4-

1

Notes

CHAPTER 4

INCOME STATEMENT: REPORTING THE RESULTS OF OPERATING

ACTIVITIES

I. Learning Objectives

1. Understand the classifications of revenues and expenses on the income

statement and the importance of those classifications.

2. Understand the timing of revenue and expense recognition and their

measurement.

3. Understand the concept of comprehensive income and the relation between

net income and comprehensive income.

4. Develop skills to analyze the relations among revenues, expenses, and net

income, and understand how differences in business models affect those

relations.

II. Organization of Class Sessions

Because of the importance of the material in Chapter 4 to an

understanding of much of accounting, we spend four hours of class time on it.

We spend one hour developing an understanding of the classifications of

revenues and expenses on the income statement and the importance of those

classifications. We then spend two hours of class time on Understand the

timing of revenue and expense recognition, their measurement, and the

concept of comprehensive income and the relation between net income and

comprehensive income. We spend the last hour working Problems 4.34, 4.35, or

4.36. We find that these are excellent devices for testing comprehension of

material in the first four chapters.

III. Lecture Outline

1. Understand the classifications of revenues and expenses on the income

statement and the importance of those classifications.

Begin by illustrating with U.S. GAAP and IFRS which allow significant

latitude with respect to whether and how to aggregate revenues from multiple

business lines (segments) on the income statement. We discuss typical ways

income statements classify and display items. Chapter 2 introduces the income

statement, one of the principal financial statements. The income statement is

Notes 4-

2

also called the statement of operations or the statement of operating activity,

or the statement of profit and loss.

The income statement begins with revenues followed by a list of expenses.

U.S. GAAP and IFRS requirements for the presentation of income statements

are similar, with some important differences. Then explain the meaning terms,

concepts and why accountants treat interest as an expense in measuring net

income but do not treat dividends on common stock as an expense. And also

why is it important to separate gains from revenues. Other than separating

revenues from expenses, U.S. GAAP provides little guidance about which items

the firm must separately display or their order. IFRS requires, at a

minimum,the separate display of revenues, financing costs (for Example,

interest expense), income tax expense, profit or loss for the period, and certain

other items.

Income statements begin with revenues; for this reason, analysts often

refer to revenue growth as “top–line” growth. In Chapter 2 we define revenues

(or sales, sales revenues, or for some non-U.S. firms, turnover) as the inflow of

net assets (for Example, cash or receivables) received in exchange for providing

goods and services. U.S. GAAP and IFRS allow significant latitude with

respect to whether and how to aggregate revenues from multiple business lines

(segments) on the income statement; there is no requirement that a firm with

multiple segments separately disclose on the income statement the revenues of

each segment.

The word net before the word sales means that sales revenues less

discounts, allowances, and returns; we revisit these topics later in this chapter.

Net income or profit for a period is the difference between revenues from

selling goods and services and the expenses incurred to generate those

revenues, plus some gains or losses of the period. If the expenses plus losses

exceed the revenues plus gains, the result is a net loss. U.S.GAAP and IFRS

require the accrual basis of accounting, which detaches the recognition of

revenue from the receipt of cash.

For each revenue and expense component, have the students discuss

whether the treatment under the cash basis gives a fair measurement of

performance for the period. Their suggestions as to a more desirable treatment

of some items lead directly into the accrual basis of accounting. We find this

initial overview of the two methods a useful introduction. Problems 4.34, and

4.35 relate to the classifications of revenues and expenses on the income

statement.

2. Understand the timing of revenue and expense recognition and their

measurement.

4-

3

Notes

Next, consider the recognition of revenue under the accrual basis.

Criteria for Revenue Recognition and its Measurement and Application of

Revenue Recognition Criteria. Chapter 7 introduces criteria for a firm to use

in deciding when to recognize revenue (timing) and how much revenue to

recognize (measurement). Recognizing revenue often triggers the recognition

of expenses associated with those revenues. We therefore discuss the

accounting procedures for recognizing both revenues and expenses. We

describe the concept of comprehensive income and distinguish net income

from comprehensive income.

Revenue recognition refers to the timing and measurement of revenues.

Revenue recognition is among the most complex issues in financial reporting.

The U.S. GAAP contains over 200 pieces of authoritative guidance for

recognizing revenues. The quantity and complexity of this guidance result

from several factors. First, misreporting of revenues (either reporting

revenues before the firm earns them or reporting nonexistent revenues)

Second, firms often bundle products and services and sell them in multiple-

element arrangements, and each element of the arrangement has the

potential to result in revenue recognition. As a general principle, under the

accrual basis of accounting, the firm recognizes revenue when the transaction

meets both of the following conditions: Completion of the earnings process.

and Receipt of assets from the customer.

