Chapter 09 – Current Liabilities

Chapter 09

Current Liabilities

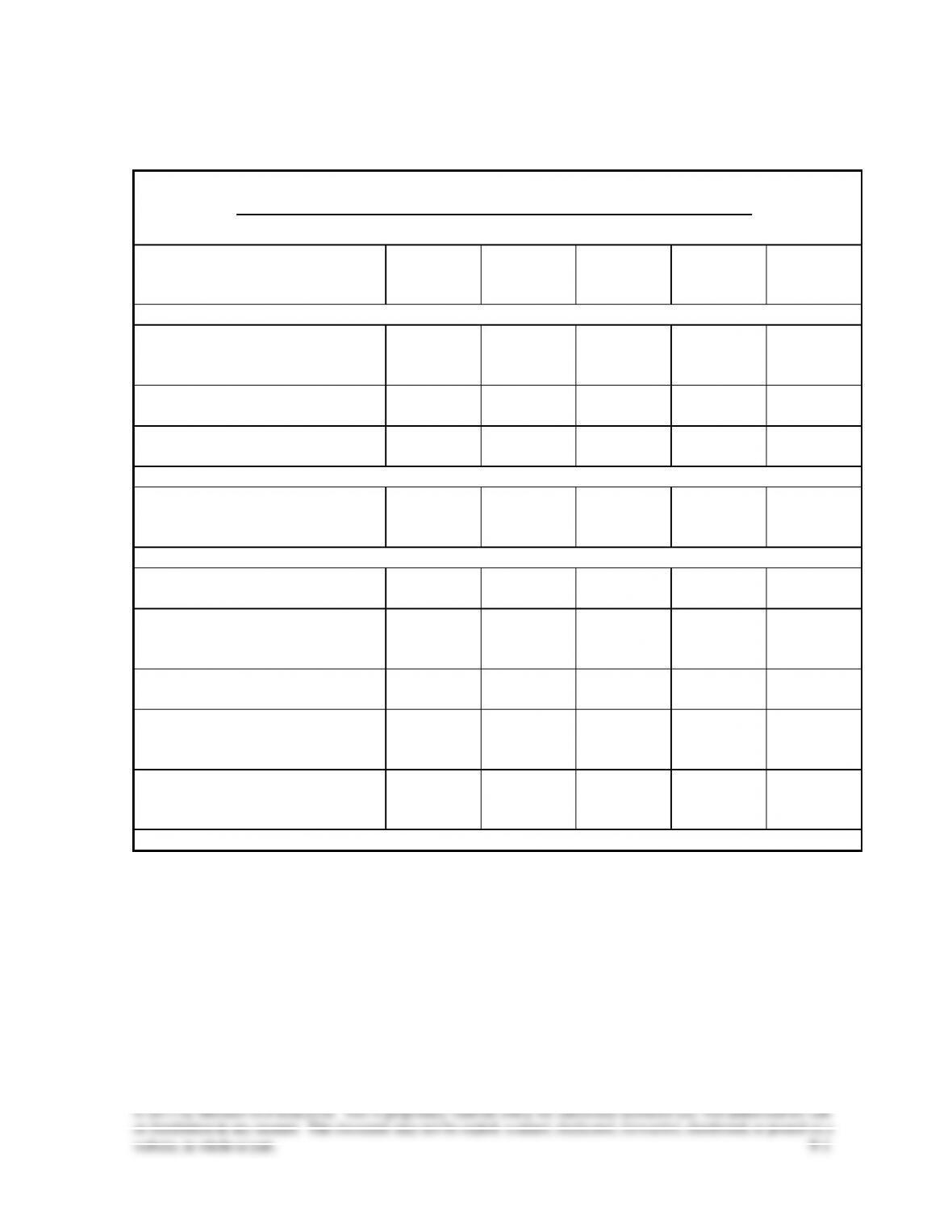

Student Learning Objectives and Related Assignment Materials*

Student Learning Objectives

Discussion

Questions

Quick

Studies

Exercises

Problems

(A &B set)**

Beyond the

Numbers

Conceptual objectives:

C1. Describe current and long-term

liabilities and their

characteristics.

