nature of transactions, T-accounts, and journal entries. 2. Understand how the recording of transactions […]

978-0324651140 Chapter 2 Solution Manual Part 1

2-1 Solutions CHAPTER 2 THE BASICS OF RECORD KEEPING AND FINANCIAL STATEMENT PREPARATION Questions, Exercises, and Problems: Answers and Solutions 2.1 See the text or the glossary at the end of the book. 2.2 Accounting is governed by the balance […]

978-0324651140 Chapter 2 Solution Manual Part 2

2-21 Solutions 2.27 b. continued. (3) Building ……………………………………………………. 3,200 Land …………………………………………………………. 930 Cash ……………………………………………………… 4,130 Assets = Liabilities + Shareholders’ Equity (Class.) +3,200 +930 –4,130 Acquires building costing $3,200 million and land costing $930 million, and pays in cash. (4) […]

978-0324651140 Chapter 2 Solution Manual Part 3

2-41 Solutions 139,800 (12) 24,350 5,800 Solutions 2-42 2.36 a. continued. Deposit with Suppliers (A) Equipment (A) (6) 8,000 (4) 4,000 (5) 10,000 8,000 14,000 Accumulated Depreciation (XA) Note Payable (L) 400 (16) 30,000 (2) 1,500 (17) 1,900 30,000 Accounts […]

978-0324651140 Chapter 2 Solution Manual Part 4

2-61 Solutions Assets = Liabilities + Shareholders’ Equity (Class.) +1,500 –1,500 Dividend Liabilities understated by $1,500 and shareholders’ equity overstated by $1,500. Solutions 2-62 2.41 continued. f. Actual Entries: Machinery ……………………………………………………….. 50,000 Accounts Payable …………………………………………. 50,000 Assets = Liabilities + […]

978-0324651140 Chapter 3 Lecture Note

3-1 Notes CHAPTER 3 BALANCE SHEET: PRESENTING AND ANALYZING RESOURCES AND FINANCING I. Learning Objectives 1. Understand the accounting concepts of assets, liabilities, and shareholders’ equity; including the criteria for recognizing (recording) these items on the balance sheet, determining their […]

978-0324651140 Chapter 3 Solution Manual Part 1

3-1 Solutions CHAPTER 3 BALANCE SHEET: PRESENTING AND ANALYZING RESOURCES AND FINANCING Questions, Exercises, and Problems: Answers and Solutions 3.2 Conservatism emphasizes the early recognition of losses and delayed recognition of gains. Based on the conservatively reported earnings, a shareholder […]

978-0324651140 Chapter 3 Solution Manual Part 2

3-21 Solutions d. Under both U.S. GAAP and IFRS, common stock does not meet the definition of a liability because the firm need not repay the funds in a particular amount at a particular time. e. Under both U.S. GAAP […]

978-0324651140 Chapter 3 Solution Manual Part 3

Solutions 3-38 3.33 a. continued. Noncurrent Liabilities: Long-Term Debt …………………………. $ 180,654 33.3% $ 73,674 21.0% Common Stock …………………………… $ 4,115 0.8% $ 4,113 1.2% Additional Paid-in Capital …………. 63,379 11.7% 56,982 16.2% Less Other Equity Reserves……….. (104,574) (19.3%) (91,244) […]

978-0324651140 Chapter 4 Lecture Note

4- 1 Notes CHAPTER 4 INCOME STATEMENT: REPORTING THE RESULTS OF OPERATING ACTIVITIES I. Learning Objectives 1. Understand the classifications of revenues and expenses on the income statement and the importance of those classifications. 2. Understand the timing of revenue […]

978-0324651140 Chapter 4 Solution Manual Part 1

4-1 Solutions CHAPTER 4 INCOME STATEMENT: REPORTING THE RESULTS OF OPERATING ACTIVITIES Questions, Exercises, and Problems: Answers and Solutions 4.2 Revenues measure the inflow of net assets from operating activities and expenses measure the outflow of net assets consumed in […]

978-0324651140 Chapter 4 Solution Manual Part 2

4-19 Solutions 4.25 (Cemex S.A.B.; income statement formats.) The missing items appear in boldface type below: CEMEX S.A.B. IFRS Income Statements December 31, 2007 and 2006 December 31, 2007 2006 Income (Expense) from Financial Instru- ments ………………………………………………….. 2,387 (161) Other […]

