Archives: Solution Manual

978-0078025679 Chapter 15 Lecture Note Part 1

Financial Reporting and Analysis 6e Financial Reporting for Owner’s Equity CHAPTER 15 FINANCIAL REPORTING FOR OWNERS’ EQUITY CHAPTER OVERVIEW Statement readers must understand accounting procedures and reporting conventions for owner’s equity for the following reasons: (1) Appropriate income measurement; (2) […]

978-0078025679 Chapter 14 Solution Manual Part 5

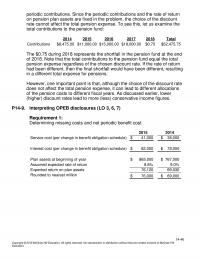

14–55 + Contributions 150.00 – Pension Benefits Paid at end of Year (350.00) = Dec 31 2013 / Jan 1 2014 PBO Balance $4,160.00 The corridor is 10% of Maximum $($6,650 PBO, $4,160 plan assets) or $665. The “cost” of […]

978-0078025679 Chapter 14 Solution Manual Part 4

14–46 periodic contributions. Since the periodic contributions and the rate of return on pension plan assets are fixed in the problem, the choice of the discount rate cannot affect the total pension expense. To see this, let us examine the […]

978-0078025679 Chapter 14 Solution Manual Part 3

14–31 P14–5. Calculating PBO, ABO and pension expense Requirement 1: Calculation of PBO on January 1, 2014: Annual pension benefits starting on 12/31/2029 and continuing for 10 years thereafter (11 years total = 76 – 66). Years of service credit […]

978-0078025679 Chapter 14 Solution Manual Part 2

14–16 E14-21. Determining pension elements (LO 3, 4, 6) Requirement 1: Prior Service Cost Amortization Year ended 2014 ($650,000/20) = $32,500 Year ended 2015 ($650,000/20) = 32,500 Requirement 2: Pension Expense for 2014: Service cost $ 45,000 Interest cost ($650,000 […]

978-0078025679 Chapter 14 Solution Manual Part 1

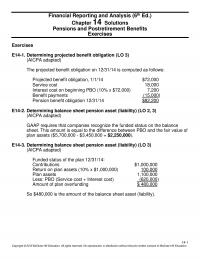

14-1 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Financial Reporting and Analysis (6th Ed.) Chapter 14 Solutions E14–1. Determining projected benefit obligation (LO 3) (AICPA adapted) The […]

978-0078025679 Chapter 14 Lecture Note

Financial Reporting and Analysis 6e Pensions and Postretirement Benefits CHAPTER 14 PENSIONS AND POSTRETIREMENT BENEFITS CHAPTER OVERVIEW Pension plan contracts allow employees to exchange current service for payments to be received during retirement. Defined contribution pension plans specify amounts to […]

978-0078025679 Chapter 13 Solution Manual Part 4

13–42 is in “steady–state,” whereby its fixed asset acquisitions are just sufficient to replace its assets going out of service, it has no net change in deferred tax liabilities related to fixed assets. Intangible assets other than nondeductible goodwill: This […]

978-0078025679 Chapter 13 Solution Manual Part 3

13–31 As the above journal entries indicate, Lance has no deferred tax assets or liabilities under U.S. GAAP because the same method is used for book and tax. Under IFRS, a deferred tax liability results. The amounts reported are $35,000 […]

978-0078025679 Chapter 13 Solution Manual Part 2

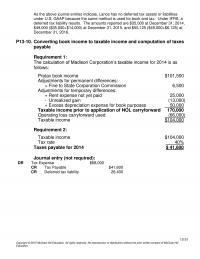

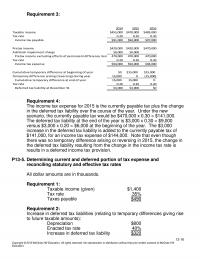

13–16 Requirement 3: 2014 2015 2016 Taxable income $455,000 $470,000 $485,000 Tax rate 0.20 0.20 0.20 Income tax payable $91,000 $94,000 $97,000 Pretax income $420,000 $420,000 $470,000 Add back impairment charge 50,000 50,000 Pretax income excluding effects of permanent difference […]

