Archives: Solution Manual

Accounting Chapter 14 Homework That different time periods may be appropriate for different budgets

CHAPTER 14 Cost Planning CHAPTER OUTLINE: I. Introduction A. Why Budgets are Useful B. Definition of Performance Reporting II. Cost Classifications A. Relationship of Cost to Volume of Activity 1. Variable cost 2. Fixed cost 3. Mixed cost B. According […]

Accounting Chapter 13 Homework Analysis The Work Process Inventory Account Working

Chapter 13 Cost Accounting and Reporting C13.30. (continued) d. EI 27,000 Solving for the missing amount, raw materials used = $252,000 Raw material purchases and usage will differ by the amount of change in the inventory of raw material. Materials […]

Accounting Chapter 13 Homework The activity based costing approach is likely to provide better information

© McGraw-Hill Education, 2017 13-11 E13.18. a. Total cost for 4,200 toy flutes produced: Raw materials …………………………………………………………… $490.00 Direct labor (21 direct labor hours)………………………………………. 357.00 Overhead applied based on machine hours (36 hours * $5.60)………….. 201.60 Overhead applied based on […]

Accounting Chapter 13 Homework Use several examples of different cost objects to illustrate that

CHAPTER 13 Cost Accounting and Reporting CHAPTER OUTLINE: I. Cost Management A. Value Chain Functions II. Cost Accumulation and Assignment A. Cost Objects B. Cost Pools C. Cost Assignment III. Cost Classifications A. Cost Relationship to Product or Activity 1. […]

Accounting Chapter 12 Homework Candy co Break Even b Calculate Operating Income 5300

12–37 Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. C12.33. (continued) e. To: Dominic From: Your Cost-Volume-Profit Analysis Person Subject: Analysis Results per pizza with the related cost […]

Accounting Chapter 12 Homework All tools are very simple to use and the discussion should

12–31 Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. C12.33. (continued) 4. The following solution screen is from the dinkytown.net site: b. and the presentation of the results. […]

Accounting Chapter 12 Homework Our Groups Business Should Not Cause The

12–21 Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. P12.25. (continued) c. Break-even point in sales dollars = Fixed expenses / Contribution margin ratio = $70,000 / 50% […]

Accounting Chapter 12 Homework Operating Income Changes Loss

12–11 Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. E12.13. a. Use the model, enter the known data, and solve for the unknown. Per Unit * Volume = […]

Accounting Chapter 12 Homework Sales Salary Sales Commission 500 2400 Units

12-1 CHAPTER 12 Managerial Accounting and Cost-Volume-Profit Relationships CHAPTER OUTLINE: I. Managerial Accounting Contrasted to Financial Accounting A. The Management Process 1. Variety of firm’s objectives 2. Planning and Control B. Differences Between Financial and Managerial Accounting 1. Future orientation […]

Accounting Chapter 11 Homework January 2017 Net Income For The Year

© McGraw-Hill Education, 2017 11-19 C11.16 (continued) d. expectations formed in part b. As expected, PepsiCo is more leveraged than is Coca Cola, but the debt ratio portrays the extent to which this is true more clearly than does the […]

Accounting Chapter 11 Homework Roi Relatively Low Although The Two year Trend

© McGraw-Hill Education, 2017 11-11 P11.11. e. By selling inventory for cash, Arch Company will improve its acid-test ratio to 1.7 because a current asset that is included in the acid-test numerator (Cash of $180,000) will replace a current asset […]

Accounting Chapter 11 Homework For examination purposes, emphasis should be placed on interpretation

CHAPTER 11 Financial Statement Analysis CHAPTER OUTLINE: I. Interpretation of Financial Condition and Results of Operations A. Liquidity Measures 1. Review of working capital, current ratio, and acid-test ratio B. Activity Measures 1. Turnover a. Significance and general model 2. […]

Accounting Chapter 10 Homework Eps Figure Has Already Been Restated The

CHAPTER 10 Corporate Governance, Notes to the Financial Statements, and Other Disclosures CHAPTER OUTLINE: I. Corporate Governance A. General background and perspective 1. Impact of stock market and corporate failures 2. Variety of reform measures B. Sarbanes-Oxley Act (SOX) of […]

Accounting Chapter 1 Homework Use Exercise 15 Generate Discussion About The

CHAPTER 1 Accounting—Present and Past CHAPTER OUTLINE: I. What Is Accounting? A. Definition B. Uses of Accounting Information C. Classifications 1. Financial Accounting 2. Managerial Accounting / Cost Accounting 3. Auditing — Public Accounting 4. Internal Auditing 5. Governmental and […]