978-0324651140 Chapter 5 Lecture Note

5-1 Notes CHAPTER 5 STATEMENT OF CASH FLOWS: REPORTING THE EFFECTS OF OPERATING, INVESTING, AND FINANCING ACTIVITIES ON CASH FLOWS I. Learning Objectives 1. Understand why using the accrual basis of accounting to prepare the balance sheet and income statement […]

978-0324651140 Chapter 5 Solution Manual Part 1

5-1 Solutions CHAPTER 5 STATEMENT OF CASH FLOWS: REPORTING THE EFFECTS OF OPERATING, INVESTING, AND FINANCING ACTIVITIES ON CASH FLOWS Questions, Exercises, and Problems: Answers and Solutions 5.1 See the text or the glossary at the end of the book. […]

978-0324651140 Chapter 5 Solution Manual Part 2

5.31 continued. c. Inventory ………………………………………………………… 7,500 Accounts Payable ………………………………………….. 7,500 Change in Cash = Change in Liabilities + Change in Shareholders’ Equity – Change in Non-cash Assets +7,500 +7,500 (4) Increases by $7,500; operating increase in cash from increase in […]

978-0324651140 Chapter 5 Solution Manual Part 3

5-41 Solutions 4,394 √ √ 1,259 Solutions 5-42 5.36 continued. b. GTI, INC. Statement of Cash Flows For 2007 and 2008 2008 2007 Operations: Sale of Patents ………………………………………… $ 63 $ — Acquisition of Property, Plant and Equip- ment …………………………………………………… […]

978-0324651140 Chapter 5 Solution Manual Part 4

5-53 Solutions 5.42 (Swoosh Shoes, Inc.; interpreting the statement of cash flows.) a. Swoosh Shoes’ growth in sales and net income led to increases of b. Swoosh Shoes increased its acquisitions of property, plant and equipment to provide the firm […]

978-0324651140 Chapter 6 Lecture Note

6-1 Notes CHAPTER 6 INTRODUCTION TO FINANCIAL STATEMENT ANALYSIS I. Learning Objectives 1. Understand the relation between the expected return and risk of investment alternatives and the role financial statement analysis plays in providing information about returns and risk. 2. […]

978-0324651140 Chapter 6 Solution Manual Part 1

6-1 Solutions CHAPTER 6 INTRODUCTION TO FINANCIAL STATEMENT ANALYSIS Questions, Exercises, and Problems: Answers and Solutions 6.2 The increase in the cost of goods sold to sales percentage could result from increases in the purchase prices of inventory items or […]

978-0324651140 Chapter 6 Solution Manual Part 2

6-21 Solutions b.5(23,063 + 20,178) = 21,620.5. c.5(20,178 + 26,175) = 23,176.5. Solutions 6-22 6.22 b. continued. Accounts Receivable Turnover Ratio Accounts Receivable Year Numerator Denominator Turnover Ratio Inventory Turnover Ratio Inventory Year Numerator Denominator Turnover Ratio 2005 30,435 […]

978-0324651140 Chapter 6 Solution Manual Part 3

6-41 Solutions Thus, Carrefour appears to use financial leverage more effectively than Target and Wal-Mart. One might question Carrefour’s greater use of financial leverage, given its weaker profitability. Question d. addresses the risk levels of these firms. Solutions 6-42 6.28 […]

978-0324651140 Chapter 6 Solution Manual Part 4

Solutions 6-56 6.32 continued. in cash and marketable securities. It generates interest revenue from these investments, which it includes in other revenues. It is interesting to This leaves Firms (3) and (5) as Nestle and Toyota Motor in some combination. […]

978-0324651140 Chapter 7 Lecture Note

7-1 Notes CHAPTER 7 REVENUE RECOGNITION, RECEIVABLES, AND ADVANCES FROM CUSTOMERS I. Learning Objectives 1. Understand and apply the criteria for recognizing revenue, including the timing of the recognition and measurement of revenue. 2. Understand the relation between revenues (an […]

978-0324651140 Chapter 7 Solution Manual Part 1

7-1 Solutions CHAPTER 7 REVENUE RECOGNITION, RECEIVABLES, AND ADVANCES FROM CUSTOMERS Questions, Exercises, and Problems: Answers and Solutions 7.2 The cost recovery method defers revenue recognition past the point where the seller has delivered goods to the customer. It is […]

978-0324651140 Chapter 7 Solution Manual Part 2

7.21 (Abson Corporation; journal entries for service contracts.) a. 1/31/08–3/31/08 Cash ………………………………………………………………. 180,000 Service Contract Fees Received in Advance ……. 180,000 Assets = Liabilities + Shareholders’ Equity (Class.) +180,000 –180,000 To record sale of 300 annual contracts. 3/31/08 7-21 Solutions […]