978-0078025679 Chapter 13 Solution Manual Part 1

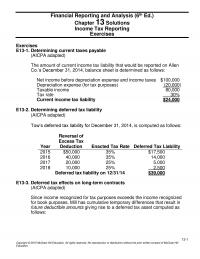

13-1 Financial Reporting and Analysis (6th Ed.) Chapter 13 Solutions Income Tax Reporting Exercises Exercises E13–1. Determining current taxes payable (AICPA adapted) The amount of current income tax liability that would be reported on Allen Co.’s December 31, 2014, balance […]

978-0078025679 Chapter 13 Lecture Note

Financial Reporting and Analysis 6e Income Tax Reporting CHAPTER 13 INCOME TAX REPORTING CHAPTER OVERVIEW The rules for computing income for financial reporting purposes—book income—differ from the rules for computing income for tax purposes. The differences between book income and […]

978-0078025679 Chapter 12 Solution Manual Part 6

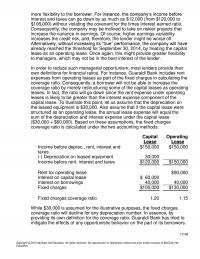

12–69 more flexibility to the borrower. For instance, the company’s income before interest and taxes can go down by as much as $12,000 (from $120,000 to $108,000) without violating the covenant for the times interest earned ratio. Consequently, the company […]

978-0078025679 Chapter 12 Solution Manual Part 5

12–61 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Financial Reporting and Analysis (5th Ed.) Chapter 12 Solutions Financial Reporting for Leases Cases Cases C12-1. AMR Corporation: Constructively […]

978-0078025679 Chapter 12 Solution Manual Part 4

12–46 Requirement 4: MONTHLY REDUCTION PAYMENT INTEREST LEASE IN RECEIVABLE DATE INCOME PAYMENTS RECEIVABLE BALANCE 09/01/14 60,000.00$ 09/01/14 –$ 1,789.20$ 1,789.20$ 58,210.80 10/01/14 582.11 1,789.20 1,207.09 57,003.71 11/01/14 570.04 1,789.20 1,219.16 55,784.55 12/01/14 557.85 1,789.20 1,231.35 54,553.20 01/01/15 545.53 1,789.20 […]

978-0078025679 Chapter 12 Solution Manual Part 3

12–31 P12–6. Assessing guaranteed and unguaranteed residual values for the lessee (LO 3, 4, 5) Requirement 1: This is a capital lease for Task because the lease meets at least one of the criteria for capital lease treatment. The lease […]

978-0078025679 Chapter 12 Solution Manual Part 2

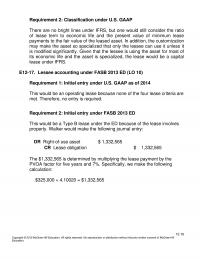

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Requirement 2: Classification under U.S. GAAP There are no bright lines under IFRS, but one would still consider the ratio […]

978-0078025679 Chapter 12 Solution Manual Part 1

12-1 Financial Reporting and Analysis (6th Ed.) Chapter 12 Solutions Financial Reporting for Leases Exercises Exercises E12–1. Accounting for lessee with purchase option (LO 3, 4, 5) Requirement 1: Amount capitalized by Leland at 07/01/2014 The $100,000 represents a bargain […]

978-0078025679 Chapter 12 Lecture Note

Financial Reporting and Analysis 6e Financial Reporting for Leases CHAPTER 12 FINANCIAL REPORTING FOR LEASES Chapter Overview The treatment of leases in FASB ASC 840 represents a compromise between the unperformed–contract and property-right approaches. FASB ASC 840 adopts a middle-of–the- […]

978-0078025679 Chapter 11 Solution Manual Part 5

11–54 The issue price would by $219.231 million if the market yield is 8.125% and $290.816 million if the market yield is 6.125%. Requirement 8: Century and millennium bonds share a common feature: a very large share of the issue […]