1, 14

9-1, 9-14

9-1

TTN

C2. Identify and describe known

current liabilities.

15, 16, 17

9-2, 9-3,

9-4

9-2

TIA

C3. Explain how to account for

contingent liabilities.

1, 11

9-4

9-3

CIP

Analytical objectives:

A1. Compute the times interest

earned ratio and use it to

analyze liabilities.

9-11

9-12

9-5

RIA, CA,

TTN, ED,

GD

Procedural objectives:

P1. Prepare entries to account for

short-term notes payable.

9-5

9-4, 9-5

9-1

TIA

P2. Compute and record employee

payroll deductions and

liabilities.

5, 6, 7, 8

9-6

9-6, 9-7,

9-15, 9-16

9-2, 9-3, 9-6

HTR

P3. Compute and record employer

payroll expenses and liabilities.

5, 9

9-7

9-6, 9-8,

9-15, 9-16

9-2, 9-3, 9-6

P4. Account for estimated

liabilities, including warranties

and bonuses.

2, 3, 10

9-8, 9-9,

9-10, 9-13

9-9, 9-10,

9-11, 9-13,

9-18

9-4

RIA, EC

P5. Identify and describe the details

of payroll reports, records, and

procedures. (Appendix 9A)

12, 13

9-12

9-14, 9-17

9-6

Notes appear on next page.

Chapter 09 – Current Liabilities

* Assignment materials that can be completed by students using:

Sage 50 and QuickBooks Pro 2013 templates – Problems 9-1A and

9-4A, and the Comprehensive Problem for Bug-Off Exterminators, which covers various

learning objectives in chapters 1 through 9.

Excel template – Problem 9-1A and 9-2A.

** The Serial Problem for Success Systems, which covers numerous learning objectives, can be

most of the chapters. Even if previous segments were not assigned, students can begin the segment

of the serial problem that is included in this chapter. It is most readily solved if students use the

Working Papers that accompany the book.)

