Archives: Solution Manual

978-0137024971 Chapter 9 Part 6

–– 350 Exhibit TN-1: The Relevant Organizational Structure Frits Seegers President Citibank California Frits Seegers President Citibank California James McGaran Branch manager Branch manager Other branch managers Other branch managers Financial District James McGaran Financial District Lisa Johnson Lisa Johnson […]

978-0137024971 Chapter 9 Part 5

Chapter 9: Behavioral and Organizational Issues in Management Accounting and Control Systems – 343 – Pedagogy This case illustrates the tensions that emerge when the performance measurement system is expanded to include measures beyond financial results. Strategy and structure Before […]

978-0137024971 Chapter 9 Part 4

Chapter 9: Behavioral and Organizational Issues in Management Accounting and Control Systems – 333 – (d) The top employees will likely stay since their income will increase. The weaker sales people will likely leave to find jobs where the income […]

978-0137024971 Chapter 9 Part 3

Chapter 9: Behavioral and Organizational Issues in Management Accounting and Control Systems – 323 – of information that should be generated from the system from those employees who work with a MACS on a routine basis (and in some cases […]

978-0137024971 Chapter 9 Part 2

– 313 – 9-51 Some management thinkers believe that the best type of organizational culture is one in which pay for performance is unnecessary. In this view, people will perform well if the owners pay the people a good salary. […]

978-0137024971 Chapter 9 Part 1

Chapter 9: Behavioral and Organizational Issues in Management Accounting and Control Systems – 303 – Chapter 9 Behavioral and Organizational Issues in Management Accounting and Control Systems QUESTIONS 9-1 In the context of a management accounting and control system, control […]

978-0137024971 Chapter 8 Part 4

Chapter 8: Measuring Life-Cycle Costs – 323 – (b) How has MB reacted to the changing world market for luxury automobiles? from traditional strategies at Mercedes: • many new product introductions; • partnering with suppliers; • reduced parts and system […]

978-0137024971 Chapter 8 Part 3

Chapter 8: Measuring Life-Cycle Costs – 317 – Stage 4 for different members of the class and then have them compare the plans that they devise. For instance, in Stage 3 you might ask some students to devise a plan […]

978-0137024971 Chapter 8 Part 2

Chapter 8: Measuring Life-Cycle Costs – 307 – 8-33 As shown below, Greyson will now never reach a break-even time. Beginning with Y4, Q4, Greyson will incur quarterly losses of $20,000 and will never show a positive cumulative profit. (000) […]

978-0137024971 Chapter 8 Part 1

– 297 – Chapter 8 Measuring Life-Cycle Costs QUESTIONS 8-1 The total–life-cycle costing approach is a comprehensive way for managers to understand and manage costs through a product’s design, development, manufacturing, marketing, distribution, maintenance, service, and disposal 8-2 The three […]

978-0137024971 Chapter 7 Part 4

Chapter 7: Measuring and Managing Process Performance – 237 – (c) Items 1, 2, 5, 8, 10, and 12 are internal failures; the remainder are external failure items. Internal customers affected by external failure items are listed below. Item Number […]

978-0137024971 Chapter 7 Part 3

Chapter 7: Measuring and Managing Process Performance – 227 – Using an experienced coordinator Training employees Stage 3: Identifying benchmarking partners Size of partners Stage 4: Information gathering and sharing methods Type of benchmarking […]

978-0137024971 Chapter 7 Part 2

Chapter 7: Measuring and Managing Process Performance – 217 – 7-39 (a) The article reports that customer service representatives are commonly evaluated on time to complete a call or whether they sell a new product to the customer. The article […]

978-0137024971 Chapter 7 Part 1

– 207 – Chapter 7 Measuring and Managing Process Performance QUESTIONS 7-1 The throughput contribution is the difference between revenues and direct materials for the quantity of product sold. Investments equal the materials 7-2 In process layouts, all similar equipment […]

978-0137024971 Chapter 6 Part 4

Atkinson, Solution Manual t/a Management Accounting, 6E – 126 – discussed in Chapter 5 and the Kaplan-Anderson HBR article, as an easy and effective tool for handling order complexity. TN Exhibit 6-2 shows a slide that incorporate far more process […]

