Archives: Solution Manual

978-0134065823 Chapter 22 Solution Manual Part 1

22-1 Chapter 22 Audit of the Capital Acquisition and Repayment Cycle Concept Checks P. 720 1. The characteristics of the liability accounts in the capital acquisition and repayment cycle that result in a different auditing approach than the approach […]

978-0134065823 Chapter 21 Solution Manual Part 3

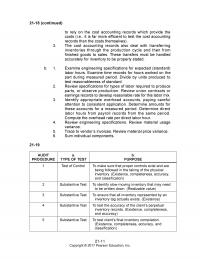

21–25 (continued) CLIENT a. ISSUES TO CONSIDER b. LOCATIONS TO VISIT c. POTENTIAL RISKS OF MATERIAL MISSTATEMENT d. AUDITOR RESPONSES TO RISKS 4. Food Giant Three–fourths of the inventory balance is located at the five independent storage warehouses. There is […]

978-0134065823 Chapter 21 Solution Manual Part 2

21–11 21–18 (continued) to rely on the cost accounting records which provide the costs (i.e., it is far more efficient to test the cost accounting records than the costs themselves). 3. The cost accounting records also deal with transferring inventories […]

978-0134065823 Chapter 21 Solution Manual Part 1

21-1 Chapter 21 Audit of the Inventory and Warehousing Cycle Concept Checks P. 694 1. Inventory is often the most difficult and time consuming part of many audit engagements because: 1. Inventory is generally a major item on the […]

978-0134065823 Chapter 20 Solution Manual Part 2

20–24 A flowchart of steps for each type of test is given below (requirements a., b., and c.): TESTS OF CONTROLS OR SUBSTANTIVE TESTS OF TRANSACTIONS TESTS OF DETAILS OF BALANCES 5 4 2 7 9 8 6 3 1 […]

978-0134065823 Chapter 20 Solution Manual Part 1

20-1 Chapter 20 Audit of the Payroll and Personnel Cycle Concept Checks P. 666 1. Transactions for the payroll and personnel cycle are generally far more significant than for payroll–related balance sheet accounts because entities pay payroll related expenses […]

978-0134065823 Chapter 2 Solution Manual

2-1 Chapter 2 The CPA Profession Concept Checks P. 28 1. The four major services that CPAs provide are: a. Audit and assurance services Assurance services are independent professional services that improve the quality of information for decision makers. […]

978-0134065823 Chapter 19 Solution Manual Part 3

19–17 19–27 (continued) 4. The paving and fencing are land improvements and should be depreciated over their useful lives. Land improvements (may be $50,000 combined with buildings account — buildings and improvements) Land $50,000 To correct initial recording of paving […]

978-0134065823 Chapter 19 Solution Manual Part 2

19–11 19–25 a. Both U.S. GAAP and IFRS standards generally contain similar requirements for assessing the impairment of assets, including goodwill. Both standards require the testing of goodwill for impairment at least annually, or more frequently if there are indications […]

978-0134065823 Chapter 19 Solution Manual Part 1

19-1 Chapter 19 Completing the Tests in the Acquisition and Payment Cycle: Verification of Selected Accounts Concept Checks P. 645 1. The reason for the emphasis on current period acquisitions in auditing property, plant, and equipment is that there […]

978-0134065823 Chapter 18 Solution Manual Part 4

Copyright © 2017 Pearson Education, Inc. 18–28 (continued) a. BERGERON INTERNAL CONTROLS b. TRANSACTION– RELATED AUDIT OBJECTIVE(S) c. TEST OF CONTROLS 11. Controller reconciles on a monthly basis the accounts payable listing to the accounts payable general ledger account. Controller […]

978-0134065823 Chapter 18 Solution Manual Part 3

Copyright © 2017 Pearson Education, Inc. 18–24 (continued) MISSTATEMENT a. TRANSACTION– RELATED AUDIT OBJECTIVE NOT MET b. PREVENTIVE CONTROL c. SUBSTANTIVE PROCEDURE 4 Acquisition transactions are properly classified (classification). Account distributions are reviewed by a responsible individual prior to entry […]

