13-1 Solutions

CHAPTER 13

INTERCORPORATE INVESTMENTS IN COMMON STOCK

Questions, Exercises, and Problems: Answers and Solutions

13.2 Control is present when one entity has sufficient ownership interest or

contractual rights to make both strategic and operating decisions for another

entity. Significant influence is present when one entity has sufficient

13.3 Dividends represent revenues under the fair-value method, or a return of

13.4 Firms use over time the service potential of assets with a limited life. The

13.5 When control is present, a parent and a subsidiary operate as a single

economic entity. Eliminating intercompany profit and loss in these cases

Solutions 13-2

13-3 Solutions

13.6 The Investment account changes under the equity method with all changes in

13.7 Under the equity method, the change each period in the net assets, or

shareholders’ equity, of the subsidiary appears on the one line, Investment in

13.8 When the investor uses the equity method, total assets include the Investment

in Subsidiary account. The investment account reflects the parent’s interest in

13.9 If Company A owns less than, or equal to, 50% of Company B’s voting stock, it

is a minority investor in Company B. If Company A owns more than 50% of

13.10 An economic entity is a group of companies that operates under the control of

a parent company instead of as separate companies. The parent company

Solutions 13-4

13.11 Failing to eliminate the Investment in Subsidiary account will result in double

13-5 Solutions

13.12 The noncontrolling interest in net income is an income statement account that

shows the claim of the noncontrolling shareholders on the net income of the

consolidated group of companies. The noncontrolling interest in net assets is

13.13 One can envision scenarios where the equity method or proportionate

consolidation better reflects the relation between the joint owners and the joint

venture. For example, assume a joint venture in which one of the joint owners

13.14 Contracts or other agreements might shift control of the entity from its owners

13.15 (Hanna Company; equity method entries.)

Investment in Stock of Denver Company …………………… 550,000

Cash ……………………………………………………………….. 550,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+550,000

–550,000

To record acquisition of common stock.

Solutions 13-6

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+120,000

+120,000

IncSt → RE

To accrue 100% share of Denver Company’s earnings.

13-7 Solutions

13.15 continued.

Cash or Dividends Receivable …………………………………. 30,000

Investment in Stock of Denver Company ……………… 30,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+30,000

–30,000

To accrue dividends received or receivable.

13.16 (Weber Corporation; equity method entries.) (Amounts in Millions)

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+100

–100

To record acquisition of shares of common stock.

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+20

+20

IncSt → RE

To accrue Weber Computer’s earnings for the year.

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+6

–6

To record dividends received or receivable.

Solutions 13-8

13-9 Solutions

13.16 continued.

