4-1 Solutions

CHAPTER 4

INCOME STATEMENT: REPORTING THE RESULTS

OF OPERATING ACTIVITIES

Questions, Exercises, and Problems: Answers and Solutions

4.2 Revenues measure the inflow of net assets from operating activities and

4.3 Cost is the economic sacrifice made to acquire goods or services. When the

expense.

4.4 Current accounting practice takes the viewpoint of shareholders by reporting

4.5 The assets and income from operations that a firm has decided to discontinue

4.6 The revenues must be earned (the firm must have achieved substantial

Solutions 4-2

4.7 The matching convention assigns expenses to the related revenues. If the

4-3 Solutions

4.8 Revenues are part of the ongoing central operations of the firm, so they are

relatively persistent and sustainable. In contrast, gains arise from relatively

4.9 The profit margin percentage, because it uses only sales revenues and net

income, which are not affected by differences in display and format. Settings

4.10 Firms do not necessarily recognize revenues when they receive cash or

recognize expenses when they disburse cash. Thus, net income will not

4.11 (Neiman Marcus; revenue recognition.)

February March April

a. — — $ 800

4.12 (Fonterra Cooperative Group Limited; revenue recognition.)

a. No. Fonterra has not yet delivered the milk and, therefore, has not

achieved substantial performance.

Solutions 4-4

4-5 Solutions

4.12 continued.

d. No. Fonterra would clearly not recognize revenue on hearing that some of

the milk delivered was spoiled. The question is how they record the non–

e. No. Accrual accounting usually recognizes revenue when a firm sells

4.13 (Sun Microsystems; expense recognition.)

June July August

a. — $ 15,000 $ 15,000

e. — — —

4.14 (Tesco Plc.; expense recognition.)

Solutions 4-6

a. None (this is a September expense).

4-7 Solutions

4.14 continued.

e. £4,000 in maintenance and repairs expense (the repair does not extend

4.15 (Bombardier Corporation; relating net income to balance sheet changes.)

4.16 (Magyar Telekom; relating net income to balance sheet changes.) (Amounts

in Millions of HUF)

a. Assets = Liabilities + Shareholders’ Equity.

b. 2007

Retained Earnings, Beginning of Year (Part

a

. above) …… HUF 397,311

4.17 (Lenovo Group Limited; income statement relations.) (Amounts in Thousands)

The missing items appear in boldface type below:

