1-1 Notes

CHAPTER 1

INTRODUCTION TO BUSINESS ACTIVITIES AND

OVERVIEW OF FINANCIAL STATEMENTS

AND THE REPORTING PROCESS

I. Learning Objectives

1. Understand four principal activities of business entities: (a) establish goals

and strategies, (b) obtain financing, (c) make investments, and (d) conduct

operations.

2. Understand the purpose and content of the principal financial statements:

(a) balance sheet, (b) income statement, and (c) statement of cash flows, and

(d) statement of shareholders’ equity.

3. Understand the roles of participants in the financial reporting process,

including managers and governing boards, accounting standard setters and

regulators, independent external auditors, and financial statement users.

4. Gain an awareness of financial reporting as part of a global system for

providing information for resource allocation decisions, including the

existence of two financial reporting systems (U.S. GAAP and International

Financial Reporting Standards).

5. Understand the difference between the cash basis and the accrual basis of

accounting, and why the latter provides a more informative measure of

performance.

II. Organization of Class Sessions

Coverage of this chapter requires three class sessions. However, if students

have read the first chapter prior to the initial class meeting, one session should

be sufficient. We proceed with the assumption that the latter is generally not

the case and the instructor devotes two class sessions to this chapter.

During the first class session, we overview the principal activities of a

business and the content of the four principal financial statements. We provide

each student with a recent copy of the annual report of a publicly-held

corporation. We select a firm whose annual report is not too complicated and is

likely to be of interest to students (for Example, Microsoft, PepsiCo, Nike,

McDonalds). The annual reports of most corporations are available online.

Students seem to appreciate the immediate link with the real world as they begin

their study of accounting. We consider the four statements separately and

discuss the types of information each attempts to convey, continually relating

each financial statement to the principal activities of a business. Efforts to show

Notes 1-2

the relations among the four financial statements during the first class session

are likely to be ineffective. The students’ subsequent reading of the chapter

serves to reinforce the points made and provides them with a head start as they

prepare for the second class session.

During the second class session, we examine the content of each of the four

principal financial statements in greater depth and the relations between the

statements. Because most students at the introductory accounting level learn by

doing, we use several of the numerical exercises and problems at the end of the

chapter. These exercises and problems emphasize particular concepts within, or

relations between, the four principal financial statements and are

straightforward; by referring to material in the chapter, students would

experience little difficulty in solving them.

During the second class session, we also develop students’ sensitivity to the

financial reporting environment. Most students begin their study of financial

accounting with a sense that accountants follow precise rules and procedures to

develop exact and unambiguous financial statements. We use several questions

at the end of the chapter to communicate the nature of accounting standards and

the standard-setting process.

III. Lecture Outline

1. Understand four principal activities of business entities: (a) establish

goals and strategies, (b) obtain financing, (c) make investments, and

(d) conduct operations.

The initial course in financial accounting serves not only as an

introduction to the concepts, procedures, and uses of financial accounting but

also as an introduction to business. The course introduces students to

business terminology and to the roles of marketing, finance, operations, and

other activities in running a business.

