Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

5-41 Solutions

Solutions 5-42

5.36 continued.

b. GTI, INC.

Statement of Cash Flows

For 2007 and 2008

2008 2007

Operations:

Sale of Patents ................................................ $ 63 $ --

Acquisition of Property, Plant and Equip-

ment ............................................................ (54) (1,433)

5-43 Solutions

5.36 continued.

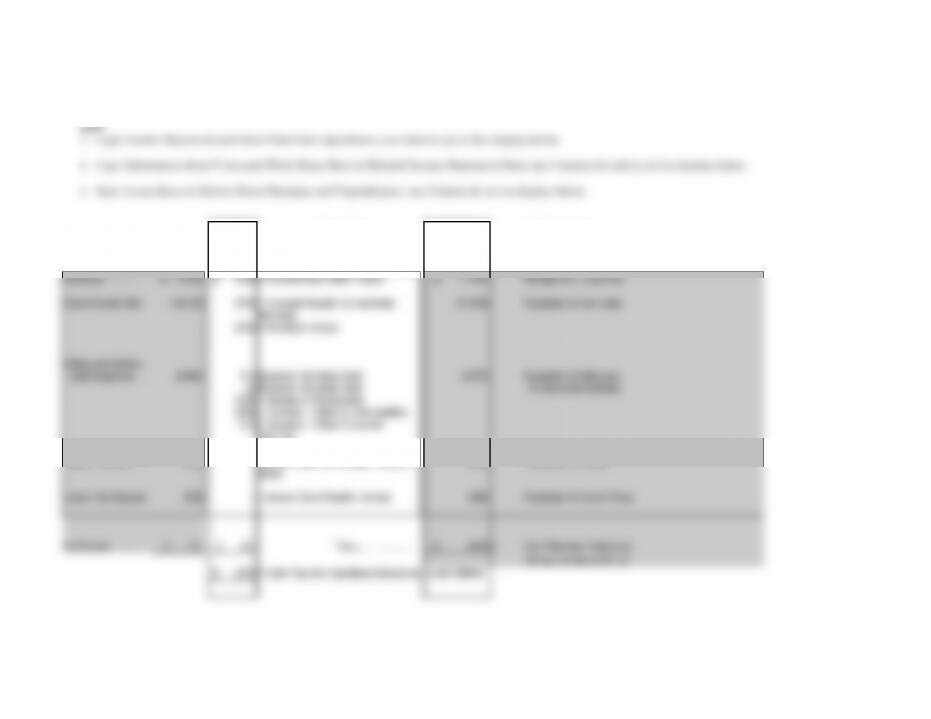

c. Deriving Direct Method Cash Flow from Operations Using Data from T-Account Work Sheet

(All Dollar Amounts in Thousands)

Indirect

Changes in

Direct

From Operations:

Operations, 2007

Method

Related Balance Sheet Accounts from

T-Account Work Sheet

Method

Receipts less Expenditures

(a)

(b)

(c)

(d)

2007

Revenues…………..

$ 22,833

$ (168)

= Accounts Receivable Increase

$ 22,665

Receipts from Customers

Cost of Goods Sold

(16,518)

(769)

= Accounts Payable for Inventories

Decrease

(17,919)

Payments for Inventories

(632)

= Inventory Increase

Selling and Adminis-

trative Expenses…. (4,849)

641

(Expense Not Using Cash)

(4,673)

Payments for Selling and

25

(Expense Not Using Cash)

Administrative Services

(154)

= Increase in Prepayments

(299)

= Decrease in Other Current Liabilities

(37)

= Decrease in Other Noncurrent

Liabilities

Interest Expense……

(459)

-

Interest Payable (no change in balance

sheet)

(459)

Payments for Interest

Income Tax Expense.

(590)

-

= Income Taxes Payable Increase

(590)

Payments for Income Taxes

Net Income……….…

$ 417

$ 417

Totals………………

$ (976)

=

Cash Flow from Operations

Derived via Direct Method

$ (976)

= Cash Flow from Operations Derived via Indirect Method

Solutions 5-44

5.36 continued.

d. Cash flow from operations was negative during 2007, despite positive

and prepayments with only minor reductions in current operating

liabilities. The small reductions in current operating liabilities

relative to the declines in current operating assets reflect either a

stretching of short-term creditors or a return to a normal level of

5.37 (CVS Caremark Corporation; interpreting a statement of cash flows based

on the direct method for presenting cash flow from operations.)

c. Amount Paid for Interest ................................................... $ 468.2

5-45 Solutions

Solutions 5-46

5.38 (CVS Caremark Corporation; interpreting a statement of cash flows based

on the direct method for presenting cash flow from operations.)

