12-1 Solutions

CHAPTER 12

MARKETABLE SECURITIES AND DERIVATIVES

Questions, Exercises, and Problems: Answers and Solutions

12.2 a. Debt securities that a firm intends to hold to maturity (for example, to lock

in the yield at acquisition for the full period to maturity) and has the ability

to hold to maturity (for example, the firm has adequate liquid assets and

b. The classification as “trading securities” implies a firm’s active involvement

in buying and selling securities for profit. The holding period of trading

c. Amortized acquisition cost equals the purchase price of debt securities

plus or minus amortization of any difference between acquisition cost and

Solutions 12-2

12-3 Solutions

12.2 continued.

d. Unrealized holding gains and losses occur when the fair value of a

e. Realized gains and losses appear in the income statement when a firm

12.3 Firms acquire trading securities primarily for their short-term profit potential.

Including the unrealized holding gain or loss in income provides the financial

12.4 The required accounting does appear to contain a degree of inconsistency.

One might explain this seeming inconsistency by arguing that the balance

sheet and income statement serve different purposes. The balance sheet

attempts to portray the resources of a firm and the claims on those users by

Solutions 12-4

12-5 Solutions

12.5 A derivative is a hedge when the firm bears a risk such that the change in the

value of the derivative attempts to offset the change in the value of the firm as

time passes. We distinguish an attempt at hedging from an effective hedge

Under this interpretation, a derivative is not a hedge when changes in the fair

If the firm chooses not to use hedge accounting when it could, the fluctuations

in the fair value of the derivative appear in income, not offset by the changes in

12.6 A

fair-value hedge

is a hedge of an exposure to changes in the fair value of a

12.7 Firms do not recognize the fair value of the commitment except to the extent

commitment.

12.8 The rationale relates to matching. Under a fair value hedge, firms report

recognized assets and liabilities at fair value and include unrealized gains and

losses in net income. Firms also report associated derivatives at fair value

Solutions 12-6

12-7 Solutions

12.9 To qualify for hedge accounting, there must be an expectation that the

derivative will be effective in hedging a particular risk. Obtaining a derivative

that will be highly effective in hedging a particular risk may be costly. A firm

12.10 This statement is correct. Firms would report all financial assets and financial

12.11 (Classifying securities.)

c. Securities available for sale; current asset.

d. Securities available for sale; noncurrent asset.

12.12 (Accounting principles for marketable securities and derivatives).

a. (4) The firm has option to use hedge accounting, deferring income

effects until realization and reporting changes in fair value in periodic

b. (1) This derivative is not an accounting hedge, so gains and losses

Solutions 12-8

c. (1) Because not both ability and intent to hold to maturity are present, it

d. (3) Standard treatment for securities available for sale.

12-9 Solutions

12.13 (Murray Company; accounting for bonds held to maturity.)

a. Present Value of Periodic Payments: $3,000 X 6.73274a = $ 20,198

b. See Schedule 12.1 below.

Schedule 12.1

Amortization Table for $100,000 Bonds with Interest Paid

Semiannually at 6% and Priced to Yield 8% Compounded

Semiannually

(Exercise 13)

Period

Balance at

Beginning

of Period

Interest

Revenue

for Period

Cash

Received

Portion of

Payment

Increasing

Carrying

Value

Balance

at End

of Period

1

$93,267

$3,731

$3,000

$731

$ 93,998

2

$93,998

$3,760

$3,000

$760

$ 94,758

3

$94,758

$3,790

$3,000

$790

$ 95,548

4

$95,548

$3,822

$3,000

$822

$ 96,370

5

$96,370

$3,855

$3,000

$855

$ 97,225

6

$97,225

$3,889

$3,000

$889

$ 98,114

7

$98,114

$3,925

$3,000

$925

$ 99,038

8

$99,038

$3,962

$3,000

$962

$ 100,000

c. January 1, 2008

Marketable Debt Securities ………………………………… 93,267

Cash ……………………………………………………………. 93,267

Solutions 12–10

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–93,267

+93,267

12–11 Solutions

12.13 c. continued.

