Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

12-21

P12.25.

(continued)

c.

Break-even point in sales dollars = Fixed expenses / Contribution margin ratio

= $70,000 / 50% = $140,000

d.

Because sales mix might change. For example, if the company sold only the economy

model, total contribution margin would equal the economy model contribution margin

ratio ($5 / $12 = 41.666%) multiplied by the current break-even point in sales dollars of

e.

Proposed Expansion:

Luxury

Economy

Value

Total

Rev.

$20 * 6,000 = $120,000

$12 * 17,000 = $204,000

$15 * 8,000 = $120,000

$444,000

f.

No. Based on this data analysis, adding the Value model would result in lower total

operating income by $21,000 ($150,000 current operation versus $129,000 proposed).

P12.26.

a.

MegaMuscle

PowerGym

ProForce

Selling price per unit (A)

$170

$220

$310

b.

MegaMuscle

PowerGym

ProForce

Monthly sales volume

4,000 units

3,000 units

1,000 units

Selling price per unit

$ 170

$ 220

$ 310

Sales

$680,000

$660,000

$310,000

Chapter 12 Managerial Accounting and Cost-Volume-Profit Relationships

P12.26.

(continued)

c.

Break-even point = Fixed expenses / Overall CM ratio

= $468,000 / 30.1% = $1,554,817

d.

Operating income = Total CM - Fixed expenses

= $497,000 - $468,000 = $29,000

P12.27.

a.

Per Unit

*

Volume

=

Total

%

Revenue

$ 32

100.0%

Variable Expense

20

62.5%

b.

Per Unit

*

Volume

=

Total

%

Revenue

$ 32

100.0%

Variable Expense

20

62.5%

c.

1.

Per Unit

*

Volume

=

Total

%

Revenue

$ 32

100.00%

12-23

P12.27.

(continued)

2.

Per Unit

*

Volume

=

Total

%

Revenue

$ 32

100.00%

3.

As sales volume moves above the break-even point, contribution margin and operating

4.

The new cost structure has much more risk, because if sales volume declines, the

P12.28.

a.

Contribution margin ratio = $378,000 / $840,000 = 45%

Break-even revenues = ($290,000 fixed expenses / 45% CM ratio) = $644,444 (rounded)

b.

If the new machine is leased:

Sales volume = 1,500 units * 120% = 1,800 units

Selling price per unit = $840,000 / 1,500 units = $560 per unit

Break-even revenues = ($320,000 fixed expenses / 50% CM ratio) = $640,000

c.

Revenues (1,800 units * $560 per unit) ……………….………………

$1,008,000

Variable expenses (1,800 units * $280 per unit)………………………

(504,000)

Note: Increase in operating income ($184,000 - $88,000)……………

$ 96,000

Increase in operating income due to operating leverage:

Increase in operating income due to additional sales:

(1,800 – 1,500) * $280 per unit contribution margin…………………

$ 84,000

Chapter 12 Managerial Accounting and Cost-Volume-Profit Relationships

12-24

d.

Yes, the new machine should be leased. The break-even point in sales dollars remains

nearly the same under both alternatives because the increase in fixed costs is offset by a

decrease in variable costs, which results in an increase in the contribution margin ratio.

C12.29.

Pros:

1.

The sale will still generate a positive contribution margin ratio of 14% (rounded).

To illustrate, assume that the normal selling price is $1.00 — which would mean that

the normal variable cost is $0.60 and the normal contribution margin is $0.40. If the

discount is given, the selling price will fall to $0.70 — which would mean that the

contribution margin will fall to $0.10, and the contribution margin ratio will fall to

14% ($0.10 / $0.70).

3.

The candy given to the children will increase brand awareness and could lead to

greater sales volume in the future.

4.

The Substance Abuse Awareness Club is a positive moral force in the community.

Cons:

1.

Sweet Tooth Candy Company incurs an opportunity cost equal to the lost contribution

2.

When other customers learn of the discounted sale, they may ask for the same special

3.

