3-1 Solutions

CHAPTER 3

BALANCE SHEET: PRESENTING AND ANALYZING

RESOURCES AND FINANCING

Questions, Exercises, and Problems: Answers and Solutions

3.2 Conservatism emphasizes the early recognition of losses and delayed

3.3 One justification relates to the requirement that an asset or liability be

measured with sufficient reliability. When there is an exchange between a firm

3.4 The underlying principle is that acquisition cost includes all costs required to

and are included in the acquisition cost measurement of the asset.

3.5 The justification relates to the uncertainty as to the ultimate economic effects

of the contracts. One party or the other may pull out of the contract. The

Solutions 3-2

3-3 Solutions

3.7 a. The contract between the investors and the construction company as well

as cancelled checks provide evidence as to the acquisition cost.

c. There are at least two possibilities for ascertaining current replacement

cost. One alternative is to consult a construction company to determine

the cost of constructing a similar office building (that is, with respect to

d. The accountant might consult a local real estate dealer to ascertain the

e. The accountant might use the amount described in Part

d.

but exclude

transactions cost when measuring fair value. The accountant might also

Solutions 3-4

3-5 Solutions

3.8 a. Liability—Receivable from Supplier or Prepaid Merchandise Orders.

3.9 a. Yes; amount of accrued interest payable.

e. Yes; at the expected, undiscounted value of future service costs arising

from all sales made prior to the balance sheet date. The income statement

f. No. If the firm expected to lose a reasonably estimable amount in the suit,

then it would show an estimated liability.

i. Airlines recognize an expense and a liability for future services as

passengers accumulate miles at regular fares, as those passengers reach

Solutions 3-6

3-7 Solutions

3.10 a. The expected value of the liability is $90,000 in both cases (.90 X $100,000

b. The liability for the coupons would be measured at $90,000.

3.11 a. In the definitions of assets and liabilities,

probable

is used to capture the

b. In the recognition criteria for liabilities with uncertain amount and/or

3.12 (Aracruz Celulose; balance sheet formats.)

a. U.S. GAAP Balance Sheet. Assets and liabilities are listed on the balance

are shown first, under their respective categories.

ARACRUZ CELULOSE

Balance Sheet

For the Year Ended December 31, 2006

(Amounts in Thousands)

Assets

Solutions 3-8

3-9 Solutions

3.12 a. continued.

Liabilities and Shareholders’ Equity

Current Liabilities ………………………………………………………………………… $ 286,819

b. IFRS Balance Sheet. Note that IFRS permits firms discretion as to how

they list assets and liabilities on their balance sheet. One acceptable

Solutions 3-10

3-11 Solutions

3.13 (Delhaize Group; balance sheet formats.)

DELHAIZE GROUP

Balance Sheet

For the Year Ended December 31, 2007

(Amounts in Millions of Euros)

Assets

Current Assets:

Cash and Cash Equivalents …………………………………………………………. 248.9

Receivables ……………………………………………………………………………………. 564.6

Total Assets ………………………………………………………………………………. 8,821.9

Liabilities and Shareholders’ Equity

Current Liabilities:

Accounts Payable …………………………………………………………………………. 1,435.8

Accrued Expenses ………………………………………………………………………… 375.7

Obligations under Finance Leases …………………………………………….. 595.9

Solutions 3-12

Share Capital …………………………………………………………………………………. 50.1

3-13 Solutions

3.14 (Classifying financial statement accounts.) (Unless indicated, classifications do

not differ between U.S. GAAP and IFRS.)

d. NI (U.S. GAAP); NI and NA (IFRS). Under U.S. GAAP, all R&D expenditures

e. NA.

i. CA.

j. CL.

n. NL.