978-0137024971 Chapter 6 Part 3

Chapter 6: Measuring and Managing Customer Relationships – 117 – retain Customer 4 in years 1 and 2 provides net benefits and helps (c) Assuming that n is very large and the numbers in the table remain about the same […]

978-0137024971 Chapter 6 Part 2

Chapter 6: Measuring and Managing Customer Relationships – 107 – 6-22 (a) If Saunders reduced its sales discounts so that net revenues increased by 10%, the net revenue would increase to $220,000 and operating With 10% Initial Revenue Increase Net […]

978-0137024971 Chapter 6 Part 1

– 97 – Chapter 6 Measuring and Managing Customer Relationships QUESTIONS 6-1 Nonfinancial measures such as customer satisfaction and customer loyalty are important in managing relationships with customers, but an excessive focus on improving customer performance with only these metrics […]

978-0137024971 Chapter 5 Part 6

Chapter 4: Activity-Based Cost Systems – 147 – level. Total gross margin increases by almost 81% and operating profit increases more than ten-fold. The huge profit increase assumes only a A comparison of product line profitability before and after the […]

978-0137024971 Chapter 5 Part 5

Chapter 5: Activity-Based Cost Systems –137– cost rates? (b) Capacity Cost Rates Cost/ Days Used Paid Hrs Nonprod. Prod. Prod. Cost Month Per Month Per Day Hours Hrs/Day Hrs/Mo Per Hr Production and Setup Labor $3,900 20 7.5 1.5 6.0 […]

978-0137024971 Chapter 5 Part 4

Chapter 5: Activity-Based Cost Systems –127– retailer to develop a retailer profitability model for the cola beverage category (one of the highest gross volume categories in a retail grocery store). From the retailer’s perspective, profit would be measured by the […]

978-0137024971 Chapter 5 Part 3

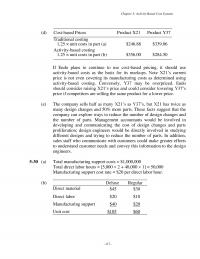

Chapter 5: Activity-Based Cost Systems –117– (d) Cost-based Prices Product X21 Product Y37 Traditional costing 1.25 × unit costs in part (a) $246.88 $339.06 Activity-based costing 1.25 × unit costs in part (b) $356.00 $284.50 If Endo plans to continue […]

978-0137024971 Chapter 5 Part 2

Chapter 5: Activity-Based Cost Systems –107– Labor Vanilla Chocolate Straw- berry Mocha- Almond Total Number of production runs 18 16 4 3 Handle production run (hours/run) 2.5 2.5 2.5 2.5 Indirect labor: handle runs 45.0 40.0 10.0 7.5 102.5 Setup […]

978-0137024971 Chapter 5 Part 1

–97– Chapter 5 Activity-Based Cost Systems QUESTIONS 5-1 Traditional volume-based cost allocation systems that use only drivers that vary directly with the volume of products produced—such as direct labor dollars, direct labor hours, or machine hours—are likely to systematically distort […]

978-0137024971 Chapter 4 Part 4

Atkinson, Solutions Manual t/a Management Accounting, 6E Direct labor and material costs $32.000 Overhead costs: Casting (1 $10.833) $10.833 Assembly (0.5 $9.889) 4.944 15.777 Unit cost $47.777 Number of units per month 1,000.000 Total manufacturing costs per month […]

978-0137024971 Chapter 4 Part 3

Atkinson, Solutions Manual t/a Management Accounting, 6E – 122 – 4-46 (a) Mixing and Reaction Pulverizing Blending Chambers and Packing Total conversion costs $424,600 $1,551,000 $559,900 Total number of process hours 8,760 35,040 8,760 Conversion cost per process hour $48.470 […]

978-0137024971 Chapter 4 Part 2

Atkinson, Solutions Manual t/a Management Accounting, 6E – 112 – 4-37 Service Departments Production Departments S1 S2 P1 P2 Overhead costs $65,000 $55,000 $160,000 $240,000 Allocation of S1 costs (65,000) 15,000 20,000 30,000 Allocation of S2 costs — (70,000) 33,600 […]

