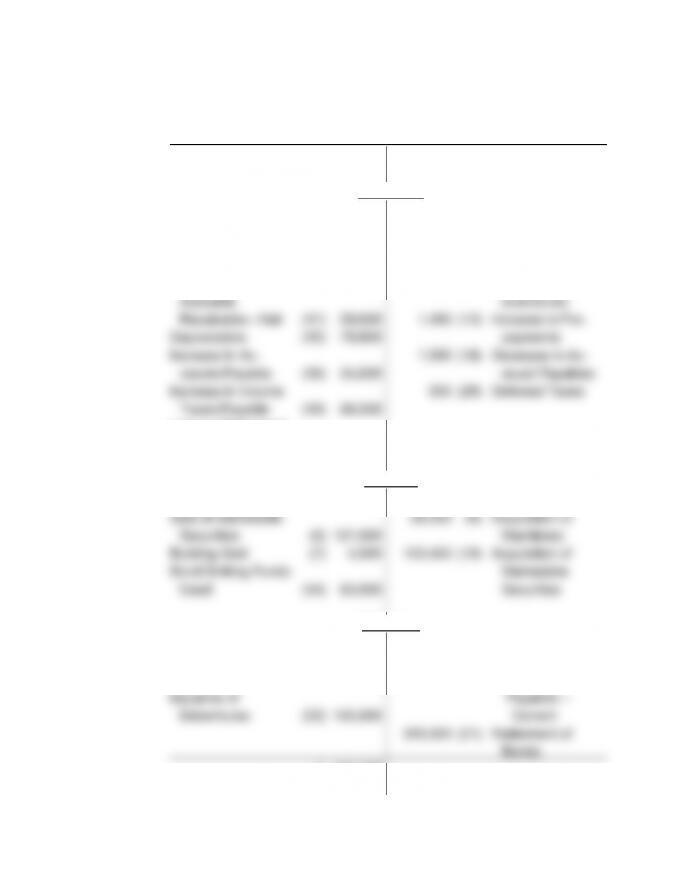

15–13 Solutions

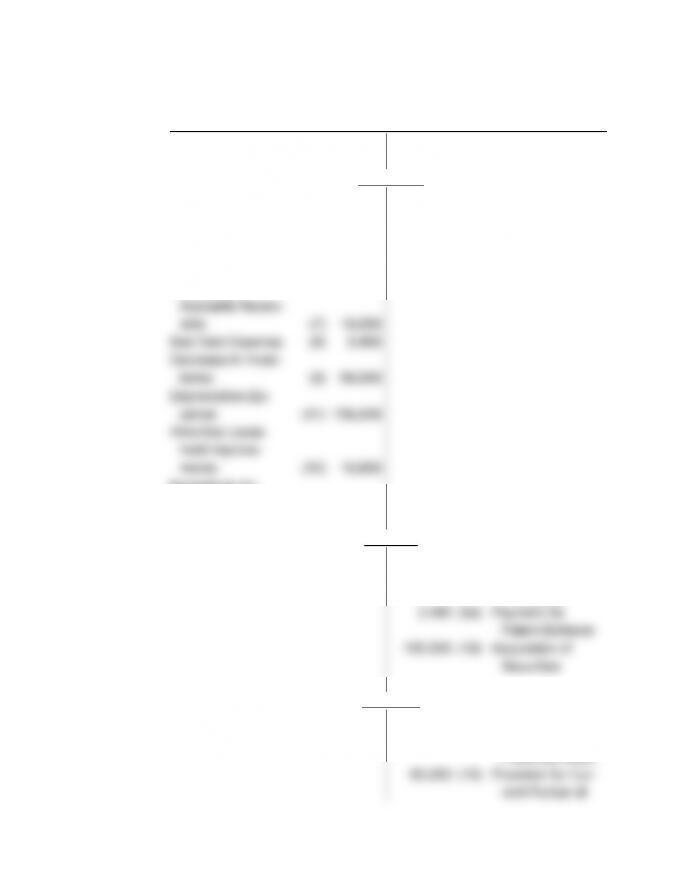

15.5 (Metals Company deriving direct method cash flow from operations using data from T-account work

sheet.) (All Dollar Amounts in Millions) (Based on financial statements of Alcoa.)

(c)–(d) Sum Across Rows to Derive Direct Receipts and Expenditures

Indirect

Changes in

Direct

From Operations:

Operations

Method

Related Balance Sheet Accounts from T-Account Work

Sheet

Method

Receipts Less Expenditures

(a)

(b)

(c)

(d)

Sales Revenues ……………..

$20,465.0

$74.6

= Accounts Receivable Decrease

20,539.6

Receipts from Customers

Gain on Sale of Marketable

Equity Securities ……………

20.8

(20.8)

Gain Produces No Operating Cash

–

Equity in Earnings of

Affiliates ……………………….

