Problem 6-5B (Concluded)

Part 3

There are several possible reasons why some prenumbered checks are

missing from the sequence of canceled checks returned with a bank

statement. Reasons include:

(1) Some of the checks in the numbered sequence may have cleared the

error, it will return the check separately with a note of explanation to

the depositor.

Financial & Managerial Accounting, 5th Edition

406

SERIAL PROBLEM — SP 6

Serial Problem — SP 6, Success Systems (50 minutes)

Part 1

SUCCESS SYSTEMS

Bank Reconciliation

March 31, 2014

Bank statement balance ………...

$77,354

Book balance …………………………….…………………………

$77,845

Add

Add

Bank error ………………………………...

Deposits in Transit …………………..

500

0

Bank interest …………………………..

33

______

77,854

77,878

Deduct

Deduct

Outstanding Check…………………

128

Safety deposit rental ….. $ 50

______

Charge for checks………. 102

152

Adjusted bank balance …………..

$77,726

Adjusted book balance …………………………..

$77,726

Part 2

Mar. 25

Miscellaneous Expenses …………………………….……….

677

50

Cash ……………………………………………………....

101

50

To record safety deposit box rental.

26

Miscellaneous Expenses …………………………….……….

677

102

Cash ……………………………………………………....

101

102

To record charge for printing checks

31

Cash …………………………………………………………..……….

101

33

Interest Revenue …………………………………..……….

404

33

To record interest earned.

Reporting in Action — BTN 6-1

1.

($ in thousands)

Balance

December

31, 2011

Cash and

equivalents

as % of:

Balance

December

31, 2010

Cash and

equivalents

as % of:

Cash and cash

equivalents ……………

$ 325,336

—

$ 393,927

—

Current assets ………..

878,676

37.0%

808,145

48.7%

Current liabilities …….

615,531

52.9

584,210

67.4

Stockholders’ equity .

500,056

65.1

370,991

106.2

Total assets …………….

1,228,024

26.5

1,061,647

37.1

Analysis comment: Cash and cash equivalents have decreased as a

percent of the various bases over this period. Looking just at this

measure, it is probably safe to say that Polaris’s liquidity position has

slighty deteriorated.

2. Per the statement of cash flows for year ended December 31, 2011

($ thousands):

Cash and equivalents, beginning-year …………. $393,927

Reporting in Action (Concluded)