a. 2006

b. Cost of Revenues ................................................................. $ 32,079.2

Increase in Inventories for the Year .................................. 624.1

Purchases for Inventory ..................................................... $ 32,703.3

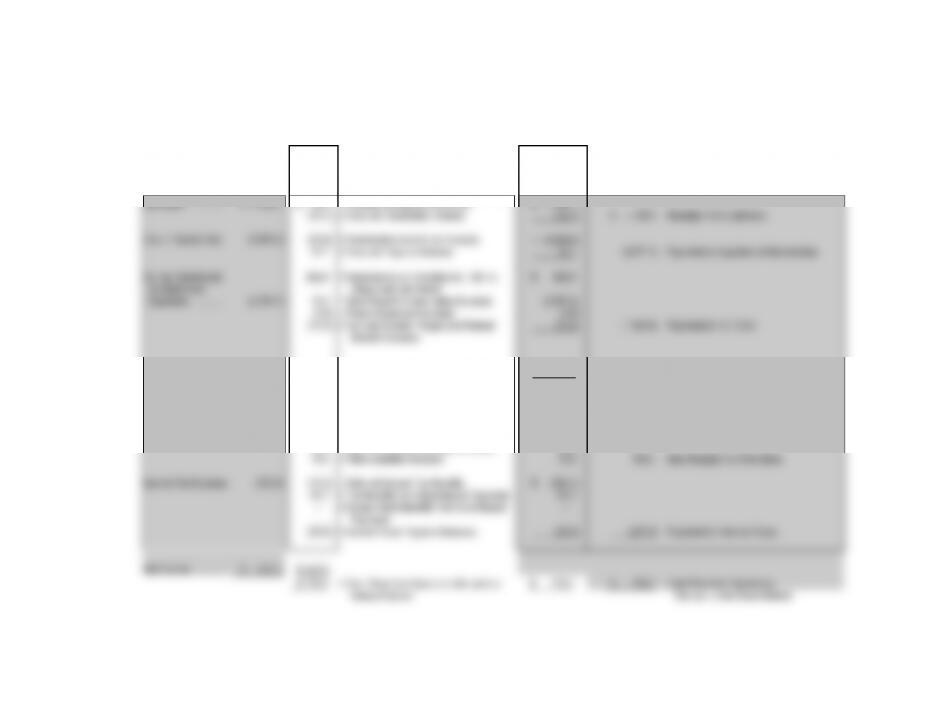

5.39 (Nordstrom Inc.; Derive cash flow from operations presented with the direct method from annual report presentation that uses the indirect

method.)

Deriving Direct Method Cash Flow from Operations Using Data from T-Account Work Sheet

(All Dollar Amounts in Millions)

Fiscal Year 2006

Indirect

Changes in

Direct

Operations

Method

Related Balance Sheet Accounts from

T-Account Work Sheet

Method

(a)

(b)

(c)

(d)

Net Sales .................

$ 8,560.7

$ 17.1

(61.3)

= Provision for Bad Debt Expense

= Accounts Receivable Increase

$ 8,577.8

(61.3)

$ 8,516.5 Receipts from Customers

Cost of Goods Sold ..

(5,353.9)

(38.6)

84.3

= Merchandise Inventories Increase

= Accounts Payable Increase

$ (5,392.5)

84.3

( 5,308.2) Payments to Suppliers of Merchandise

Selling General and

Administrative

Expenses ............... (2,296.9)

248.2

37.4

(4.7)

= Depreciation and Amortization, Net not

Using Cash this Period

= Stock-Based Compensation Expense

= Prepaid Expenses Increase

$ 248.2

(2,259.5)

(4.7)

48.7

= Accrued Salaries, Wages and Related

Benefits Increase

48.7

(1,967.3) Payments for S, G & A

Interest Expense ......

(42.8)

$ (42.8)

(42.8) Payments for Interest

Other Income, Net ....

238.5

128.0

= Asset Backed Securities Decrease

(Increase)

$ 366.5

(7.7)

= Other Assets Increase

(7.7)

23.5

= Other Current Liabilities Increase

23.5

30.7

= Deferred Property Incentives Increase

30.7

17.3

= Other Liabilities Increase

17.3

430.3 New Receipts for Other Items

Income Tax Expense

(427.6)

(58.3)

= Deferred Income Tax Benefits

$ (485.9)

43.6

= Tax Benefits from Stock-Based Payments

43.6

(38.3)

= Excess Stock Benefits from Stock-Based

Payments

(38.3)

(5.5)

= Income Taxes Payable Decrease

(5.5)

(486.1) Payments for Income Taxes

Net Income ...............

