Chapter 07 – Accounts and Notes Receivable

Chapter 07

Accounts and Notes Receivable

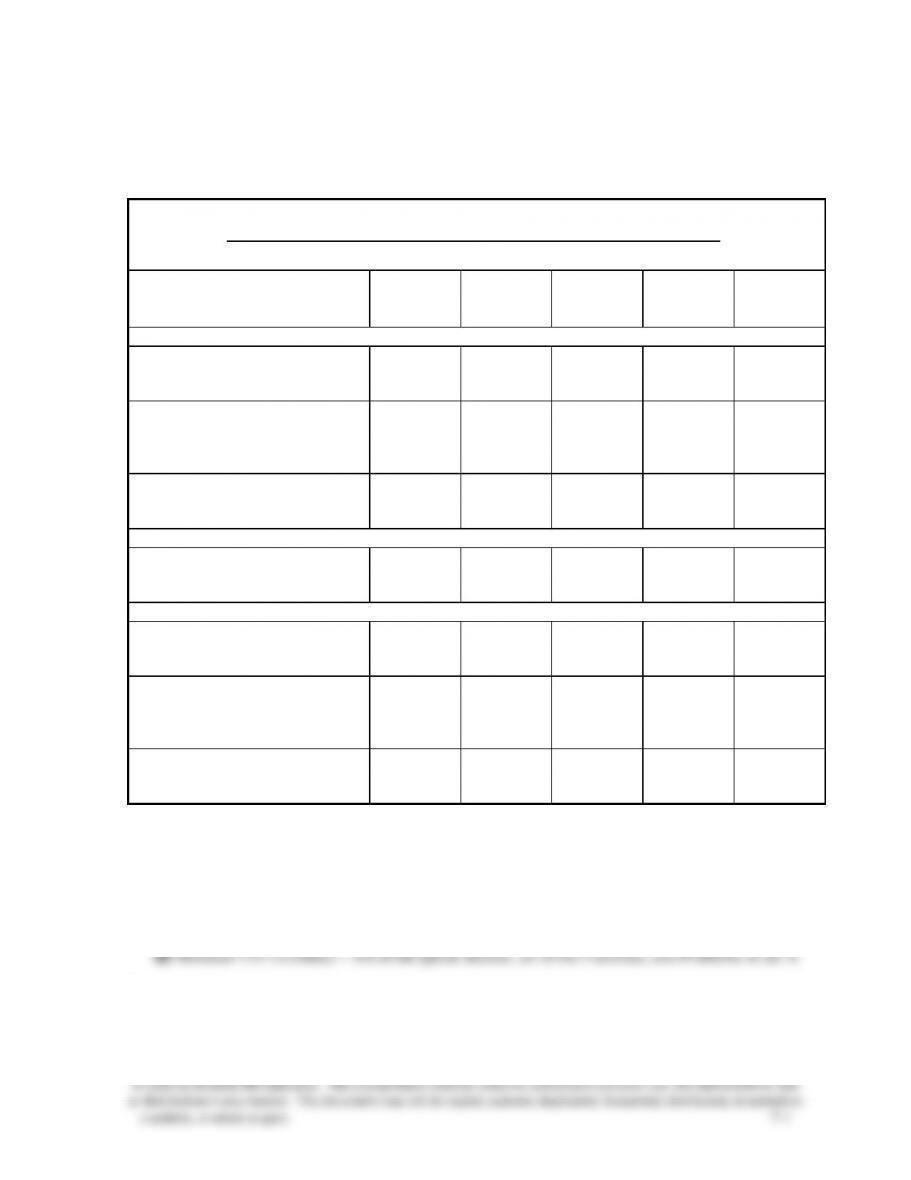

Student Learning Objectives and Related Assignment Materials*

Student Learning Objectives

Discussion

Questions

Quick

Studies

Exercises

Problems

(A &B set)**

Beyond the

Numbers

Conceptual objectives:

C1. Describe accounts receivable

and how they occur and are

recorded.

1, 7, 10

7-1, 7-12

7-1, 7-2

7-1, 7-2

TTN, ED,

HTR, GD

C2. Describe a note receivable,

computation of its maturity

date, and recording of its

existence.

6

7-5

7-13

7-5

C3. Explain how receivables

can be converted to cash before

maturity.

7-8

7-10

7-5

Analytical objectives:

A1 Compute accounts receivable

turnover and use it to help

assess financial condition.