978-0078025679 Chapter 11 Solution Manual Part 4

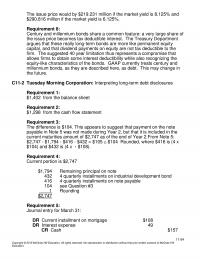

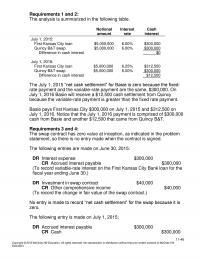

11–46 Requirements 1 and 2: The analysis is summarized in the following table. Notional amount Interest rate Cash interest July 1, 2015: First Kansas City loan $5,000,000 6.00% $300,000 Quincy B&T swap $5,000,000 6.00% $300,000 Difference in cash interest $0 […]

978-0078025679 Chapter 11 Solution Manual Part 3

11–31 It does not appear as though Checkpoint Systems has already recognized a loss contingency reserve related to this law suit because there is no mention of a recorded loss accrual or provision. (By comparison, notice what Visa has to […]

978-0078025679 Chapter 11 Solution Manual Part 2

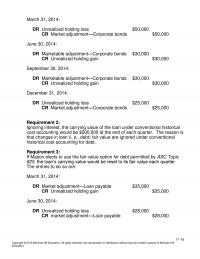

11–16 March 31, 2014: DR Unrealized holding loss $50,000 CR Market adjustment—Corporate bonds $50,000 June 30, 2014: DR Marketable adjustment—Corporate bonds $30,000 CR Unrealized holding gain $30,000 September 30, 2014: DR Marketable adjustment—Corporate bonds $30,000 CR Unrealized holding gain $30,000 […]

978-0078025679 Chapter 11 Solution Manual Part 1

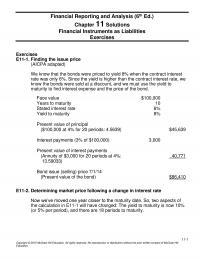

11-1 Financial Reporting and Analysis (6th Ed.) Chapter 11 Solutions Financial Instruments as Liabilities Exercises Exercises E11–1. Finding the issue price (AICPA adapted) We know that the bonds were priced to yield 8% when the contract interest rate was only […]

978-0078025679 Chapter 11 Lecture Note

Financial Reporting and Analysis 6e Financial Instruments as Liabilities CHAPTER 11 FINANCIAL INSTRUMENTS AS LIABILITIES CHAPTER OVERVIEW A financial statement liability is (1) a currently existing obligation arising from past events, which necessitates (2) payment of cash, or provision of […]

978-0078025679 Chapter 10 Solution Manual Part 4

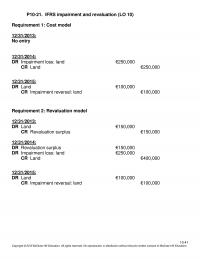

10–41 P10–21. IFRS impairment and revaluation (LO 10) Requirement 1: Cost model 12/31/2013: No entry 12/31/2014: DR Impairment loss: land €250,000 CR Land €250,000 12/31/2015: DR Land €100,000 CR Impairment reversal: land €100,000 Requirement 2: Revaluation model 12/31/2013: DR Land […]

978-0078025679 Chapter 10 Solution Manual Part 3

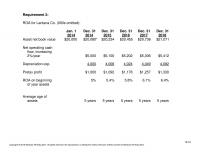

10–31 Requirement 2: ROA for Lantana Co. (000s omitted): Jan. 1 Dec. 31 Dec. 31 Dec. 31 Dec. 31 Dec. 31 2014 2014 2015 2016 2017 2018 Asset net book value $20,000 $20,080* $20,234 $20,455 $20,736 $21,071 Net operating cash […]

978-0078025679 Chapter 10 Solution Manual Part 2

10–16 P10–7. Determining asset impairment Requirement 1: Book value: = $35,000,000 – [($35,000,000/7) x 4] = $35,000,000 – 20,000,000 = $15,000,000 Requirement 2: Yes, the asset is impaired. The book value of $15,000,000 is greater than the undiscounted future cash […]

