10–41 Solutions

10.31 continued.

g. Carrying Value of Liability: $1,000,000 X 107.1062% ……… $ 1,071,062

h. Interest expense for first six months is $39,535 (= .078/2 X $1,013,711).

Unrealized Gain:

Carrying Value before Unrealized Gain ………………………. $ 1,013,246

i. Interest expense for the second six months is $40,692 (= .083/2 X

Unrealized Gain:

Carrying Value before Unrealized Gain ………………………. $ 981,240

10.32 (Lowe’s; interpreting disclosures of long-term debt.)

a. The likely explanation is that Lowe’s issued these notes and bonds at face

Solutions 10–42

10.32 continued.

b.

Term to Coupon Historical

Issue Face Maturity at Issue Interest Market

Date Value Issue Date Price Rate Interest Rate

October $500 $496

2005 Million 10 Years Million5% 5.1%a

a= PV(.0255,20,12500000, 500000000,0). 5.1% = 2.55% X 2.

b= PV(.02805,60,13750000,500000000,0). 5.61% = 2.805% X 2.

c. Lowe’s has amortized some of the initial issue discount, so that the

carrying value on February 2, 2007 exceeds the issue price by the amount

d. Holders of the convertible notes receive a portion of their return in the

e. The weighted average historical market interest rate is higher than the

10–43 Solutions

f. Excess of Fair Value over Carrying Value on February 2, 2007:

$4,301 – $4,013 ……………………………………………………………… $ 288

Solutions 10–44

10.33 (IBM and Adair Corporation; accounting for lease by lessor and lessee.)

a. January 1, 2008

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+10,000

+10,000

Computer …………………………………………………………. 10,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+10,000