7-11

7-15

RIA, CA

Procedural objectives:

P1. Apply the direct write-off

method to account for accounts

receivable.

2, 3, 5, 8

7-9, 7-10

7-3

P2. Apply the allowance method

and estimate uncollectibles

based on sales and on accounts

receivable.

4, 6, 9

7-2, 7-3, 7-4

7-4, 7-5, 7-6,

7-7, 7-8, 7-9,

7-16

7-2, 7-3, 7-4

CA, EC, CIP,

TIA, GD

P3. Record the honoring and

dishonoring of a note and

adjustments for interest.

7-6, 7-7

7-11, 7-12,

7-14

7-5

* Assignment materials that can be completed by students using:

Sage 50 and QuickBooks Pro 2013 templates – Problems 7-1A and

7-5A, and the Serial Problem for Success Systems, which covers numerous learning objectives.

(The serial problem, which began in chapter 1, continues in most of the chapters. Even if

previous segments were not assigned, students can begin the segment of the serial problem that

is included in this chapter.)

Excel templates – None.

.

Chapter 07 – Accounts and Notes Receivable

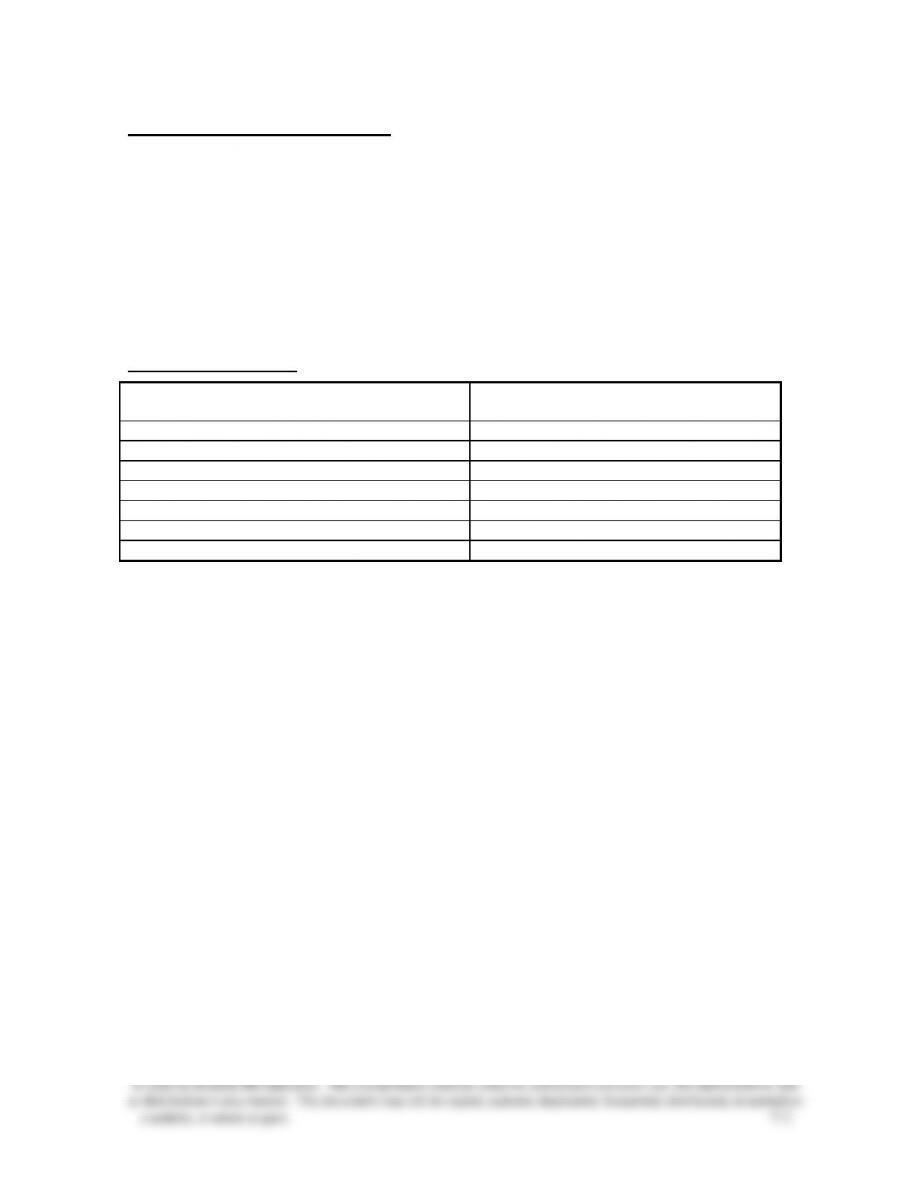

Synopsis of Chapter Revisions

• Under Armour: NEW opener with new entrepreneurial assignment

• Added explanation of credit card sales

• New discussion of mobile payment systems using mini-card-readers and iPads

• New illustration comparing bad debts recognition under the allowance method versus the

direct write-off method

• Revised exhibit on aging of accounts receivable, including all detailed accounts