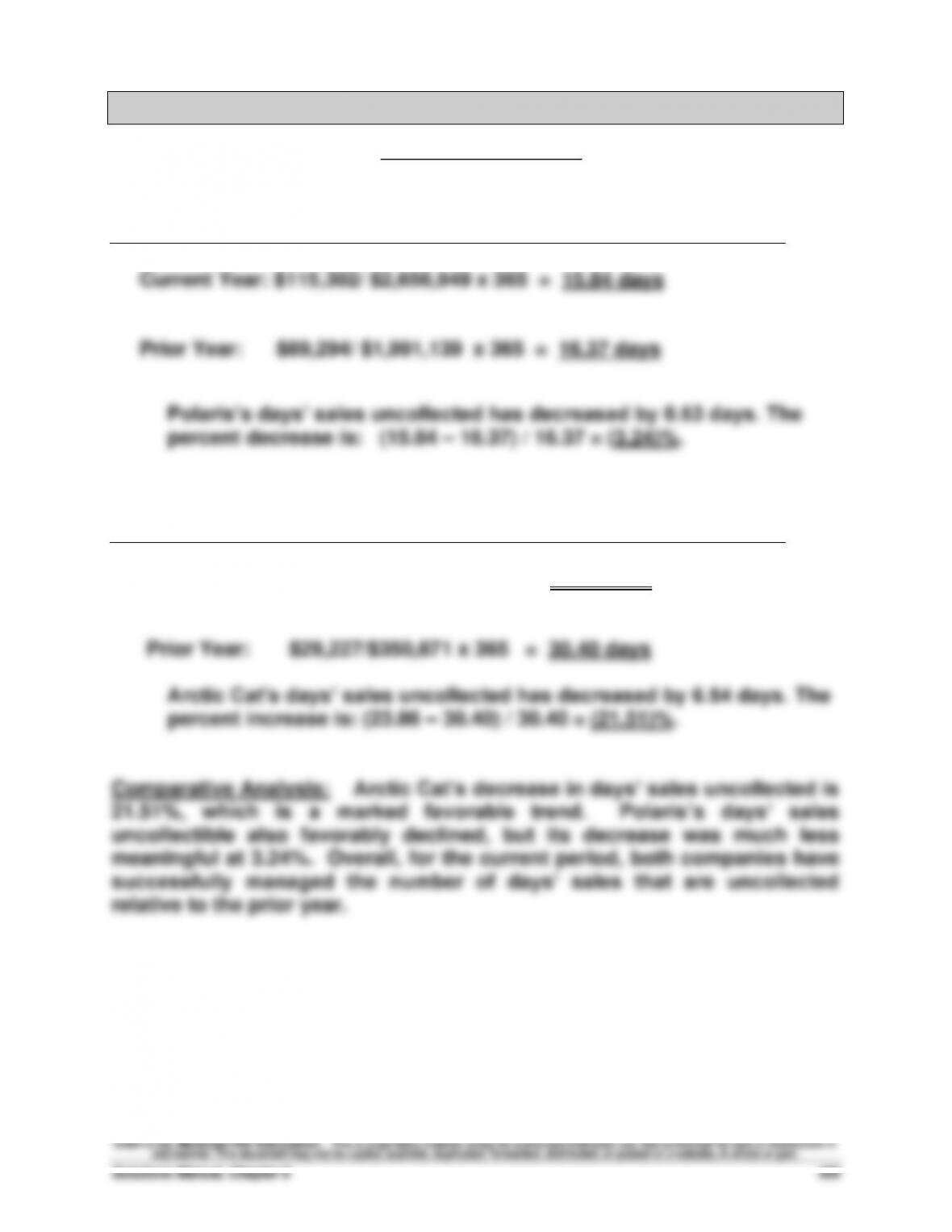

3. Days’ Sales Uncollected ($ thousands)

Days’ sales uncollected = x 365

total assets. Polaris’s receivables are historically low because much of

their sales are made to an intermediary finance company that extends

longer-term credit to their end customers.

4. Solution depends on the annual report information obtained.

Accounts receivable

Net sales

Comparative Analysis — BTN 6-2

Days’ sales uncollected = x 365

Polaris ($ thousands)

Arctic Cat ($ millions)

Current Year: $23,732/$363,015 x 365 = 23.86 days

Accounts receivable

Net sales

Ethics Challenge — BTN 6-3

1. In a small business office it is very important that the owner of the

2. Unfortunately, due to collusion of the employees, the bank

3. Despite the collusion, the scheme is not foolproof. For example, some

ways in which the scheme might be uncovered or prevented include the

following:

• A bank employee may become suspicious and call Dr. Conrad and

4. Dr. Conrad should review her salary schedules for employees to make

sure that she is at least offering market pay. She may want to consider

bonding her employees to insure herself against material losses. Dr.

Communicating in Practice — BTN 6-4B

Memorandum

To: “Owner”

From: “Consultant”

Date: __________

Subject: Advice on monitoring purchase discounts

[Instructor’s Note: The response should acknowledge the owner’s concern and

recommend the net method of recording purchases. It should explain how this method

results in the recording of “Discounts Lost,” which will flow through to the income

statement, thus providing the information desired. The memo might look something like

the following.]

The net method gives management an advantage in controlling and

monitoring purchase discounts. When invoices are recorded at gross

amounts, the amount of discounts taken is deducted from the balance of

the Merchandise Inventory account.

This means that the amount of any discounts lost is not reported in any

account or on the income statement. Consequently, discounts lost are

unlikely to come to the attention of management. However, when

purchases are recorded at net amounts, a discounts lost expense is

brought to management’s attention as an operating expense on the income

statement. Management can then seek to identify the reason for discounts

lost, such as oversight, carelessness, or unfavorable terms.