978-0324651140 Chapter 7 Solution Manual Part 3

7-41 Solutions 7.40 continued. c. The contract has three elements: quarterly service (fair value of $320 January 4, 2008: Journal entry to record contract for pest control services. Cash ………………………………………………………………. 300 Advances from Customer ……………………………… 300 Assets = Liabilities + […]

978-0324651140 Chapter 7 Solution Manual Part 4

7-61 Solutions 7.48 continued. c. The percentage-of-completion method probably gives the best measure 7.49 (Furniture Retailers; revenue recognition when payment is uncertain.) a. Installment Method (1) January 2008 Accounts Receivable ………………………………………… 8,400 Inventory …………………………………………………….. 6,800 Deferred Gross Margin …………………………………. 1,600 […]

978-0324651140 Chapter 8 Lecture Note

8-1 Notes CHAPTER 8 WORKING CAPTIAL I. Learning Objectives 1. Identify the principal components of working capital (other than accounts receivable and advances from customers, discussed in Chapter 7, and marketable securities, discussed in Chapter 12) and the business transactions […]

978-0324651140 Chapter 8 Solution Manual Part 1

8-1 Solutions CHAPTER 8 WORKING CAPITAL Questions, Exercises, and Problems: Answers and Solutions 8.3 The underlying principle is that acquisition cost includes all costs required to prepare an asset for its intended use. Assets provide future services. Costs that a […]

978-0324651140 Chapter 8 Solution Manual Part 2

8-21 Solutions Plus Warranty Expense for 2009: .06 X $18,000 ……………. 1,080 Less Actual Warranty Costs (Plug) ……………………………….. (870) Balance, December 31, 2009 ………………………………………. $ 1,535 Plus Warranty Expense for 2010: .06 X $16,000 ……………. 960 Less Actual Warranty Costs […]

978-0324651140 Chapter 8 Solution Manual Part 3

Solutions 8-38 8.42 (Fortune Brands; lower of cost or market; U.S. GAAP versus IFRS.) a. No journal entry will be recorded because U.S. GAAP does not permit firms to writeup the value of their inventory above its acquisition cost. Raw […]

978-0324651140 Chapter 9 Lecture Note

9-1 Notes CHAPTER 9 LONG-LIVED TANGIBLE AND INTANGIBLE ASSETS: I. Learning Objectives 1. Understand the concepts distinguishing expenditures on long-lived assets that qualify for asset recognition from expenditures that firms treat as expenses in the period incurred. 2. Understand the […]

978-0324651140 Chapter 9 Solution Manual Part 1

9-1 Solutions CHAPTER 9 LONG-LIVED TANGIBLE AND INTANGIBLE ASSETS Questions, Exercises, and Problems: Answers and Solutions 9.2 The central concept underlying GAAP for these three items is the ability to identify and reliably measure expected future benefits. The self-constructed building […]

978-0324651140 Chapter 9 Solution Manual Part 2

Solutions 9-20 Assets = Liabilities + Shareholders’ Equity (Class.) –375 –375 IncSt → RE $3,000 X .25 X 6/12 = $375. 9-21 Solutions 9.28 a. continued. Accumulated Depreciation …………………………………. 1,875 Equipment ……………………………………………………. 2,200 Assets = Liabilities + Shareholders’ Equity (Class.) […]

978-0324651140 Test Bank Chapter 1 Part 1

Chapter 1 1. The managers of a business prepare financial statements to present meaningful information about that business’s activities to external users, 2. The independent external auditors of a business prepare financial statements to present meaningful information about that business’s […]

978-0324651140 Test Bank Chapter 1 Part 2

97. The _____ basis of accounting typically recognizes revenue when a firm sells goods (manufacturing and retailing firms) or renders services (service firms), and recognizes expenses in the period when the firm recognizes the revenues that the costs helped produce. […]

978-0324651140 Test Bank Chapter 10 Part 1

Chapter 10 1. Firms typically finance long-term assets, particularly property, plant, and equipment, with long-term borrowing or funds provided directly or indirectly by shareholders. 2. The more long-term debt in a firm’s capital structure, the less the risk that the […]

978-0324651140 Test Bank Chapter 10 Part 2

93. Harris Corporation Harris Corporation issued $2,000,000, 10-percent, 10-year bonds on January 2, Year 2. The bonds pay interest semiannually on January 1 and July 1. The bonds were priced on the market to yield 8 percent. Refer to the […]

