CHAPTER

14

Cost Planning

CHAPTER OUTLINE:

I. Introduction

A. Why Budgets are Useful

B. Definition of Performance Reporting

II. Cost Classifications

A. Relationship of Cost to Volume of Activity

2. Fixed cost

3. Mixed cost

B. According to a Time-Frame Perspective

1. Committed cost

2. Discretionary cost

III. Budgeting

A. The Budgeting Process in General

1. Usefulness of budgets–A function of management philosophy

2. Starting point for budget

a. Actual performance of current period

b. Zero–based budgeting approach

B. The Budget Time Frame

2. Multi–period, rolling budget

3. Different periods for different budgets

C. The Budgeting Process

1. Broad assumptions about the economy, industry, and company

2. Operating budget

a. Sales/revenue forecast

b. Purchases/production budget

Chapter 14 Cost Planning

CHAPTER OUTLINE (continued)

e. Cash budget and the timing of cash receipts and cash payments

f. Balance sheet budget

3. Sales forecast is the key

D. Illustration of the Purchases/Production Budget

1. Using the cost of goods sold model

2. Based on gross profit ratio

E. Cost of Goods Sold Budget Discussion

F. Operating Expense Budget Challenges

G. Budgeted Income Statement Discussion

IV. Standard Costs

A. Standards Defined – A Unit Budget Allowance

B. Using Standard Costs

2. Focus may be on dollar amounts and/or quantities

C. Developing Standards

2. Attainable standards

3. Past experience standards

D. Costing Products with Standard Costs

1. A budget for each component

2. Illustration of product cost development

E. Other Uses of Standards

V. Budgeting for Other Analytical Purposes

A. Other Important Resources

2. Utilization of productive capacity

B. Other Functional Areas

Instructor’s Manual / Solutions Manual

TEACHING/LEARNING OBJECTIVES:

Primary: To have the student understand:

1. That the sales/activity forecast is the starting point – and the key – to the entire budgeting

process.

3. That standard costs are unit budgets, and in turn, to appreciate how standards can be used in

the planning and control process.

Supporting: To have the student understand:

4. The significance of top management’s attitude toward the budgeting process, and the

5. That different time periods may be appropriate for different budgets.

6. How individual budgets interrelate to make up the overall operating budget.

TEACHING OBSERVATIONS:

1. The reasons for and advantages of budgeting for an entity can be related to the personal

budgeting that students may have done.

3. Be careful not to get caught up in the “how to” aspects of preparing budgets, or students

4. Emphasize that standards are unit budgets, and can be used to accomplish all of the

objectives associated with budgets.

5. Call attention to the behavioral implications that result from the standard setting process and

emphasize the importance of the perception that standards are attainable by those whose

Chapter 14 Cost Planning

ASSIGNMENT OVERVIEW:

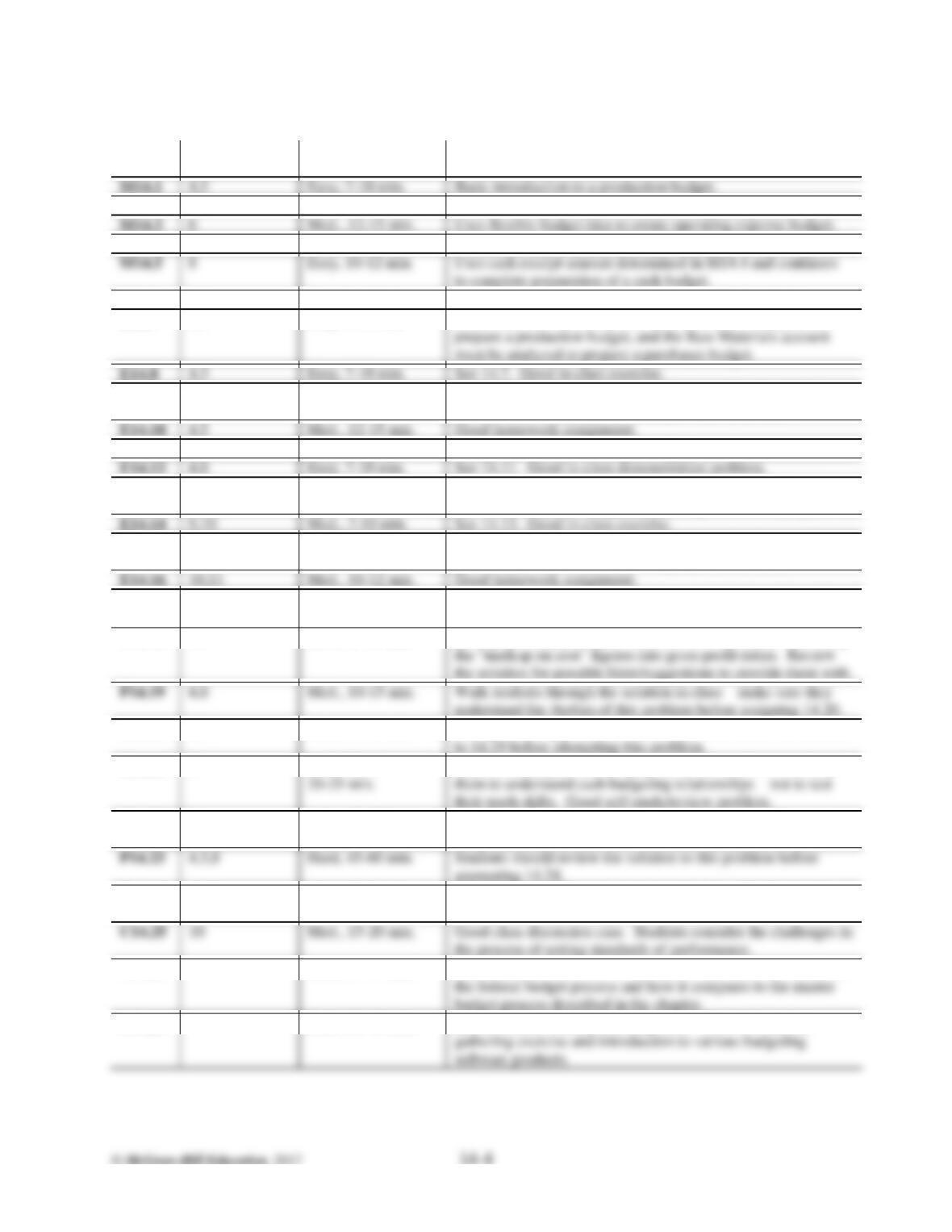

NO.

LEARNING

OBJECTIVES

DIFFICULTY &

TIME ESTIMATE

OTHER COMMENTS

M14.1

4,5

Easy, 7-10 min.

Basic introduction to a production budget.

M14.2

4,5

Med., 10-12 min.

Purchases budget requires analysis of beginning inventory.

M14.3

6

Med., 12-15 min.

Uses flexible budget idea to create operating expense budget.

M14.4

8

Easy, 7-10 min.

Straight-forward analysis of cash receipts.

M14.5

8

Easy, 10-12 min.

Uses cash receipt amount determined in M14.4 and continues

to complete preparation of a cash budget.

M14.6

10

Easy, 7-10 min.

Basic introduction to standard cost per unit determination.

E14.7

4,5

Easy, 7-10 min.

Stress that the Finished Goods account must be analyzed to

E14.8

4,5

Easy, 7-10 min.

See 14.7. Good in-class exercise.

E14.9

5

Easy, 7-10 min.

Emphasize the importance of management planning in the

development of appropriate ending inventory policies.

E14.10

4,5

Med., 12-15 min.

Good homework assignment.

E14.11

4,8

Easy, 5-8 min.

Straight-forward cash receipts budget.

E14.12

4,8

Easy, 7-10 min.

See 14.11. Good in-class demonstration problem.

E14.13

9,10

Easy, 5-8 min.

Emphasize that standards must be appropriate and fair if they

are to be useful for managerial planning and control purposes.

E14.14

9,10

Med., 7-10 min.

See 14.13. Good in-class exercise.

E14.15

10,11

Easy, 5-8 min.

Emphasize the importance of management planning and data

gathering in the development of appropriate standards.

E14.16

10,11

Med., 10-12 min.

Good homework assignment.

P14.17

4,5

Med., 10-12 min.

The key is to calculate budgeted cost of sales for each month,

using: Sales * (1 – Gross profit ratio).

P14.18

4,5

Hard, 15-20 min.

Group learning problem. Students have difficulty converting

4,8

Med., 10-15 min.

Walk students through the solution in class—make sure they

understand the rhythm of this problem before assigning 14.20.

P14.20

4,8

Hard, 25-35 min.

to 14.19 before attempting this problem.

Group learning problem. Students should review the answers

P14.21

8

Med.-Hard,

Explain to students that the purpose of this problem is to help

P14.22

8

Hard, 45-60 min.

Excel problem. Group learning problem. Good homework

assignment.

P14.23

4,5,8

Hard, 45-60 min.

Students should review the solution to this problem before

attempting 14.24.

P14.24

4,5,8

Hard, 45-60 min.