The seller measures revenue as the amount of cash, or the cash-

equivalent value of other assets, that it receives from customers. As a starting

point, this amount is the exchange price between buyer and seller at the time

of sale. If the firm has not performed all of its obligations, however, it will

need to adjust the exchange price to reflect those unperformed obligations.

Two common examples of adjustments are sales discounts and allowances,

and sales returns.

We emphasize the recognition of revenue at the time firms sell goods or

render services. We use Exercises 4.11 or 4.12 here. These are excellent short

discussion questions that help students identify the appropriate revenue

recognition point in a variety of situations.

Criteria for expense Recognition is whether the consumption of the asset

results from a transaction that leads to the recognition of revenue and the

consumption of the asset results from the passage of time. In case of Expense

measurement, expenses measure the consumption of assets during an

accounting period, so the basis for expense measurement is the same as the

measurement of the consumed asset. If the firm measures an asset at

acquisition cost on the balance sheet, it also measures expenses based on the

acquisition cost of the asset consumed.

Notes 4-

4

The chapter concludes by describing how to analyze common-size income

statements to understand how a given firm performs over time, to explain

that performance, and to compare performance across firms. Consider the

recognition of expenses and its measurement under the accrual basis. We

emphasize the matching convention as it applies to merchandising and service

firms here, omitting consideration of product costs for a manufacturing firm

for the most part. Exercises 4.13 and 4.14 are excellent short discussion

questions.

3. Understand the concept of comprehensive income and the relation

between net income and comprehensive income.

Demonstrate the relation between the balance sheet and income

statement. Point out that revenues and expenses increase and decrease

retained earnings, respectively. We enter transactions and other events that

affect net income in separate revenue and expense accounts during the period.

After preparing an income statement for the period, we close these

revenue and expense accounts by transferring their balances to the Retained

Earnings account. Net income under U.S. GAAP, or profit under IFRS, reports

increases in net assets from certain transactions with nonowners such as

customers. Net income, or profit, does not include all transactions with

nonowners. Both U.S. GAAP and IFRS define net income, or profit, for the

current period to exclude certain events and transactions with nonowners that

change net assets.

Both U.S. GAAP and IFRS use the term Other Comprehensive Income

(OCI) to refer to changes in net assets that are not transactions with owners

and that do not appear on the income statement. The sum of net income and

other comprehensive income is Comprehensive Income, which includes all

changes in net assets for a period except for changes arising from transactions

with owners.

The students should observe that both U.S. GAAP and IFRS specify the

items that do not appear in the income statement and that are included in

other comprehensive income. Next, we work several problems that require

students to enter transactions and other events in T-accounts. Problems 4.25,

4.26, 4.27, 4.28, 4.29 and 4.30.