Amortization Expense …………………………………………….. 1.6

Investment in Stock of Weber Computer ………………. 1.6

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+1.6

–1.6

IncSt → RE

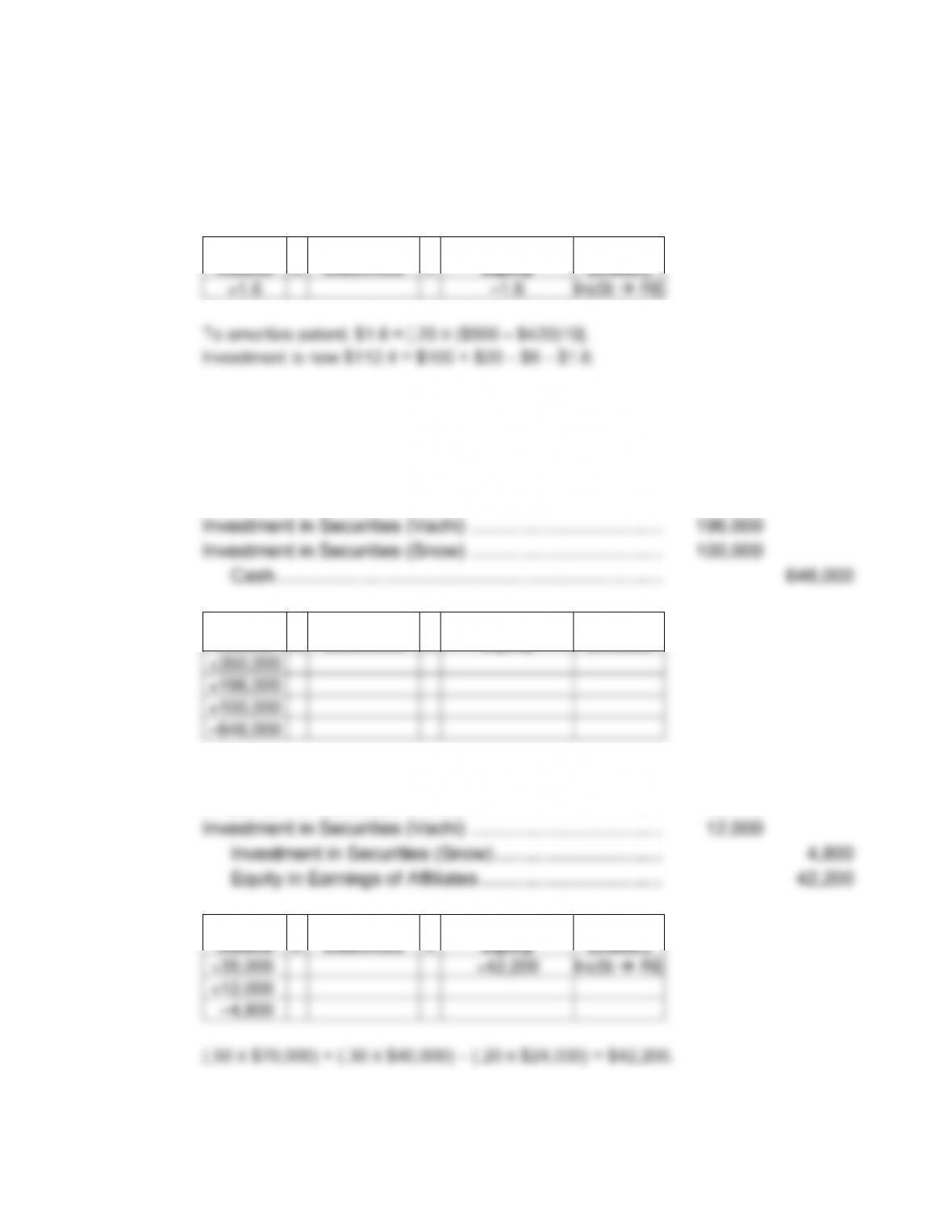

To amortize patent; $1.6 = [.20 X ($500 – $420)10].

Investment is now $112.4 = $100 + $20 – $6 – $1.6.

13.17 (Wood Corporation; journal entries to apply the equity method of accounting

for investments in securities.)

January 2

Investment in Securities (Knox) ……………………………….. 350,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+350,000

+196,000

+100,000

–646,000

December 31

Investment in Securities (Knox) ……………………………….. 35,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+35,000

+42,200

IncSt → RE

+12,000

–4,800

(.50 X $70,000) + (.30 X $40,000) – (.20 X $24,000) = $42,200.

Solutions 13–10

13.17 continued.

December 31

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+19,500

–15,000

–4,500

(.50 X $30,000) + (.30 X $15,000) = $19,500.