2008 2007

Solutions 4-8

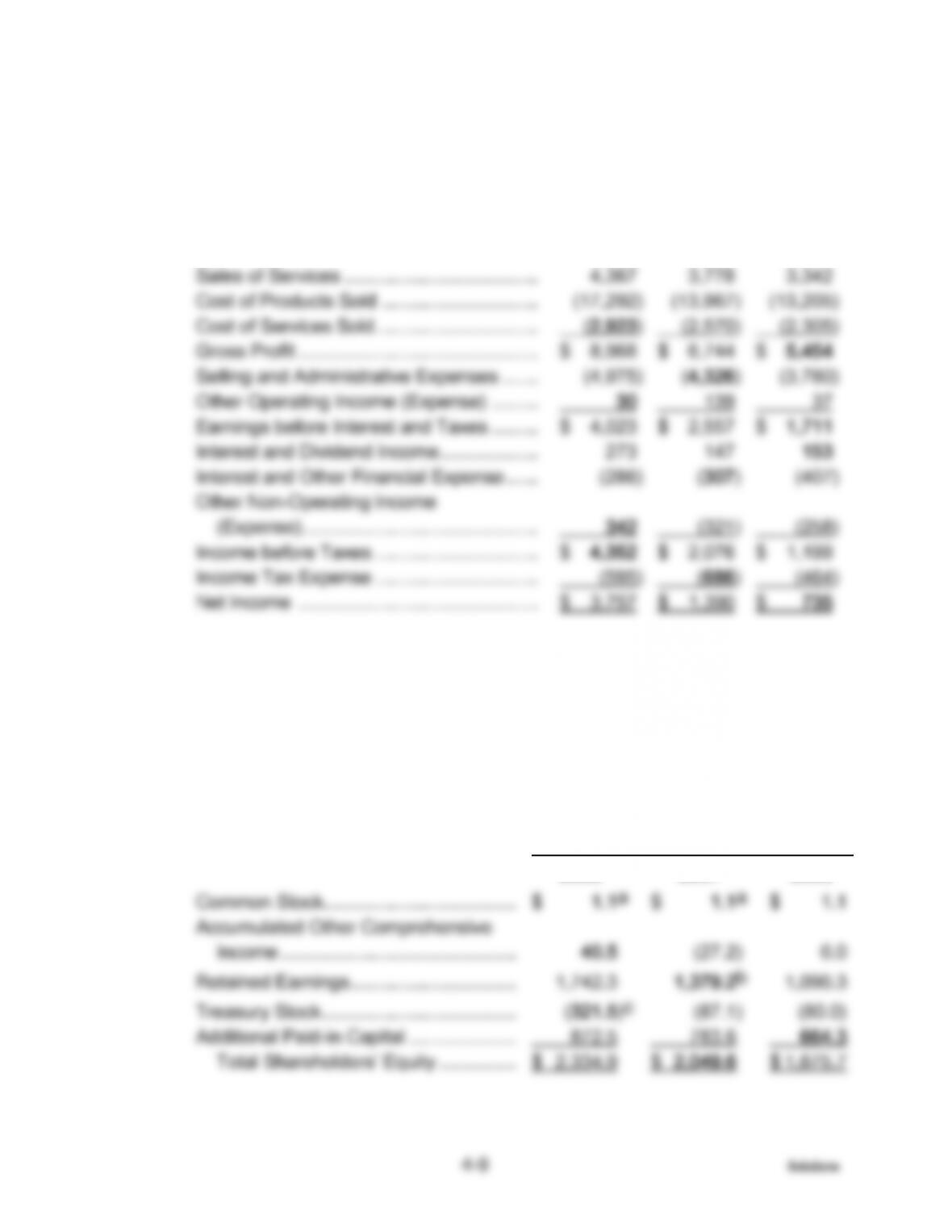

4.18 (ABB; income statement relations.) (Amounts in Millions)

The missing items appear in boldface below:

2007 2006 2005

Sales of Products ………………………………. $ 24,816 $ 19,503 $ 17,622

4.19 (James John Corporation; income and equity relations.) (Amounts in Millions)

The missing items appear in boldface below:

JAMES JOHN CORPORATION

Comparative Balance Sheets

March 31, 2008, 2007, and 2006

March 31,

2008 2007 2006

Solutions 4-10

4-11 Solutions

4.19 continued.

