Financial & Managerial Accounting, 5th Edition

444

Problem 7-5B (75 minutes)

Part 1

2012

Nov. 1

Notes Receivable—S. Julian …………………………..

4,800

Accounts Receivable—S. Julian ………………....

4,800

To record note received on account.

Dec. 31

Interest Receivable …………………………………………..

64

Interest Revenue ………………………………………..

64

To record interest earned [$4,800 x .08 x 60/360].

2013

Jan. 30

Cash ………………………………………………………………..

4,896

Interest Revenue* ……………………………………....

32

Interest Receivable ……………………………………..

64

Notes Receivable—S. Julian ……………………....

4,800

To record cash received on note with interest.

*[$4,800 x .08 x 30/360]

Feb. 28

Notes Receivable—King Co ……………………………..

12,600

Accounts Receivable—King Co. ………………....

12,600

To record note received on account.

Mar. 1

Notes Receivable—M. Shelley ………………………....

6,200

Accounts Receivable—M. Shelley ……………....

6,200

To record note received on account.

30

Accounts Receivable—King Co ………………………..

12,684

Interest Revenue ………………………………………..

84

Notes Receivable—King Co ………………………..

12,600

To record receivable for dishonored note

plus interest [$12,600 x .08 x 30/360].

Apr. 30

Cash ………………………………………………………………..

6,324

Interest Revenue ………………………………………..

124

Notes Receivable—M. Shelley …………………....

6,200

To record cash received on note plus interest

($6,200 x .12 x 60/360 = $124).

Problem 7-5B (Concluded)

June 15

Notes Receivable—R. Solon …………………………..

2,000

Accounts Receivable—R. Solon ………………...

2,000

To record note received on account.

June 21

Notes Receivable—J. Felton …………………………..

9,500

Accounts Receivable—J. Felton ………………..

9,500

To record note received on account.

Aug. 14

Cash ……………………………………………………………...

2,034

Interest Revenue* ……………………………………..

34

Notes Receivable—R. Solon ……………………..

2,000

To record cash received on note plus interest.

*[$2,000 x .08 x 72/360] rounded to nearest dollar

Sept. 19

Cash ……………………………………………………………...

9,690

Interest Revenue* ……………………………………..

190

Notes Receivable—J. Felton ……………………..

9,500

To record cash received on note plus interest.

*[$9,500 x .08 x 90/360] rounded to nearest dollar

Nov. 30

Allowance for Doubtful Accounts …………………...

12,684

Accounts Receivable—King Co ………………...

12,684

To record write-off of accounts.

Part 2

Analysis Component: When a business pledges its receivables as security

for a loan and the loan is still outstanding at period-end, the business must

disclose this information in notes to its financial statements. This is a

SERIAL PROBLEM — SP 7

Serial Problem — SP 7, Success Systems (50 minutes)

1. a. Bad debts expense is recorded as 1% of total revenues:

$43,853 x .01 = $438.53 which is $439 rounded to nearest dollar.

2014

Mar. 31

Bad Debts Expense ………………………………………..

439

Allowance for Doubtful Accounts……………...

439

To record estimated bad debts.

1. b. Bad debts expense is recorded as 2% of accounts receivable:

Mar. 31

Bad Debts Expense ………………………………………..

454

Allowance for Doubtful Accounts……………...

454

To record estimated bad debts.

Bad Debts Expense ………………………………………..

Allowance for Doubtful Accounts……………...

To record estimated bad debts.

Reporting in Action — BTN 7-1

1. Polaris’s receivables at December 31, 2011, are $115,302 thousand.

2. Accounts receivable turnover for 2011 ($ thousands)

This time period is about ~15 days because Polaris typically sells its

4. Liquid assets as a percent of current liabilities ($ thousands)

company is in a slightly better position at December 21, 2010, as

compared to December 31, 2011. In either year, Polaris should not have

difficulty satisfying its current liabilities with these liquid assets. As a

benchmark, many prefer a ratio close to 100% for liquid assets divided by

current liabilities.

5. Note 1 to Polaris’s financial statements describes its significant

6. Solution depends on the financial statement information obtained.

($115,302 + $89,294)/2

$325,336 + $115,302 + $298,042

Comparative Analysis — BTN 7-2

1. Accounts Receivable Turnover ($ thousands)

Polaris (Current Year):

= 25.97 times

2. Average Collection Period (or “Average Days’ Sales Uncollected”)

Polaris (Current Year): 365 days / 25.97 times = 14.05 days

Polaris (Prior Year): 365 days / 22.16 times = 16.47 days

3. Both companies appear reasonably efficient in collecting accounts

receivable. Arctic Cat collects them over a longer period of time in both

years vis-à-vis Polaris due to Polaris’ arrangement with a financing

$2,656,949

($115,302 + $89,294)/2

Ethics Challenge — BTN 7-3

1. If the estimate for bad debts is reduced then less Bad Debts Expense

will be recognized on the income statement resulting in a higher net

2. Accounting procedures often allow for alternate methods or require the

use of estimates. Therefore, managers have some leeway in their

3. An informed owner or an effective board of directors will be aware of

alternate accounting methods and how estimates can affect the

financial statements. The owner or board should review the

reasonableness of the manager’s and accountant’s estimate for bad

debts expense. Also, if the company is audited, the auditors will review

this estimate for reasonableness.