214.0

(47.1)

Alcoa’s Share of Earnings Retained by Affiliates

166.9

Receipts for Equity

Method Investments

Cost of Goods Sold …………

(9,963.3)

664.0

Depreciation on Manufacturing Facilities

(9,464.3)

Payments for Inventory

33.9

= Accounts Payable Increase

(198.9)

= Increase in Inventories

General and Administrative

(5,721.3)

Payments for General and

Expenses ……………………..

(5,570.2)

(40.3)

= Prepayments Increase

Administrative Services

(110.8)

= Decrease in Other Current Liabilities

Interest Expense ……………..

(2,887.3)

–

(2,887.3)

Payments for Interest

Income Tax Expense ……….

(911.6)

82.0

Deferred Income Taxes Uses no Cash this Period

(829.6)

Payment for Income Taxes

Net Income …………………….

= $1,367.4

= 1,367.4

Totals …………………………..………..

$1,804.0

= Cash Flow from Operations

$1,804.0

= Cash Flow from Operations Derived via Indirect Method

Derived via Direct Method

Solutions 15–14

15.6 (Ingers Company; working backwards from statement of cash flows.)

(2) Cash (Operations—Depreciation Expense Add-

back) ………………………………………………………….. 179.4

Accumulated Depreciation …………………………. 179.4

(6) Cash (Operations—Decrease in Accounts Re-

ceivable) ……………………………………………………… 50.9

Accounts Receivable …………………………………. 50.9

(7) Inventories ……………………………………………………. 15.2

Cash (Operations—Increase in Inventories) …….. 15.2

15–15 Solutions

Solutions 15–16

15.6 continued.

(13) Marketable Securities ……………………………………….. 4.6

Cash (Investing—Acquisition of Marketable

Securities) ……………………………………………….. 4.6

(17) Long-Term Debt Payable ………………………………….. 129.7

Cash (Financing—Repayment of Long-Term

Debt) ………………………………………………………. 129.7

(18) Cash (Financing—Issue of Common Stock

under Option Plan) ……………………………………….. 47.9

Common Stock, Additional Paid-in Capital ……. 47.9

(21) Leasehold Asset ………………………………………………. 147.9

Capitalized Lease Obligation …………………………. 147.9

(22) Preferred Stock ……………………………………………….. 62.0

Common Stock, Additional Paid-in Capital ……….. 62.0

15–17 Solutions

15.7 (Warren Corporation; preparing a statement of cash flows.)

a. Cash

√ 223,200

Operations

Net Income (5) 234,000

Loss on Sale of Ma-

chinery (1b) 15,600

Amortize Patent (2b) 5,040

Decrease in

Increase in Ac-

counts Payable (13) 153,360

Investing

Sale of Machinery (1b) 57,600 463,200 (1a) Acquisition of

Machinery

Financing

13,200 (3) Retirement of

Preferred Stock

Solutions 15–18

Serial Bonds

√ 174,000

15–19 Solutions

15.7 a. continued.

Allowance for Un-

Accounts Receivable collectible Accounts Inventory

√ 327,600 20,400 √ √ 645,600

3,600 (6) (6) 3,600 2,400 (8) 66,000 (9)

18,000 (7)

√ 306,000 19,200 √ √ 579,600

Leasehold Allowance for

Improvements Amortization Patents

√ 104,400 58,800 √ √ 36,000

10,800 (12) (2a) 2,400 5,040 (2b)

√ 104,400 69,600 √ √ 33,360

Bonds Payable

Accounts Payable Dividends Payable (Current)

126,000 √ — √ 60,000 √

153,360 (13) 48,000 (4) (15) 60,000 60,000 (14)

279,360 √ 48,000 √ 60,000 √

Solutions 15–20

506,400 √

15–21 Solutions

15.7 continued.

b. WARREN CORPORATION

Statement of Cash Flows

For the Year Ending June 30, 2009

Operations:

Net Income ………………………………………………. $ 234,000

Loss on Sale of Machinery …………………………. 15,600

Depreciation …………………………………………….. 106,800

Amortization of Leasehold Improvements …….. 10,800

Cash Flow from Operations……………………………. $ 612,000

Investing:

Sale of Machinery …………………………………….. $ 57,600

Payment of Legal Fee for Patent Defense … …. (2,400)

Acquisition of Securities for Plant Expan–

sion …………………………………………………….. (180,000)

Acquisition of Machinery ……………………………. (463,200)

Solutions 15–22

15.8 (Roth Company; preparing a statement of cash flows.)

a. Cash

√ 37,950

Operations

Net Income (1) 95,847 3,600 (2) Gain on Sale of

Bond Discount Marketable

Amortization (6) 225 Securities

Depreciation (10) 1,875 16,050 (4) Gain on Condem-

Increase in Income nation of Land

Investing

Sale of Marketable 122,250 (5) Acquisition of

Financing

Issuance of Bonds (7) 97,500

Marketable

Securities Accounts Receivable Inventory

15–23 Solutions

Solutions 15–24

15.8 a. continued.