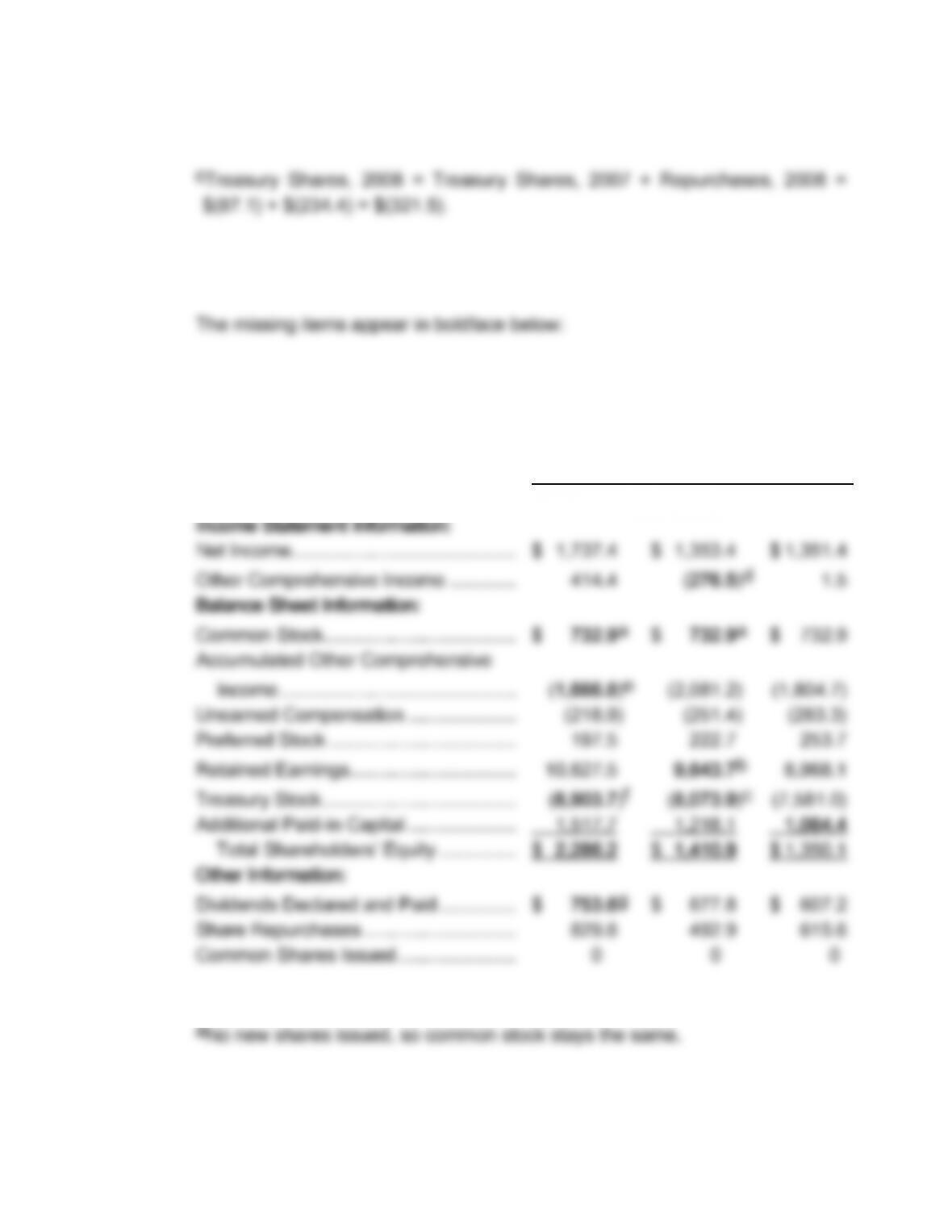

4.20 (Colgate Palmolive Company; income and equity relations.) (Amounts in

Millions)

COLGATE PALMOLIVE COMPANY

Comparative Balance Sheets

December 31, 2007, 2006, and 2005

December 31,

2007 2006 2005

Calculations:

Solutions 4-12

4-13 Solutions

4.20 continued.

dAccumulated Other Comprehensive Income, End of 2006 = Accumulated

Other Comprehensive Income, End of 2005 + Other Comprehensive Income,

2006. $(2,081.2) = $(1,804.7) + Other Comprehensive Income, 2006. Other

Comprehensive Income, 2006 = $(276.5).

eAccumulated Other Comprehensive Income, End of 2007 = Accumulated

4.21 (MosTechi Corporation; accumulated other comprehensive income relations.)

(Amounts in Millions of Yen)

The missing items appear in boldface below:

MOSTECHI CORPORATION

Comparative Balance Sheets

March 31, 2008, 2007, and 2006

March 31,

2008 2007 2006

Calculations:

Solutions 4-14

aAccumulated Other Comprehensive Income, End of 2007 = Accumulated

4-15 Solutions

4.21 continued.

cRetained Earnings, End of 2008 = Retained Earnings, End of 2007 + Net

4.22 (Solaronx Company; accumulated other comprehensive income relations.)

(Amounts in Millions)

The missing items appear in boldface below:

SOLARONX COMPANY

Comparative Balance Sheets

December 31, 2008, 2007, and 2006

December 31,

2008 2007 2006

Calculations:

aTotal Shareholders’ Equity, End of 2006 = $5 – $1,919 + $2,998 – $73 +

Solutions 4-16

Retained Earnings, End of 2007 = Retained Earnings, End of 2006 + Net

4-17 Solutions

4.22 continued.

eAccumulated Other Comprehensive Income, End of 2008 = Accumulated

Other Comprehensive Income, End of 2007 + Other Comprehensive Income,

4.23 (Bayer Group; discontinued operations.)

a. In 2007, 51% [= 2,410/(2,410 + 2,306)] of Bayer’s income came from

c. The large decline in Bayer’s assets held for discontinued operations is due

Solutions 4-18

4.24 (Orascom Telecom Holding S.A.E.; discontinued operations.) (Amounts in

Thousands of Egyptian Pounds)

The missing items appear in boldface type below:

ORASCOM TELECOM HOLDING S.A.E.

Comparative Balance Sheets

December 31, 2007 and 2006

December 31,

2007 2006