June 30, 2008

Cash ……………………………………………………………….. 3,000

Marketable Debt Securities ………………………………… 731

Interest Revenue …………………………………………… 3,731

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+3,000

+3,731

IncSt → RE

+731

December 31, 2008

Cash ……………………………………………………………….. 3,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+3,000

+3,760

IncSt → RE

+760

d. December 31, 2011

Cash ……………………………………………………………….. 3,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+3,000

+3,962

IncSt → RE

+962

December 31, 2011

Cash ……………………………………………………………….. 100,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+100,000

–100,000

Solutions 12–12

12.14 (Kelly Company, accounting for bonds held to maturity.)

a. Present Value of Periodic Payments: $17,500 X 5.41719a = $ 94,801

b. See Schedule 12.2 below.

Schedule 12.2

Amortization Table for $500,000 Bonds with Interest Paid

Semiannually at 7% and Priced to Yield 6% Compounded

Semiannually

(Exercise 14)

Period

Balance at

Beginning

of Period

Interest

Revenue

for Period

Cash

Received

Portion of

Payment

Reducing

Carrying

Value

Balance

at End

of Period

(1)

(2)

(3)

(4)

(5)

(6)

1

$513,541

$15,406

$17,500

$(2,094)

$ 511,447

2

$511,447

$15,343

$17,500

$(2,157)

$ 509,291

3

$509,291

$15,279

$17,500

$(2,221)

$ 507,069

4

$507,069

$15,212

$17,500

$(2,288)

$ 504,781

5

$504,781

$15,143

$17,500

$(2,357)

$ 502,425

6

$502,225

$15,075a

$17,500

$(2,425)

$ 500,000

aAmount does not equal 3% of balance at the beginning of the period due to

rounding.

c. January 1, 2008

Marketable Debt Securities ………………………………… 513,341

12–13 Solutions

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–513,341

+513,341

Solutions 12–14

12.14 c. continued.

