Financial & Managerial Accounting, 5th Edition

392

Exercise 6-14B (Concluded)

b.

Recording inventory at net amounts

Oct. 2

Merchandise Inventory …………………………………….…..

2,940

Accounts Payable …………………………………………..

2,940

To record merchandise purchases less

discount [$3,000 – ($3,000 x .02) = $2,940].

10

Accounts Payable ………………………………………………..

490

Merchandise Inventory ……………………………….…..

490

To record credit memo for returns

[$500 – ($500 x .02)].

*13

Discounts Lost ………………………………………………..…..

50

Accounts Payable …………………………………………..

50

To record the discount lost [($3,000 – $500) x.02].

17

Merchandise Inventory …………………………………….…..

5,292

Accounts Payable …………………………………………..

5,292

To record merchandise purchases less

discount [$5,400 – ($5,400 x .02) = $5,292].

26

Accounts Payable ………………………………………………..

5,292

Cash ………………………………………………………….…..

5,292

To record payment for merchandise.

31

Accounts Payable ………………………………………………..

2,500

Cash ………………………………………………………….…..

2,500

To record payment for merchandise less returns

($2,940 – $490 + $50).

* This entry could alternatively be recorded on October 31 when the cash payment is

made (this is likely because it is stated that invoice was mistakenly filed for

payment on October 31 and, thus, would probably not be known as of October 13).

PROBLEM SET A

Problem 6-1A (20 minutes)

1. Violates separation of duties. The company should implement a policy

2. Violates the principle of establishing responsibility. Only Julia should

3. Violates the proper application of technological controls. While the

4. Violates regular and independent review. Benedict Shales needs to

5. Violates the insuring of assets and the bonding of key employees. We

do not have enough information to know if the company can afford the

Financial & Managerial Accounting, 5th Edition

394

Problem 6-2A (30 minutes)

Part 1

Feb. 2

Petty Cash ……………………………………………………….

400

Cash …………………………………………………….…

400

To establish the $400 petty cash fund.

Part 2

Nakashima Gallery

Petty Cash Payments Report (for February)

Delivery expense

Feb. 23

Delivery of customer’s merchandise ………..…………..

$ 20.00

Mileage expense

Feb. 14

Reimbursement for mileage ……………………..……

68.00

Postage expense

Feb. 12

Express delivery of contract …………………….…….

$ 7.95

Feb. 27

Purchased postage stamps ……………………..……

54.00

61.95

Merchandise inventory (transportation-in)*

Feb. 9

COD charges on purchases ……………………..……

32.50

Feb. 25

COD charges on purchases ……………………..……

13.10

45.60

Office supplies expense

Feb. 5

Purchased paper for copier ……………………..……

14.15

Feb. 20

Purchased stationery ……………………………….…………..

67.77

81.92

Total

$277.47

* Transportation-in costs are included in Merchandise Inventory under a perpetual system.

Part 3

Feb. 28

Delivery Expense ……………………………………….………..

20.00

Mileage Expense ………………………………………..………..

68.00

Postage Expense ……………………………………….………..

61.95

Merchandise Inventory ……………………………….………..

45.60

Office Supplies Expense …………………………….………..

81.92

Cash Over and Short ………………………………….………..

2.11

Cash …………………………………………………….…

279.58

To reimburse the petty cash fund.

Feb. 28

Petty Cash ……………………………………………………….

100.00

Cash …………………………………………………….…

100.00

To increase the petty cash fund to $500.

Note: The two Feb. 28 entries can be combined into one.

Problem 6-3A (20 minutes)

Part 1

May 1

Petty Cash ……………………………………………………….

300.00

Cash …………………………………………………………..….

300.00

To establish the $300 petty cash fund.

May 15

Janitorial Expenses ………………………………………….….

88.00

Miscellaneous Expenses ………………………………….….

53.68

Postage Expenses ……………………………………………….

53.50

Advertising Expense ………………………………………..….

47.15

Cash Over and Short …………………………………..….

4.48

Cash …………………………………………………………..….

237.85

To reimburse the petty cash fund.

May 16

Petty Cash ……………………………………………………….

200.00

Cash …………………………………………………………..….

200.00

To increase the petty cash fund to $500.

May 31

Postage Expenses ……………………………………………….

147.36

Mileage Expense ………………………………………………….

23.50

Delivery Expense ……………………………………………..….

34.75

Cash Over and Short ………………………………………..….

6.19

Cash …………………………………………………………..….

211.80

To reimburse the petty cash fund.

May 31

Cash ………………………………………………………………..….

100.00

Petty Cash ………………………………………………….….

