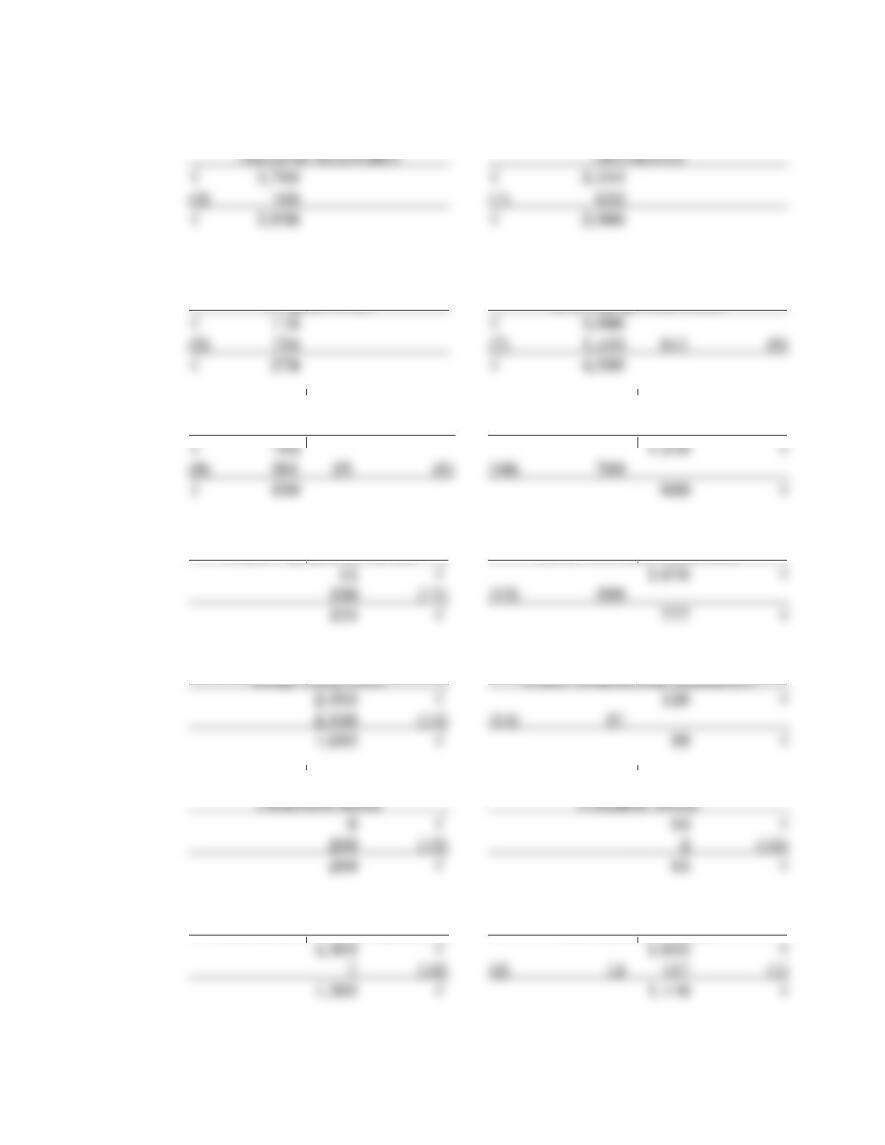

5.31 continued.

Change

in Cash

=

Change in

Liabilities

+

Change in

Shareholders’

Equity

–

Change in

Non-cash

Assets

+7,500

+7,500

(4) Increases by $7,500; operating increase in cash from increase in

Accounts Payable.

(5) Increases by $7,500; operating decrease in cash for increase in

inventory.

The net effect of these two transactions is to leave cash from

operations unchanged, because the amounts added and subtracted

change in such a way as to cancel out each other.

d. Inventory ………………………………………………………… 6,000

Change

Change in

Shareholders’

Non-cash

Solutions 5-22

5.31 e. continued.

f. Cash ………………………………………………………………. 1,450

Change

in Cash

=

Change in

Liabilities

+

Change in

Shareholders’

Equity

–

Change in

Non-cash

Assets

+1,450

Opns

–1,450

(1) Increases by $1,450 for collection of cash from customers.

(4) Increases by $1,450; operating increase in cash reflected by

decrease in the amount of Accounts Receivable. OK to show as a

reduction in the subtraction on Line (5).

g. Cash ………………………………………………………………. 10,000

Bonds Payable ………………………………………………. 10,000

Change

in Cash

=

Change in

Liabilities

+

Change in

Shareholders’

Equity

–

Change in

Non-cash

Assets

+10,000

+10,000

Finan

(8) Increases by $10,000; increase in cash from security issue.