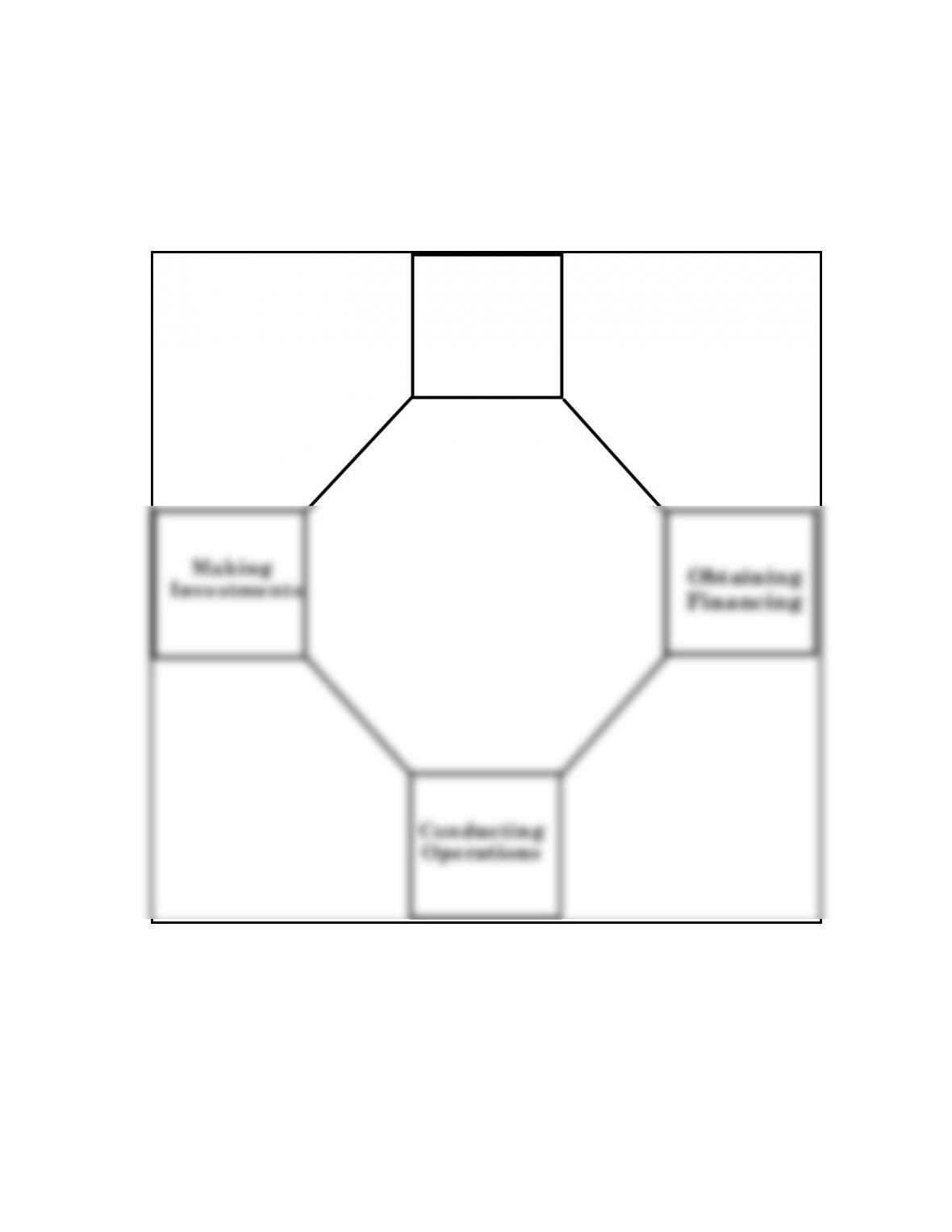

Begin by displaying the diagram of the four principal business activities

(Exhibit 1.1 in this instructor’s manual). Using the company’s annual report

which was distributed to students, raise the following questions:

A. What is the likely goal of the firm? (make the shareholders wealthy,

make the managers wealthy, provide jobs, or enhance community

welfare)

B. What strategies might the firm pursue to accomplish this goal? (price its

products low relative to competitors to achieve dominant market share,

invest in technology to achieve status as a technology leader in the

industry, diversify product lines into high growth product markets, or

diversify geographically into high growth geographical markets)

1-3 Notes

C. What sources of capital, or funds, might the firm access to finance its

activities? (investors who wish to obtain an ownership interest in the

firm [shareholders], lenders who wish their funds returned with interest

either relatively quickly [short-term creditors] or several years later

[long-term creditors])

D. How might the firm use the capital it obtains? (invest in land, buildings,

equipment, products, employees, or advertising)

E. How will the firm use the investments to generate a profit? (conduct

manufacturing, marketing, and related operations to produce and sell a

good or service)

2. Understand the purpose and content of the principal financial

statements: (a) balance sheet, (b) income statement, and (c) statement

of cash flows, and (d) statement of shareholders’ equity.