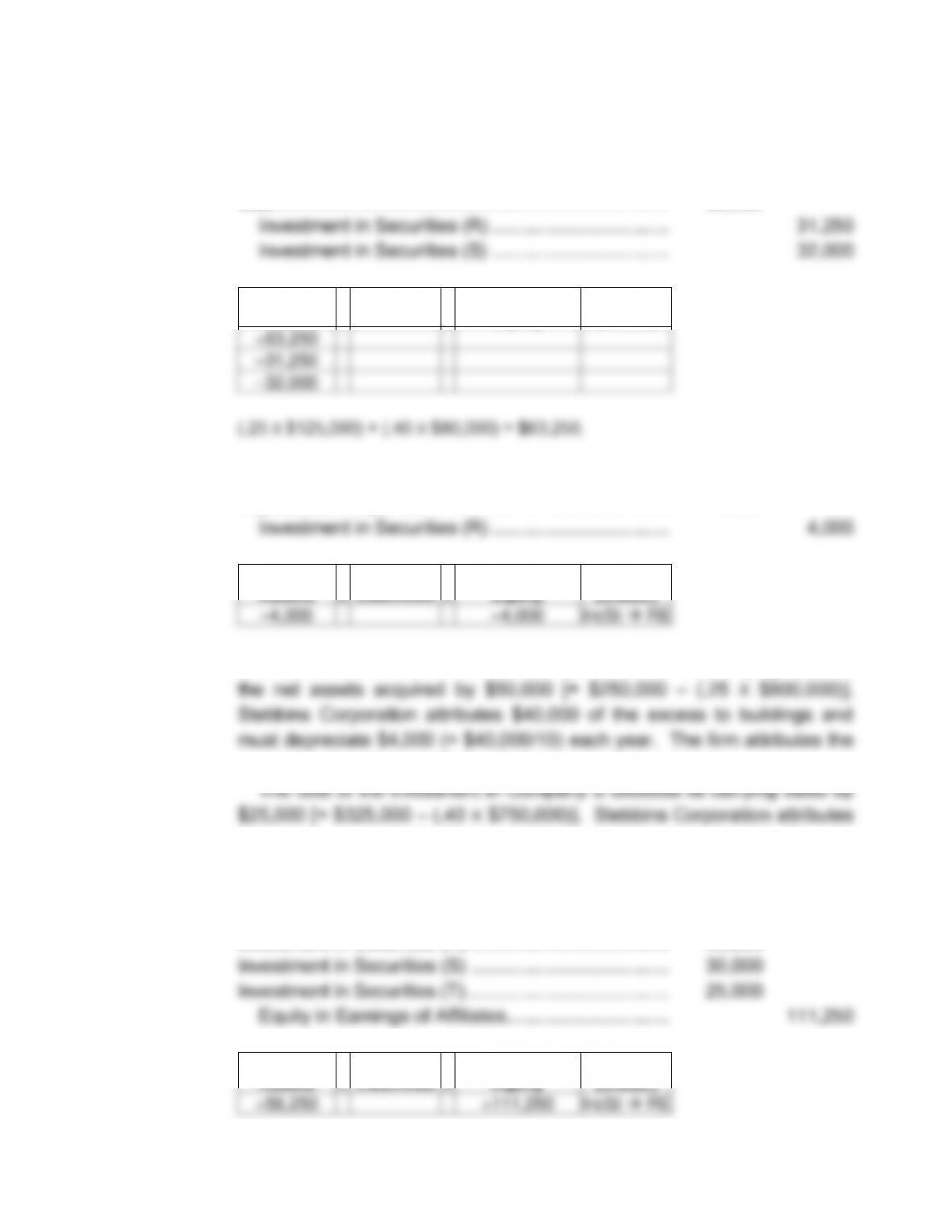

13.18 (Stebbins Corporation; journal entries to apply the equity method of accounting

for investments in securities.)

a. January 1, 2008

Investment in Securities (R) ……………………………….. 250,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+250,000

+325,000

+475,000

–1,050,000

December 31, 2008

Investment in Securities (R) ……………………………….. 50,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+50,000

+23,000

IncSt → RE

+48,000

–75,000

13–11 Solutions

Solutions 13–12

13.18 a. continued.

December 31, 2008

Cash ……………………………………………………………….. 63,250

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+63,250

–31,250

–32,000

(.25 X $125,000) + (.40 X $80,000) = $63,250.