100.00

To decrease the petty cash fund to $400.

Part 2

If the May 31 replenishment is not made and no entry is recorded, then

Financial & Managerial Accounting, 5th Edition

396

Problem 6-4A (30 minutes)

Part 1

BRANCH COMPANY

Bank Reconciliation

July 31, 2013

Bank statement balance …………

$27,233

Book balance …………………………….…………………………

$27,497

Add

Add

Deposit of July 31 …………………

11,514

38,747

Proceeds of note less

collection charge…………………………..

7,955

35,452

Deduct

Deduct

Checks No. 3031 …… $1,482

NSF check …………………. $ 805

3065 …… 382

Service charge …………… 25

3069 …… 2,281

4,145

Error (Check 3056) …….. 20

850

Adjusted bank balance …………..

$34,602

Adjusted book balance …………………………..

$34,602

Part 2

July 31

Cash …………………………..…………………………………..…..

7,955

Collection Expense ……………………………………………..

45

Notes Receivable ……………………………………….…..

8,000

To record note collection less fees.

July 31

Accounts Receivable—E. Shaw ……………………….….

805

Cash ……………………………………………………….……..

805

To charge account for NSF check plus fees.

July 31

Miscellaneous Expenses …………………………..…….…..

25

Cash ……………………………………………………….……..

25

To record bank service fee.

July 31

Rent Expense …………………………..……………………..…..

20

Cash ……………………………………………………….……..

20

To correct an entry error.

Problem 6-4A (Concluded)

Part 3

a. If the company’s Cash account balance of $27,497 is listed on the

bank reconciliation as $27,947 then:

b. The bank’s collection of the $8,000 note less the $45 collection fee

should have been added to the book balance of cash. Instead, it was

added to the bank statement balance. As a result:

Financial & Managerial Accounting, 5th Edition

398

Problem 6-5A (50 minutes)

Part 1

CHAVEZ COMPANY

Bank Reconciliation

September 30, 2013

Bank statement balance ……………

$18,453.25

Book balance …………………………..

$17,404.20

Add

Add

Interest earned …… $ 12.50

Deposit of Sept. 30…………………..

1,682.75

20,136.00

Proceeds of note

less $15 fee ……… 1,485.00

1,497.50

18,901.70

Deduct

Deduct

Checks No. 5893 ……. $494.25

NSF check ……………… 600.25

5906 ……… 982.30

Error (Check 5904) .. 30.00

5908 ……. 388.00

1,864.55

630.25

Adjusted bank balance ……………..

$18,271.45

Adjusted book balance ……….

$18,271.45

Part 2

Sept. 30

Cash ……………………………………………………….

12.50

Interest Earned …………………………..…………………..

12.50

To record interest earned.

30

Cash ……………………………………………………….

1,485.00

Collection Expense ………………………………….…………..

15.00

Notes Receivable ……………………………….…………..

1,500.00

To record note collection less fee.

30

Accounts Receivable— S.Nilson …………………………..

600.25

Cash ………………………………………………….……

600.25

To charge account for NSF check plus fee.

30

Computer Equipment ……………………………….…………..

30.00

Cash ………………………………………………….……

30.00

To correct an entry error.

Problem 6-5A (Concluded)

Part 3

There are several possible reasons why some prenumbered checks are

missing from the sequence of canceled checks returned with a bank

statement. Reasons include:

(1) Some of the checks in the numbered sequence may have cleared the

bank in a previous period and were returned with the bank statement

error, it will return the check separately with a note of explanation to

the depositor.

Financial & Managerial Accounting, 5th Edition

400

PROBLEM SET B

Problem 6-1B (20 minutes)

1. Violates both applying technological control and effective segregation

of duties. It is safe to assume that Latisha Tally has knowledge of

employee passwords since she implemented the system of password

2. Violates applying technological controls. The theater’s system needs to

3. Violates segregation of duties. The company needs to have three

4. Violates applying technological controls. The use of the check protector

5. Violates segregation of duties. It is good internal control to separate

Problem 6-2B (30 minutes)

Part 1

Mar. 5

Petty Cash ……………………………………………………….

250

Cash …………………………………………………….…

250

To establish the $250 petty cash fund.

Part 2

Blues Music Center

Petty Cash Payments Report (for March)

Delivery expense

Mar. 11

Delivery of customer’s merchandise …………..…………

$ 10.75

Mileage expense

Mar. 30

Reimbursement for mileage ……………………….….

56.80

Postage expense

Mar. 28

Paid postage ……………………………………………..………..