We use the financial statements distributed to students or the financial

statements of Nordstrom, Inc. from Chapter 1 (Exhibits 1.1, 1.2, 1.3, and 1.4)

to address the following questions:

A. Balance Sheet

1. What information does the statement attempt to convey? (relation

2. Is this statement a report as of a point in time or of activity over time?

3. What are the components or basic classifications within the balance

4. What is the relation between these components? (assets = liabilities +

shareholders’ equity)

5. What is the interpretation of this relation? (investing = financing)

6. Are the assets listed in increasing or decreasing order of liquidity?

7. What valuation methods does the firm use to prepare its balance

sheet? (current cash equivalent valuation or acquisition cost

valuation)

8. What valuable resources of a firm does the balance sheet exclude?

B. Income Statement

1. What information does the income statement convey? (the results of

operating performance)

Notes 1-4

2. Why use net income as the measure of operating performance?

3. Is the income statement a report as of a point in time or of activity

over time? (over time)

4. What are the components of the statement? (revenues, expenses and

net income)

5. What is the numerical relation between these components? (net

6. What is the interpretation of this relation? (operating performance is

a function of accomplishments, or outputs, and efforts, or inputs)

7. How are revenues and expenses measured? (current cash equivalent

amount or allocation of acquisition cost amount)

8. What items affecting profitability does the income statement exclude?

C. Statement of Cash Flows

1. What information does this statement convey? (the principal reasons

2. Is the statement of cash flows a report as of a point in time or of

activity over time? (over time)

3. What are the components of the statement? (net cash flows from

D. Statement of Shareholders’ Equity

1. What information does this statement convey? (displays components

of shareholders’ equity, including common shares and retained

earnings, and changes in those components)

2. Is the statement of shareholders’ equity a report as of a point in time

or of activity over time? (a point in time, a snap shot)