Special pricing transactions that are not based on quantity discounts may be in

violation of federal price discrimination laws. Legal counsel should be consulted

before agreeing to the special price.

Recommendation: An appropriate corporate policy and other safeguards concerning

special order pricing arrangements should be developed, and the candy should be sold

at the special price.

Instructor’s Manual / Solutions Manual

C12.30.

To: Tommy

From: Your Idea Person

Subject: Attitude Adjustment Proposal

It is recommended that a proposal be made to the restaurant manager that drink prices

be set at $3.00 in exchange for our organization's special promotion of the restaurant

for our meetings. With a regular price of $4.00 and a 50% contribution margin ratio,

C12.31.

a.

As a firm increases operating leverage by adding more fixed expenses to its cost

structure, the break-even point in terms of units and sales dollars also increases. Thus,

a principal risk associated with greater operating leverage is that a decrease in sales—

which leads to decreases in contribution margin, operating income, and cash flows—

may result in a relatively greater inability to cover fixed expenses. Why? Because

b.

1. Financial leverage relates to a firm’s use of long-term debt in its capital structure,

and operating leverage relates to a firm’s use of fixed costs in its cost structure.

2. Financial leverage reflects a financing decision on the part of management—how

much money to borrow and thereby how much interest expense to take on.

3. Financial leverage magnifies ROE relative to ROI. This adds risk: ROI must exceed

the cost of debt (i.e., the interest rate on borrowed funds) in order for financial

C12.31.

(continued)

Chapter 12 Managerial Accounting and Cost-Volume-Profit Relationships

12-26

4. With financial leverage, the magnification on ROE works both ways; the more

leveraged the firm is, the more its stockholders lose as a percentage of their

C12.32.

a.

Step 1: Calculate the contribution margin ratio for each firm:

HighTech, Inc.

OldTime Co.

Sales……………………………

$2,100,000

100%

$2,100,000

100%

Variable expenses………………

420,000

20%

1,260,000

60%

b.

The break-even point for each firm is different because each firm has a different amount of

fixed costs to be recovered and a different contribution margin ratio that represents the rate

c.

Solution approach: Prepare all changes relative to each assumed change in sales volume.

Calculate the variable expense ratio for each firm using the income statement data

provided – 20% for HighTech, Inc. and 60% for OldTime Co.

1. Increase in Sales by 20%

HighTech, Inc.

OldTime Co.

Sales………………………………………………

$2,520,000

$2,520,000

2. Decrease in Sales by 20%

HighTech, Inc.

OldTime Co.

Sales………………………………………………

$1,680,000

$1,680,000

Instructor’s Manual / Solutions Manual

12-27

C12.32.

(continued)

d.

HighTech, Inc.

OldTime Co.

1. Operating income reported in 2015 ………………

$210,000

$210,000

2. Operating income reported in 2015 ………………

$210,000

$210,000

e.

HighTech, Inc. has significantly more operating leverage than does OldTime Co. because

HighTech’s fixed costs are much higher ($1,470,000 versus $630,000) and its

contribution margin ratio is also much higher (80% versus 40%). Thus, if sales

increase/decrease by 20% in 2016, HighTech, Inc. will benefit/suffer proportionately

more than OldTime Co. because OldTime’s cost structure is riskier.

i.

The answer calculated in part (h) is equal to the answer calculated in part (d). The

important point is that an expected change in operating income can be computed given a

percentage change in sales by knowing each firm's degree of operating leverage. The

degree of operating leverage is calculated by dividing a firm's total contribution margin

Chapter 12 Managerial Accounting and Cost-Volume-Profit Relationships

12-28

C12.33.