978-0324651140 Test Bank Chapter 10 Part 3

122. What are the general principles for measuring financial instruments. MEASUREMENT OF FINANCIAL INSTRUMENTS: GENERAL PRINCIPLES The term financial instrument refers to a financial arrangement in which a firm contracts to receive or make specified payments in the future in […]

978-0324651140 Test Bank Chapter 11 Part 1

Chapter 11 1. Many off-balance-sheet financings fall into one of two categories that accounting typically does not recognize as liabilities: executory contracts and contingent obligations. 2. U.S. GAAP and IFRS provide guidance for deciding whether a given financing arrangement appears […]

978-0324651140 Test Bank Chapter 11 Part 2

89. GKC Corporation GKC Corporation entered into noncancelable, long-term material contracts with suppliers for the purchase of raw materials beginning in the calendar Year 4. These contracts amounted to $500,000 at December 31, Year 4, relating to raw materials with […]

978-0324651140 Test Bank Chapter 11 Part 3

2011 Income Tax Expense 19,000 Deferred Tax Liability 3,400 Cash or Income Tax Payable 22,400 112. What is off-balance-sheet financing? How are they structured? How are they treated under U.S. GAAP and IFRS. OFF-BALANCE-SHEET FINANCING Off-balance-sheet financing refers to obtaining […]

978-0324651140 Test Bank Chapter 12 Part 1

Chapter 12 1. A firm initially records the purchase of marketable securities at acquisition cost, which includes the purchase price plus any commissions, taxes, and other appropriate costs incurred. 2. The term marketable securities refers to the financial instruments that […]

978-0324651140 Test Bank Chapter 12 Part 2

78. Which of the following is/are elements of a derivative? 79. Which of the following is/are elements of a derivative? A. Many derivatives require no initial investment, that is, no initial cash payment to the counterparty. B. A derivative may […]

978-0324651140 Test Bank Chapter 12 Part 3

127. Mo Company acquired $500,000 face value of the outstanding bonds of Shemp Company on January 1, 2008. The bonds pay interest semiannually on June 30 and December 31 at an annual rate of 7% and mature on December 31, […]

978-0324651140 Test Bank Chapter 13 Part 1

Chapter 13 1. The accounting for investments in common stock depends on (1) the expected holding period, and (2) the purpose of the investment, as determined by both the percentage held and management intent. 2. Securities that firms expect to […]

978-0324651140 Test Bank Chapter 13 Part 2

a. 25% b. $110 c. $138 71. The Seagram Company owns 25 percent of the shares of DuPont, and accounts for its investment using the equity method. During the year DuPont earned income of $1,500 million and declared dividends. Seagram’s […]

978-0324651140 Test Bank Chapter 14 Part 1

Chapter 14 1. Shareholders’ equity is a residual interest. It represents the shareholders’ claim on the assets of a firm after the firm satisfies all higher-priority claims. 2. All corporations must issue preferred stock. FALSE 3. Common and preferred stock […]

978-0324651140 Test Bank Chapter 14 Part 2

101. Firms occasionally issue stock options in order to 102. The Prime Corporation is a new company about to issue stock. The corporation sells 2,000 shares of common stock (par value $2) at $10 per share. The journal entry to […]

978-0324651140 Test Bank Chapter 14 Part 3

182. Which of the following is/are true concerning accumulated other comprehensive income? 183. Which of the following is/are not true concerning accumulated other comprehensive income? A. Firms measure marketable equity securities classified as available for sale at fair value and […]

978-0324651140 Test Bank Chapter 14 Part 4

225. Discuss the reasons that investors buy preferred stock and the dividend rights of preferred stockholders. Owners of preferred stock have a claim on the assets of a firm that is senior to the claim of common shareholders. Preferred shares […]

978-0324651140 Test Bank Chapter 14 Part 5

239. Describe the accounting for stock splits and reverse stock splits. STOCK SPLITS Stock splits (or, more technically, split-ups) resemble stock dividends. The corporation issues additional shares of stock to shareholders in proportion to their existing holdings. The firm receives […]

978-0324651140 Test Bank Chapter 15 Part 1

Chapter 15 1. Net income for a particular period will likely differ from cash flow from operations for the same period. 2. Firms typically report cash flows from operations using the direct method. FALSE 3. The proper interpretation of information […]