• New illustration on why the banker’s rule is commonly applied

PowerPoint® Slides

Chapter Learning Objective

PowerPoint® Slides

C1

6-15

P1

16-19

P2

16,20-34

C2

35-40

P3

40-43

C3

44

A1

45

Chapter 07 – Accounts and Notes Receivable

Chapter Outline

Notes

I. Accounts Receivable

A receivable is an amount due from another party. Accounts

Receivable are amounts due from customers for credit sales.

A. Recognizing Accounts Receivable

Accounts Receivable occur from credit sales to customers.

1. Sales on Credit

Credit sales are recorded by increasing (debiting) Accounts

Receivable.

a. The General Ledger continues to keep a single Accounts

Receivable account.

b. A supplementary record, called the accounts receivable

ledger, is created to maintain a separate account for each

customer that tracks the balance of each customer.

c. The sum of the individual accounts in the accounts

receivable ledger equals the debit balance of the Accounts

Receivable account in the general ledger.

d. Entry to record credit sale: debit Accounts Receivable—

Customer Name, credit Sales. The debit is posted to the

Accounts Receivable account in the general ledger and to

the customer account in the accounts receivable ledger.

e. Many larger retailers maintain their own credit cards to

grant credit to preapproved customers and to earn interest

on unpaid balances. The entries are the same as in d.

above except for the possibility of added interest revenue;

entry to record interest: debit Interest Receivable, credit

Interest Revenue.

2. Credit Card Sales (examples: Visa, MasterCard, American

Express)

Sellers allow customers to use third-party credit and debit

cards for several reasons:

a. The seller does not have to evaluate each customer’s

credit standing.

b. The seller avoids the risk of extending credit to customers

who may not pay.

c. The seller typically receives cash from the credit card

company sooner than had it granted credit directly to

customers.

d. A variety of credit options for customers offers a potential

increase in sales volume.

e. Entry for credit card sales when cash is received upon

deposit of sales receipt: debit Cash (for the amount of sale

less the credit card charge), debit Credit Card Expense (for

Chapter 07 – Accounts and Notes Receivable

Chapter Outline

Notes

accounting period, bad debts expense is estimated and recorded

in an adjusting entry. Advantages include that it records bad debt

expense when the related sales are recorded and it reports

accounts receivable on the balance sheet at the estimated amount

of cash to be collected.

1. Recording bad debts expense. The allowance method

estimates bad debts expense at the end of the accounting

period and records it with an adjusting entry. Entry to record

estimate of bad debt expense: debit Bad Debts Expense,

credit Allowance for Doubtful Accounts, a contra-asset

account. (This contra account is used instead of Accounts

Receivable because, at the time of the adjusting entry, the

company does not know which customers will not pay.).

Realizable value is the expected proceeds from converting

an asset into cash; in the balance sheet, the Allowance for

Doubtful Accounts is subtracted from Accounts Receivable

to show the amount expected to be collected.

2. Writing off a bad debt. When a specific account is

identified as uncollectible, it is written off against the

Allowance for Doubtful Accounts. Entry to write off a bad

debt: debit Allowance for Doubtful Accounts, credit

Accounts Receivable. (Note that the write-off does not affect

the realizable value of accounts receivable.)

3. Recovering a bad debt. Recovering of a bad debt requires

two journal entries. The first entry is a reversal of the write-

to prepare an adjusting entry at the end of the accounting period.

The percent of sales method—also referred to as the income

statement method, uses income statement relations to estimate

bad debts.

1. Based on experience, company estimates what percentage of

credit sales will be uncollectible.

2. Bad debts expense is calculated as the estimated percentage

times sales for the period.

3. The amount calculated is the estimated bad debt expense for

the period; this amount is used in the adjusting entry. The

allowance account ending balance rarely equals the bad debt

expense because the allowance account was not likely to be

zero prior to adjustment.