This practice gives management better control over persons responsible

for paying bills on time to take advantage of favorable discounts. This also

means it’s less likely that favorable discounts are lost.

Taking It to the Net — BTN 6-5

[Instructor Note: These answers were taken from the 2010 Report to the Nation.]

1. The median loss caused by occupational frauds was $160,000.

2. Nearly one-quarter of fraud cases involved losses of at least $1 million

in losses.

3. Companies lose 5% of their annual revenues to fraud; this 5% figure

translates to a potential total fraud loss of more than $2.9 trillion.

4. The typical length of fraud schemes was 18 months from the time the

fraud began until it was detected.

5. Less than 30% of victim organizations conducted surprise audits,

6. Asset misappropriation schemes were most common at 90% of cases

with a median loss of $135,000.

7. Financial statement fraud schemes made up less than 5% of cases with

a median loss of more than $4 million.

8. Corruption schemes comprised 33% of cases with a median loss of

$250,000.

9. Less than 15% of the perpetrators had convictions prior to committing

their frauds.

Teamwork in Action — BTN 6-6

Common internal controls visible in a typical retail store include:

1. Door locks and roll–down screens for after-hours lock-up.

2. Electronic detection devices stationed at entrances or anti-theft

3. Security cameras.

4. Security guards.

5. Cash registers.

6. Separate cash drawers or transaction codes to identify clerks at

registers.

7. Bar coding on merchandise.

8. Limited number of apparel items allowed in a dressing room.

9. Dressing room attendants.

10. A security safe on the premises.

11. Timeclocks.

Entrepreneurial Decision — BTN 6-7

1. Seven principles of internal control along with examples are:

a. Establish responsibilities. The clerks at the counter should be

responsible for handling cash. The other employees should be

responsible for preparing the orders and helping customers. There

also should be employees assigned responsibilities such as

procedures. Other records should include those for inventories,

supplies, payroll time records, and so on.

c. Insure assets and bond key employees. The owner should acquire

insurance for the employees and the physical facilities. Insurance

should also be acquired for potential casualties such as a

e. Divide responsibility for related transactions. The employee

responsible for ordering inventory should be separate from the

employee controlling inventory who should also be separate from

the employee who pays for inventory.

f. Apply technological controls. The owner should invest in

2. As the business grows, controls will become more important. The

owner will have more employees and will have to delegate more

Hitting the Road — BTN 6-8

No formal solution exists for this activity. It is usually interesting for the

1. Door locks and roll–down screens for after-hours lock-up.

2. Electronic detection devices stationed at entrances or anti-theft devices

on merchandise that must be removed by a cashier.

3. Security cameras.

4. Security guards.

5. Cash registers.

6. Bar coding on products and assets.

7. A security safe on the premises.

Global Decision — BTN 6-9

1.

(EUR thousands)

Current

year

balance

Cash as

percent

of:

Prior

year

balance

Cash as

percent

of:

Cash (and equivalents) …………

151,887

—

154,859

—

Current assets …………..………

509,708

29.8%

575,897

26.9%

Total assets ……………….………

1,520,184

10.0

1,545,722

10.0

Current liabilities ……….………

644,277

23.6

616,166

25.1

Shareholders’ equity ….………

446,218

34.0

442,890

35.0

Analysis comment: Cash has increased as a percent of current assets

compared to the prior year. Cash has decreased as a percent of current

liabilities and stockholders’ equity as compared to the prior year. Cash

as a percent of total assets has remained constant compared to the

prior year. All changes were nominal and suggest that Piaggio’s

liquidity (cash) position has not changed drastically from the prior year.

Global Decision (Concluded)

2. Cash, beginning-year (EUR thousands)……………………………………. 154,859

3. Days’ Sales Uncollected Formula (EUR thousands)

Current Year: x 365 = 15.8 days

Prior year: x 365 = 22.2 days

The number of days of uncollected sales in accounts receivable has

Accounts receivable

65,560

1,516,463

90,421

1,485,351