18.00

Merchandise inventory (transportation-in)*

Mar. 6

COD charges on purchases ……………………….….

$12.50

Mar. 27

COD charges on purchases ……………………….….

45.10

57.60

Office supplies expense

Mar. 12

Purchased file folders ………………………………..…………

14.13

Mar. 14

Reimbursement for office supplies …………….…………

11.65

Mar. 18

Purchased paper ……………………………………….…………

20.54

46.32

Total

$189.47

* Transportation-in costs are included in Merchandise Inventory under a perpetual system.

Part 3

Mar. 31

Delivery Expense ……………………………………….………..

10.75

Mileage Expense ………………………………………..………..

56.80

Postage Expense ……………………………………….………..

18.00

Merchandise Inventory ………………………………………..

57.60

Office Supplies Expense …………………………….………..

46.32

Cash Over and Short …………………………….………..

1.00

Cash …………………………………………………….…

188.47

To reimburse the petty cash fund.

Mar. 31

Petty Cash ……………………………………………………….

50.00

Cash …………………………………………………….…

50.00

To increase the petty cash fund to $300.

Note: The two entries on Mar. 31 could be combined into one.

Problem 6-3B (20 minutes)

Part 1

Jan. 3

Petty Cash …………………………………………………………..

150.00

Cash ……………………………………………………….……..

150.00

To establish the petty cash fund.

Jan. 14

Office Supplies Expense ……………………………………...

14.29

Merchandise Inventory* ……………………………………....

19.60

Repairs Expense—Computer ……………………………....

38.57

Miscellaneous Expenses …………………………..………...

12.82

Cash Over and Short …………………………………………...

2.44

Cash ……………………………………………………….……..

87.72

To reimburse the petty cash fund.

* Transportation-in costs are included in Merchandise Inventory

under a perpetual system.

Jan. 15

Petty Cash …………………………………………………………..

50.00

Cash ……………………………………………………….……..

50.00

To increase the petty cash fund.

Jan. 31

Advertising Expense …………………………………………...

50.00

Postage Expenses ……………………………………………....

48.19

Delivery Expense ………………………………………………...

78.00

Cash Over and Short …………………………………………...

6.46

Cash ……………………………………………………….……..

182.65

To reimburse the petty cash fund.**

Jan. 31

Petty Cash …………………………………………………………..

50.00

Cash ……………………………………………………….……..

50.00

To increase the petty cash fund.**

Part 2

If the January 31 reimbursement is not made and no entry is recorded, then

Problem 6-4B (30 minutes)