(11) Increases by $10,000.

5-23 Solutions

5.31 continued.

h. Cash ………………………………………………………………. 4,500

Equipment (Net) …………………………………………… 4,500

Change

in Cash

=

Change in

Liabilities

+

Change in

Shareholders’

Equity

–

Change in

Non-cash

Assets

+4,500

Invst

–4,500

(6) Increases by $4,500; increase in cash from sale of noncurrent

asset.

(11) Increases by $4,500.

5.32 (Heidi’s Hide-Out; inferring cash flows from trial balance data.)

c. Wage Expense ……………………………………………………….…….. $ (20,000)

Less Increase in Advances to Employees ($1,500 –

Solutions 5-24

5-25 Solutions

5.33 (Digit Retail Enterprises, Inc.; inferring cash flows from balance sheet and

income statement data.)

b. Cost of Goods Sold ……………………………………………………….. $ (145,000)

Less Increase in Merchandise Inventory ($65,000 –

Year ………………………………………………………………………… $ (160,000)

d. Salaries Expense …………………………………………………………. $ (68,000)

g. Increase in Retained Earnings ($11,800 – $11,500) ………… $ 300

Less Net Income ………………………………………………………….. (9,600)

Solutions 5-26

5.33 continued.

$90,000) …………………………………………………………………… 10,000

5.34 (Hale Company; preparing and interpreting a statement of cash flows

using a T-account work sheet.)

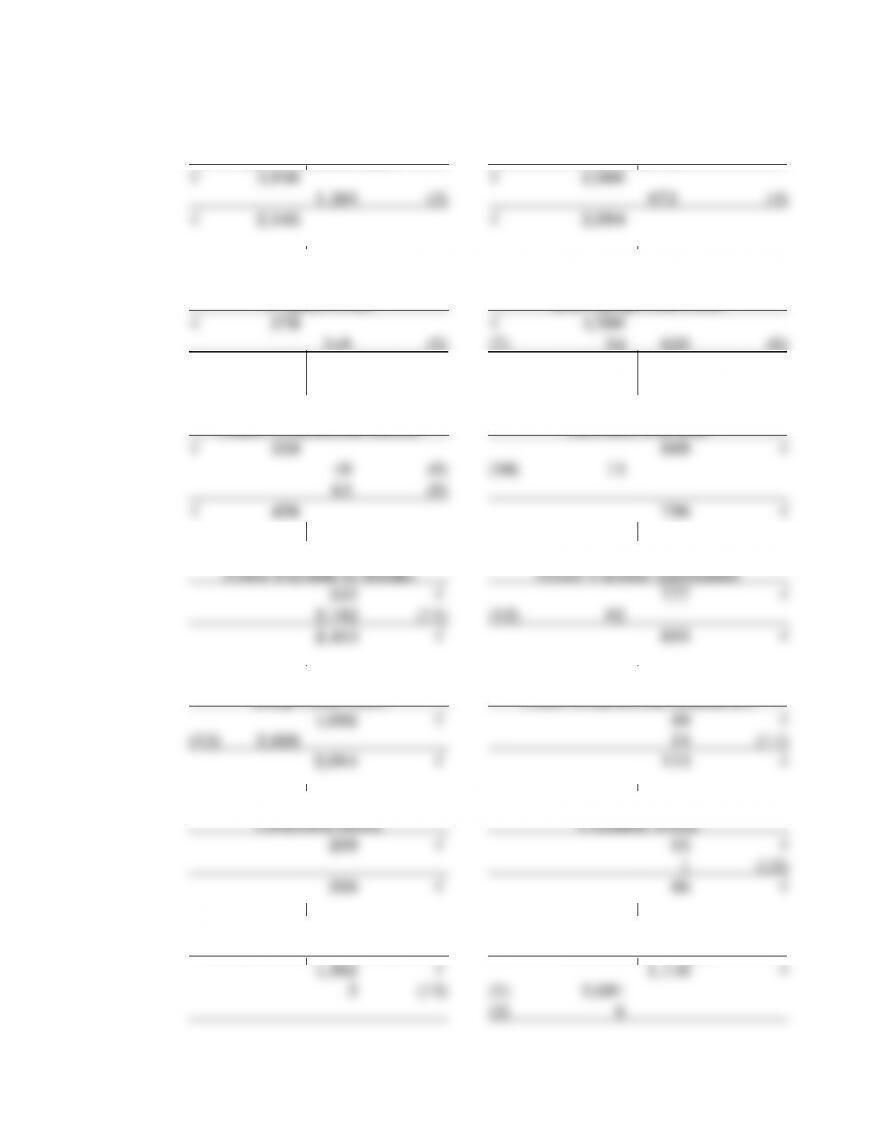

a. HALE COMPANY

Statement of Cash Flows

For the Year

Acquisition of Equipment ………………………………. (55,000)

Cash Flow from Investing ………………………………….. (50,000)

5-27 Solutions

5.34 a. continued.