978-1133188797 Solution Manual Gibson_Ch13_SM_13e Part 2

446 PROBLEM 13-8 a. City of Toledo Revenues – Business-Type Activities Charge for Services Vertical Common-Size Business-type activities: 2003 2004 2005 2006 2007 2008 2009 2010 Charges for services: Water 36.9 37.5 36.6 35.5 35.2 32.2 32.1 32.9 Sewer 40.0 […]

978-1133188797 Solution Manual Gibson_Ch13_SM_13e Part 1

436 Chapter 13 Personal Financial Statements and Accounting for Governments and Not-For-Profit Organizations QUESTIONS 13– 1. Personal financial statements may be prepared for an individual, a husband and wife, or a larger family group. 13– 3. No. 13– 4. No. […]

978-1133188797 Solution Manual Gibson_Ch12_SM_13e Part 3

426 b. Horizontal Common-Size For the Years Ended December 31 Total United States Europe Africa Asia and other 2010 Sales and other operating revenues Unaffiliated customers Inter-company Total revenues 100.0 100.0 100.0 26.9 100.0 28.1 26.2 —— 25.7 32.0 —— […]

978-1133188797 Solution Manual Gibson_Ch12_SM_13e Part 2

419 b. The operating ratio decreased, indicating improved efficiency. Funded debt to Percent earned to operating property increased, indicating improved profitability. Operating revenue to operating property increased slightly, indicating improved profitability. c. Cash flow per share has increased much more […]

978-1133188797 Solution Manual Gibson_Ch12_SM_13e Part 1

409 Chapter 12 Special Industries: Banks, Utilities, Oil and Gas, Transportation, Insurance, Real Estate Companies QUESTIONS 12– 1. Interest income, service charges, and earnings in investments are the main sources of revenue for banks. 12– 2. Loans are assets because […]

978-1133188797 Solution Manual Gibson_Ch11_SM_13e Part 6

400 CASE 11-5 BOOKS UNLIMITED (Part 2) (This case provides the opportunity to review Borders Group, Inc. per the 10-K for the fiscal year ended January 29, 2011.) This comment is included in Note 1: On February 16, 2011 (the […]

978-1133188797 Solution Manual Gibson_Ch11_SM_13e Part 5

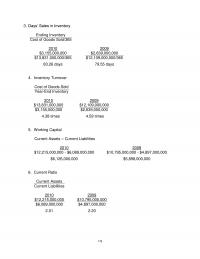

394 CASE 11-4 BOOKS UNLIMITED (Part 1) a. Liquidity Ratios 1. Days’ Sales in Inventory = Ending Inventory Cost of Goods Sold/365 2009 $915,200,000 = $915,200,000 = 134.44 days $2,484,800,000/365 $6,807,671 2008 $1,242,000,000 = $1,242,000,000 = 169.89 days $2,668,300,000/365 $7,310,410 […]

978-1133188797 Solution Manual Gibson_Ch11_SM_13e Part 4

384 c. No. Return on average assets before interest and taxes (third goal) is equal to return on sales before interest and taxes (first goal) times turnover of average assets (second goal). If Calcor Company achieved the first two goals, […]

978-1133188797 Solution Manual Gibson_Ch11_SM_13e Part 3

374 (15) Land, Buildings, and Equipment: Let: A = land, buildings, and equipment D = accumulated depreciation N = net fixes assets A – D = N A – [(A/3*)] = $195,000 x 2/3A = $195,000 A = $292,500 *From […]

978-1133188797 Solution Manual Gibson_Ch11_SM_13e Part 2

364 7. Acid-Test Ratio = Cash Equivalents + Marketable Securities + Accounts Receivable Current Liabilities $64,346 + $99,021 = 2.22 $73,730 8. Cash Ratio = Cash Equivalents + Marketable Securities Current Liabilities $64,346 = 0.87 $73,730 Debt: 1. Debt Ratio […]

978-1133188797 Solution Manual Gibson_Ch11_SM_13e Part 1

354 Chapter 11 Expanded Analysis QUESTIONS 11– 1. Based on the study reported in the text, liquidity and debt ratios are regarded 11– 2. (a) Debt/equity, current ratio (b) Debt/equity, current ratio 11– 3. The dividend payout ratio does not […]

978-1133188797 Solution Manual Gibson_Ch10_SM_13e Part 4

341 CASE 10-4 THE RETAIL MOVER a. 1. 2007 2008 2011 Total current assets $ 628,408,895 $ 719,478,441 $ 1,044,689,000 Total current liabilities 366,718,656 458,999,682 661,058,000 Working capital 261,690,239 260,478,759 383,631,000 Working capital was fairly constant between 2007 and 2008. […]