Chapter 07 – Accounts and Notes Receivable

Chapter Outline

Notes

E. Estimating Bad Debts—Percent of Receivables Method—the

accounts receivable method uses balance sheet relations to

estimate bad debts.

1. Goal of the bad debts adjusting entry for these methods is to

make the Allowance for Doubtful Accounts balance equal to

the portion of accounts receivable that is estimated to be

uncollectible. The estimated balance for the allowance account

is obtained in one of two ways.

2. The percent of accounts receivables method assumes that a

given percentage of a company’s receivables is uncollectible.

F. Estimating Bad Debts—Aging of Receivables Method. The aging

of accounts receivable method uses both past and current

receivables information to estimate the allowance amount. See

Exhibit 7.11 for an example. Specifically:

1. Each receivable is classified by how long it is past its due date,

2. Experience is used to estimate the percent of each

uncollectible class (the longer an amount is past due, the more

likely it is to be uncollectible),

3. The percents are applied to each class and then totaled to get

the estimated balance in the Allowance for Doubtful

Accounts.

G. Estimating Bad Debts—Summary of Methods. Exhibit 7.13

summarizes the principles for all three estimation methods.

Percent of sales is focused on the income statement and matches

bad debts expense with sales. The accounts receivables methods

are balance sheet focused and report accounts receivable at

realizable value.

II. Notes Receivable

A promissory note is a written promise to pay a specified amount of

money (the principal of the note) usually with interest (the cost for

borrowing money) either on demand or at a definite future date.

Promissory notes are notes payable to the maker (person promising to

pay) and notes receivable to the payee (person to be paid). Sellers

sometimes ask for a note to replace an accounts receivable when a

customer requests an extension to pay their account.

A. Computing Maturity and Interest

1. The maturity date is the day the note must be repaid.

a. When the time of the note is expressed in days, its maturity

date is the specified number of days after the note’s date.

b. When months are used, the note matures and is payable in

Chapter 07 – Accounts and Notes Receivable

Chapter Outline

Notes

2. Interest Computation:

Principal of note times the annual interest rate times the time

expressed in years. Note that a year has 360 days for interest

computations (the banker’s rule).

B. Recognizing Notes Receivable: debit Notes Receivable for

principal or face amount of note; credit will vary (depends on

reason note is received). Note that interest is not recorded until

earned.

C. Valuing and Settling Notes

The principal and interest of a note are due on its maturity date.

1. Recording an Honored Note. The maker of the notes usually

honors the note and pays it in full; entry (by the payee) to

record: debit Cash, credit Notes Receivable, credit Interest

Revenue. When a note is dishonored, we remove it from Notes

Receivable and charge it back to an Account Receivable.

2. Recording a Dishonored Note. When the maker does not pay

at maturity, the note is dishonored; entry (by payee) to record:

debit Accounts Receivable (for the principal and interest due),

credit Note Receivable (for principal), credit Interest Revenue.

3. Recording End-of-Period Interest Adjustment. When notes

receivable are outstanding at the end of a period, any accrued

interest earned is computed and recorded. Entry (by payee) to

record: debit Interest Receivable, credit Interest Revenue.

4. Entry to record honoring of a note if interest has been accrued:

debit Cash (for full amount received), credit Interest

Receivable (amount previously accrued), credit Interest

Revenue (amount earned since accrual date), credit Notes

Receivable (face amount of note).

III. Disposing of Receivables

Companies can convert receivables to cash before they are due.

Reasons for this include the need for cash or a desire to not be

involved in collection activities.

A. Selling Receivables

A company can sell all or a portion of its receivables to a finance

company or a bank.

1. Buyer, called a factor, charges the seller a factoring fee and

then takes ownership of the receivables and receives cash

when come due.

2. Entry (by seller of receivables): debit Cash, debit Factoring

Fee Expense, credit Account Receivable.

Chapter 07 – Accounts and Notes Receivable

Chapter Outline

Notes

B. Pledging Receivables

A company can pledge its receivables and/or inventory as security

for a loan.

1. Borrower retains ownership of the receivables.

2. If borrower defaults on the loan, the lender has the right to be

paid from the cash receipts of collections on accounts

receivable.

3. The borrower’s financial statements must disclose the

pledging of the receivables.

IV. Global View

A. Recognition of Receivables – Both GAAP and IFRS have similar

asset criteria that apply to recognition of receivables. Both refer to

the realization principle and an earnings process. Under GAAP,

realization implies an arm’s-length transaction. Under IFRS

realization is applied in terms of reliable measurement and

likelihood of economic benefits. IFRS refers to risk transfer and

ownership reward.

