10–53 Solutions

10.34 continued.

b. Plan (1):

Asset—Cash.

Plan (2): Operating Lease Method: None.

c. $150,000 = $100,000 Depreciation + (.10 X $100,000 X 5) Interest.

e. The method of accounting for a lease affects only the timing of expenses,

interest expense is smaller.

f. (1) $30,000 = $20,000 depreciation + $10,000 bond interest.

g. (1) $30,000.

Solutions 10–54

10.34 g. continued.

CAROM SPORTS COLLECTIBLES SHOP SUMMARY

(Not Required)

2008 2009 2010 2011 2012 Total

Plan 1

Depreciation

Expense ……….. $ 20,000 $ 20,000 $ 20,000 $ 20,000 $ 20,000 $ 100,000

Plan 2 (Operating)

Plan 2 (Financing)

Depreciation

Interest

10.35 (Northern Airlines; financial statement effects of capital and operating leases.)

(Amounts in Millions)

a. Capital Lease Liability, December 31, 2007 ……………………… $ 1,088

Plus Interest Expense (Plug) ………………………………………….. 102

aA comparison of the commitments under capital leases on December

10–55 Solutions

10.35 continued.

d. December 31, 2008

Interest Expense ……………………………………………….. 102

10–57 Solutions

10.35 continued.

f. Present Value of Operating Lease Commitment on

December 31, 2007

Present Value

Year Payments Factor at 10.0% Present Value

2008 $ 1,065 .90909 $ 968

aAssume that the firm pays the $7,453 at the rate of $815 a year for 9.145

(= $7,453/$815) periods at 10%.

Present Value of Operating Lease Commitment on

December 31, 2008

Present Value

Year Payments Factor at 10.0% Present Value

2009 $ 1,098 .90909 $ 998

Solutions 10–58

aAssume that the firm pays the $6,710 at the rate of $855 a period for 7.848

(= $6,710/$855) periods.

10–59 Solutions

10.35 continued.

g. Long-Term Debt Ratio Based on Reported Amounts:

h. Long-Term Debt Ratio Including Capitalization of Operating Leases:

10.36 (FedUp Corporation; financial statement effects of capital and operating

leases.) (Amounts in Millions)

a. Capital Lease Liability, May 31, 2007 ………………………………. $ 401

Plus Interest Expense: .05 X $401 ………………………………….. 20

c. During Fiscal 2008

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+10

+10

To record new capital leases signed.

May 31, 2008

Solutions 10–60

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–121

–101

–20

IncSt → RE

To record interest expense on capital leases, the cash

payment, and decrease in the capital lease liability for

the difference.

10–61 Solutions

10.36 c. continued.

May 31, 2008

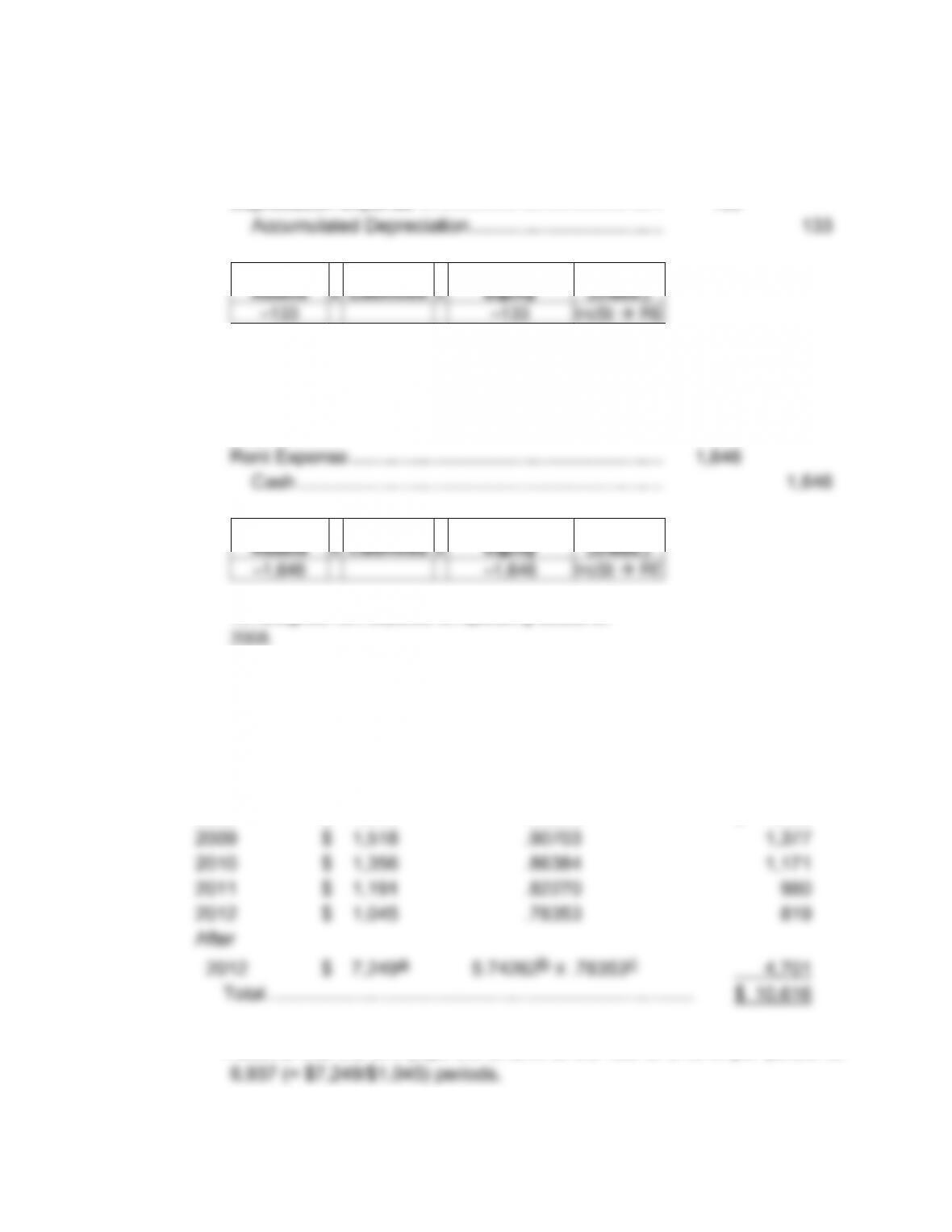

Depreciation Expense ……………………………………….. 133

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–133

–133

IncSt → RE

To recognize depreciation expense on capitalized

leased asset for 2008.

d. May 31, 2008

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–1,646

–1,646

IncSt → RE

To recognize rent expense on operating leases for

e. Present Value of Operating Lease Commitment on

May 31, 2007

Present Value

Year Payments Factor at 5% Present Value

2008 $ 1,646 .95238 $ 1,568

aAssume that the firm pays the $7,249 at the rate of $1,045 per period for

Solutions 10–62

10–63 Solutions

10.36 e. continued.

Present Value of Operating Lease Commitment on

May 31, 2008

Present Value

Year Payments Factor at 5% Present Value

2009 $ 1,672 .95238 $ 1,592

bFactor for the present value of an annuity of $984 million for 6.890

cFactor for the present value of $1 for five periods at 5%.

f. Long-Term Debt Ratio Based on Reported Amounts:

g. Long-Term Debt Ratio Including Capitalization of Operation Leases:

Solutions 10–64

10.37 (GSB Corporation; measuring interest expense.)

Solving for BB:

Thus, interest expense for this last six month period equals $5,447.62 (= .05 X