Solutions 12–56

of the note payable at the beginning of the year

tractual interest rate of 6% on the face amount of the

carrying value of the note payable for the difference.

12–57 Solutions

12.30 a. continued.

December 31, 2009

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+143

+143

IncSt → RE

To record interest expense for the increase in the

carrying value of the swap contract for the passage of

December 31, 2009

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–1,000

–1,000

To record cash paid to the counterparty because the

Firm B must revalue the note payable and the swap contract for changes

in fair value. The bank resets the interest rate in the swap agreement to

Present Value of Interest Payments: $3,000 X .96154 = ……… $ 2,885

December 31, 2009

Solutions 12–58

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+1,888

–1,888

IncSt → RE

To measure the note payable at fair value using an

12–59 Solutions

12.30 a. continued.

The fair value of the swap contract increases. Sandretto Corporation will

receive $1,000 at the end of 2010 because of the swap contract. Thus,

the swap contract becomes an asset instead of a liability. The present

December 31, 2009

Swap Contract (Liability) ……………………………………. 926

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+962

–926

–1,888

IncSt → RE

To measure the swap contract at fair value using a

At the end of 2009, the Note Payable account has a balance of $50,962

and the Swap Contract account has a debit balance of $962.

b. January 1, 2010

Note Payable ……………………………………………………. 50,962

Swap Contract (Asset) …………………………………… 962

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–50,000

–50,962

–962

To repay note payable prior to maturity and close

out the swap contract.

c. The entries would be identical if Sandretto Corporation chose the fair

Solutions 12–60

12–61 Solutions

12.31 (Avery Corporation; accounting for an interest rate swap as a cash flow

hedge.)

January 1, 2008

Equipment …………………………………………………………….. 50,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+50,000

+50,000

To record the acquisition of equipment by giving a $50,000

note payable with a variable interest rate of 6%.

December 31, 2008

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–3,000

–3,000

IncSt → RE

To recognize interest expense and cash payment at the

The fair value of the swap agreement on December 31, 2008 after the

Avery Corporation on December 31 of 2009 and December 31 of 2010 if the

interest rate remains at 8%.

December 31, 2008

Swap Contract ………………………………………………………. 1,783

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+1,783

+1,783

OCInc →

AOCInc

To measure the swap contract at fair value and recognize

an asset on the balance sheet and a gain in other compre-

hensive income.

Solutions 12–62

12–63 Solutions

12.31 continued.

December 31, 2009

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–4,000

–4,000

IncSt → RE

To recognize interest expense and cash payment at the

Avery Corporation must also recognize interest on the swap contract because

of the passage of time.

December 31, 2009

Swap Contract ………………………………………………………. 143

Interest on Swap Contract ………………………………….. 143

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+143

+143

OCInc →

AOCInc

– .06)] required by the swap contract. The entry is:

December 31, 2009

Cash ……………………………………………………………………. 1,000

Swap Contract ………………………………………………….. 1,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+1,000

–1,000

To record cash received from the counterparty because

the interest rate increased from 6% to 8%.

Solutions 12–64

12–65 Solutions

12.31 continued.

December 31, 2009

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–1,000

OCInc →

AOCInc

+1,000

IncSt → RE

To reclassify a portion of other comprehensive income to

net income for the hedged portion of interest expense on

the note payable.

likewise, has a credit balance of $926.

Resetting the interest rate on December 31, 2009 to 4% changes the fair

value of the swap contract from an asset to a liability. The present value of the

swap contract is:

December 31, 2009

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–926

+962

–1,888

OCInc →

AOCInc

To measure the swap contract at fair value and recognize

a liability on the balance sheet and a loss in other com-

prehensive income.

December 31, 2010

Interest Expense ……………………………………………………. 2,000

Cash ……………………………………………………………….. 2,000

Solutions 12–66

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–2,000

–2,000

IncSt → RE

12–67 Solutions

12.31 continued.