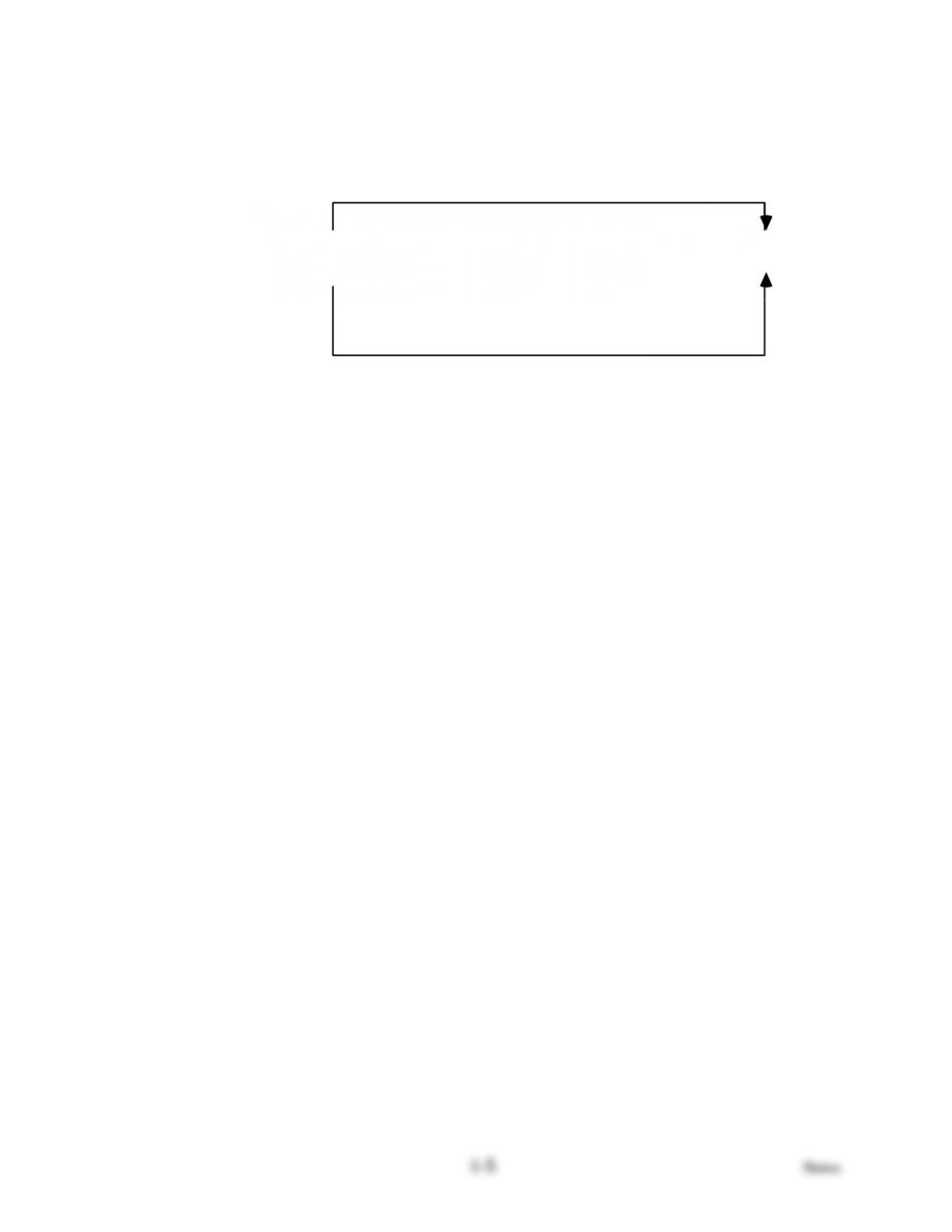

Finally, some time is spent at this point in the course integrating the

accrual basis of accounting with cash receipts and disbursements. We find the

following diagram to be helpful in linking the income statement and

statement of cash receipts and disbursements.

Given any three of the four statements, we can derive the fourth one. The

usual accounting problem gives (1), (2), and (3), and asks for (4).

(2) Income Statement (Accrual Concept)

(3) Statement of Cash Receipts

and Disbursements

(1) Balance Sheet

Beginning of the Period

(4) Balance Sheet

End of the Period

The last few problems provided in the text require a thorough

understanding of the accrual basis of accounting. Because of the complexity

and length of these problems, you might prefer assigning them over two or

three class periods.

We ask students to use the transactions spreadsheet to prepare solutions

to these problems. They should enter the given information and reprogram

the spreadsheet to solve for unknown amounts.

4. Develop skills to analyze the relations among revenues, expenses, and

net income, and understand how differences in business models affect

those relations.

Users of financial statements often analyze the ratio of net income to

revenues, called the profit margin percentage, when evaluating profitability.

Students should consider the following firms and their profit margin

percentages for a recent year:

A. Nordstrom (retail clothing): 7.9%.

B. Scania (engine and truck manufacturing): 8.4%.

C. Colgate Palmolive (consumer and pet products): 11.1%.

D. Polo Ralph Lauren (clothing design and manufacture): 9.3%.

E. McDonald’s (retail food): 16.4%.

F. Boeing (airplane manufacture): 3.6%.

Looking above results we should be in a position to analyze that we can we

conclude that Boeing and McDonald’s have the worst and best profitability,

respectively? Do differences in profit margin percentages signal differences in

operating performance, and do they have economic or strategic explanations?

Answering these questions requires understanding both the income

statement and investments in assets that firms in different industries must

Notes 4-

6

have in order to generate revenues. In this section, we focus on tools for

understanding the income statement, recognizing that the analysis of

profitability and operating performance also requires consideration of the

assets used to generate profits.

We merely introduce interpretation of the income statement at this point

in the course because we treat it more fully in Chapter 6. Problems 4.31, 4.32,

4.33, 4.34, and 4.35 work well for this purpose.