June 30, 2008

Cash ……………………………………………………………….. 17,500

Interest Revenue …………………………………………… 15,406

Marketable Debt Securities …………………………….. 2,094

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+17,500

+15,406

IncSt → RE

–2,094

December 31, 2008

Cash ……………………………………………………………….. 17,500

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+17,500

+15,343

IncSt → RE

–2,157

d. December 31, 2010

Cash ……………………………………………………………….. 17,500

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+17,500

+15,075

IncSt → RE

–2,425

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+500,000

–500,000

12–15 Solutions

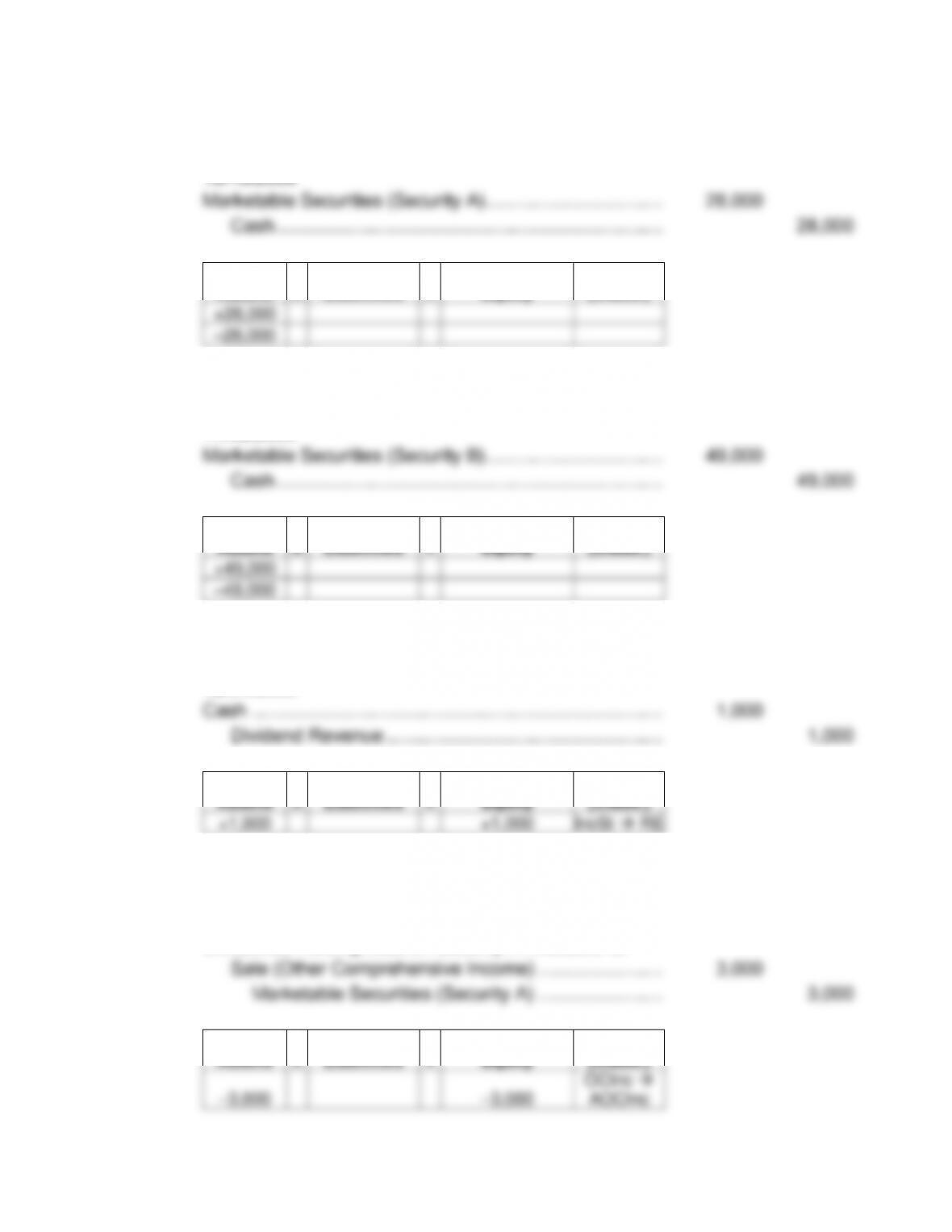

12.15 (Elston Corporation; accounting for securities available for sale.)

10/15/2008

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+28,000

–28,000

To record acquisition of shares of Security A.

11/02/2008

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+49,000

–49,000

To record acquisition of shares of Security B.

12/31/2008

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+1,000

+1,000

IncSt → RE

To record dividend received from Security B.

12/31/2008

Unrealized Holding Loss on Security A Available for

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–3,000

–3,000

OCInc →

AOCInc

Solutions 12–16

12–17 Solutions

12.15 continued.

12/31/2008

Marketable Securities (Security B) ……………………………. 6,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+6,000

+6,000

OCInc →

AOCInc

To record unrealized holding gain on Security B.

2/10/2009

Realized Loss on Sale of Securities Available for Sale

Marketable Securities (Security A) ………………….. 25,000

Unrealized Holding Loss on Security A

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+24,000

–4,000

IncSt → RE

–25,000

+3,000

OCInc →

AOCInc

To record sale of Security A.

12/31/2009

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+1,200

+1,200

IncSt → RE

To record dividend received from Security B.

Solutions 12–18

12.15 continued.

12/31/2009

Unrealized Holding Gain on Security B Available for

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–2,000

–2,000

OCInc →

AOCInc

To revalue Security B to market value.

7/15/2010

Cash ……………………………………………………………………. 57,000

Unrealized Holding Gain on Security B Available for

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+57,000

+8,000

IncSt → RE

–53,000

–4,000

OCInc →

AOCInc

To record sale of Security B.

12.16 (Simmons Corporation; accounting for securities available for sale.)

6/13/2008

12–19 Solutions

12.16 continued.

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+12,000

+29,000

+43,000

–84,000

To record acquisition of marketable equity securities as a

temporary investment.

10/11/2008

Cash ……………………………………………………………………. 39,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+39,000

–4,000

IncSt → RE

–43,000

To record sale of Security U.

12/31/2008

Unrealized Holding Gain on Security S Avail-

able for Sale (Other Comprehensive

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+1,500

+1,500

OCInc →

AOCInc

To revalue Security S to market value.

Solutions 12–20

12.16 continued.

12/31/2008

Unrealized Holding Loss on Security T Available for

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–2,800

–2,800

OCInc →

AOCInc

To revalue Security T to market value.

12/31/2009

Marketable Securities (Security S) (= $15,200 –

Unrealized Holding Gain on Security S Avail-

able for Sale (Other Comprehensive

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+1,700

+1,700

OCInc →

AOCInc

To revalue Security S to market value.

12/31/2009

Unrealized Holding Loss on Security T Avail-

able for Sale (from 12/31/2008 Entry)

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+5,500

+2,800

OCInc →

AOCInc