A-1 Solutions

APPENDIX

TIME VALUE OF CASH FLOWS

Questions, Exercises, and Problems: Answers and Solutions

A.2 The value of cash flows differs over time because cash can earn interest.

A.3 In simple interest, only the principal sum earns interest. In compound

A.4 There is no difference; these items refer to the same thing.

A.5 The timing of the first payment for an annuity due is now (at the beginning

(1) Guess a rate.

(2) Compute the net present values of the cash flows using the current

guess.

Solutions A-2

(5) Otherwise, the current guess is the implicit rate of return.

A-3 Solutions

A.9 The formula assumes that the growth [represented by the parameter g in

the formula 1/(r – g)] continues forever. That is a long time. The formula

A.10 a. $5,000 X 3.20714 X 1.06 = $16,998.

A.14 a. ¤90,000 X 14.20679 X 1.05 = ¤90,000 X (15.91713 – 1.0) = ¤1,342,542.

b. ¤90,000 X 18.53117 X 1.10 = ¤90,000 X (21.38428 – 1.0) = ¤1,834,585.

Solutions A-4

A.16 continued.

b. Asking questions about compound interest calculations on

examinations presents a difficult logistical problem to teachers. They

A.17 (Effective interest rates.)

a. 12% per period; 5 periods.

A.18 a. $100 X 1.21665 = $121.67.

A.19 a. $100 X .30832 = $30.83.

A.20 a. $100 X 14.23683 = $1,423.68.

A-5 Solutions

Solutions A-6

A.21 a. $1,000(1.00 + .94340) + $2,000(4.21236 – .94340) + $2,500(6.80169 –

4.21236) = $14,955.

3.79079) = $12,593.

A.22 a. $3,000 + ($3,000/.06) = $53,000.

A.24 a. $60,000 + ($60,000/.1664) = $420,577. (1.08)2 – 1 = .1664.

b. $60,000 + ($60,000/.2544) = $295,850. (1.12)2 – 1 = .2544.

A.27 a. 16% = ($67,280/$50,000)1/2 – 1.

b. Amount

Carrying (Reducing) Carrying

Value Interest Increasing Value

Start for Year Carrying End of Year

A-7 Solutions

A.28 (Berman Company; find implicit interest rate; construct amortization

schedule.)

b. Amount

(Reducing)

Carrying Payment Increasing Carrying

Value Interest End of Carrying Value

Start for Year Year Value End of Year

Year of Year = (2) X .14 (Given) = (3) – (4) = (2) + (5)

(1) (2) (3) (4) (5) (6)

1 $ 86,000 $ 12,040 $ 8,000 $ 4,040 $ 90,040

2 90,040 12,605 8,000 4,605 94,645

A.29 a. Terms of sale of 2/10, net/30 on a $100 gross invoice price, for example,

b. Table 1 can be used. Use the 2% column and the 18-period row to see

that the rate implied by 2/10, net 30 must be at least 42.825% (=

1.42825 – 1).

A.30 (Present value of a perpetuity.)

Solutions A-8

A-9 Solutions

A.32 a. Will: $24,000 + $24,000(3.31213) = $103,488.72 (Preferred).

Dower Option: $300,000/3 = $100,000.

A.34 $1.00(1.00 + .92456 + .85480 + .79031 + .73069) = $1.00 X 4.30036 = $4.30.

A.35 $600/12 = $50 saved per month. $2,000/$50 = 40.0.

A.36 a. $ 3,000,000 X 7.46944 = $ 22,408,320.

Solutions A-10

A.37 (Friendly Loan Company; find implicit interest rate; truth-in lending laws

reduce the type of deception suggested by this problem.)

The effective interest rate is 19.86% and must be found by trial and error.

A.38 (Black & Decker Company; derive net present value/cash flows for decision

to dispose of asset.)

$40,698. The $100,000 is gone and an economic loss of $50,000 was

A-11 Solutions

Solutions A-12

A.39 (Lynch Company/Bages Company; computation of present value of cash

flows; untaxed acquisition, no change in tax basis of assets.)

A.40 (Lynch Company/Bages Company; computation of present value of cash

flows; taxable acquisition, changing tax basis of assets.)

$4,258,199. If the merger is taxable, then the value of the firm V satisfies:

(1) V = 8.51356 X [$700,000 – .40($700,000 – V/20)]

A.41 (Valuation of intangibles with perpetuity formulas.)

a. $50 million = $4 million/.08.

A-13 Solutions

A.42 (Ragazze; analysis of benefits of acquisition of long-term assets.)

a. $270,831.

Cash Cash

Inflows Outflows Total Present

Operating Test (1) + (2) Values at 12%

Dec. 31 Receipts Salvage Maintenance Runs – (3) – (4) Factor Cash Flow

Year (1) (2) (3) (4) (5) (6) (7)

Solutions A-14

A-15 Solutions

A.43 (Gulf Coast Manufacturing; choosing between investment alternatives.)