Solutions 3-14

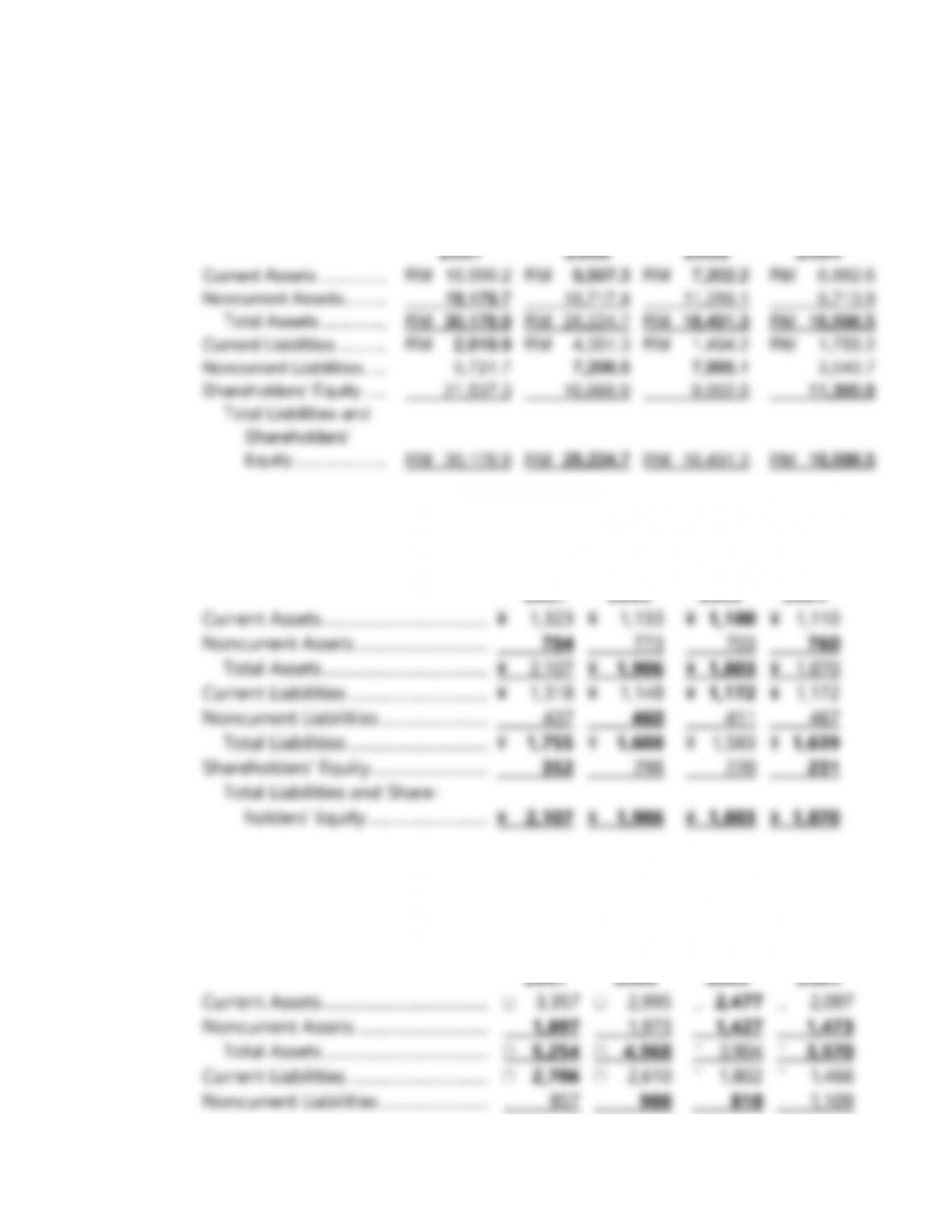

3.15 (Genting Group; balance sheet relations.)

The missing items appear in boldface type below (amounts in millions of

ringgit, RM).

3.16 (Kajima; balance sheet relations.)

The missing items appear in boldface type below (amounts in billions of yen).