978-0078025679 Chapter 10 Solution Manual Part 1

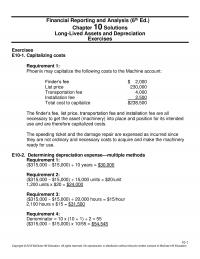

Financial Reporting and Analysis (6th Ed.) Chapter 10 Solutions Long-Lived Assets and Depreciation Exercises Exercises E10–1. Capitalizing costs Requirement 1: Phoenix may capitalize the following costs to the Machine account: Finder’s fee $ 2,000 List price 230,000 Transportation fee 4,000 […]

978-0078025679 Chapter 10 Lecture Note

Financial Reporting and Analysis 6e Long-Lived Assets CHAPTER 10 LONG-LIVED ASSETS CHAPTER OVERVIEW Generally accepted accounting principles for long–lived assets are far from perfect. The need for reliable (unbiased and accurate), cost–effective, and objective (verifiable) numbers causes these assets to […]

978-0078025679 Chapter 1 Solution Manual Part 2

1-14 1) By identifying the key business and financial risks facing the company, the audit committee can ensure that those risks are properly disclosed in the MD&A (Management Discussion & Analysis) section of the annual report. A second reason is […]

978-0078025679 Chapter 1 Solution Manual Part 1

1-1 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Financial Reporting and Analysis (6th Ed.) Chapter 1 Solutions The Economic and Institutional Setting for Financial Reporting Problems Problems […]

978-0078025679 Chapter 1 Lecture Note

Financial Reporting and Analysis 6e The Economic and Institutional Setting for Financial Reporting CHAPTER 1 THE ECONOMIC AND INSTITUTIONAL SETTING FOR FINANCIAL REPORTING CHAPTER OVERVIEW Financial statements contain information about a company, its economic health, and its products that help […]

978-0078025600 Chapter 9 Solution Manual Part 3

Problem 9-2B (60 minutes) 1. Each employee’s FICA withholdings for Social Security Ahmed Carlos June Marie Total Maximum base ………… $110,100 $110,100 $110,100 $110,100 Earned through 9/23 … 108,500 36,650 6,650 22,200 Amount subject to tax $ 1,600 $ 73,450 […]

978-0078025600 Chapter 9 Solution Manual Part 2

Financial & Managerial Accounting, 5th Edition 514 Exercise 9-17 (concluded) (b) Aug 31 Salaries (or Wages) Expense ………………………….. 10,020.00 FICA—Social Sec. Taxes Payable ………….……. 298.84 FICA—Medicare Taxes Payable ……………..……. 145.29 Employee Fed. Inc. Taxes Payable ………………. 2,380.00 Employee State Inc. […]

978-0078025600 Chapter 9 Solution Manual Part 1

Chapter 9 Current Liabilities QUESTIONS 1. A current liability is expected to be paid within one year or the company’s operating cycle, whichever is longer. Any liability that is not current is considered to be long term. 2. An estimated […]

978-0078025600 Chapter 9 Lecture Note

Chapter 09 – Current Liabilities Chapter 09 Current Liabilities © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, […]

978-0078025600 Chapter 8 Solution Manual Part 3

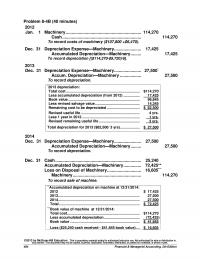

Financial & Managerial Accounting, 5th Edition 484 **Accumulated depreciation on machine at 12/31/2014: 2012 $ 17,425 2013 ……………………………………………………………………… 27,500 2014 ……………………………………………………………………… 27,500 Total …………………………………………………………………….. $ 72,425 ***Book value of machine at 12/31/2014: Total cost ……………………………………………………………… $114,270 Less accumulated depreciation …………………………..…. […]