978-0134065823 Chapter 18 Solution Manual Part 2

Copyright © 2017 Pearson Education, Inc. 18–20 AUDIT PROCEDURE a. TYPE OF EVIDENCE b. TRANSACTION AUDIT OBJECTIVE c. TEST OF CONTROL OR SUBSTANTIVE TEST OF TRANSACTION 1.a. Inspection Recorded acquisitions and payments are for goods and services received, consistent with […]

978-0134065823 Chapter 18 Solution Manual Part 1

18-1 Chapter 18 Audit of the Acquisition and Payment Cycle: Tests of Controls, Substantive Tests of Transactions, and Accounts Payable Concept Checks P. 616 1. There are several balance sheet and income statement accounts related to the acquisition and […]

978-0134065823 Chapter 17 Solution Manual Part 3

17–31 (continued) b. Determination of ARIA – Note that there are many ways to estimate ARIA. One method is as follows: ARIA = AAR / (IR x CR x APR) = .05 / [1.0 x .8 x (1 – .6)] […]

978-0134065823 Chapter 17 Solution Manual Part 2

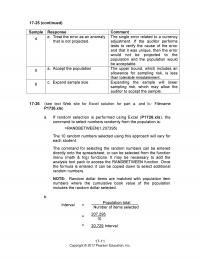

17–11 17–25 (continued) Sample Response Comment 4 e. Treat the error as an anomaly that is not projected. The single error related to a currency adjustment. If the auditor performs tests to verify the cause of the error and that […]

978-0134065823 Chapter 17 Solution Manual Part 1

17-1 Chapter 17 Audit Sampling for Tests of Details of Balances Concept Checks P. 575 1. The steps in nonstatistical sampling for tests of details of balances and for tests of controls are almost identical, as illustrated in the […]

978-0134065823 Chapter 16 Solution Manual Part 4

16–28 16–36 (continued) c. The auditor would likely deem that the risks of material misstatement related to all of the transaction–related audit objective for sales and cash receipts transactions as significant risks due to the deficiencies in internal control and […]

978-0134065823 Chapter 16 Solution Manual Part 3

16–21 16–30 (continued) d. When no response is received to the second request for positive confirmation, the auditor should use alternative procedures. These normally include examination of the customer’s remittance advice and related cash receipt. This is often a simple […]

978-0134065823 Chapter 16 Solution Manual Part 2

16–11 16–17 (continued) of controls based upon the selection of the significant controls. The auditor would then perform the tests of the significant controls to determine the effectiveness ofthe controls and to plan the substantive tests that are necessary based […]

978-0134065823 Chapter 16 Solution Manual Part 1

16-1 Chapter 16 Completing the Tests in the Sales and Collection Cycle: Accounts Receivable Concept Checks P. 537 1. Auditors perform substantive analytical procedures for the entire sales and collection cycle, including accounts receivable. This is necessary because of […]

978-0134065823 Chapter 15 Solution Manual Part 3

15-20 15–34 (continued) INVOICE NUMBER EXCEPTION ANALYSIS 6810 Confirm the account balances to the customers; examine the reduction in the perpetual inventory records. 7625 Trace the amount to the sales journal and accounts receivable master file; examine the shipping document […]

978-0134065823 Chapter 15 Solution Manual Part 2

15-11 15–28 (continued) 2. Test time delay between warehouse removal slip date and billing date for timeliness of billing. (Timing) 3. Trace entries into perpetual inventory records to determine that inventory is properly relieved for shipments. (Posting and summarization) e. […]

978-0134065823 Chapter 15 Solution Manual Part 1

15-1 Chapter 15 Audit Sampling for Tests of Controls and Substantive Tests of Transactions Concept Checks P. 489 1. A representative sample is one in which the characteristics of interest for the sample are approximately the same as for […]