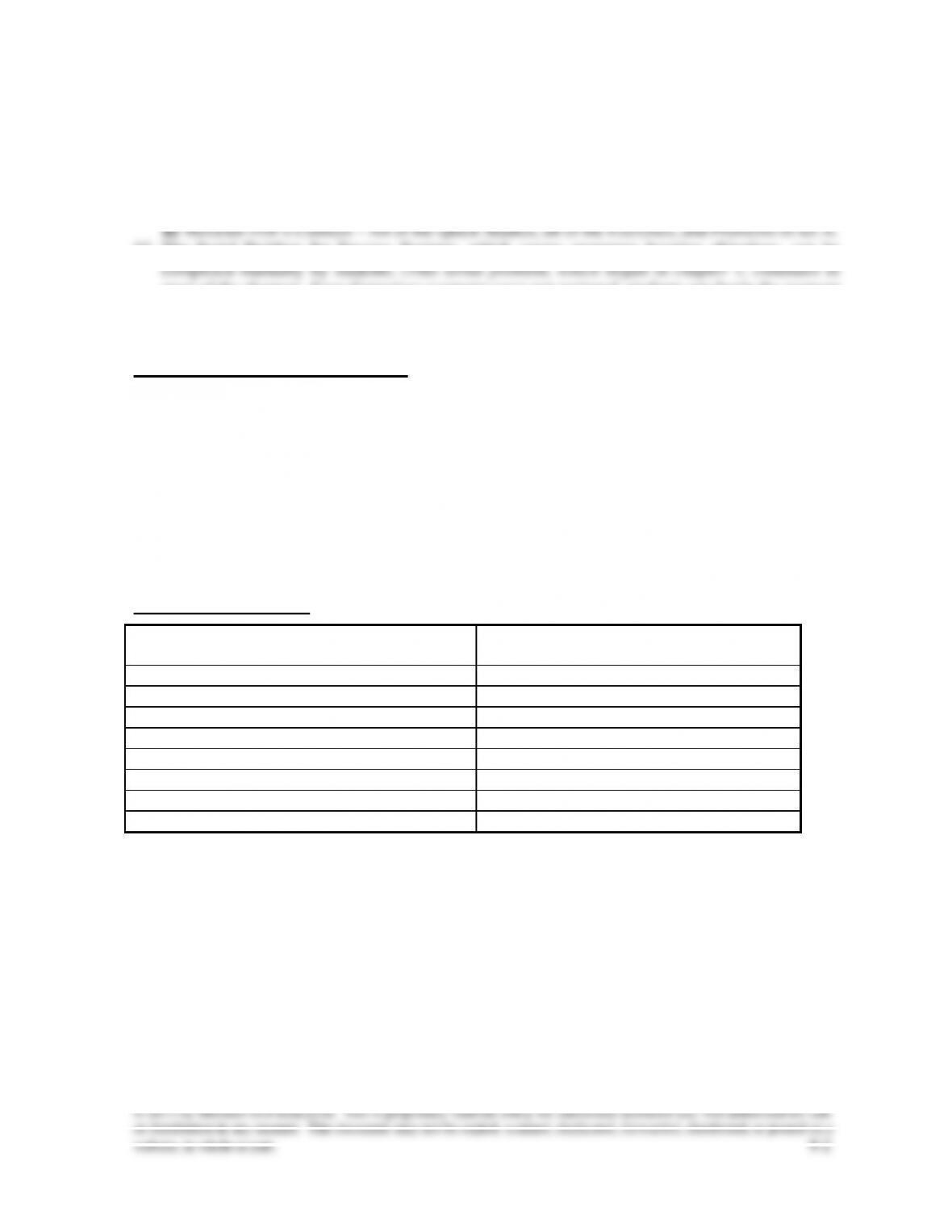

Synopsis of Chapter Revisions

• SmartIT Staffing: NEW opener with new entrepreneurial assignment

• Revised unearned revenues example based on Rihanna ticket sales

• Added explanation on the role of sellers as tax collection ‘agents’ for the government

• New information on franchise costs and how they are accounted for

• Added select formulas to enhance the exhibit on payroll deductions

• Updated payroll rates to 2012 with discussion on likely adjustments for 2013 and 2014

• Added discussion on maximum withholding allowances claimed

• New discussion on IRS actions against companies that fail to pay employment taxes

• New evidence on payroll fraud, its median loss, and time taken to uncover such frauds

PowerPoint® Slides

Chapter Learning Objective

PowerPoint® Slides

C1

6-8

C2

9-11

P1

12-20

P2

21-26

P3

27-29

C3

30,38-40

P4

31-37

A1

41

Chapter 09 – Current Liabilities

Chapter Outline

Notes

I. Characteristics of Liabilities

A. Defining Liabilities

A liability is a probable future payment of assets or services that a

company is presently obligated to make as a result of past

transactions or events. Note three crucial factors:

1. Past transaction or event.

2. Present obligation.

3. Future payment of assets or services.

B. Classifying Liabilities

1. Current liabilities (also called short-term liabilities)—

Obligations due within one year or the company’s operating

cycle, whichever is longer.

2. Long-term liabilities—Obligations not expected to be paid

within the longer of one year or the company’s operating

cycle.

C. Uncertainty in Liabilities—answers to the following questions are

often decided when a liability is incurred; however, one or more

may be uncertain for some liabilities:

1. Whom to pay?

2. When to pay?

3. How much to pay?

II. Known Liabilities—Set by agreements, contracts, or laws and are

measurable. Examples of these liabilities in the current classification

include:

A. Accounts Payable

Amounts owed to suppliers, also called vendors, for products or

services purchased with credit; also known as trade accounts

payable.

B. Sales Taxes Payable

Amounts the seller has collected as sales taxes from customers

when sales occur, which have not yet been remitted to the proper

governmental agency.

1. Entry (by seller) to record cash sale subject to sales tax: debit

Cash, credit Sales, credit Sales Taxes Payable.

2. Entry (by seller) when sales taxes are remitted: debit Sales

Tax Payable, credit Cash.