$ 678.0

$ 678.0

$ 1,142.4

= Cash Flow from Operations Derived via

$ 1,142.4

$ 1,142.4 Cash Flow from Operations

Indirect Method

Derived via the Direct Method

5.40 (Nordstrom Inc.; Derive cash flow from operations presented with the direct method from annual report presentation that uses the indirect

method.)

Deriving Direct Method Cash Flow from Operations Using Data from T-Account Work Sheet

(All Dollar Amounts in Millions)

Fiscal Year 2005

Indirect

Changes in

Direct

Operations

Method

Related Balance Sheet Accounts from

T-Account Work Sheet

Method

(a)

(b)

(c)

(d)

Net Sales .................

$ 7,722.8

$ 20.9

(15.1)

= Provision for Bad Debt Expense

= Accounts Receivable Increase

$ 7,743.7

(15.1)

$ 7,728.6 Receipts from Customers

Cost of Goods Sold ..

(4,888.0)

(20.8)

31.7

= Merchandise Inventories Increase

= Accounts Payable Increase

$ (4,908.8)

31.7

(4,877.1) Payments to Suppliers of Merchandise

Selling General and

Administrative

Expenses ............... (2,100.7)

242.9

13.3

(1.0)

= Depreciation and Amortization, Net not

Using Cash this Period

= Stock-Based Compensation Expense

= Prepaid Expenses Increase

$ 242.9

(2,087.4)

(1.0)

(11.3)

= Accrued Salaries, Wages and Related

Benefits Increase

(11.3)

(1,856.8) Payments for S, G & A

Interest Expense ......

(45.3)

$ (45.3)

(45.3) Payments for Interest

Other Income, Net ....

196.4

(135.8)

= Asset Backed Securities Decrease

(Increase)

$ 60.6

(3.5)

= Other Assets Increase

(3.5)

38.8

= Other Current Liabilities Increase

38.7

49.5

= Deferred Property Incentives Increase

49.5

19.3

= Other Liabilities Increase

19.3

164.6 New Receipts for Other Items

Income Tax Expense

(333.9)

(11.2)

= Deferred Income Tax Benefits

$ (345.1)

41.1

= Tax Benefits from Stock-Based Payments

41.1

--

= Excess Stock Benefits from Stock-Based

Payments

--

(33.9)

= Income Taxes Payable Decrease

(33.9)

(337.9) Payments for Income Taxes

Net Income ...............

$ 551.3

$ 551.3

$ 776.2

= Cash Flow from Operations Derived via

$ 776.2

$ 776,2 Cash Flow from Operations

Indirect Method

Derived via the Direct Method

5-49 Solutions

5.41 (Quinta Company; working backwards through the statement of cash

flows.)

QUINTA COMPANY

Condensed Balance Sheet

January 1, 2008

($ in 000's)

Assets

Current Assets:

Cash ................................................................. $ 20

Accounts Payable ............................................ $ 255

Other Current Liabilities ................................ 130

Total Current Liabilities ............................. $ 385

Bonds Payable ..................................................... 60

Shown below are T-accounts for deriving the solution. Entries (1)—(13)

are reconstructed from the statement of cash flows. Changes for the year

are appropriately debited or credited to end-of-year balances to get

Solutions 5-50

5-51 Solutions

5.41 continued.

Buildings Accumulated

Land and Equipment Depreciation

Other Current

Bonds Payable Common Stock Retained Earnings

Shown on the following page is the Transactions Spreadsheet. Entries (1)—(13)

are reconstructed from the statement of cash flows. Changes for the year are

appropriately debited or credited to end-of-year balances to get beginning-of-year

balances. Amounts are shown in thousands.

Solutions 5-52

5.41 continued.