Accumulated Investment in

Depreciation 30%-Owned Company Other Assets

Accounts Payable Dividends Payable Income Taxes Payable

31,830 √ -0- √ -0- √

25,995 √ 12,000 √ 51,924 √

Deferred

Unrealized Holding

Loss on Marketable

15–25 Solutions

15.8 continued.

b. ROTH COMPANY

Statement of Cash Flows

For the Three Months Ended March 31, 2009

Operations:

Net Income ………………………………………………. $ 95,847

Equity in Earnings …………………………………….. (8,640)

Increase in Accounts Receivable ………………… (37,500)

Increase in Inventories …………………………..….. (26,250)

Decrease in Accounts Payable …………………… (5,835)

Cash Flow from Operations……………………………. $ 52,500

Investing:

Proceeds from Sale of Marketable Securi-

ties ……………………………………………………… $ 17,400

Supplementary Information

Holders of the firm’s preferred stock converted shares with a carrying

value of $45,000 into shares of common stock.

Solutions 15–22

15.8 continued.

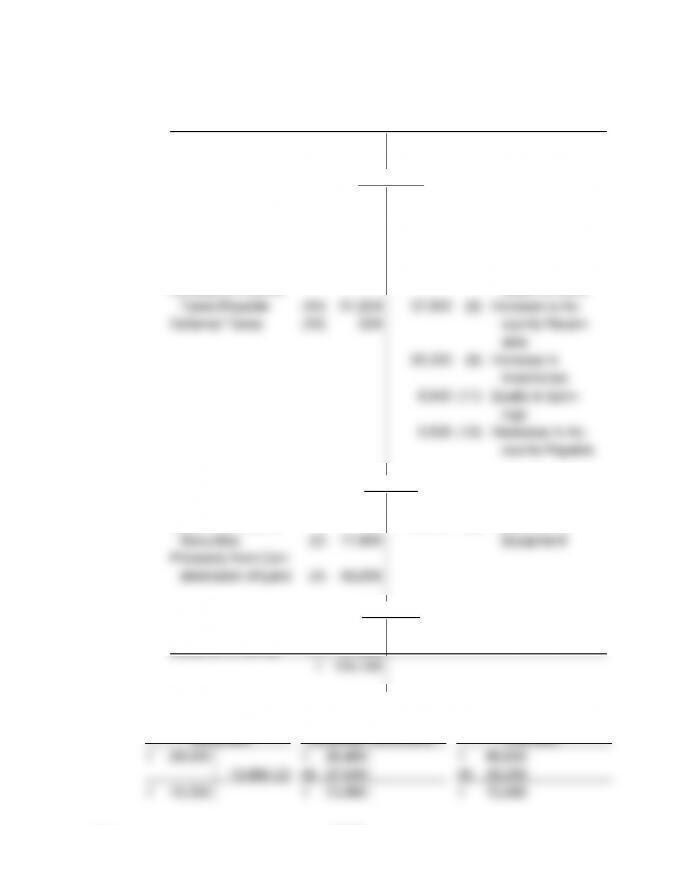

c. Roth deriving direct method cash flow from operations using data from T-account work sheet.

(a) (The letters correspond to the column headers in the exhibit below.) Copy Income Statement and Cash Flow from Operations

(b) Copy Information from T-Account Work Sheet Next to Related Income Statement Item

(c) – (d) Sum Across Rows to Derive Direct Receipts and Expenditures

Indirect

Changes in

Direct

From Operations:

Operations

Method

Related Balance Sheet Accounts from T-Account Work

Sheet

Method

Receipts Less Expenditures

(a)

(b)

(c)

(d)

Sales …………………………….

$364,212

$(37,500

)

= Accounts Receivable Increase

326,712

Receipts from Customers

Gain on Sale of Marketable

Equity Securities ……………

3,600

(3,600)

Gain Produces No Operating Cash

—

Equity in Earnings of

30%-Owned Company……

8,640

(8,640)

Roth’s Share of Earnings Retained by Affiliates

—

Receipts for Equity

Method Investments

Gain on Condemnation

of Land…………………………

16,050

(16,050)

—

Proceeds of Land

Condemnation

Cost of Sales ………………….