978-0134065823 Chapter 14 Solution Manual Part 4

14–30 14–34 (continued) d. TRANSACTION– RELATED AUDIT OBJECTIVE SUBSTANTIVE TEST OF TRANSACTIONS AUDIT PROCEDURES 1. Recorded sales occurred. Select a sample of sales from sales journal and examine customer’s purchase order, sales order form, and bill of lading to determine […]

978-0134065823 Chapter 14 Solution Manual Part 3

14–21 14–30 POSSIBLE ERROR OR FRAUD CONTROL 1. Customer checks are properly credited to customer accounts and are properly deposited, but errors are made in recording receipts in the cash receipts journal. g. An employee, other than the bookkeeper, periodically […]

978-0134065823 Chapter 14 Solution Manual Part 2

14–11 14–23 (continued) 4. a. Online sales are recorded in the sales system (Completeness). b. Review online sales system documentation and make inquiries of client personnel to determine that the automatic interface is a part of the system design. Enter […]

978-0134065823 Chapter 14 Solution Manual Part 1

14-1 Chapter 14 Audit of the Sales and Collection Cycle: Tests of Controls and Substantive Tests of Transactions Concept Checks P. 452 1. a. The customer order is a request from the customer indicating the quantity and the description […]

978-0134065823 Chapter 13 Solution Manual Part 3

13–17 13–32 (continued) Parts 7, 9, and 1 are all a part of planning and are therefore done early. These are in the sequence shown in Chapter 8. As part of planning the audit, the auditor obtains an understanding of […]

978-0134065823 Chapter 13 Solution Manual Part 2

Copyright © 2017 Pearson Education, Inc. 13–26 a. TRANSACTION–RELATED AUDIT OBJECTIVE b. TEST OF CONTROL PROCEDURE c. SUBSTANTIVE TEST 1. Recorded transactions exist, recorded transactions are stated at the correct amounts, and transactions are properly classified. (Occurrence, Accuracy, and Classification) […]

978-0134065823 Chapter 13 Solution Manual Part 1

13-1 Chapter 13 Overall Audit Strategy and Audit Program Concept Checks P. 419 1. The five types of tests auditors use to determine whether financial statements are fairly stated include the following: Risk assessment procedures Tests of […]

978-0134065823 Chapter 12 Solution Manual Part 4

12-31 12–35 (continued) Establish standardized programming procedures and have Melinda review changed programs for compliance with those procedures. Melinda should reconcile the Job Processed Log to the job schedule developed by her.Melinda should assign or at least approve […]

978-0134065823 Chapter 12 Solution Manual Part 3

12-21 12–28 (continued) 4. Access the client’s electronic inventory master file and list all items or parts of which the quantity on hand seems excessive in relation to quantity used or sold during the year. This list provides data for […]

978-0134065823 Chapter 12 Solution Manual Part 2

12-11 12–21 (continued) system. She must obtain an understanding of internal control to determine whether it is possible to conduct an audit at all. Auditing standards require, at a minimum, an understanding of internal control. The auditor must understand the […]

978-0134065823 Chapter 12 Solution Manual Part 1

12-1 Chapter 12 Assessing Control Risk and Reporting on Internal Controls Concept Checks P. 381 1. As illustrated by Figure 12–1, there are four phases in the process of understanding internal control and assessing control risk. In the first phase […]

978-0134065823 Chapter 11 Solution Manual Part 2

11–11 Copyright © 2017 Pearson Education, Inc. 11–25 1. a. Adequate documents and records, and independent checks on performance. b. Transactions are recorded on the correct dates (cutoff). c. Carefully coordinate the physical count of inventory on the 2. a. […]

978-0134065823 Chapter 11 Solution Manual Part 1

11-1 Chapter 11 Internal Control and COSO Framework Concept Checks P. 339 1. Management typically has three broad objectives in designing effective internal controls. 1. Reliability of Reporting While this objective relates to both external and internal reporting, we […]

