Solutions 1-18

Selling and Administrative Expenses ………….. (4,973) (4,355) (3,921)

1-19 Solutions

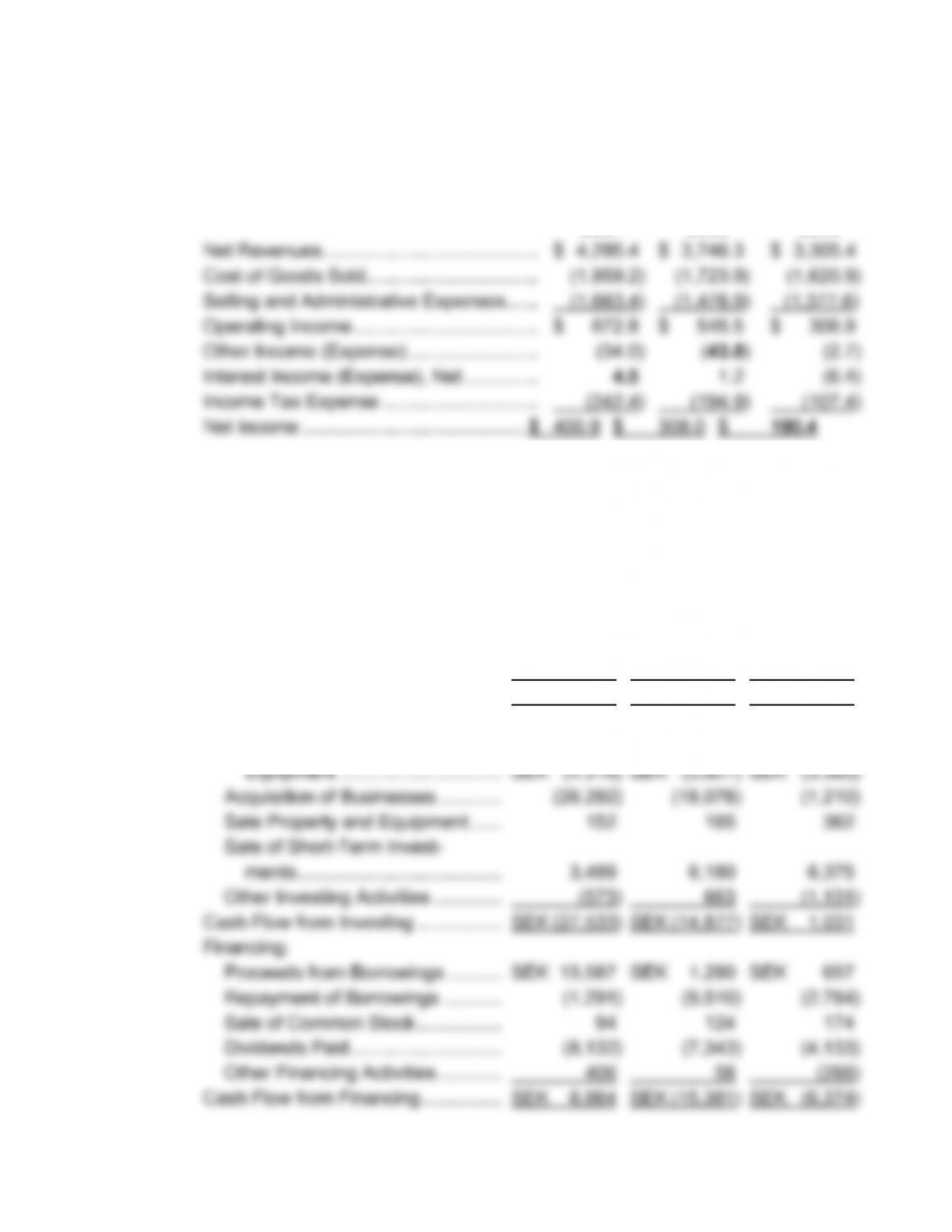

1.36 (Polo Ralph Lauren; income statement relations.) (Amounts in Millions)

The missing items appear in boldface type below.

2007 2006 2005

1.37 (Ericsson; statement of cash flows relations.)

ERICSSON

Statement of Cash Flows

(Amounts in SEK Millions)

2007 2006 2005

Operations:

Revenues, Net of Expenses …….. SEK 19,210 SEK 18,489 SEK 16,669

Cash Flow from Operations …………. SEK 19,210 SEK 18,489 SEK 16,669

Investing:

Acquisition of Property and

Solutions 1-20

1-21 Solutions

1.38 (Jackson Corporation; statement of cash flows relations.)