Basic Data Repeated from Problem Present Value Computations

Mercedes- Mercedes-

Lexus Benz Factor Source [B] Lexus Benz

Initial Cost at the Start of 2008 …………. $60,000 $45,000 1.00000 $ 60,000 $ 45,000

[B]T[i,j,r] means Table i (= Table 2 or Table 4) from the back of the book, row j, interest rate r.

a. Strategy L, buying one Lexus has lower present value of costs, but the difference is so small that we’d encourage the CEO to go

Solutions A-16

A.44 (Wal-Mart Stores; perpetuity growth model derivation of results in Chapter

6.)

a. Reproduce Exhibit 6.22 for Problem A.43.

Growth Rate for Terminal Value: 10.0%

Factor to Present

Discount Value at

End of Cash to End of End of 2008

Year Flow 2008 Origin of Factor 14 = [2] X [3]

[1] [2] [3] [4] [5]

Note A: ($7,884 X 1.10)/(.12 – .10) = $433,620.

Numerator is the amount of the first collection, at the end of

2014.

A-17 Solutions

A.44 continued.

b. Change Growth Rate.

Growth Rate for Terminal Value: 9.0%

Factor to Present

Discount Value at

End of Cash to End of End of 2008

Year Flow 2008 Origin of Factor 14 = [2] X [3]

[1] [2] [3] [4] [5]

c. Change Growth Rate.

Growth Rate for Terminal Value: 5.0%

Factor to Present

Discount Value at

End of Cash to End of End of 2008

Year Flow 2008 Origin of Factor 14 = [2] X [3]

[1] [2] [3] [4] [5]

Solutions A-18

A.44 continued.

d. Comment. In models such as this, the total valuation comes largely

from the terminal value. The terminal value changes more than

A.45 (Fast Growth Start–Up Company; valuation involving perpetuity growth

model assumptions. (Amounts in Millions)

We find the answer with trial and error, starting with 5 years of fast

Free Discount

End of Cash Factors Present Value

Year Flow from Table 2 End of Year 0

0 $ 100 1.00000 $ 100.0

1 125 0.86957 108.7

A-19 Solutions

A.45 continued.

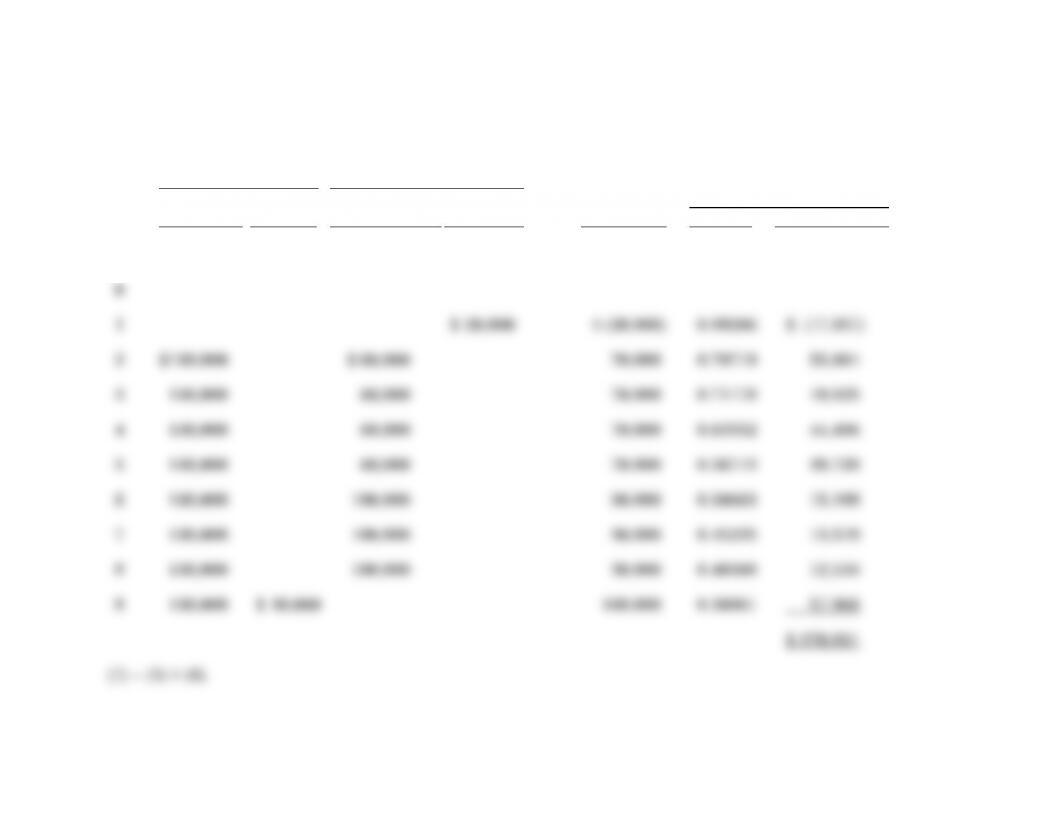

Growth Rate for Early Years of Fast Growth: 25%

Growth Rate for Steady State, Terminal Value: 4%

Discount Rate: 15%

Number of Years of Fast Growth: 6

Free Discount

End of Cash Factors Present Value

Year Flow from Table 2 End of Year 0

0 $ 100 1.00000 $ 100.0

1 125 0.86957 108.7

2 156 0.75614 118.1

Free Discount

End of Cash Factors Present Value

Year Flow from Table 2 End of Year 0

0 $ 100 1.00000 $ 100.0

1 125 0.86957 108.7

Solutions A-20