The amounts in the T-account work sheet below are in thousands.

Cash

√ 52

Operations

Investing

Financing

√ 58

Accounts Receivable Inventory Land

Buildings and Accumulated

Solutions 5-28

5.34 a. continued.

Interest Payable Mortgage Payable Common Stock

4-29 Solutions

5.34 continued.

b. Deriving Direct Method Cash Flow from Operations Using Data from T-Account Work Sheet (All Dollar

Amounts in Thousands)

Indirect

Changes in

Direct

From

Operations:

Operations

Method

Related Balance Sheet Accounts from

T-Account Work Sheet

Method

Receipts less

Expenditures

(a)

(b)

(c)

(d)

Revenues………………

$1,200

$ (13)

= Accounts Receivable Increase

$ 1,187

Receipts from Customers

Cost of Goods Sold……

(788)

5

= Accounts Payable Increase

(794)

Payments for Merchandise

(11)

= Merchandise Inventory Increase

Wages and Salaries……

(280)

—

= Other Current Liabilities Increase

(280)

Payments for Wages and

Salaries

Depreciation Expense….

(54)

54

(Expense Not Using Cash)

—

Interest Expense………..

(12)

(2)

= Interest Payable Decrease

(14)

Payments for Interest

Income Tax Expense…..

(22)

—

= Income Taxes Payable Increase

(22)

Payments for Income Taxes

Net Income………………

$ 44

$ 44

Totals

$ 77

= Cash Flow from Operations

Derived via Direct Method

$ 77

= Cash Flow from Operations Derived via

Indirect Method

Solutions 5-30

5.34 continued.

c. Statement of Cash Flows presenting the direct method and a

reconciliation of income to cash flows from operations.

HALE COMPANY

Statement of Cash Flows

For the Year

Reconciliation of Net Income to Cash from Operations:

Net Income……………………………………………………. $ 44,000

Depreciation …………………………………………………. 54,000

Changes in Operating Accounts:

Investing Activities:

Cash Used for New Acquisition of Equipment ….. $ (55,000)

Cash Received from Disposition of Equipment …. 5,000

d. Cash flow from operations was sufficient to finance acquisitions of

equipment during the year. The firm used the excess cash flow to pay

dividends and retire long-term debt.

5-31 Solutions

5.35 (Dickerson Manufacturing Company; preparing and interpreting a

statement of cash flows using a T-account work sheet.)

a. DICKERSON MANUFACTURING COMPANY

Statement of Cash Flows

For the Year

Operations:

Net Income………………………………………………… $ 568,000

Cash Flow from Investing ………………………………. (1,029,000)

Financing:

Solutions 5-32

5.35 a. continued.

The amounts in the T-account work sheet below are in thousands.

Cash

√ 358

Operations

Investing

Financing

Accounts Receivable Inventory

√ 946 √ 1,004

5-33 Solutions

Solutions 5-34

5.35 a. continued.

Land Accounts Payable

b. Dickerson Manufacturing Company is heavily capital intensive. Its

5-35 Solutions

5.36 (GTI, Inc.; preparing and interpreting a statement of cash flows using a T–

account work sheet.) (Amounts in Thousands)

a.

T-Account Work Sheet for 2007

Operations

Investing

1,433 (7) Acquisition of

Property, Plant,

and Equipment

391 (9) Acquisition of

Patent

Financing

Solutions 5-36

5-37 Solutions

5.36 a. continued.

Property, Plant

Prepayments and Equipment (Net)

Other Noncurrent Assets Accounts Payable

Notes Payable to Banks Other Current Liabilities

Long-Term Debt Other Noncurrent Liabilities

Additional Paid-in Capital Retained Earnings

Solutions 5-38

5-39 Solutions

5.36 a. continued.

T-Account Work Sheet for 2008

Cash

√ 475

Operations

Investing

Financing

Solutions 5-40

5.36 a. continued.

Accounts Receivable Inventories

Property, Plant

Prepayments and Equipment (Net)

√ 122 √ 4,027

Other Noncurrent Assets Accounts Payable

Long-Term Debt Other Noncurrent Liabilities

Additional Paid-in Capital Retained Earnings