Chapter 09 – Current Liabilities

Chapter Outline

Notes

C. Unearned Revenues

Amounts received in advance from customers for future products

or services; also known as deferred revenues, collections in

advance and prepayments.

1. Entry to record receipt of amounts in advance for future

products or services: debit Cash, credit Unearned Revenue.

2. Entry to record revenue for that portion earned: debit

Unearned Revenue, credit Revenue.

D. Short-Term Notes Payable

Written promise to pay a specified amount on a definite future

date within one year or the company’s operating cycle, whichever

is longer. Can arise from many transactions; two common

examples:

1. Note given to extend credit period; interest-bearing note is

substituted for an overdue account payable.

a. Entry to record partial payment on account and

substitution of note payable for overdue amount: debit

Accounts Payable, credit Cash, credit Notes Payable.

b. Entry to record payment when note becomes due: debit

Note Payable, debit Interest Expense, credit Cash.

2. Note given to borrow from bank

Entries (by borrower) to record:

a. Receipt of cash when note is signed: debit Cash, credit

Note Payable.

b. Payment of principal and interest: debit Note Payable,

debit Interest Expense, credit Cash.

c. Accrual of interest when notes payable are outstanding at

the end of a period: debit Interest Expense, credit Interest

Payable.

d. Payment of note when interest has been accrued: debit

Interest Expense (amount incurred since accrual date),

debit Interest Payable (amount previously accrued), debit

Notes Payable, credit Cash (for full amount paid).

E. Payroll Liabilities

An employer incurs several expenses and liabilities from salaries

and wages earned, from employee benefits, and from payroll taxes

levied on the employer.

1. Gross pay—total compensation an employee earns

(includes wages, salaries, commissions, bonuses).

2. Net pay—gross pay less all deductions; also called take-

home pay.

Chapter 09 – Current Liabilities

Chapter Outline

Notes

3. Employee Payroll Deductions—amounts withheld from an

employee’s gross pay, either required or voluntary; commonly

called withholdings. The employer withholds payroll

deductions from employees’ pay and is obligated to remit to

the designated organizations.

a. Employee FICA taxes (Social Security and Medicare

taxes) equal current rate times gross wages subject to tax.

(For year 2005, Social Security tax is 6.2% of the first

$90,000 earned by the employee in the calendar year and

Medicare tax is 1.45% of all amounts earned by the

employee).

b. Employee income tax withholding is determined from

tables published by the IRS based on employee’s annual

earnings rate and the number of withholding allowances

claimed.

c. Employee voluntary deductions (charitable contributions,

medical insurance premiums, pension contributions, and

union dues) are withheld and reported as part of the

employer’s current liabilities until paid.

4. Illustrative entry (by employer) to accrue payroll expenses and

liabilities: debit Salaries Expense, credit FICA-Social

Securities Taxes Payable, credit FICA-Medicare Taxes

Payable, credit Employee Federal Income Taxes Payable,

credit Employee Medical Insurance Payable, credit Employee

Union Dues Payable, credit Salaries Payable (for the amount

of the net pay).

5. Employer Payroll Taxes are recorded as expenses and

current liabilities. Employer taxes include:

a. Employer FICA taxes—employers must pay FICA taxes

equal in amount to the FICA taxes withheld from their

employees.

b. Federal and state unemployment taxes—Employers must

pay a federal unemployment tax on wages and salaries

paid to their employees. (For year 2008, employers were

required to pay FUTA taxes of as much as 6.2% on the

first $7,000 earned by each employee; this tax can be

reduced by a credit of up to 5.4% for taxes paid to a state

program.) All states place a payroll tax for unemployment

insurance on employers; the amounts vary.

Chapter 09 – Current Liabilities

Chapter Outline

Notes

c. Illustrative entry (by employer) to record payroll tax

expense and related liabilities: debit Payroll Tax Expense,

credit FICA-Social Securities Taxes Payable, credit FICA-

Medicare Taxes Payable, credit State Unemployment

Taxes Payable, credit Federal Unemployment Taxes

Payable.

F. Multi-Period Known Liabilities—often include unearned revenues

and notes payable that extend over multiple periods.