Excel problem. Group learning problem. Emphasize the

inter-relationships among the budgets.

C14.25

Med., 15-20 min.

Good class discussion case. Students consider the challenges in

the process of setting standards of performance.

C14.26

Med., 30-40 min.

budget process described in the chapter.

Internet case. This case is intended to introduce the student to

C14.27

Med., 30-45 min.

gathering exercise and introduction to various budgeting

software products.

Internet case. Group learning case. Good information

M14.1.

Use the cost of goods sold model, and work from the bottom up and then top down to

calculate production:

June

July

Beginning inventory…………………………..………………

3,600

4,800

Add: Production……………………………..………………..

?

?

Goods available for sale ……………………..……………..…

?

?

Less: Ending inventory (16,000 * 30%) ……..………………

(14,000 * 30%) …..…………………

Units sold………………………………………………………

M14.2.

Use the same approach as M14.1, but notice that raw material used is a function of

quantity produced from the production budget. Each unit requires 3 pounds of raw

material.

June

Beginning inventory (13,200 * 3 pounds * 25%) …….……….……

9,900

Purchases ……………………………………………………………

Raw materials available for use ………………………………..……

Less: Ending inventory (15,400 * 3 pounds * 25%) ……..…….……

Raw materials used in production (13,200 * 3 pounds)…….………

Raw materials available for use = 39,600 + 11,550 = 51,150 pounds

M14.3.

Variable

Rate

June

July

August

Budgeted sales (units)…..…………….

12,000

16,000

14,000

Variable operating expenses:

Sales commissions…….…………..

$2.00/unit

$24,000

$32,000

$28,000

Marketing promotions……………..

$1.00/unit

12,000

16,000

14,000

Supplies…………………………….

$0.75/unit

12,000

10,500

Bad debt expense…………………..

$0.25/unit

Utilities……………………………..

$0.50/unit

6,000

8,000

7,000

Total variable expense………….……

M14.3.

(continued)

June

July

August

Fixed operating expenses:

Salaries……………………………..

$ 2,000

$ 2,000

$ 2,000

Rent…………………………………

Depreciation………………………..

Advertising…………………………

Utilities……………………………..

3,000

3,000

3,000

Total fixed expense……….…….……

Budgeted operating expense………….

$69,600

$87,600

$78,600

M14.4.

June

July

August

Budgeted sales units……..……………………….

12,000

16,000

14,000

Unit selling price…………………………………

$18

$18

$18

30% of current month’s sales………………….

60% of prior month’s sales…………………….

172,800

8% of second prior month’s sales……………..

Total collections…………………………………

$265,680

M14.5.

August

Beginning cash balance….……………………………….…….

$ 25,000

Cash Receipts:

Cash collections from sales………..……………………….

265,680

Total cash available……………………………………………

$290,680

Cash Disbursements:

For payment of inventory purchases……………………….

40,000

For payment of other manufacturing expenses……………..

For payment of operating expenses…………………………

76,200

For payment to retire bond…………………………………

For payment of dividends………………………………….

15,000

Total cash disbursements……………………………………..

Excess of available cash over disbursements…………………

$ 11,480

Ending cash balance…………………………………………..

$ 20,000

M14.6.

Cost per unit

Raw materials (3 pounds per unit * $1 per pound) ….……………..

Direct labor (0.25 hours per unit * $12 per hour)………………….

Standard cost per unit

E14.7.

a.

Use the cost of goods sold model, and work from the bottom

up and then top down to calculate production:

medallions

Beginning inventory…………………………………………

1,000

Goods available for sale..……………………………………

?

Less: Ending inventory………………………………………

(800)

Quantity sold…………………………………………………

2,000

Goods available for sale = 2,000 + 800 = 2,800 medallions

b.

Use the same approach, but notice that quantity used is a

function of quantity produced from the production budget.

Each medallion requires 2/3 of a yard of ribbon.

yards

Beginning inventory…………………………………………

Purchases ……………………………………………………

Raw materials available for use …………………………….

Less: Ending inventory………………………………………

(20)

Raw materials used in production (2/3 * 1,800 medallions)…

1,200

Raw materials available for use = 1,200 + 20 = 1,220 yards

E14.8.

a.

Use the “Cost of Goods Sold” model:

Beginning inventory, Finished Goods………………………..

5,900

Add: Production………………………………………………

64,400

Goods available for sale………………………………………

Less: Ending inventory, Finished Goods…………………….

(8,300)

Units sold…………………………………………………….

Steps:

(1) Units sold based on sales forecast.

(2) Ending inventory is given.

(3) Goods available for sale = units sold (based on sales

forecast) + ending inventory.