978-0137024971 Chapter 4 Part 1

Atkinson, Solutions Manual t/a Management Accounting, 6E – 102 – Chapter 4 Accumulating and Assigning Costs to Products QUESTIONS 4-1 The cost of the raw materials entered into production is moved from the raw materials account to the work–in-process inventory […]

978-0137024971 Chapter 3 Part 5

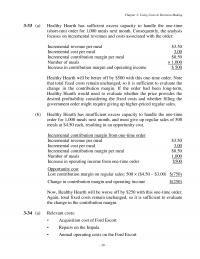

Chapter 3: Using Costs in Decision Making – 69 – The campaign was less than successful; the company announced that it had “overreached.” Nordstrom had “alienated its faithful clientele” [7] by (d). Nordstrom may need to reconsider its value proposition. […]

978-0137024971 Chapter 3 Part 4

Chapter 3: Using Costs in Decision Making – 59 – 3-65 (a) XLl XL2 XL3 Sales price $10.00 $14.00 $12.00 Direct materials (4.00) (4.50) (5.00) Direct labor (2.00) (3.00) (2.50) Variable overhead (2.00) (3.00) (2.50) Unit contribution margin $2.00 $3.50 […]

978-0137024971 Chapter 3 Part 3

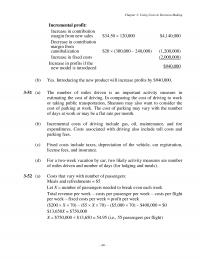

Chapter 3: Using Costs in Decision Making – 49 – Incremental profit: Increase in contribution margin from new sales $34.50 120,000 $4,140,000 Decrease in contribution margin from cannibalization $20 (300,000 – 240,000) (1,200,000) Increase in fixed costs (2,000,000) […]

978-0137024971 Chapter 3 Part 2

Chapter 3: Using Costs in Decision Making – 39 – Incremental revenue per meal $3.50 Incremental cost per meal 3.00 Incremental contribution margin per meal $0.50 Number of meals × 1,000 Increase in contribution margin and operating income $ 500 […]

978-0137024971 Chapter 3 Part 1

– 29 – Chapter 3 Using Costs in Decision Making QUESTIONS 3-1 Cost information is used in pricing, product planning, budgeting, performance evaluation, and contracting. Examples of specific uses of cost information 3-2 Variable costs are costs that increase proportionally […]

978-0137024971 Chapter 2 Part 4

Chapter2: The Balanced Scorecard and Strategy Map –47– Suggestions for Classroom Use A productive way to begin the class discussion is to focus for a few minutes on why financial measures are not sufficient to direct managers’ attention to what […]

978-0137024971 Chapter 2 Part 3

Chapter2: The Balanced Scorecard and Strategy Map –41– areas development City of Charlotte Balanced Scorecard Perspective Customer Reduce crime Strengthen neighbor- hoods Provide safe, convenient transportation choices Safeguard the environment Promote economic opportunity Increase perception of safety Financial Expand tax […]

978-0137024971 Chapter 2 Part 2

Chapter2: The Balanced Scorecard and Strategy Map –31– This KPI scorecard has no role for information technology (strange for a financial service organization), no linkages from its process measure (quality certification) to a customer value proposition or to a customer […]

978-0137024971 Chapter 2 Part 1

Chapter2: The Balanced Scorecard and Strategy Map –21– Chapter 2 The Balanced Scorecard and Strategy Map QUESTIONS 2-1 Financial performance measures, such as operating income and return on investment, indicate whether the company’s strategy and its implementation profitability. Key nonfinancial […]

978-0137024971 Chapter 11 Part 3

Chapter 12: Financial Control – 453 – same while the investment level will be $80,000,000 in year 2, $70,000,000 in year 3, $60,000,000 in year 4, and $50,000,000 in year 5. Therefore, the manager’s attitude about this investment will reflect […]