Part 1

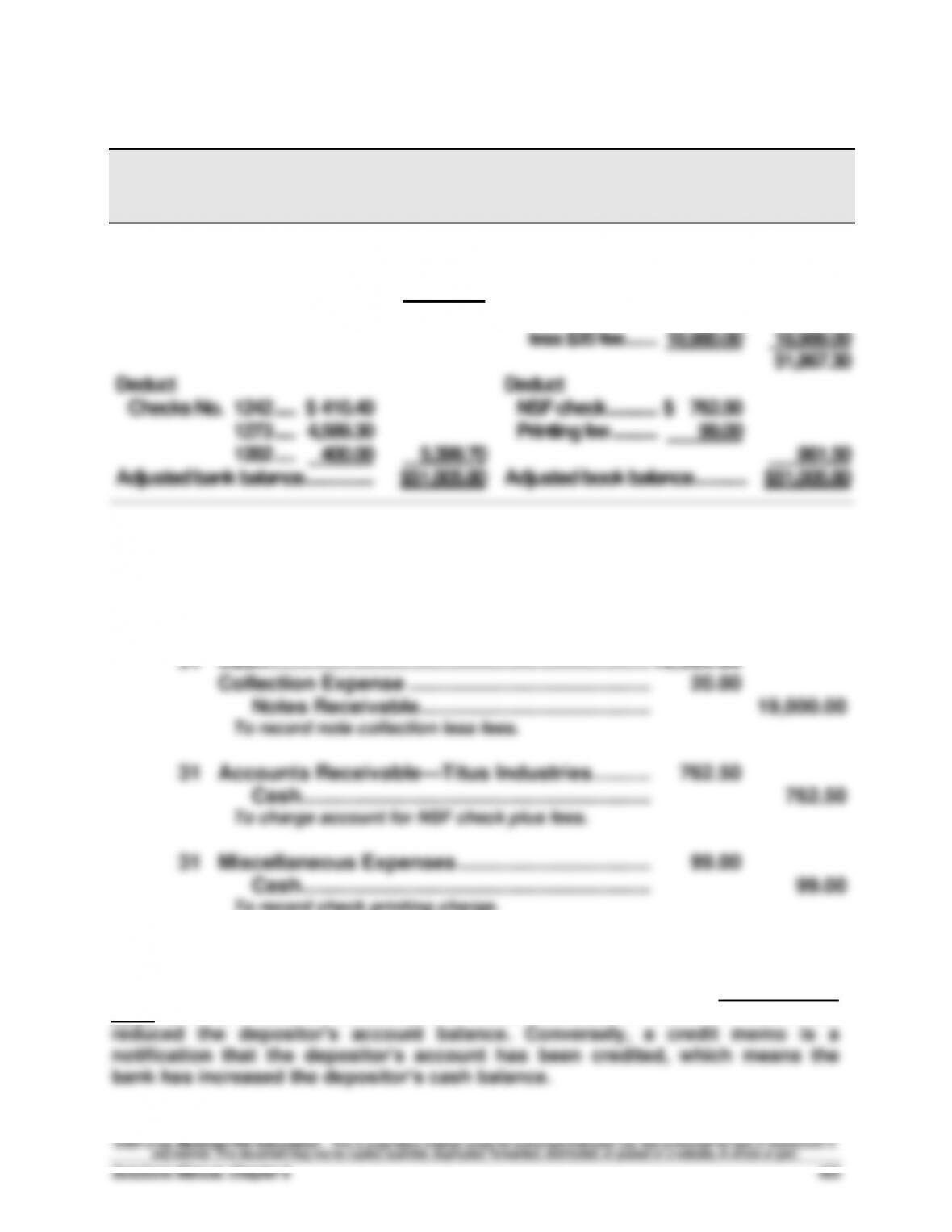

SEVERINO CO.

Bank Reconciliation

December 31, 2013

Bank statement balance …………..

$46,822.40

Book balance …………………………..

$32,878.30

Add

Add

Deposit of Dec. 31 …………………..

9,583.10

Error (Ck 1267) …. $ 9.00

56,405.50

Proceeds of note

less $20 fee …….. 18,980.00

18,989.00

51,867.30

Deduct

Deduct

Checks No. 1242 ….. $ 410.40

NSF check ………… $ 762.50

1273 ….. 4,589.30

Printing fee ……….. 99.00

1282 ….. 400.00

5,399.70

861.50

Adjusted bank balance ……………..

$51,005.80

Adjusted book balance …………..………………

$51,005.80

Part 2

Dec. 31

Cash …………………………………………………………………….

9.00

Office Supplies ……………………………………………….

9.00

To correct an entry error.

31

Cash …………………………………………………………………….

18,980.00

Collection Expense ……………………………………..……….

20.00

Notes Receivable …………………………………………….

19,000.00

To record note collection less fees.

31

Accounts Receivable—Titus Industries ………..……….

762.50

Cash ……………………………………………………….

762.50

To charge account for NSF check plus fees.

31

Miscellaneous Expenses ……………………………..……….

99.00

Cash ……………………………………………………….

99.00

To record check printing charge.

Part 3

In a banking context, a debit memo is notification from the bank that it has

debited the depositor’s account. Since the depositor’s account is a liability of the

bank (a credit balance account), the debit notification means the bank has

Financial & Managerial Accounting, 5th Edition

404

Problem 6-5B (50 minutes)

Part 1

SHAMARA SYSTEMS

Bank Reconciliation

May 31, 2013

Bank statement balance ……………..

$21,762.70

Book balance …………………….…….

$15,177.30

Add

Add

Deposit of May 31 ………………………

2,727.30

24,490.00

Proceeds of note less

$50 fee …………………………..

7,350.00

22,527.30

Deduct

Deduct

Checks No. 1780 …… $1,425.90

NSF check ……….. $431.80

1786 …… 353.10

Service charge … 14.00

1789 …… 639.50

2,418.50

Error (Ck 1788) … 10.00

455.80

Adjusted bank balance ………………..

$22,071.50

Adjusted book balance …….…………………….

$22,071.50

Part 2

May 31

Cash ………………………………………………………...…………

7,350.00

Collection Expense …………………………………..…………

50.00

Notes Receivable ……………………………………………

7,400.00

To record note collection less fee.

31

Accounts Receivable—W. Sox …………………..………

431.80

Cash ……………………………………………………….

431.80

To charge account for NSF check plus fee.

31

Miscellaneous Expenses …………………………..

14.00

Cash ……………………………………………………….

14.00

To record bank service fee.

31

Utilities Expense ……………………………………….…………

10.00

Cash ……………………………………………………….

10.00

To correct an entry error.