Below is the income statement for Year 8 that was prepared after making appropriate adjusting entries for Year

8.

Spiller Services Corporation

Income Statement

For the Year Ended December 31, Year 8

Fee Revenues

$199,400

Interest Revenue on

Notes Receivable

11,500

Total Revenues

$210,900

Depreciation Expense

(15,500)

Rent Expense

(18,700)

Insurance Expense

(11,800)

Office Supplies Expense

(11,500)

Office Salaries Expense

(124,000)

Net Income

$ 29,400

Required:

Give the adjusting entries that Spiller Services Corporation must have made at the end of Year 8 for each of the

seven income statement accounts. You may express the adjusting entries either in the form of journal entries or

T accounts.

Note that Cash is seldom involved in an adjusting entry. As cash flowed in or out of the firm from actual

transactions during the period, the cash account was debited or credited.

1.

Fees Receivable

4,400

Fee Revenues ($199,400 – $195,000)

4,400

2.

Interest Receivable

11,500

Interest Revenue on Notes Receivable

11,500

3.

Depreciation Expense

15,500

Accumulated Depreciation

15,500

4.

Prepaid Rent

800

Rent Expense

800

Note that the firm must have debited rent expense for all rent paid during Year 8. Some of the expenditure

during Year 8 must relate to rental services after Year 8. Thus, the firm must reverse part of the amount

expensed and set it up as prepaid rent.

5.

Insurance Expense

11,800

Prepaid Insurance

11,800

6.

Office Supplies Expense

11,500

Office Supplies Inventory

11,500

7.

Office Salaries Expense ($124,000 – $122,500)

1,500

Office Salaries Payable

1,500

110. Forgetful Corporation neglected to make various adjusting entries on December 31, Year 8. Indicate the

effects on assets, liabilities, and shareholders’ equity on December 31, Year 8 of failing to adjust for the

following independent items as appropriate, using the notation O/S (overstated), U/S (understated), and No (no

effect). Also, give the amount of the effect. Ignore income tax implications. Use the following format:

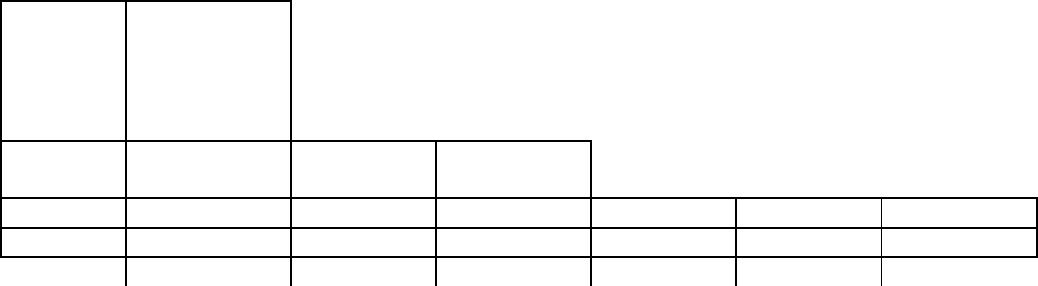

Effect of Errors

or Omissions on

December 31,

Year 8 Balance

Sheet

Assets

Liabilities

Shareholders’

Equity

Item

Direction

Amount

Direction

Amount

Direction

Amount

a.

On December 15, Year 8, Forgetful Corporation received a $1,400 advance from a customer for

products to be manufactured and delivered in January, Year 9. The firm recorded the advance by

debiting Cash and crediting Sales Revenue and has made no adjusting entry as of December 31, Year

8.

b.

On July 1, Year 8, Forgetful Corporation acquired a machine for $5,000 and recorded the acquisition

by debiting Cost of Goods Sold and crediting Cash. The machine has a five-year useful life and zero

estimated salvage value.

c.

On November 1, Year 8, Forgetful Corporation received a $2,000 note receivable from a customer in

settlement of an accounts receivable. It debited Notes Receivable and credited Accounts Receivable

upon receipt of the note. The note is a six-month note due April 30, Year 9 and bears interest at an

annual rate of 12 percent. Forgetful Corporation made no other entries related to this note during Year

8.

d.

Forgetful Corporation paid its annual insurance premium of $1,200 on October 1, Year 8, the first day

of the year of coverage. It debited Prepaid Insurance $900, debited Insurance Expense $300, and

credited Cash for $1,200. It made no other entries related to this insurance during Year 8.

e.