978-0324651140 Test Bank Chapter 15 Part 2

81. Eight Corporation declared and paid $90,000 of dividends to its shareholders during Year 3. The statement of cash flows classifies the transaction as a(n) 82. During Year 7, Seven Corporation wrote down marketable equity securities to their market value. […]

978-0324651140 Test Bank Chapter 15 Part 3

110. (CMA adapted, Jun 94 #4) Marathon Corporation, a public company, has prepared all of its year-end financial statements with the exception of the statement of cash flows. Presented below is condensed financial information for the years ended May 31, […]

978-0324651140 Test Bank Chapter 16 Part 1

Chapter 16 1. The current FASB’s financial reporting objectives identify current and potential investors and creditors as the principal users of financial reports. 2. The current FASB’s financial reporting objectives states that the principal purpose of financial reports is to […]

978-0324651140 Test Bank Chapter 16 Part 2

94. Which of the following is true? 95. Which of the following is not true? A. Acquisition cost for a merchandising firm includes the costs incurred to purchase and transport the inventory prior to sale. B. Acquisition cost for a […]

978-0324651140 Test Bank Chapter 16 Part 3

164. Which of the following is/are true? 165. Which of the following is/are true regarding the classification of redeemable preferred shares on the balance sheet? A. The classification of redeemable preferred shares on the balance sheet depends on the conditions […]

978-0324651140 Test Bank Chapter 16 Part 4

192. Discuss the definition, recognition, and measurement of liabilities. The criteria for recognition of a liability are as follows: 1. The obligation represents a present obligation, not a potential future commitment or intent. 2. The obligation exists as a result […]

978-0324651140 Test Bank Chapter 2 Part 1

Chapter 2 1. The balance sheet groups individual accounts by type (asset, liability, or shareholders’ equity) and lists these accounts with their balances as of the balance sheet date. 2. The date of the balance sheet appears at the bottom […]

978-0324651140 Test Bank Chapter 2 Part 2

91. Monmath Corp. started operations in March of Year 3. The following transactions occur during March. a. On March 1, Year 3, Monty contributes $20,000 for 10,000 shares of $1 par value stock. b. On March 1, Year 3, Monmath […]

978-0324651140 Test Bank Chapter 2 Part 3

102. Complete the shareholders’ equity section for each of the following independent situations. CASE A CASE B CASE C Common stock, 10,000 shares A C E Additional paid-in capital 25,000 D 30,000 Retained earnings 45,000 25,000 20,000 Total shareholders’ equity […]

978-0324651140 Test Bank Chapter 3 Part 1

Chapter 3 1. A balance sheet prepared according to U.S. GAAP lists assets from most liquid to least liquid, where liquid refers to the ease of converting the asset into cash. 2. A balance sheet prepared according to U.S. GAAP […]

978-0324651140 Test Bank Chapter 3 Part 2

109. The shareholders’ equity section of the balance sheet for a corporation generally does not include 110. Before preparing the balance sheet and income statement, an accountant would use what accounting record to first record the firm’s transactions? A. the […]

978-0324651140 Test Bank Chapter 4 Part 1

Chapter 4 1. Revenues measure the inflow of net assets from operating activities. 2. Expenses measure the outflow of net assets consumed in the process of generating revenues. TRUE 3. Cost is the economic sacrifice made to acquire goods or […]

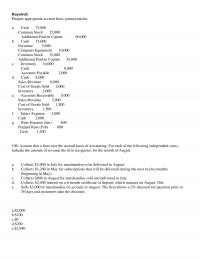

978-0324651140 Test Bank Chapter 4 Part 2

Required: Prepare appropriate accrual basis journal entries. 100. Assume that a firm uses the accrual basis of accounting. For each of the following independent cases, indicate the amount of revenue the firm recognizes for the month of August. a. Collects […]

978-0324651140 Test Bank Chapter 4 Part 3

Below is the income statement for Year 8 that was prepared after making appropriate adjusting entries for Year 8. Spiller Services Corporation Income Statement For the Year Ended December 31, Year 8 Fee Revenues $199,400 Interest Revenue on Notes Receivable […]

978-0324651140 Test Bank Chapter 5 Part 1

Chapter 5 1. A profitable firm can never run out of cash. 2. Using the accrual basis of accounting to measure net income creates the need for a separate financial statement that reports the impact of operations on cash flows. […]

978-0324651140 Test Bank Chapter 5 Part 2

97. Increased earnings 98. A mature, stable firm might show what type of cash flow pattern from operating, investing, and financing activities? A. operating outflow, investing outflow, and financing inflow B. operating inflow, investing outflow, and financing inflow C. operating […]