JACKSON CORPORATION

Statement of Cash Flows

(Amounts in Millions)

2008 2007 2006

Proceeds of Long-Term Borrow-

ing ……………………………………… $ 836 $ 5,096 $ 3,190

Issue of Common Stock ……………. 67 37 3

1.39 (JetAway Airlines; preparing a balance sheet and an income statement.)

a. JETAWAY AIRLINES

Balance Sheet

(Amounts in Thousands)

Sept. 30, Sept. 30,

2008 2007

Assets

Solutions 1-22

Other Current Assets …………………………….. 56,810 73,586

1-23 Solutions

1.39 a. continued.

Liabilities and Shareholders’ Equity

Accounts Payable …………………………..…….. $ 157,415 $ 156,755

Current Maturities of Long-Term Debt………. 11,996 7,873

b. JETAWAY AIRLINES

Income Statement

(Amounts in Thousands)

For the Year Ended: Sept. 30,

2008

Sales ……………………………………………………………………… $ 4,735,587

1.40 (Block’s Tax and Bookkeeping Services; cash versus accrual basis

accounting.)

a. Income for July, 2008:

Solutions 1-24

(1) Cash Basis Accounting

Sales Revenues ……………………………………………………… $ 13,000

1-25 Solutions

1.40 a. continued.

(2) Accrual Basis Accounting

Sales Revenues ……………………………………………………… $ 44,000

Rent (Office) …………………………………………………………… (2,000)

b. Cash on Hand:

Beginning Balance, July 1 …………………………………………… $ 0

The ending balance in cash contains the effects of both operating

1.41 (Stationery Plus; cash basis versus accrual basis accounting.)

a. Income for November, 2008:

(1) Cash Basis Accounting

Sales …………………………………………………………………….. $ 23,000

Solutions 1-26

Cost of Merchandise ……………………………………………….. (20,000)

1-27 Solutions

1.41 a. continued.

(2) Accrual Basis Accounting

Sales …………………………………………………………………….. $ 56,000

b. Income for December, 2008:

(1) Cash Basis Accounting

Sales Made in November, Collected in December ……….. $ 33,000

(2) Accrual Basis Accounting

Sales …………………………………………………………………….. $ 62,000

Cost of Merchandise ……………………………………………….. (33,600)

1.42 (ABC Company; relation between net income and cash flows.)

a.

Solutions 1-28

Cash

Balance at

Beginning

of Month

+

Cash

Receipts

from

Customers

–=

Cash

Disbursements

for Production

Costs

Cash

Balance

at End of

the MonthMonth

January $ 875 $ 1,000 $ 750 $ 1,125

1-29 Solutions

1.42 continued.

b. The cash flow problem arises because of a lag between cash

expenditures incurred in producing goods and cash collections from

customers once the firm sells those goods. For example, cash

c. The income statement and statement of cash flows provide information

about the profitability and liquidity, respectively, of a firm during a period.

d. Strategies for dealing with the cash flow problem center around (a)

reducing the lag between cash outflows to produce widgets and cash

Solutions 1-30

1-31 Solutions

1.42 d. continued.

(1) Delay paying its suppliers (increases accounts payable) or borrow from

(2) Substitute more efficient manufacturing equipment for work now

done by employees.

(3) Increase selling prices.

1.43 (Balance sheet and income statement relations.)

a. Bushels of wheat are the most convenient in this case with the given

Solutions 1-32

1.43 continued.

b. IVAN AND IGOR

Comparative Balance Sheets

(Amounts in Bushels of Wheat)

IVAN IGOR

Beginning End of Beginning End of

Assets

of Period Period of Period Period

Wheat …………………… 20 223 10 105

Accounts Payable ….. — 3 — —

Questions will likely arise as to the accounting entity. One view is that

there are two accounting entities (Ivan and Igor) to whom the Red

Bearded Baron has entrusted assets and required a periodic reporting on

1-33 Solutions

1.43 continued.

c. IVAN AND IGOR

Comparative Income Statement

(Amounts in Bushels of Wheat)

IVAN IGOR

Revenues ……………………………………………………. 243 138

Expenses:

Seed ………………………………………………………. 20 10

d. (Amounts in Bushels of Wheat) IVAN IGOR

Owner’s Equity, Beginning of Period …………………… 162 101

e. We cannot simply compare the amounts of net income for Ivan and Igor

because the Red Bearded Baron entrusted them with different amounts

Solutions 1-34