December 31, 2010

Interest on Swap Contract ………………………………………. 38

Swap Contract ………………………………………………….. 38

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+38

–38

OCInc →

AOCInc

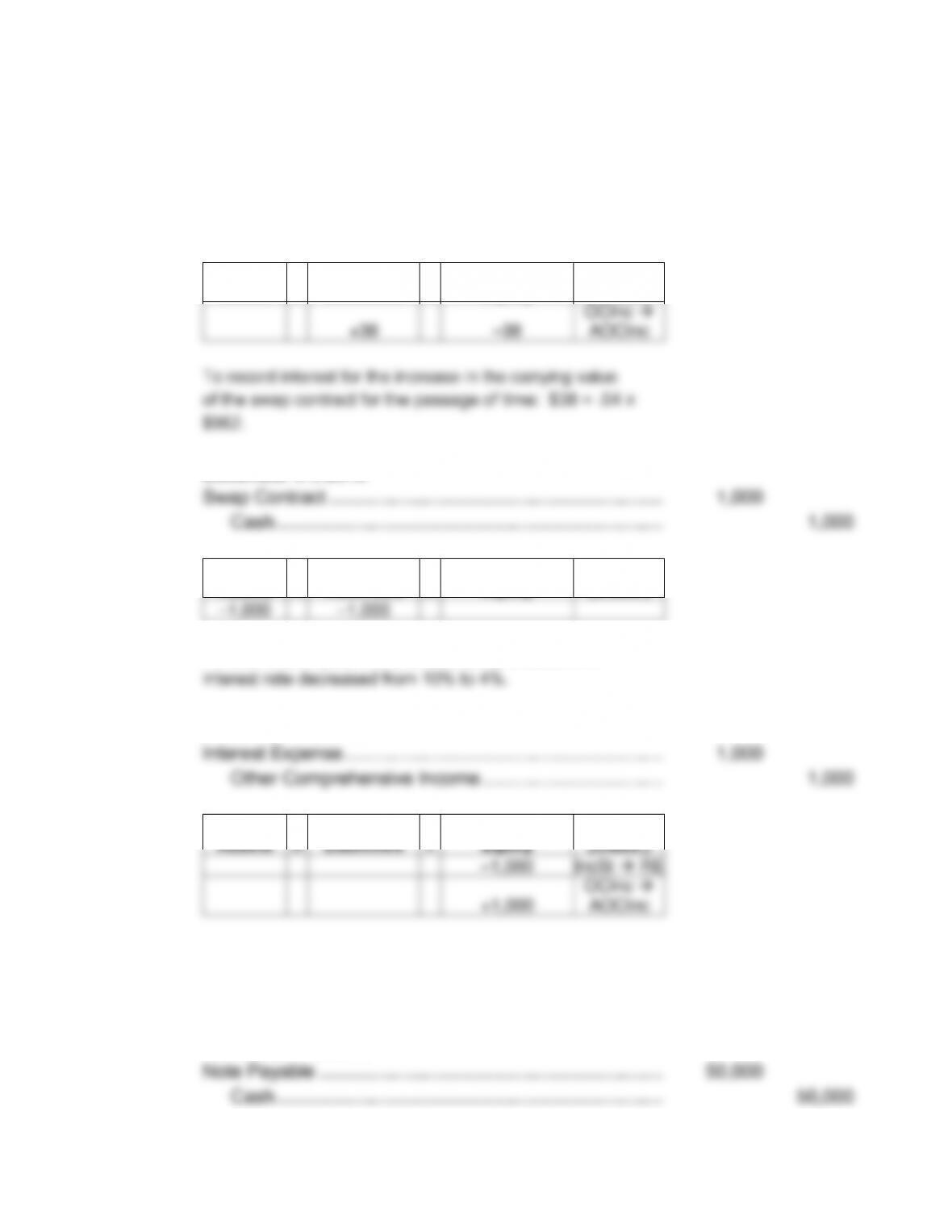

To record interest for the increase in the carrying value

of the swap contract for the passage of time: $38 = .04 X

$962.

December 31, 2010

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–1,000

–1,000

To record cash paid to the counterparty because the

December 31, 2010

Assets

=

Liabilities

+

Shareholders‘

Equity

(Class.)

–1,000

IncSt → RE

+1,000

OCInc →

AOCInc

To reclassify a portion of other comprehensive income to

net income for the hedged portion of interest expense on

the note payable.

December 31, 2010

Solutions 12–68

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–50,000

–50,000

To record repayment of note payable at maturity.

12–69 Solutions

12.31 continued.