978-0134065823 Chapter 10 Solution Manual Part 3

10–21 10-34 (continued) 7. a. Sales may be fictitiously recorded before any goods were shipped. b. Sales and accounts receivable. c. Recorded amounts meet the criteria for revenue recognition (occurrence). 8. a. Fictitious sales transactions may have been entered to […]

978-0134065823 Chapter 10 Solution Manual Part 2

10–11 10-26 (continued) whether an audit performed in accordance with auditing standards should have uncovered the fraud. The auditor is not required to search for immaterial fraudulent transactions; however, the auditor is required to follow up when one is discovered. […]

978-0134065823 Chapter 10 Solution Manual Part 1

10-1 Chapter 10 Assessing and Responding to Fraud Risks Concept Checks P. 311 1. The three conditions of fraud referred to as the “fraud triangle” are (1) Incentives/Pressures; (2) Opportunities; and (3) Attitudes/Rationalization. Incentives/Pressures are incentives of management or […]

978-0134065823 Chapter 1 Solution Manual Part 2

1-8 1-17 a. The services provided by Consumers Union are very similar to assurance services provided by CPA firms. The services provided by Consumers Union and assurance services provided by CPA firms are designed to improve the quality of information […]

978-0134065823 Chapter 1 Solution Manual Part 1

Copyright © 2017 Pearson Education, Inc. Chapter 1 The Demand for Audit and Other Assurance Services Concept Checks P. 8 1. To do an audit, there must be information in a verifiable form and some standards (criteria) by which […]

978-0134004006 Chapter 9 Lecture Note

79 “The movement of the progressive societies has hitherto been a movement from status to contract.” Sir Henry Maine I. Teacher to Teacher Dialogue What elevates a mere agreement between two or more private parties into a legally recognized contract […]

978-0134004006 Chapter 9 Case

1 Chapter 9 Nature of Traditional and E-Contracts VI. Answers to Critical Legal Thinking Cases 9.1 Implied-in-Fact Contract Yes. There was an implied-in–fact contract between the parties. The law allows for recovery of damages for the breach of an implied-in-fact […]

978-0134004006 Chapter 8 Lecture Note Part 2

Criminal Law and Cyber Crimes 73 The Fifth Amendment provides that no person can be compelled in any criminal case to give evidence against him/herself. We speak of those asserting this privilege as pleading or taking the Fifth. Only individuals […]

978-0134004006 Chapter 8 Lecture Note Part 1

Chapter 8 66 In our complex society the accountant’s certificate and the lawyer’s opinion can be instruments for inflicting pecuniary loss more potent than the chisel or the crowbar. Justice Blackmun I. Teacher to Teacher Dialogue There can be no […]

978-0134004006 Chapter 8 Case

1 Chapter 8 Criminal Law and Cybercrime VI. Answers to Critical Legal Thinking Cases 8.1 Search and Seizure No. The police officers’ use of the global positioning system (GPS) without first obtaining a search warrant does not constitute an unreasonable […]

978-0134004006 Chapter 7 Lecture Note

Chapter 7 56 The Congress shall have the power…to promote the Progress of Science and useful Arts, by securing for limited Times to Authors and Inventors the exclusive Right to their respective Writings and Discoveries. Article I, Section 8, clause […]

978-0134004006 Chapter 7 Case

1 Chapter 7 Intellectual Property and Cyber Piracy VI. Answers to Critical Legal Thinking Cases 7.1 Patent No, the claimed invention is not patentable. In order to be patentable, the claimed invention must be novel and nonobvious. Laws of nature, […]

978-0134004006 Chapter 6 Lecture Note

Strict Liability and Product Liability 49 A manufacturer is strictly liable in tort when an article he places on the market, knowing that it is to be used without inspection for defects, proves to have a defect that causes injury […]