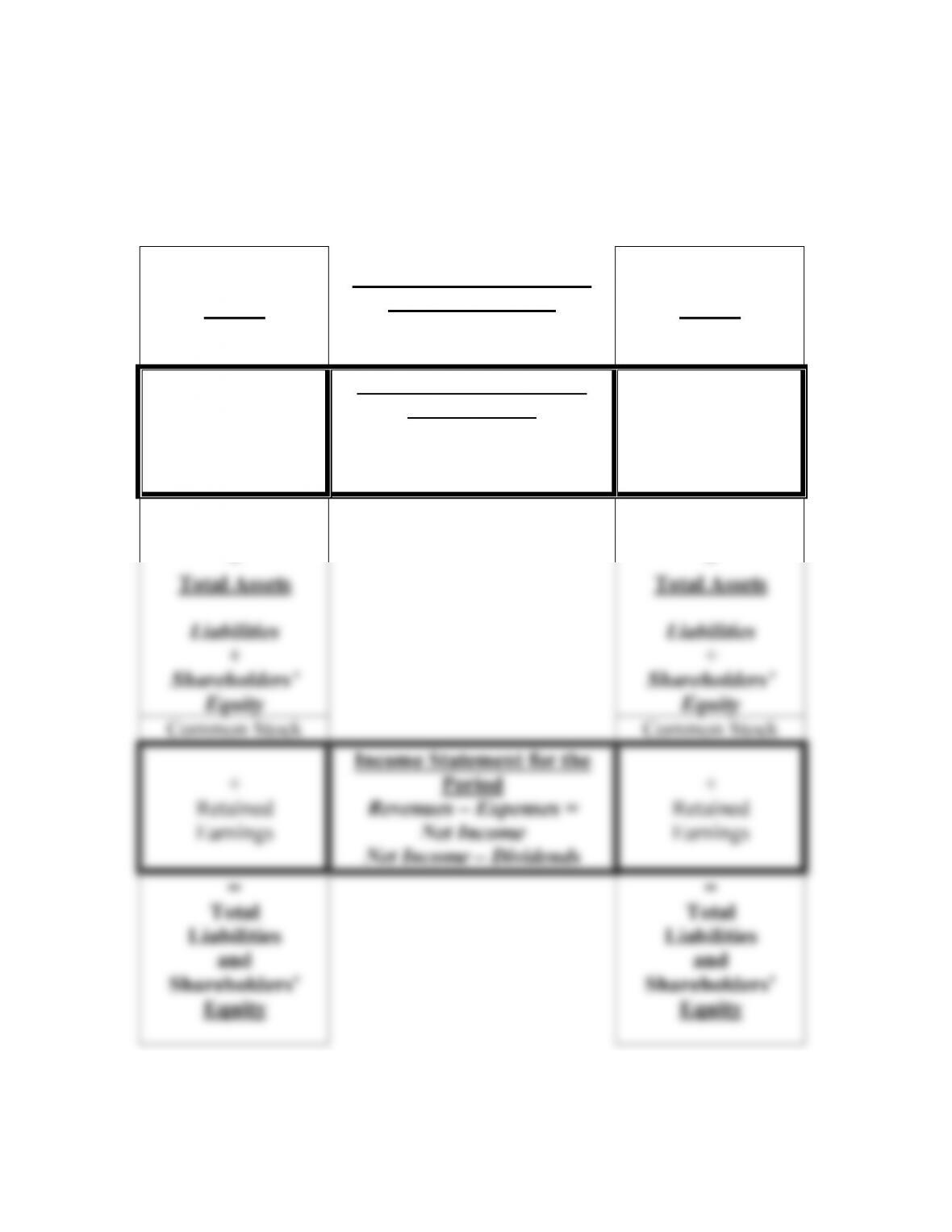

We conclude the first class session at this point. We begin the second class

session by displaying the relation among the four principal financial

1-5 Notes

sequence of topics appears below, with the number of relevant exercises in

parentheses.

1. Balance sheet relations (Exercises 1.18, 1.21, 1.22, 1.29, and 1.30)

2. Income statement relations (Exercises 1.19, 1.23, 1.24)

3. Statement of cash flow relations (Exercises 1.20, 1.27, and 1.28)

Instructors of honors undergraduate or of graduate classes may wish to

substitute problems at the end of the chapter for the exercises noted above.

Problems 1.33, and 1.34 relate to the balance sheet, Problems 1.35, and 1.36

relate to the income statement, Problems 1.37, and 1.38 relate to cash flows

and Problems 1.39, 1.42 and 1.43 relate to the principal financial statements

and require interpretation of the resulting analyses.

3. Understand the roles of participants in the financial reporting

process, including managers and governing boards, accounting

standard setters and regulators, independent external auditors, and

financial statement users.

A. Managers and Governing Boards

i. Role of managers (safeguarding and properly using the firm’s

resources)

ii. Role of governing board (selecting, compensating, and overseeing

managers; setting dividend policy; and making decisions on major

issues)

B. Accounting Standard Setters and Regulators

Role (receive input from all interested constituencies; and make

standard-setting decisions)

C. Independent External Auditors

Role (assessment of financial statements; preparing audit opinion;

and provide a report on internal control effectiveness.)

D. Users of Financial Statements

Includes investors, creditors, and other users.

3. Gain an awareness of financial reporting as part of a global system

for providing information for resource allocation decisions,

including the existence of two financial reporting systems (U.S.

GAAP and International Financial Reporting Standards).

It must be explained to the students that, the applicable accounting

guidance for preparing financial reports of U.S. firms is U.S. GAAP.

The students should know:

Notes 1-6

D. The FASB’s conceptual framework should be explained

5. Understand the difference between the cash basis and the accrual

basis of accounting, and why the latter provides a more informative

measure of performance.

These are the approaches to measure operating performance.

1-7 Notes

EXHIBIT 1.1

PRINCIPAL BUSINESS ACTIVITIES

Conducting

Operations

Obtaining

Financing

Establishing

Goals and

Strategies

Making

Investments

EXHIBIT 1.2

OVERVIEW OF PRINCIPAL FINANCIAL

STATEMENT

Balance Sheet

at Beginning of

Period

Changes in Balance Sheet

During the Period

Balance Sheet

at End of

Period

Assets

Assets

Cash

Statement of Cash Flows

for the Period

Cash Flows from Operating

Investing and Financing

Activities

Cash

+

Other Assets

=

Total Assets

Liabilities

+

Shareholders’

Equity

+

Other Assets

=

Total Assets

Liabilities

+

Shareholders’

Equity

Common Stock

Common Stock

+

Retained

Earnings

Income Statement for the

Period

Revenues – Expenses =

Net Income

Net Income – Dividends

+

Retained

Earnings

=

Total

Liabilities

and

Shareholders’

Equity

=

Total

Liabilities

and

Shareholders’

Equity

1-9 Notes

This page is intentionally left blank