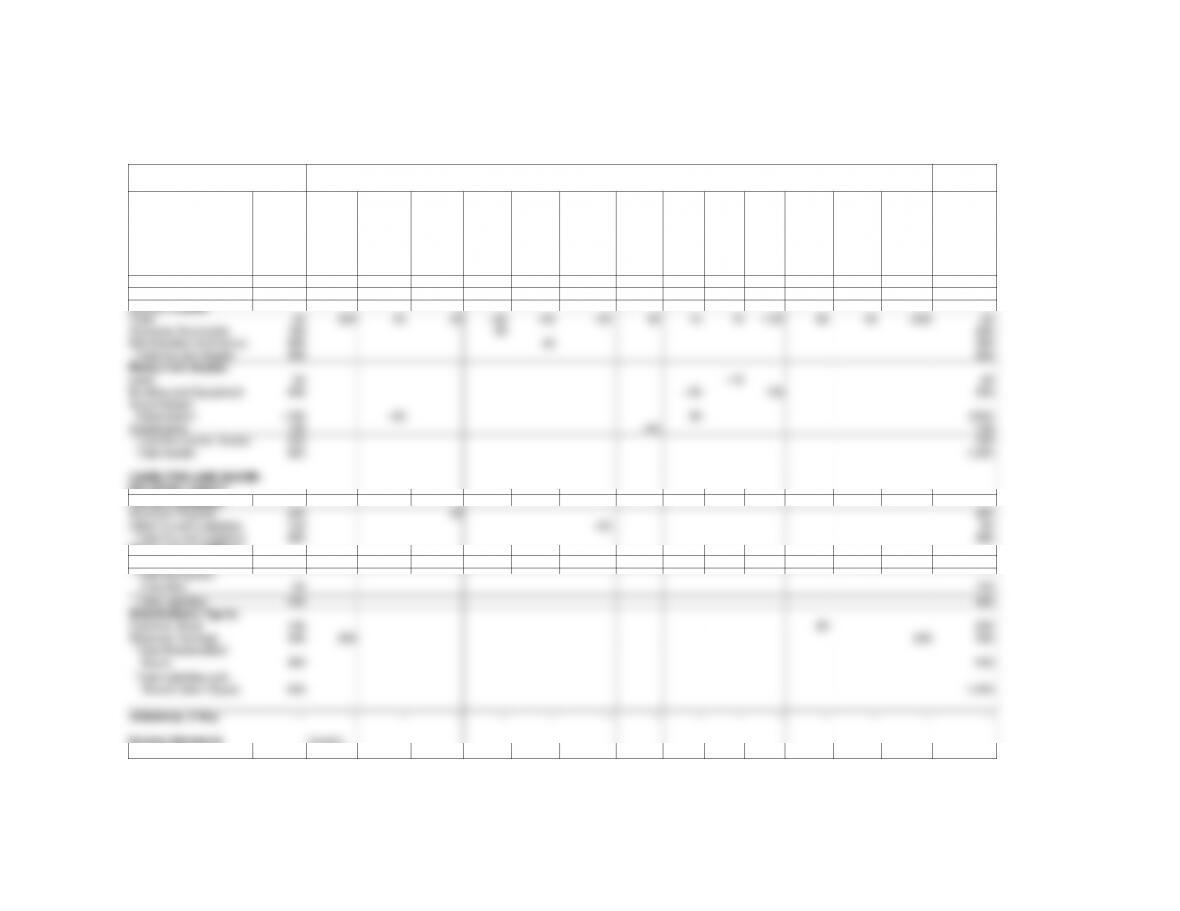

Following, we show the Transaction Spreadsheet for those who prefer to work problems with it, not with T-accounts.

Transactions spreadsheet.

Balance Sheet Accounts

Transactions, By Number and Description

Balance:

Begin-

ning of

Period

(Derived)

Net

Income

for Year

Depreci-

ation

Expense

Increase

in

Accounts

Payable

Increase

in

Accounts

Receiv-

able

Increase

in Mer-

chandise

Inven-

tories

Decrease

in Other

Current

Liabilities

Sale

of Invest-

ments

Sale of

Build-

ings

and

Equip-

ment

Sale of

Land

Acquire

New

Build-

ings

and

Equip-

ment

Issue

Common

Stock

Issue

Bonds

Payable

Dividends

Paid in

Cash

Balance:

End of

Period

(Given)

1

2

3

4

5

6

7

8

9

10

11

12

13

ASSETS

Current Assets:

Cash

20

200

60

25

–30

–40

–45

40

15

10

–130

60

40

–200

25

Accounts Receivable

190

30

220

Merchandise Inventories

280

40

320

Total Current Assets

490

565

Noncurrent Assets:

Land

50

–10

40

Building and Equipment

405

–35

130

500

Accumulated

Depreciation

–160

–60

20

(200)

Investments

140

–40

100

Total Noncurrent Assets

435

440

Total Assets

925

1,005

LIABILITIES AND SHARE-

HOLDERS’ EQUITY

Current Liabilities:

Accounts Payable

255

25

280

Other Current Liabilities

130

–45

85

Total Current Liabilities

385

365

Noncurrent Liabilities:

Bonds Payable

60

40

100

Total Noncurrent

Liabilities

60

100

Total Liabilities

445

465

Shareholders' Equity:

Common Stock

140

60

200

Retained Earnings

340

200

–200

340

Total Shareholders'

Equity

480

540

Total Liabilities and

Shareholders' Equity

925

1,005

Imbalance, if Any

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

Income Statement

Accounts

Income

Summary