2007 2006 2005 2004

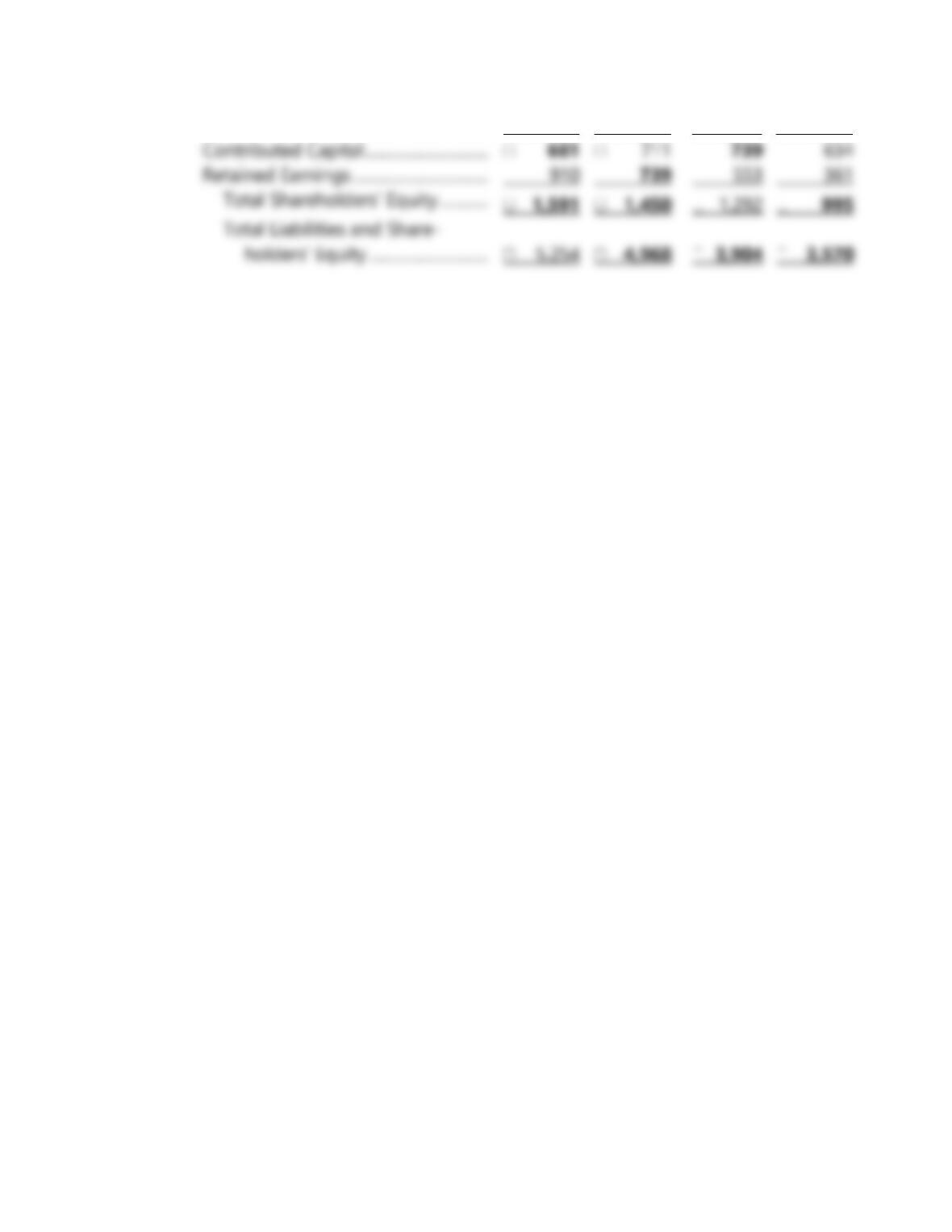

3.17 (Metso; balance sheet relations.)

The missing items appear in boldface type below (amounts in millions of

euros).

3-15 Solutions

Total Liabilities ……………………………. 3,663 3,518 2,612 2,575

Solutions 3-16

3.18 (Ford Models; asset and liability recognition and measurement.)

Accounting does not normally recognize mutually unexecuted contracts as

3.19 (Duke University; asset recognition and measurement.)

The expenditures do not qualify as an asset because: (1) Duke University

3.20 (Trader Joe’s; asset measurement.)

The acquisition cost of the refrigeration system includes the purchase price of

$1.3 million, the modification costs of $120,000, and the cost to transport and

3.21 (Nordstrom; recognition of a loss contingency.)

a. Nordstrom should recognize the contingency as soon as it is probable that

it has incurred a loss and it can reasonably estimate the amount of the

3-17 Solutions

Solutions 3-18

3.21 a. continued.

If attorneys feel that the grounds for appeal are strong, then the next

b. Under IFRS, the threshold for recognition is also probable but the meaning

3.22 (Nestlé; asset recognition and measurement.)

a. Both U.S. GAAP and IFRS would recognize Investment in Bond (noncurrent

b. Both U.S. GAAP and IFRS would recognize Prepaid Insurance (current

asset); CHF240 million would be recorded initially. At Nestlé’s year-end,

c. Both U.S. GAAP and IFRS would recognize Option to Purchase Land

d. Neither U.S. GAAP nor IFRS recognizes the employment contract, a

e. Under U.S. GAAP, Nestlé would record only the costs of obtaining the

patent as an asset on its balance sheet, Patent (noncurrent asset), CHF0.5

3-19 Solutions

Solutions 3-20

3.23 (Ryanair Holdings; asset recognition and measurement.)

a. Under both U.S. GAAP and IFRS, a decision on the part of Ryanair’s board

of directors does not give rise to an asset.

d. Under both U.S. GAAP and IFRS, Ryanair’s purchase gives rise to an asset,

Landing Rights (noncurrent asset), 50 million.

e. Under both U.S. GAAP and IFRS, Ryanair’s purchase gives rise to an asset

3.24 (Hana Microelectronic Public Company Limited; liability recognition and

measurement.)

a. Under both U.S. GAAP and IFRS, this arrangement is a mutually

unexecuted contract; as such, it does not give rise to a liability on Hana

Microelectronics balance sheet.