978-1133188797 Solution Manual Gibson_Ch10_SM_13e Part 3

PROBLEM 10-11 a. 1 Tightening of credit by suppliers could lead to cash flow problems. b. 5 For a profitable firm, a substantial decrease in receivables would not contribute to bankruptcy. c. 5 Change in notes payable to bands is […]

978-1133188797 Solution Manual Gibson_Ch10_SM_13e Part 2

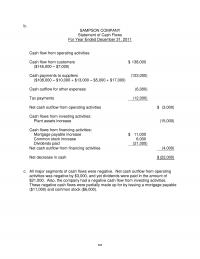

322 b. SAMPSON COMPANY Statement of Cash Flows For Year Ended December 31, 2011 Cash flow from operating activities: Cash flow from customers $ 138,000 ($145,000 – $7,000) Cash payments to suppliers (123,000) ($108,000 – $10,000 + $13,000 – $5,000 […]

978-1133188797 Solution Manual Gibson_Ch10_SM_13e Part 1

312 Chapter 10 Statement of Cash Flows QUESTIONS 10– 1. The basic justification for a statement of cash flows is that the balance sheet and the income statement do not adequately indicate changes in cash. obtained this way. The income […]

978-1133188797 Solution Manual Gibson_Ch09_SM_13e Part 3

297 Fiscal year ended October 3, 2009 statements – September 27, 2008 $5.78 Fiscal year ended October 2, 2010 statements – September 27, 2008 $5.80 c. September 7, 2008 1. October 2, 2010 statements September 27, 2008 88,454 2. October […]

978-1133188797 Solution Manual Gibson_Ch09_SM_13e Part 2

287 PROBLEM 9-9 a. Numerator Denominator Net income $ 200,000 Preferred dividends (10,000) Common shares outstanding on January 1 20,000 shares Common stock issue on July 1, 5,000 shares 2,500 (5,000 x ½) Weighted average 22,500 Two-for-one stock split on […]

978-1133188797 Solution Manual Gibson_Ch09_SM_13e Part 1

277 Chapter 9 For the Investor QUESTIONS stock during an accounting period. 9- 2. The Financial Accounting Standards Board suspended the reporting of earnings per share for nonpublic companies. 9- 3. Keller & Fink is a partnership. Earnings per share […]

978-1133188797 Solution Manual Gibson_Ch08_SM_13e Part 6

268 CASE 8-6 RETURN ON ASSETS – INDUSTRY COMPARISON Assets.) a. Johnson & Johnson 1. Net Profit Margin = Net Income Before Noncontrolling Interest Equity Income and Nonrecurring Items Net Sales $13,334 = 21.65% $61,587 2. Total Asset Turnover = […]

978-1133188797 Solution Manual Gibson_Ch08_SM_13e Part 5

262 5. Return on Operating Assets = Operating Income Year-End Operating Assets 2010 2009 $437,975 $284,349 ($1,161,519 + $1,886,130 + $99,156) ($1,055,380 + $1,897,853+ $91,000) $3,146,805 $3,044,233 13.92% 9.34% 6. Sales to Fixed Assets = Net Sales Year-End Fixed Assets […]

978-1133188797 Solution Manual Gibson_Ch08_SM_13e Part 4

252 12. Return on Common Equity = Net Income Before Nonrecurring Items – Preferred Dividends Average Common Equity Average Balance Sheet Figures 2011: $72,700 – $6,400 – $6,300 = 13.36% ($520,000 – $70,000 + $518,000 – $70,200)/2 2010: $64,900 – […]

978-1133188797 Solution Manual Gibson_Ch08_SM_13e Part 3

PROBLEM 8-11 Net Profit Retained Earnings Total Stockholders’ Equity a. A stock dividend is declared and paid. b. Merchandise is purchased on credit. c. Marketable securities are sold above cost. d. Accounts receivable are collected. e. A cash dividend is […]

978-1133188797 Solution Manual Gibson_Ch08_SM_13e Part 2

232 5. Operating Income Margin = Operating Income Net Sales 2011 2010 2009 (2) Net sales $ 1,600,000 $ 1,300,000 $ 1,200,000 Less: Material and manufacturing costs of products sold 740,000 624,000 576,000 Research and development 90,000 78,000 71,400 General […]

978-1133188797 Solution Manual Gibson_Ch08_SM_13e Part 1

222 Chapter 8 Profitability QUESTIONS 8- 1. Profits can be compared to the sales from which they are the residual. They can in different directions, depending on the base. 8- 2. Extraordinary items are by nature nonrecurring. They should be […]

978-1133188797 Solution Manual Gibson_Ch07_SM_13e Part 3

207 CASES CASE 7-1 OUTSOURCED SERVICES (This case provides an opportunity to review capitalized interest.) a. 2010 2009 Income statement interest expense $ 40,707,000 $ 28,518,000 Capitalized interest 4,100,000 4,900,000 Total interest $ 44,807,000 $ 33,418,000 b. 2010 2009 2008 […]