III. Estimated Liabilities—Known obligations of uncertain amounts that

can be reasonably estimated. Examples are:

A. Health and Pension Benefits

1. Employers often pay all or part of medical, dental, life, and

disability insurance, and many employers also contribute to

pension plans.

2. Illustrative entry to record these benefits: debit Employee

Benefits Expense, credit Employee Medical Insurance

Payable, credit Retirement Program Payable.

B. Vacation Benefits—Estimated and recorded by the employer

during the weeks the employees are working and earning the

vacation time.

1. Many employers offer paid vacations.

2. Entry to record: debit Vacation Benefits Expense, credit

Vacation Benefits Payable. When employees take

vacation, employer reduces (debits) the Vacation Benefits

Payable and credits Cash.

C. Bonus Plans

1. Many companies offer bonuses to employees; many bonuses

depend on net income.

2. The related expense and liability are recorded in a year-end

adjusting entry.

D. Warranty Liabilities

1. A warranty is a seller’s obligation to replace or correct a

product (or service) that fails to perform as expected within a

specified period.

2. To comply with the full disclosure and matching principles,

the seller reports the expected warranty expense in the period

when revenue from the sale of the product or service is

reported. The warranty obligation is reported as a liability

even though the amount, payee, and date are uncertain. The

costs are probably and the amount can be estimated based on

past experience.

E. Multi-Period Estimated Liabilities

payment will be made.

Chapter 09 – Current Liabilities

website, in whole or part. 9-7

Chapter Outline

Notes

IV. Contingent Liabilities—Potential obligation that depends on a future

event arising from past transactions.

A. Accounting for Contingent Liabilities – depends on the likelihood

that a future event will occur and the ability to estimate the future

amount owed if this event occurs. Three categories of contingent

liabilities:

1. Future event is probable and the amount can be reasonably

estimated. Record as a liability.

2. Future event is remote. Do not record or disclose in notes.

3. Future event is reasonably possible. Disclose in notes.

B. Reasonably Possible Contingent Liabilities – Examples:

1. Potential legal claims—recorded in the accounts only if

payment for damages is probable and the amount can be

reasonably estimated; if can’t be reasonably estimated or is

less than probable but reasonably possible, disclose in notes.

2. Debt guarantees (of a debt owed by another company)—

require disclosure if potential liabilities are reasonably

possible.

3. Other contingencies (e.g., environmental damages, possible

tax assessments, insurance losses, and government

investigations)—require disclosure if potential liabilities are

reasonably possible.

4. Uncertainties that are Not Contingencies – are not contingent

liabilities because they are future events not arising from past

transactions. They are not disclosed.

V. Global View

A. Characteristics of Liabilities – the definitions of current liabilities

are similar for both GAAP and IFRS. “Provision” is typically used

companies to record current liabilities in a similar manner.

treatment.

B. It is calculated by dividing income before interest expense and

income taxes by interest expense.

VII. Payroll Reports, Records, and Procedures (Appendix 9A)

A. Payroll Reports—employers are required to prepare and submit

the following reports:

Chapter 09 – Current Liabilities

Chapter Outline

Notes

1. Reporting FICA and Income Taxes. Employer’s Quarterly

Federal Tax Return (IRS Form 941)

Filed within one month after the end of each calendar quarter

to report FICA and income withholding taxes owed and

remitted.

2. Reporting FUTA and SUTA Taxes. Annual Federal

Unemployment Tax Return (IRS Form 940)

Must be mailed on or before January 31 following the end of

each tax year to report an employer’s FUTA taxes.

3. Reporting Wages and Salaries. Wage and Tax Statement

(Form W-2) must be given to employees on or before January

31 following the year covered by the report; employers must

give each employee an annual report of the employee’s wages

subject to FICA and federal income taxes and the amounts of

these taxes withheld.

B. Payroll Records

1. Payroll Register

A record for a pay period that shows the pay period dates and

the hours worked, gross pay, deductions, and net pay of each

employee; contains all the data needed to record payroll (for

each pay period) in the General Journal.

2. Payroll Check

Generally accompanied with a detachable statement of

earnings showing gross pay, deductions, and net pay.