978-0078025600 Chapter 8 Solution Manual Part 2

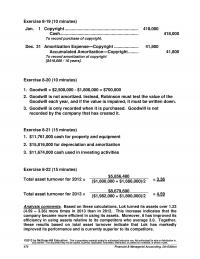

Financial & Managerial Accounting, 5th Edition 470 company became more efficient in using its assets. Moreover, it has improved its efficiency in using assets relative to its competitors who average 3.0. Together, these results based on total asset turnover indicate […]

978-0078025600 Chapter 8 Solution Manual Part 1

Chapter 8 Long-Term Assets QUESTIONS 1. A plant asset is tangible; it is used in the production or sale of other assets or services; and it has a useful life longer than one accounting period. 2. The cost of a […]

978-0078025600 Chapter 8 Lecture Note

Chapter 08 – Long-Term Assets Chapter 08 Long-Term Assets © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be copied, scanned, duplicated, […]

978-0078025600 Chapter 8 Excel

Student Name: Class: National Fargo Locust Bank Bank 1. May 19 Jul 8 Nov 28 90 120 60 Aug 17 Nov 5 Jan 27 Correct! Correct! Correct! 2. $35,000 $80,000 $42,000 10% 9% 8% 90/360 120/360 60/360 $875 $2,400 $560 […]

978-0078025600 Chapter 7 Solution Manual Part 3

Financial & Managerial Accounting, 5th Edition 444 Problem 7-5B (75 minutes) Part 1 2012 Nov. 1 Notes Receivable—S. Julian ………………………….. 4,800 Accounts Receivable—S. Julian …………………. 4,800 To record note received on account. Dec. 31 Interest Receivable ………………………………………….. 64 Interest Revenue […]

978-0078025600 Chapter 7 Solution Manual Part 2

Financial & Managerial Accounting, 5th Edition 432 PROBLEM SET A Problem 7-1A (30 minutes) June 4 Accounts Receivable—N. Morris ……………………….. 650 Sales …………………………………………………………… 650 To record sales on credit. 4 Cost of Goods Sold ………………………………………….…….. 400 Merchandise Inventory ……………………………….…….. 400 […]

978-0078025600 Chapter 7 Solution Manual Part 1

Chapter 7 Accounts and Notes Receivable QUESTIONS 1. When customers use credit cards, the selling companies can avoid having to directly evaluate the credit standing of their customers. They also avoid the risk of bad debts and often are paid […]

978-0078025600 Chapter 7 Lecture Note

Chapter 07 – Accounts and Notes Receivable Chapter 07 Accounts and Notes Receivable © 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not […]

978-0078025600 Chapter 7 Excel

Student Name: Class: Estimated Market Percent Apportioned Value of Total Cost Building $508,800 53% $477,000 «- Correct! Land 297,600 31% 279,000 «- Correct! Land Improvements 28,800 3% 27,000 «- Correct! Vehicles 124,800 13% 117,000 «- Correct! Totals $960,000 100% $900,000 […]

978-0078025600 Chapter 6 Solution Manual Part 3

Problem 6-5B (Concluded) Part 3 There are several possible reasons why some prenumbered checks are missing from the sequence of canceled checks returned with a bank statement. Reasons include: (1) Some of the checks in the numbered sequence may have […]

978-0078025600 Chapter 6 Solution Manual Part 2

Financial & Managerial Accounting, 5th Edition 392 Exercise 6-14B (Concluded) b. Recording inventory at net amounts Oct. 2 Merchandise Inventory …………………………………….….. 2,940 Accounts Payable ………………………………………….. 2,940 To record merchandise purchases less discount [$3,000 – ($3,000 x .02) = $2,940]. 10 […]

978-0078025600 Chapter 6 Solution Manual Part 1

Chapter 6 Cash and Internal Controls QUESTIONS 1. The seven broad principles are: Establish responsibilities; Maintain adequate records; Insure assets and bond key employees; Separate recordkeeping from custody of assets; Divide responsibilities for related transactions; Apply technology controls; Perform regular […]