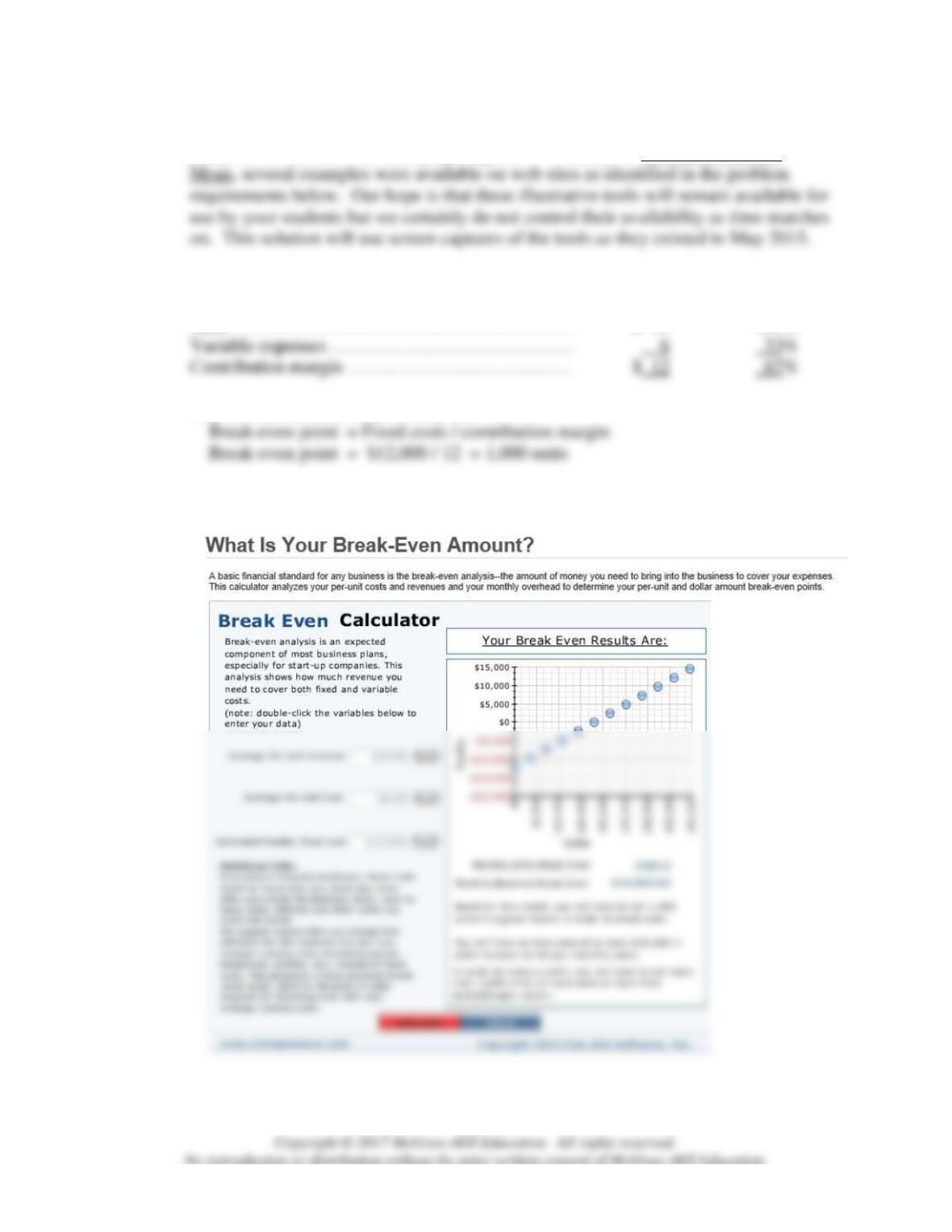

Note to instructor: The purpose of this case is to illustrate some of the problem

solving tools available over the Internet for certain applications like break-even

analysis. At the time we were preparing this 11th Edition of What the Numbers

Step 1: Calculate the contribution margin for Dominic's Italian Cafe:

Per Unit

Percentage

Sales ………………………………………………

$ 18

100%

Step 2: Calculate the break-even point:

a.