978-0324651140 Test Bank Chapter 5 Part 3

Morrissey Corporation Statement of Cash Flows For the Year Ended December 31, Year 8 Operations Net Income $1,204 Depreciation 370 Gain on Sale of Equipment (60) Increase in Accounts Receivable (160) Increase in Prepayments (70) Decrease in Income Tax Payable […]

978-0324651140 Test Bank Chapter 6 Part 1

Chapter 6 1. The return from investing in the shares of common stock has two components: cash dividends and the change in the market price of the common stock. 2. Theoretical and empirical research has shown that the expected return […]

978-0324651140 Test Bank Chapter 6 Part 2

99. The rate at which accounts receivable turnover 100. The fixed asset turnover ratio A. measures the relation between sales and the investment in fixed assets such as property, plant, and equipment B. measures the amount of sales generated from […]

978-0324651140 Test Bank Chapter 6 Part 3

128. Devlin Company Devlin Company Statement of Financial Position as of May 31 (in thousands) Assets Year 7 Year 6 Current assets Cash $ 45 $ 38 Trading securities 30 20 Accounts receivable (net) 68 48 Inventories 90 80 Prepaid […]

978-0324651140 Test Bank Chapter 6 Part 4

a. Three ratios that address how profitable a company might be include the total assets turnover, net profit margin, and inventory turnover. The total assets turnover ratio measures the efficiency of resource use, i.e., the ability to generate sales through […]

978-0324651140 Test Bank Chapter 6 Part 5

168. Describe the disaggregation of the rate of return on common shareholders’ equity. DISAGGREGATING THE RATE OF RETURN ON COMMON SHAREHOLDERS’ EQUITY ROCE disaggregates into several components (in a manner similar to the disaggregation of ROA): Thus, The profit margin […]

978-0324651140 Test Bank Chapter 7 Part 1

Chapter 7 1. If an event or transaction leads to the recognition of revenue, firms match the consumption of any assets (the expense), in time, with the revenue recognized. 2. Notes receivable is the amount owed to a seller by […]

978-0324651140 Test Bank Chapter 7 Part 2

74. In year 1, Southern Construction agrees to construct a school building for $12,000,000, receiving payments for the work of $6,000,000 in both year 1 and year 2. Southern estimates that the costs will be $4,000,000 in Year 1 and […]

978-0324651140 Test Bank Chapter 7 Part 3

A. $ 600,000 B. $ 500,000 C. $1,200,000 D. $1,000,000 E. $ 360,000 F. $ 300,000 G. $ 240,000 H. $ 200,000 I. $2,400,000 J. $2,000,000 K. $ 0 L. $ 0 M. $ 600,000 N. $ 500,000 O. $1,200,000 […]

978-0324651140 Test Bank Chapter 8 Part 1

Chapter 8 1. The current–noncurrent distinction refers to whether a firm will convert an asset to cash, or consume it, or sell it within one operating cycle and whether a firm will pay or otherwise settle a liability within one […]

978-0324651140 Test Bank Chapter 8 Part 2

91. Western Inc.’s beginning inventory is $20,000 and purchases for the year are $80,000. A physical inventory shows that $15,000 of the inventory remains at year end. How much is recorded as cost of goods sold for the year? 92. […]

978-0324651140 Test Bank Chapter 8 Part 3

Good Stuff Manufacturing Income Statement For the Month Ending April 30, Year 1 Sales $10,000 Less: Operating expenses Cost of Goods Sold $6,500 Sales Salaries Expense 1,000 Rent Expense 2,000 Utilities Expense 200 9,700 Net Income $ 300 123. Inventory […]

978-0324651140 Test Bank Chapter 9 Part 1

Chapter 9 1. The amount of goodwill represents the excess of the total purchase price over the fair value of identifiable tangible and intangible net assets. 2. Long-lived financial assets include investments in securities. TRUE 3. U.S. GAAP requires firms […]

978-0324651140 Test Bank Chapter 9 Part 2

102. U.S. GAAP provisions require a three-step procedure for measuring and recording impairments for long-lived assets other than nonamortized intangibles and goodwill. An asset impairment loss arises when the carrying values of the assets 103. Applying IFRS, the test for […]

978-0324651140 Test Bank Chapter 9 Part 3

158. Describe several issues in the accounting for long-lived assets. Long-lived assets include both tangible assets, such as land, buildings, and equipment, and intangible assets, such as patents, brand names, trademarks, customer lists, airport landing rights, and franchise rights. Long-lived […]