B. Valuation of Receivables – Both GAAP and IFRS require that

receivables be reported net of estimated uncollectibles and both

systems require that the expense for estimated uncollectibles be

recorded in the same period when any revenues from those

receivables are recorded. Both systems require the allowance

method.

C. Disposition of Receivables – both GAAP and IFRS apply similar

rules in recording dispositions of receivables. Under GAAP,

companies disclose Bad Debts Expense as Provision for Bad Debts,

where provision refers to expense. Under IFRS, provision refers to a

liability whose amount or timing is uncertain.

V. Decision Analysis—Accounts Receivable Turnover

quality (refers to the likelihood of collection without loss) and

liquidity of accounts receivable; it indicates how often the average

accounts receivable balance was converted to cash during the year.

B. It is calculated by dividing net sales by average accounts

receivable.

C. A high turnover in comparison with competitors suggests that

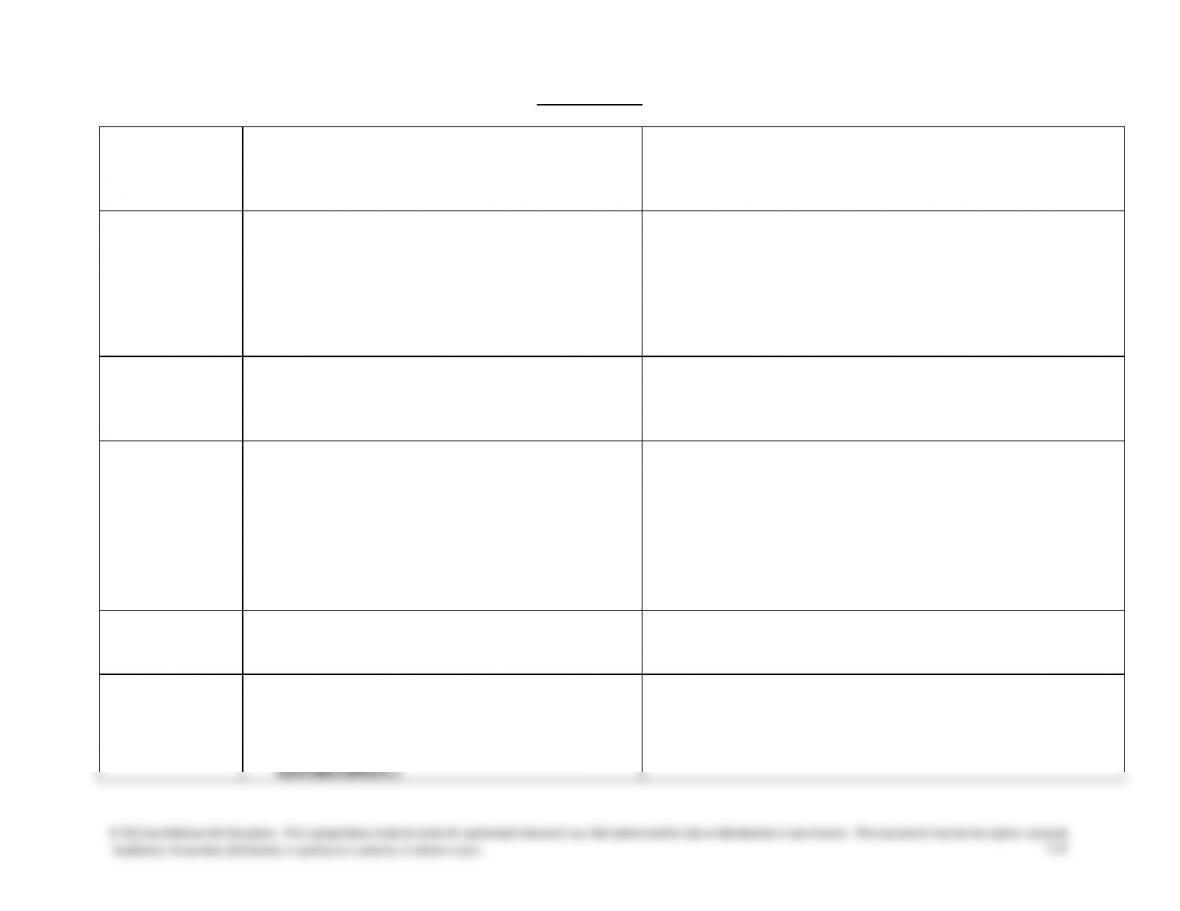

VISUAL #7-1

METHODS OF ACCOUNTING FOR BAD DEBTS

DIRECT WRITE-OFF METHOD

Bad debts expense is recorded at the time an

account is determined to be uncollectible.