December 31, 2008

Depreciation Expense ……………………………………….. 4,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–4,000

–4,000

IncSt → RE

The cost of the investment in Company R exceeds the carrying value of

remaining excess to goodwill, which it need not depreciate.

this excess to goodwill. The acquisition cost of the investment in Security

T equals the carrying value of the net assets acquired.

December 31, 2009

Investment in Securities (R) ……………………………….. 56,250

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+56,250

+111,250

IncSt → RE

13–13 Solutions

+30,000

+25,000

(.25 X $225,000) + (.40 X $75,000) + (.50 X $50,000) =

$111,250.

Solutions 13–14

13.18 a. continued.

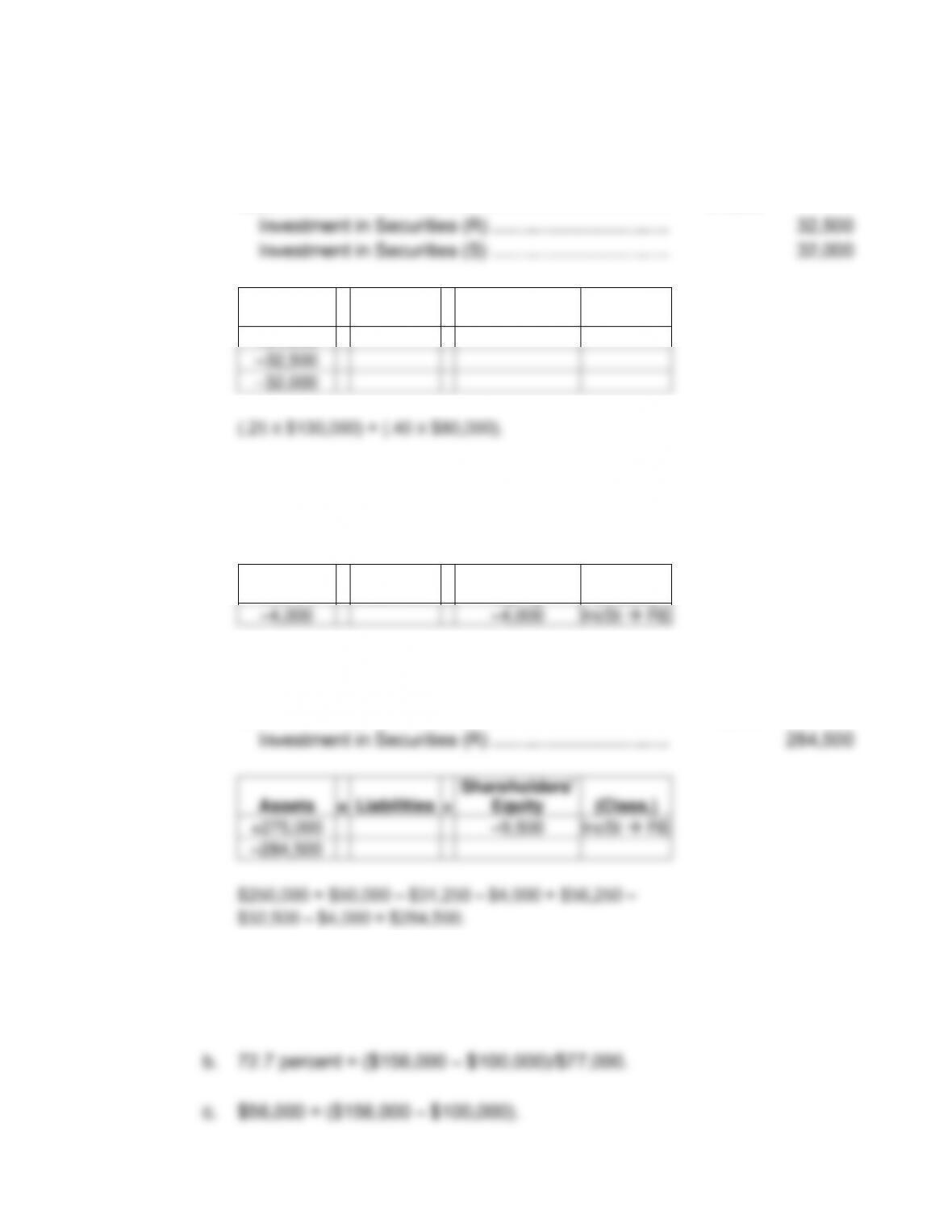

December 31, 2009

Cash ……………………………………………………………….. 64,500

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+64,500

–32,500

–32,000

December 31, 2009

Depreciation Expense ……………………………………….. 4,000

Investment in Securities (R) ……………………………. 4,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–4,000

–4,000

IncSt → RE

b. January 1, 2010

Cash ……………………………………………………………….. 275,000

Loss on Sale of Investments ………………………………. 9,500

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+275,000

–9,500

IncSt → RE

–284,500

13.19 (Laesch Company; working backwards to consolidation relations.)

a. $70,000 = ($156,000 – $100,000)/.80.

13–15 Solutions

13.20 Dealco Corporation; working backwards from consolidated income

statements.) (Amounts in Millions)

a. $56/$140 = 40%.

13.21 (CAR Corporation; consolidation policy and principal consolidation concepts.)

a. CAR Corporation should consolidate Alexandre du France Software

b. Charles Electronics ……………………………… (.75 X $120,000) = $ 90,000

c. Noncontrolling Interest shown under accounting assumed in problem:

Charles Electronics ……………………………… (.25 X $120,000) = $ 30,000

d. Charles Electronics, no increase because already consolidated.

Alexandre du France Software Systems increase by 80% of net income

less dividends:

Solutions 13–16

e. Noncontrolling Interest shown if CAR Corporation consolidated all

companies:

Charles Electronics …………………………….. (.25 X $120,000) = $ 30,000

13–17 Solutions