–10,000

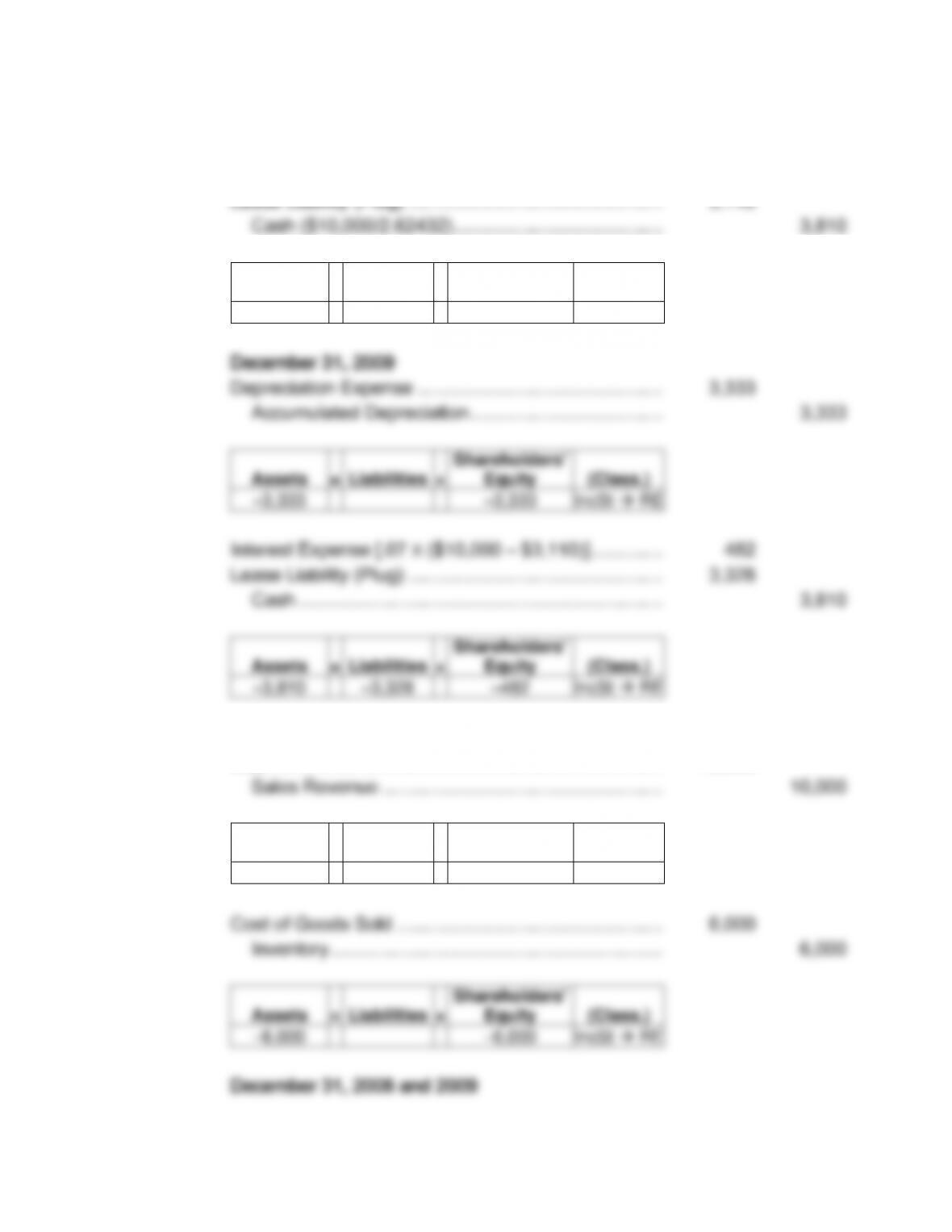

December 31, 2008

Depreciation Expense ……………………………………….. 3,333

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–3,333

–3,333

IncSt → RE

Interest Expense (.08 X $10,000) ………………………… 800

Cash ($10,000/2.57710) …………………………………. 3,880

Assets

=

Liabilities

+

Shareholders‘

Equity

(Class.)

–3,880

–3,080

–800

IncSt → RE

December 31, 2009

Depreciation Expense ……………………………………….. 3,333

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–3,333

–3,333

IncSt → RE

10–45 Solutions

10.33 a. continued.

Interest Expense [.08 X ($10,000 – $3,080)] ………….. 554

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–3,880

–3,326

–554

IncSt → RE

b. January 1, 2008

December 31, 2008

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–3,810

–3,810

IncSt → RE

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–3,810

–3,810

IncSt → RE

c. January 1, 2008

Leased Asset ……………………………………………………. 10,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+10,000

+10,000

Solutions 10–46

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–3,333

–3,333

IncSt → RE

10–47 Solutions

10.33 c. continued.

Interest Expense (.07 X $10,000) ………………………… 700

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–3,810

–3,110

–700

IncSt → RE

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–3,333

–3,333

IncSt → RE

Interest Expense [.07 X ($10,000 – $3,110)] ………….. 482

Lease Liability (Plug) …………………………………………. 3,328

Cash ……………………………………………………………. 3,810

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–3,810

–3,328

–482

IncSt → RE

d. January 1, 2008

Cash ……………………………………………………………….. 10,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+10,000

+10,000

IncSt → RE

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–6,000

–6,000

IncSt → RE

December 31, 2008 and 2009

Solutions 10–48

10.33 continued.

e. January 1, 2008

Computer Equipment …………………………………………. 6,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+6,000

–6,000

December 31, 2008

Depreciation Expense ……………………………………….. 2,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–2,000

–2,000

IncSt → RE

Cash ……………………………………………………………….. 3,810

+3,810

IncSt → RE

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–2,000

–2,000

IncSt → RE

Shareholders’

+3,810

IncSt → RE

10.33 continued.

f. January 1, 2008

Lease Receivable ……………………………………………… 10,000

Sales Revenue ……………………………………………… 10,000

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

+10,000

+10,000

IncSt → RE

Assets

=

Liabilities

+

Shareholders’

Equity

(Class.)

–6,000

–6,000

IncSt → RE

Shareholders’

Assets

=

Liabilities

+

(Class.)

IncSt → RE

10–51 Solutions

10.33 continued.