978-1133188797 Solution Manual Gibson_Ch07_SM_13e Part 2

198 3. Debt/Equity Ratio = Total Liabilities Stockholders’ Equity $193,000 = 47.4% $407,000 4. Debt to Tangible Net Worth Ratio = Total Liabilities Tangible Net Worth $193,000 = 49.9% $407,000 – $20,000 b. New asset structure for all plans: Assets […]

978-1133188797 Solution Manual Gibson_Ch07_SM_13e Part 1

188 Chapter 7 Long-Term Debt-Paying Ability QUESTIONS 7- 1. Yes, profitability is important to a firm’s long-term, debt– paying ability. ability of the entity to meet its long-run obligations, the major emphasis when determining the long-term, debt-paying ability is on […]

978-1133188797 Solution Manual Gibson_Ch06_SM_13e Part 6

176 3. Days’ Sales in Inventory Ending Inventory Cost of Goods Sold/365 2010 2009 $3,155,000,000 $2,639,000,000 $13,831,000,000/365 $12,109,000,000/365 83.26 days 79.55 days 4. Inventory Turnover Cost of Goods Sold Year-End Inventory 2010 2009 $13,831,000,000 $12,109,000,000 $3,155,000,000 $2,639,000,000 4.38 times 4.59 […]

978-1133188797 Solution Manual Gibson_Ch06_SM_13e Part 5

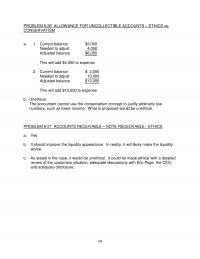

168 CONSERVATISM a. 1. Current balance $2,000 Needed to adjust 4,050 Adjusted balance $6,050 This will add $4,050 to expense 2. Current balance $ 2,000 Needed to adjust 10,000 Adjusted balance $12,000 This will add $10,000 to expense b. Unethical […]

978-1133188797 Solution Manual Gibson_Ch06_SM_13e Part 4

7. Operating Cycle = Accounts Receivable Turnover in Days + Inventory Turnover in Days 2011: 54.75 + 60.18 = 114.93 2010: 51.70 + 59.55 = 111.25 2009: 55.58 + 65.33 = 120.91 2008: 56.10 + 66.70 = 122.80 158 2007: […]

978-1133188797 Solution Manual Gibson_Ch06_SM_13e Part 3

148 d. Days’ Sales in Receivables: Gross Receivables = $50,000 = 4.56 days Net Sales/365 $4,000,000/365 e. Days’ Sales in Inventory: Ending Inventory = $400,000 = 81.11 days Cost of Goods Sold/365 $1,800,000/365 f. The days’ sales in receivables and […]

978-1133188797 Solution Manual Gibson_Ch06_SM_13e Part 2

138 PROBLEM 6-5 a. 365 days = 365 = 10.14 times per year Accounts receivable turnover in days 36 b. 365 days = 30.42 days 12.0 times per year c. Gross Receivables = $280,000 = 47.36 days Net Sales/365 $2,158,000/365 […]

978-1133188797 Solution Manual Gibson_Ch06_SM_13e Part 1

128 Chapter 6 Liquidity of Short-term Assets: Related Debt-Paying Ability QUESTIONS 6- 1. In the very short run, the procedure of making more funds available by slowing creditors would demand payment and they may refuse to sell to our firm […]

978-1133188797 Solution Manual Gibson_Ch05_SM_13e Part 2

110 Problem 5-3 Continued (In Percentage) Liabilities and Stockholders’ Equity 2010 2009 Current liabilities: Short-term borrowings and current portion of long- term debt 5.8 6.1 Accounts payable and accrued liabilities 13.3 13.9 Accrued payroll and related taxes 17.8 15.9 Accrued […]

978-1133188797 Solution Manual Gibson_Ch05_SM_13e Part 1

100 Chapter 5 Basics of Analysis QUESTIONS 5 – 1. A ratio is a fraction comparing two numbers. Ratios make the comparisons in 5 – 2. a. Liquidity is the ability to meet current obligations. Short-term creditors such as banks […]

978-1133188797 Solution Manual Gibson_Ch04_SM_13e Part 2

87 PROBLEM 4-13 a. 1. Receipt of cash: Sales, 210,000 ounces x $300 = $ 63,000,000 Cost of goods sold (1), 210,000 ounces x $250 = (52,500,000) Gross profit $ 10,500,000 Selling expenses (2,000,000) Administrative expenses (1,250,000) Profit before taxes […]