ALLOWANCE METHOD

Bad debts expense is estimated and recorded

at the end of each accounting period.

Year–end

No adjusting entry

Adjusting entry required:

Bad Debt Expense XXX

Allowance for Uncollectible Accounts XXX

(The amount is an estimate based on a percentage of sales or a

percentage of outstanding accounts receivable. If the estimate is based

on sales, the full estimate is used in the adjusting entry. If the estimate

is based on accounts receivable the allowance account balance is

brought to the amount of the estimate.)

When an

account is

determined to

be uncollectible

Write-off entry required:

Bad Debts Expense XXX

Accounts Receivable/Customer XXX

(The amount is the balance of the uncollectible account.)

Write-off entry required:

Allowance for Uncollectible Accounts XXX

Accounts Receivable/Customer XXX

(The amount is the balance of the uncollectible account.)

When an

account

previously

written off is

recovered

1. Reinstate account by reversing write-off:

Accounts Receivable/Customer XXX

Bad Debts Expense XXX

(Amount is the account balance that was written off.)

2. Record collection on account normally:

Cash XXX

Accounts Receivable/Customer XXX

(Amount is the amount collected.)

1. Reinstate account by reversing write-off:

Accounts Receivable/Customer XXX

Allowance for Uncollectible Accounts XXX

(Amount is the account balance that was written off.)

2. Record collection on account normally:

Cash XXX

Accounts Receivable/Customer XXX

(Amount is the amount collected.)

Advantages:

• Does not require adjusting entry.

• Does not require year-end estimating of

uncollectibles.

• Matches expense against related revenues.

• Reports the net realizable accounts receivable on the

balance sheet (a more accurate reporting of assets).

Disadvantages:

• Violates matching, therefore only allowed

if qualified under materiality principle.

(May be used by a business that

anticipates an immaterial amount of

uncollectibles.)

• Requires adjusting entry.

• Requires year-end estimating of uncollectibles.

Chapter 07 – Accounts and Notes Receivable

7-10

VISUAL #7-2

PROMISSORY NOTE

(6) $2,000.00 April 15, 2013 (1)

Amount Date

For value received, I promise to pay to the order of

Plexi-Plus Supply Co. (2)

Tobay, New York

(7)

Two thousand and no/100 ——————-Dollars

on June 14, 2013 (3)

plus interest at the annual rate of 9 percent. (4)

Scott Cooke (5)

for Tobay Surfer Inc.

Chapter 07 – Accounts and Notes Receivable

website, in whole or part. 7-11

Chapter 7 – Alternate Demonstration Problem #1

At the end of the year, the M. I. Wright Company showed the following

selected account balances:

Sales (all on credit) ………………………………………………………………….$300,000

Accounts Receivable ………………………………………………………………. 800,000

Allowance for Doubtful Accounts …………………………………………….. 38,000

Required:

1. Assume the company estimates that 1% of all credit sales will not be

collected.

a. Prepare the proper journal entry to recognize the expense

involved.

b. Present the balances in Accounts Receivable and Allowance for

Doubtful Accounts as they would appear on the balance sheet.

Also show the net realizable Accounts Receivable.

2. Assume the company estimates that 5% of its accounts receivable

will never be collected.

a. Prepare the proper journal entry to recognize the expense

involved.

b. Present the balances in Accounts Receivable and Allowance for

Doubtful Accounts as they would appear on the balance sheet.

Also show the net r ealizable Accounts Receivable.

3. Under each of the two assumptions (described in #1 and #2 above),

prepare the proper journal entry for the following event.

June 3 John Shifty, who owes us $500, informs us that he is

broke and cannot pay. We believe him.

Chapter 07 – Accounts and Notes Receivable

website, in whole or part. 7-12

Solution: Chapter 7 – Alternate Demonstration Problem #1

1A. Bad Debts Expense …………………………………… 3,000

Allowance for Doubtful Accounts ………….. 3,000

($ 300,000 X 1 %)

1B. Accounts Receivable …………………………………$800,000

Less: Allowance for Doubtful Accounts …….. 41,000