(207,612)

Depreciation on Manufacturing Facilities

(239,697)

Payments for Inventory

(5,835)

= Accounts Payable Increase

(26,250)

= Increase in Inventories

General and Administrative

Expenses ……………………..

(33,015)

= Prepayments Increase

(33,015)

Payments for Selling and

= Decrease in Other Current Liabilities

Administrative Services

Depreciation …………………..

(1,875)

1,875

—

Interest Expense ……………..

(1,725)

225

Bond Discount Amortization Uses No Cash this Period

(1,500)

Payments for Interest

Income Tax Expense ……….

(52,428)

504

Deferred Income Taxes Uses no Cash this Period

—

Payment for Income Taxes

51,924

= Increase in Income Taxes Payable

15–23 Solutions

Net Income …………………….

$95,847

= 95,847

Totals …………………………..………..

$52,500

= Cash Flow from Operations

$52,500

= Cash Flow from Operations Derived via Indirect Method

Derived via Direct Method

15–23 Solutions

15.9 (Biddle Corporation; preparing a statement of cash flows.)

a. Cash

√ 45,000

Operations

Investing

Sale of Equipment (4) 9,500 42,500 (6) Acquisition of

Land

Financing

19,000 (3) Retirement of

Bonds, Includ-

ing Income

Solutions 15–24

15.9 a. continued.

Plant and Accumulated

Equipment Depreciation Patents

√ 316,500 50,000 √ √ 16,500

26,500 (4) (4) 15,000 10,000 (9) 1,500 (10)

√ 290,000 45,000 √ √ 15,000

Deferred Income

Accounts Payable Accrued Liabilities Taxes

100,000 √ 105,000 √ 50,000 √

15–25 Solutions

15.9 continued.

b. BIDDLE CORPORATION

Statement of Cash Flows

For the Year Ended December, 2009

Operations:

Income from Continuing Operations …………….. $ 54,500

Loss on Sale of Equipment ………………………… 2,000

Depreciation …………………………………………….. 10,000

Amortization …………………………………………….. 1,500

Deferred Income Taxes ……………………………… 20,000

Increase in Accounts Payable …………………….. 30,000

Increase in Accounts Receivable ………………… (35,000)

Solutions 15–26

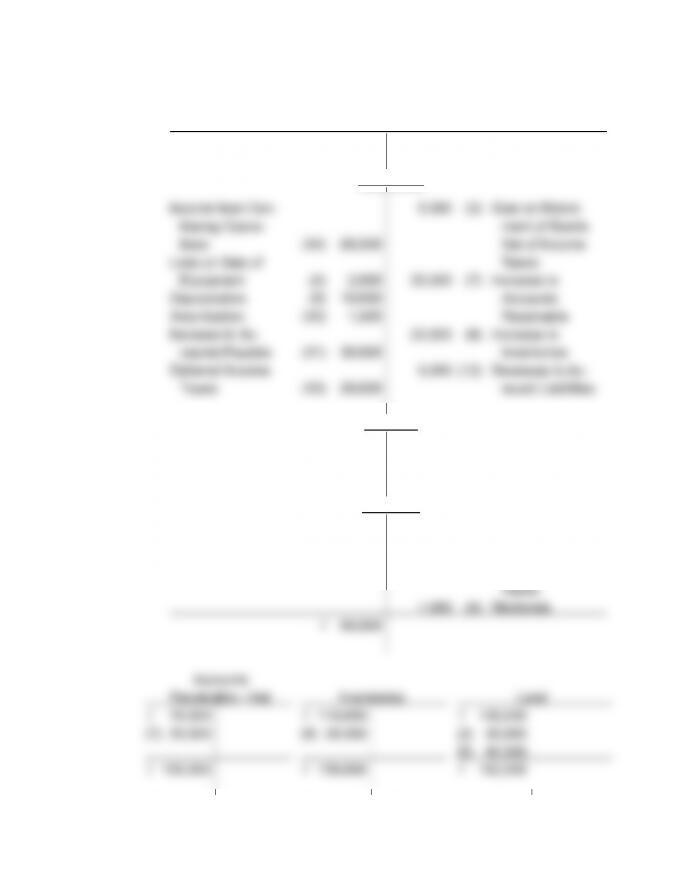

15.10 (Plainview Corporation; preparing a statement of cash flows.)

a. Cash

√ 165,300

Operations

Net Income (1) 236,580 17,000 (5) Gain on Sale of

Loss from Fire (6) 35,000 Marketable

Equity in Loss (9) 17,920 Securities

Decrease in 131,100 (12) Increase in

Loss on Retirement

of Bonds (21) 5,000

Investing

Financing

Re-issue of Treasury 130,000 (2) Dividends

Stock (3) 6,000 145,000 (17) Payment of Note

√ 142,100