The Board of Directors of Forgetful Corporation declared a dividend of $1,500 on December 31, Year

8. The dividend will be paid on January 15, Year 9. Forgetful Corporation neglected to record the

dividend declaration.

f.

On December 1, Year 8, Forgetful Corporation purchased a machine on account for $50,000, debiting

Machinery and crediting Accounts Payable for $50,000. Ten days later, the account was paid and the

company took the allowed 2 percent discount. Cash was credited $49,000, Miscellaneous Revenue

was credited $1,000, and Accounts Payable was debited $50,000. It is the policy of Forgetful

Corporation to record cash discounts taken as a reduction in the cost of assets. On December 28, Year

8, the machine was installed for $4,000 in cash; Maintenance Expense was debited and Cash was

credited for $4,000. The machine started operation on January 1, Year 9. As the machine was not

placed into operation until January 1, Year 9, as appropriate, no depreciation expense was recorded

for Year 8.

Effect of Errors or Omissions on December 31, Year 8 Balance Sheet

Assets

Liabilities

Shareholders’

Equity

Item

Direction

Amount

Direction

Amount

Direction

Amount

a.

U

$1,400

O

$1,400

b.

U

$4,500

U

$4,500

c.

U

$ 40

U

$ 40

d.

e.

U

$1,500

O

$1,500

f.

U

$3,000

U

$3,000

111. Entries for the following items were either omitted or recorded incorrectly in preparing the financial

statements for Year 4. Indicate the amount and nature [understatement (U), overstatement (O), no effect (N)] of

the effect of the omission on total assets, total liabilities, and net income for Year 4. Ignore income tax effects.

Use the following format:

Total Assets

Total Liabilities

Net Income

a.

The company received a payment of $4,600 from a customer for an order that the company has not yet

produced. It credited the $4,600 to sales revenue.

b.

The company failed to record a dividend of $5,000 that was declared but not yet paid.

c.

The company repaid a loan of $5,000 to the bank. It recorded the transaction in the appropriate accounts

but in the amount of $50,000. The company has accounted for all interest on the loan correctly.

d.

The ending balance of finished goods inventory was incorrectly recorded at $4,000 more than its proper

balance due to a mistake in taking a physical inventory.

e.

The company correctly entered a stock issue of $22,000 on December 31, Year 4, in the cash account

but mistakenly credited it to Bonds Payable.

f.

On the basis of an incorrect report from the company’s credit collection agency, specific accounts

receivable of $2,700 were written off, but are actually expected to be collectible accounts. The company

correctly made a provision for estimated uncollectible accounts for year 4.

Total Assets

Total Liabilities

Net Income

a.

N

U; $4,600

O; $4,600

b.

N

U; $5,000

N

c.

U; $45,000

U; $45,000

N

d.

O; $4,000

N

O; $4,000

e.

N

O; $22,000

N

f.

N

N

N

112. Entries for the following items were either omitted or recorded incorrectly in preparing the financial

statements for Year 3. Indicate the amount and nature [understatement (U), overstatement (O), no effect (N)] of

the effect of the omission on total assets, total liabilities, and net income for Year 3. Ignore income tax effects.

Use the following format:

Total Assets

Total Liabilities

Net Income

a.

On December 1, Year 3, a firm debits Prepaid Rent (Advances to Car Rental Agency) for $600 for 6

months’ rent on an automobile. The firm has neglected to make the adjusting entry on December 31.

b.

A firm debits Administrative Expenses for $6,000 for a microcomputer acquired on July 1, Year 3.

The microcomputer has an expected useful life of 3 years and zero estimated salvage value.

c.

A firm rents out excess office space for the 6-month period beginning January 1, Year 3. It received

the rental check for this period of $600 on December 26, Year 2, and correctly credited Advances

from Tenants. It made no further journal entries during Year 3.

d.

Interest on Notes Receivable of $500 had accrued by December 31, Year 3, but the firm overlooked

making an entry to record this interest.

e.

A firm receives a check for $250 from a customer on December 31, Year 3, in settlement of an

account receivable. The firm recorded this entry with a credit to Sales.

f.

A firm records as $470 an expenditure of $740 for travel during December, Year 3.

Total Assets

Total Liabilities

Net Income

a.