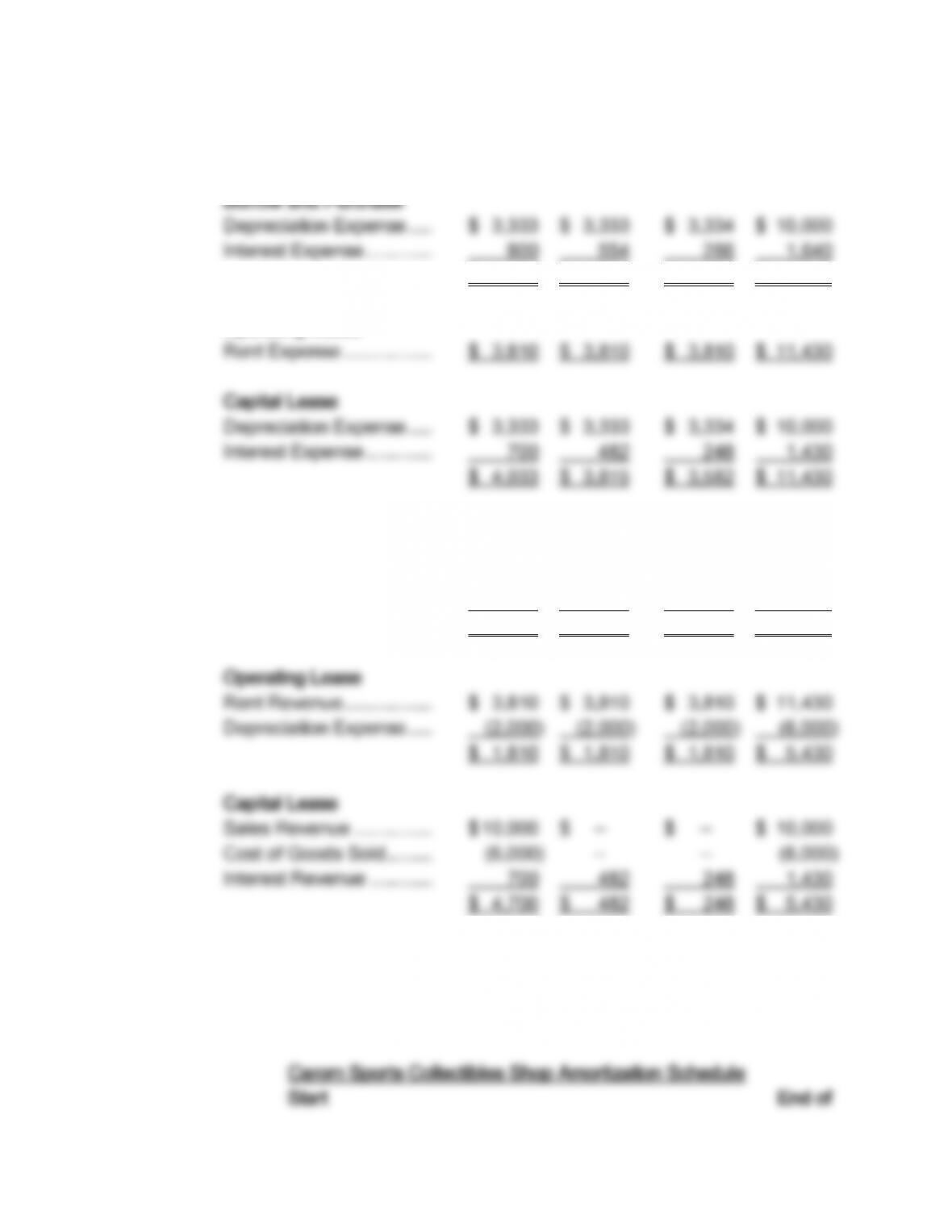

g. Lessee 2008 2009 2010 Total

$ 4,133 $ 3,887 $ 3,620 $ 11,640

Operating Lease

h. Lessor 2008 2009 2010 Total

Sale

Sales Revenue …………… $ 10,000 $ — $ — $ 10,000

Cost of Goods Sold ……… (6,000) — — (6,000)

$ 4,000 $ — $ — $ 4,000

10.34 (Carom Sports Collectibles Shop; comparison of borrow/buy with operating

and capital leases.)

a. $100,000/3.79079 = $26,379.725 = $26,380.

Solutions 10–52

of Year Interest Year

Year Balance (10%) Payment Reduction Balance