3. Employee’s Earnings Report.

A record of an employee’s hours worked, gross earnings,

deductions, net pay, and certain personal information about

the employee; contains the data the employer needs to prepare

a Form W-2.

C. Payroll Procedures

1. Computing Federal Income Taxes

Computed using a wage bracket withholding table based on

gross pay, number of personal exemptions, the employee’s tax

status, and pay period.

a. Withholding allowance—a number that is used to reduce

the amount of federal income tax withheld from an

employee’s pay, and which corresponds to the personal

exemptions the employee is allowed to subtract from

annual earnings in calculating taxable income.

b. Form W-4—withholding allowance certificate form. Filed

by employee with employer to identify personal

exemptions claimed.

2. Payroll Bank Account

A separate payroll bank account is used in a company with

many employees.

Chapter 09 – Current Liabilities

Chapter Outline

Notes

a. One check for total payroll is drawn on the regular bank

account or an electronic funds transfer for this amount is

executed to provide deposit for the payroll bank account.

b. Individual payroll checks are drawn on payroll account.

c. Helps with internal control and reconciling the regular

bank account.

3. Who Pays What Payroll Taxes and Benefits—who pays which

employee benefits and what portion, is subject to agreements

between companies and their workers. Self-employed

workers must pay both the employer and employee FICA

taxes for social security and Medicare.

VIII. Corporate Income Taxes (Appendix 9B)

A. Income Tax Liabilities

1. Corporations (but not sole proprietorships or partnerships) are

subject to income taxes and must estimate their tax liability

when preparing financial statements.

2. Entry to record estimated income tax liability: debit Income

Taxes Expense, credit Income Taxes Payable.

B. Deferred Income Tax Liabilities

1. Income tax laws and GAAP are different.

2. Temporary differences arise when the tax return and the

income statement report a revenue or expense in different

years. When temporary differences exist, corporations

compute income taxes expense on the income reported on the

income statement; the result is that the income taxes expense

is different from the amount payable to the government; this

difference is the deferred income tax liability.

3. Entry to record estimated income tax liability when there are

temporary differences: debit Income Taxes Expense, credit

Income Taxes Payable, credit Deferred Income Tax Liability

4. Temporary differences can also cause corporations to pay

income taxes before they are reported on the income statement

Chapter 09 – Current Liabilities

website, in whole or part. 9-10

Chapter 9 – Alternate Demonstration Problem #1

On November l, 2013, Orleaon Co. borrowed $200,000 for 90 days at 9%

by signing a note.

Required:

1. Assume that the face value of the note is equal to the principal of

the loan. Prepare the general journal entries to record issuing the

note, accrual of interest at the end of 2013 and the payment of the

note at maturity.

2. Assume that the face value of the note ($204,500) includes both the

principal of the loan and the interest to be paid at maturity. Prepare

the general journal entries to record issuing the note, accrual of

interest at the end of 2013 and the payment of the note at maturity.

Chapter 09 – Current Liabilities

Solution: Chapter 9 – Alternate Demonstration Problem #1

1.

Issuance:

11/1/13

Cash …………………………………………

200,000

Notes Payable ……………………..

200,000

Year end accrual:

12/31/13

Interest Expense ……………………….

3,000

Interest Payable …………………..

3,000

($200,000 X 9% X 60/360 = $ 3,000)

Maturity date:

1/30/14

Notes Payable …………………………..

200,000

Interest Expense ……………………….

1,500

Interest Payable ………………………..

3,000

Cash ……………………………………

204,500

2.

Issuance:

11/1/13

Cash …………………………………………

200,000

Discount on Notes Payable ……….

4,500

Notes Payable ……………………..

204,500

Year end accrual:

12/31/13

Interest Expense ……………………….

3,000

Discount on Notes Payable. …

3,000

($200,000 X 9% X 60/360 = $3,000)

Maturity date:

1/30/14

Notes Payable …………………………..

204,500

Cash ……………………………………

204,500

1/30/14

Interest Expense ……………………….

1,500

Discount on Notes Payable ….

1,500