O; 100

N

O; 100

b.

U; 5,000

N

U; 5,000

c.

N

O; 600

U; 600

d.

U; 500

N

U; 500

e.

O; 250

N

O; 250

f.

O; 270

N

O; 270

113. When examining the work an accountant performs for many organizations, many of the challenges revolve

around creating adjusting entries that bring the accounts into an accrual accounting basis. Four such adjusting

entries may include accounting for accrued revenues (unrecorded revenues), accrued expenses (unrecorded

expenses), deferred revenue (previously recorded revenues), and deferred expenses (previously recorded

expenses).

Required:

For each type of adjusting entry listed above, discuss an example adjusting entry that a lighting retailer might

make.

Adjusting entries often bring accounts that are partially or fully on a cash basis to an accrual accounting basis.

Making an adjusting entry for accrued revenues may be recognizing revenues that have been earned, but not yet

114. What is revenue recognition?

REVENUE RECOGNITION

115. What are the criteria for revenue recognition?

CRITERIA FOR REVENUE RECOGNITION

As a general principle, under the accrual basis of accounting, the firm recognizes revenue when the transaction

meets both of the following conditions:

1. Completion of the earnings process. The seller has done all (or nearly all) that it has promised to do for the

2. Receipt of assets from the customer. The seller has received cash or some other asset that it can convert to

cash, for example, by collecting an account receivable.

116. How do sellers measure revenue?

REVENUE MEASUREMENT

The seller measures revenue as the amount of cash, or the cash-equivalent value of other assets, that it receives

117. How are expenses recognized and measured?

EXPENSE RECOGNITION AND MEASUREMENT

TIMING OF EXPENSE RECOGNITION

Assets provide future benefits, and expenses measure the consumption of those benefits. Timing of expense

recognition focuses on when the firm consumes the benefits. The critical question is, “When does the firm

consume the benefits of an asset?” That is, when does the asset leave the balance sheet and become an expense

on the income statement?

1. The consumption of the asset results from a transaction that leads to the recognition of revenue. The

consumption of the benefit embodied in the asset is an expense in the period when the firm recognizes revenue.

2. The consumption of the asset results from the passage of time. When the firm consumes the benefits of an

asset over time, that cost becomes an expense of the period when the firm consumes the benefits. For example,

118. How do Merchandising and Manufacturing firms report product costs and changes in Inventory?

RECOGNITION OF PRODUCT COSTS

A seller of goods can easily associate (or match) the consumption of the benefits of the asset sold with revenues

from its sale. Specifically, at the time of sale and revenue recognition, the asset (inventory) leaves the seller’s

acquisition cost. When the firm sells the items, it recognizes the cost of the inventory as an expense (cost of

goods sold) on the income statement.

Manufacturing Firms and Inventory

A manufacturing firm incurs costs as it produces goods by changing the physical form of raw materials. For a

manufacturing firm, product costs are the costs incurred in manufacturing goods for sale. The costs to produce

119. How are period expenses recognized and measured?

RECOGNITION OF PERIOD EXPENSES

Many expenditures benefit specific accounting periods and do not benefit specific revenue transactions. The

firm therefore cannot link the timing of recognition of the expenses associated with these expenditures to

revenue recognition from specific sales. A common example of a period expense is the cost of management,

EXPENSE MEASUREMENT

120. What is comprehensive income?

COMPREHENSIVE INCOME

Net income under U.S. GAAP, or profit under IFRS, reports increases in net assets from certain transactions

repurchases).

The items reported in other comprehensive income relate to changes in the amount of

assets and liabilities resulting from transactions with nonowners—transactions whose effects

authoritative guidance has chosen to exclude from net income. Both U.S. GAAP and IFRS

Both U.S. GAAP and IFRS require the presentation of an income statement and the presentation of the items of

Other Comprehensive Income. U.S. GAAP permits three reporting formats. Starting January 1, 2009, IFRS

permits free choice between the first two reporting formats.

1. A single statement of comprehensive income that shows all the changes in net assets except from transactions

with owners;

2. A two-statement presentation that includes an income statement and a separate statement of comprehensive

income.

3. A separate display of the items comprising Other Comprehensive Income within a statement of changes in

shareholders’ equity. Firms applying U.S. GAAP use this alternative more often than the other two.

121. What are common-size income statements?