(4) Beginning inventory is given.

(5) Production = goods available – beginning inventory.

Chapter 14 Cost Planning

E14.8.

(continued)

b.

Beginning inventory, Raw Materials …………………..……

74,700

Add: Purchases………………………………………………

315,500

Raw materials available for use ……………………..………

Less: Ending inventory, Raw Materials …………….………

Raw materials used in production ……………………..……

Steps:

(1) Raw materials used in production = units produced *

pounds per unit = 64,400 * 5 = 322,000 pounds

(2) Ending inventory is given

(3) Raw materials available for use = raw materials used in

production + ending inventory

(4) Beginning inventory is given

E14.9.

a.

Use the raw material inventory/usage model:

Quarter I

Quarter II

Beginning inventory …………………………………………

5,000

9,000

Add: Purchases ………………………………………………

?

?

Raw materials available for use ……………………………..

Less: Ending inventory (25% of next quarter’s usage)………

Usage (2 ounces * number of gallons of product to be produced)…

Working backwards (up the model):

Raw materials available for use ……………………………..

Purchases (subtract beginning inventory)……………………

b.

production forecast.

Inventory provides a “cushion” for delivery delays or production needs in excess of the

E14.10.

a.

July

August

September

Sales forecast (units)

6,000

6,800

5,600

Production forecast (analysis of finished goods inventory):

Beginning inv. (70% of current month’s sales)…..

4,000 a

4,760

3,920

Add: Production…………………………………..

? .

? .

? .

Less: Ending inv. (70% of next month’s sales)…..

(3,920)

(3,710)

6,800

5,600

E14.10.

(continued)

Working backwards (up the model):

July

August

September

Goods available for sale……………………………

10,760

10,720

9,310

Production (subtract beginning inventory)…….…

b.

For raw materials purchases, the model is similar, but keys on the production forecast

and raw materials inventory instead of the sales forecast and finished goods inventory.

July

August

September

Production forecast (units)…………………..……

6,360

5,960

5,390

Raw materials used (6.5 pounds per unit)……..…

41,340

38,740

35,035

Purchases forecast (analysis of raw materials inventory):

Beginning inv. (60% of current month’s usage)...

26,000 b

23,244

Purchases (in pounds)….…………………………

? .

? .

Raw materials available for use………………..…

?

?

Less: Ending inv. (60% of next month’s usage)....

(23,244)

Raw materials used (in pounds)………………..…

38,740

Working backwards (up the model):

Raw materials available for use………………..…

64,584

59,761

Purchases (subtract beginning inventory)…………

E14.11.

May

June

July

August

Sales forecast…………………………

$240,000

$280,000

$300,000

$350,000

Cash collections:

30% of current month’s sales …………………………………

$ 90,000

$105,000

150,000

18% of second prior month’s sales ……………………………

43,200

E14.12.

July

August

September

October

November

Actual sales

$98,000

$105,000

Sales forecast

$114,000

$94,000

$122,000

Cash collections:

30% of sales made in the current month……

$ 34,200

$ 28,200

$36,600

55% of prior month’s sale……………………

9,800

10,500

11,400

E14.13.

a.

Worktype 1 (0.15 hours @ $12.30 per hour)

$ 1.845

Worktype 2 (0.30 hours @ $10.90 per hour)

Worktype 3 (0.60 hours @ $19.50 per hour)

Total direct labor cost per pedestal

E14.14.

a.

Costs for a “batch” of 10 quarts:

Triphate solution (11 quarts @ $0.30 per quart) ………………………

$ 3.30

Sobase granules (4 pounds @ $0.74 per pound) ………………………

2.96

Methage (2 ounces @ $1.20 per ounce)…………………………………

2.40

Bottles (10 @ $0.12 each)………………………………………………

Total cost for 10 quarts…………………………………………………

$ 9.86

Cost per quart ($9.86 / 10 quarts)…………..……………………………

b.

Other factors to be considered:

1. Possible cost increases during coming year.

2. Spillage / spoilage / waste in the manufacturing process.

E14.15.

a.

Raw material cost………………………………………………

$2.83 per bushel

Direct labor and variable overhead ……………………………

0.42 per bushel

Fixed overhead…………………………………………………

0.35 per bushel

b.

This cost per pound is not very useful for management planning and control because it

includes unitized fixed expenses, which do not behave on a per unit basis.

E14.16.

a.

Raw materials:

Sheet metal cost for 12 pads (1.5 * $0.14 cost of sheet metal for 8 pads)…..

Foam pad cost for 12 pads (12 pads * $0.02 cost per pad)..…………………