1. The following solution screen is from the entrepreneur.com site:

Instructor’s Manual / Solutions Manual

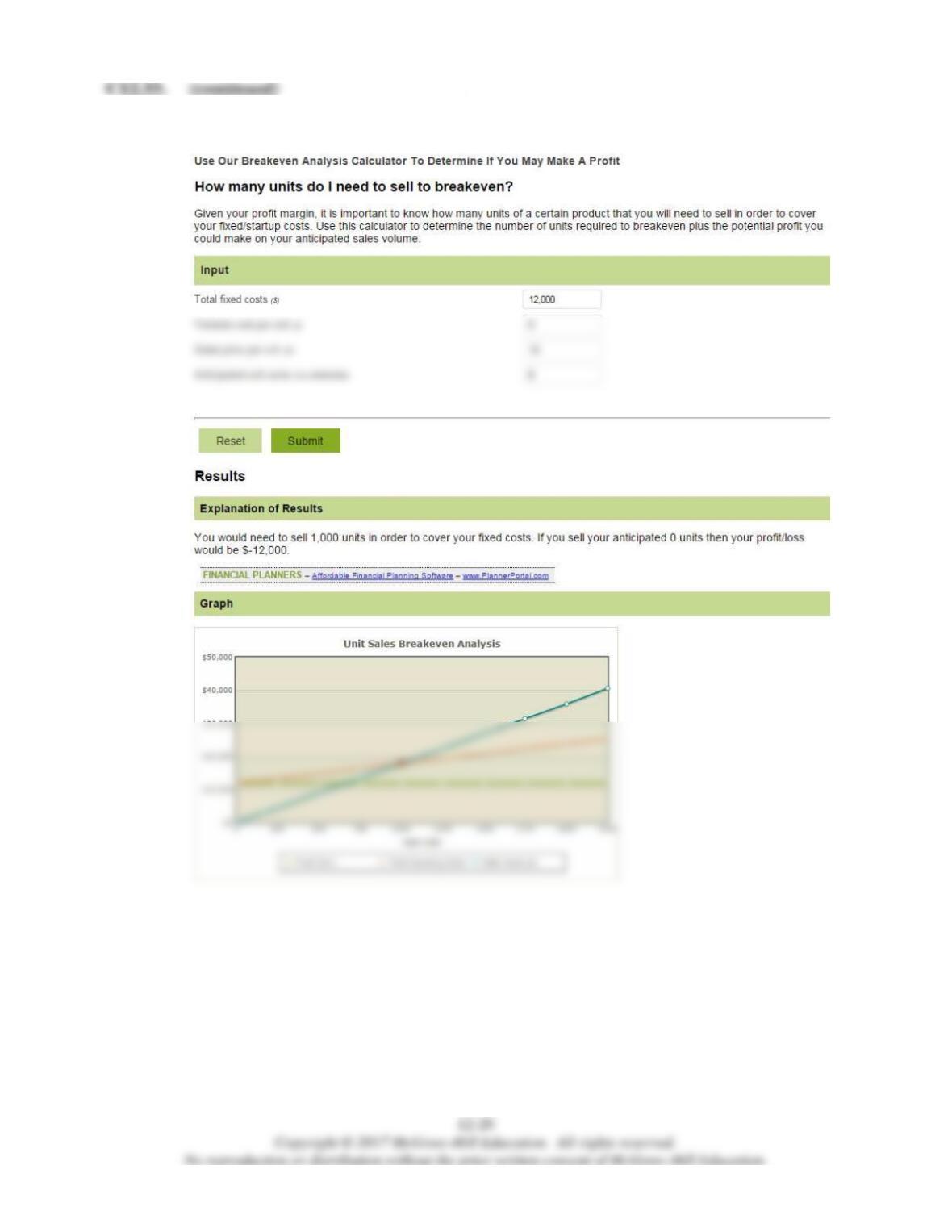

2. The following solution screen is from the calcxml.com site:

Chapter 12 Managerial Accounting and Cost-Volume-Profit Relationships

12-30

C12.33.

(continued)