978-0137024971 Chapter 11 Part 2

Atkinson, Solutions Manual t/a Management Accounting, 6E – 444 – increase in return on investment Return on investment = (return on sales) (investment turnover). 1.1 × 1.6 = [(1 + x) × 0.8] × (2.0 × 0.8) x = […]

978-0137024971 Chapter 11 Part 1

Atkinson, Solutions Manual t/a Management Accounting, 6E – 434 – Chapter 11 Financial Control QUESTIONS 11-1 Financial control is the formal evaluation of some financial facet of an organization or a responsibility center to assess organization and management performance. Financial […]

978-0137024971 Chapter 10 Part 8

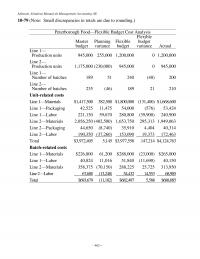

Atkinson, Solutions Manual t/a Management Accounting, 6E – 462 – 10–79 (Note: Small discrepancies in totals are due to rounding.) Peterborough Food—Flexible Budget Cost Analysis Master budget Planning variance Flexible budget Flexible budget variance Actual Line 1— Production units 945,000 […]

978-0137024971 Chapter 10 Part 7

Chapter 10: Using Budgets for Planning and Coordination – 453 – (c) Increased sales effort Oct. Nov. Dec. Jan. Feb. Mar. Apr. May Unit production and sales – Chairs 900 975 950 1,326 1,548 1,533 1,554 1,560 – Tables 175 […]

978-0137024971 Chapter 10 Part 6

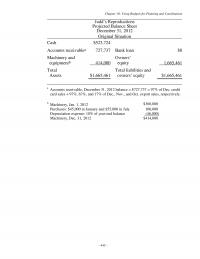

Chapter 10: Using Budgets for Planning and Coordination Judd’s Reproductions Projected Balance Sheet December 31, 2012 Original Situation Cash $523,724 Accounts receivablea 727,737 Bank loan $0 Machinery and equipmentb 414,000 Owners’ equity 1,665,461 Total Assets $1,665,461 Total liabilities and owners’ […]

978-0137024971 Chapter 10 Part 5

Chapter 10: Using Budgets for Planning and Coordination – 433 – (d) The above analysis relies on cost estimates based on allocation of other manufacturing support, selling support, and general and administrative operations for Ace and Bell. 10–77 (a) Number […]

978-0137024971 Chapter 10 Part 4

Chapter 10: Using Budgets for Planning and Coordination (d) Direct material price variance = (AP – SP) × AQ = ($9.75 – 10) × 4,200 = $ – 0.25 × 4,200 = $1,050 Favorable (e) Direct material quantity variance = […]

978-0137024971 Chapter 10 Part 3

Chapter 10: Using Budgets for Planning and Coordination – 413 – Ending cash balance $112,000 10–60 (a) With 2,000,000 medical claims Shadyside Insurance Company should employ 13.33 = ((2,000,000/150,000) 1) supervisors, 26.67 = ((2,000,000/150,000) 2) senior clerks, and […]

978-0137024971 Chapter 10 Part 2

Chapter 10: Using Budgets for Planning and Coordination (b) Material quantity variance = AQ SQ SP F 40 000 59,000 000 ,$100 $500, (c) Yes, the relationship with […]

978-0137024971 Chapter 10 Part 1

– 393 – Chapter 10 Using Budgets to for Planning and Coordination QUESTIONS 10-1 A budget is a quantitative model of the expected consequences of the 10-2 Flexible resources are those that vary with the activity level of the firm […]

978-0137024971 Chapter 1 Part 2

Chapter 1: How Management Accounting: Information Supports Decision Making – 11 – required to perform each procedure—would be tracked, and delay time—the time between when the patient showed up for a procedure and the time when the procedure was actually […]

978-0137024971 Chapter 1 Part 1

– 1 – Chapter 1 How Management Accounting Information Supports Decision Making QUESTIONS 1-1 Management accounting is a discipline that designs planning and performance measurement systems, using financial and nonfinancial information, to help an cycle includes prospective data on costs, […]