13.22 (Joyce Company and Vogel Company; equity method entries.)

Joyce Company’s Books

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+420,000

–420,000

To record acquisition of common stock.

(2) Accounts Receivable …………………………………………. 29,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+29,000

+29,000

IncSt → RE

To record intercompany sales on account.

(2) Cost of Goods Sold …………………………………………… 29,000

Inventories …………………………………………………… 29,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–29,000

–29,000

IncSt → RE

To record cost of intercompany sales.

(3) Advance to Vogel Company ……………………………….. 6,000

Cash ……………………………………………………………. 6,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+6,000

–6,000

To record advance to Vogel Company.

Solutions 13–18

13.22 continued.

(4) Cash ……………………………………………………………….. 16,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+16,000

–16,000

To record collections on account from Vogel Company.

(5) Cash ……………………………………………………………….. 4,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+4,000

–4,000

To record collection of advance from Vogel Company.

(6) Cash ……………………………………………………………….. 20,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+20,000

–20,000

To record dividend from Vogel Company.

(7) Investment in Stock of Vogel Company ……………….. 30,000

Assets

=

Liabilities

+

Shareholders‘

Equity

(Class.)

+30,000

+30,000

IncSt → RE

To accrue 100% share of Vogel Company’s net income.

13–19 Solutions

13.22 continued.

(8) Amortization Expense ……………………………………….. 4,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–4,000

–4,000

IncSt → RE

To record amortization of patent; $4,000 = ($20,000 –

$380,000)/10.

Vogel Company’s Books

(1) No entry.

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+29,000

+29,000

To record intercompany purchase of materials on

account.

(3) Cash ……………………………………………………………….. 6,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+6,000

+6,000

To record advance from Joyce Company.

(4) Accounts Payable …………………………………………….. 16,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–16,000

–16,000

To record payment for purchases on account.

Solutions 13–20