Communicating in Practice — BTN 7-4

TO: Sid Omar

FROM: (Your Name)

DATE: _______________

SUBJECT: Difference Between Bad Debts Expense and Allowance

become uncollectible is what gives rise to bad debts expense and the

allowance for doubtful accounts.

Determining Bad Debts Expense

Bad debts expense represents the estimated amount of the year’s sales

that will become uncollectible. The reported amount of bad debts expense

The Allowance for Doubtful Accounts unadjusted balance at the end of the

year is the cumulative result of recording bad debts expense and writing

off specific accounts receivable in all past years. The recognition of bad

debts expense at the end of each year has the effect of increasing the

Allowance for Doubtful Accounts balance. However, when specific

had an “abnormal” balance of $16,000. Then, when this year’s bad debts

expense of $59,000 is added to Allowance for Doubtful Accounts, the result

is an ending balance of $43,000.

Sid, I hope this clarifies the matter for you. If you have further questions,

please call me.

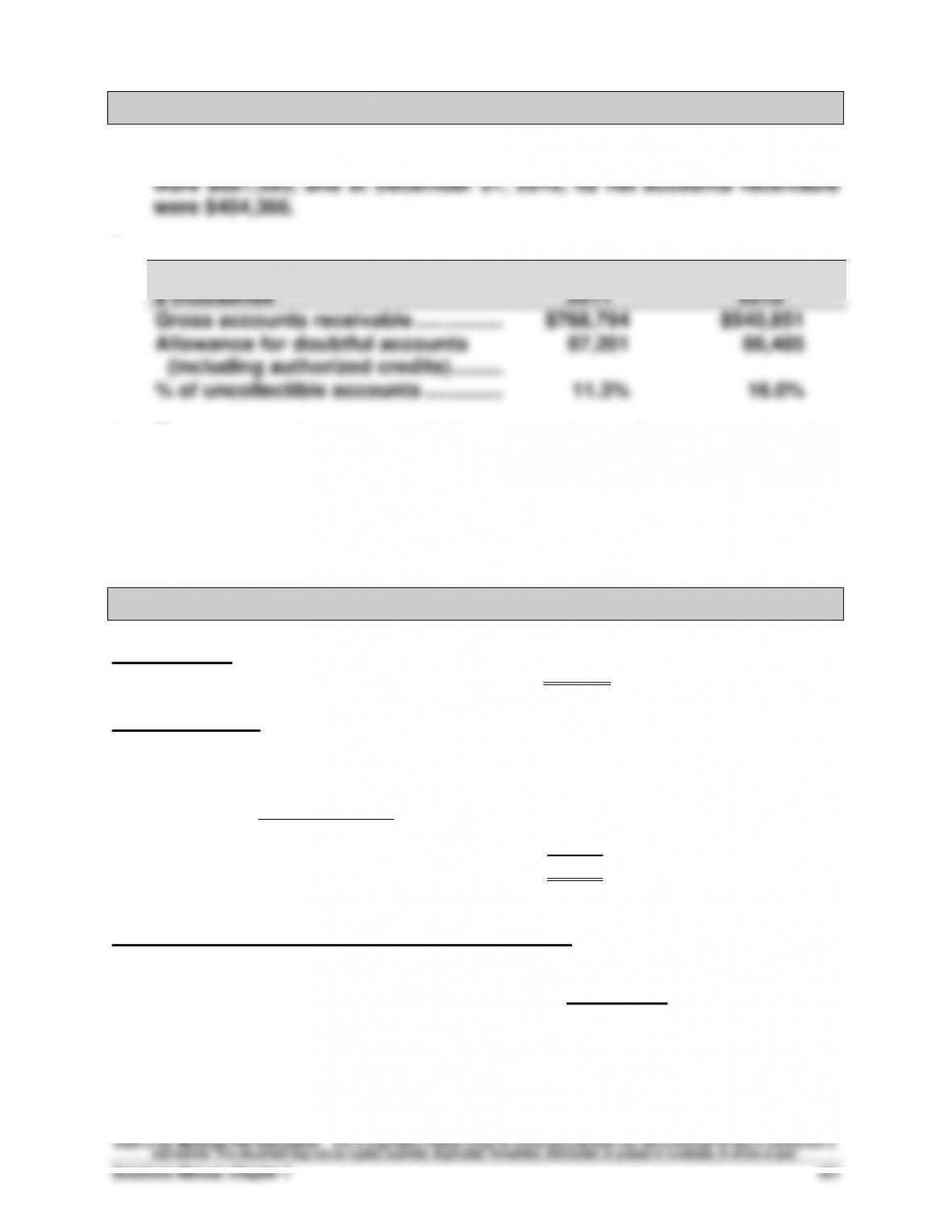

Taking It to the Net — BTN 7-5

1. At December 31, 2011, eBay’s ($ thousands) net accounts receivable

2.

$ thousands

December 31,

2011

December 31,

2010

Gross accounts receivable …………….…….

$768,794

$540,851

Allowance for doubtful accounts

(including authorized credits) …………….

87,201

86,485

% of uncollectible accounts …………..…….

11.3%

16.0%

3. These percentages seem high compared to other companies, but

eBay’s operations are all online, and the risk of fraudulent transactions

is likely higher than other companies. eBay’s prior experience has

apparently caused them to estimate this high amount of uncollectible

accounts.

Teamwork in Action — BTN 7-6

Instructor note: Computations for the aging schedule are in the Problem 7-4A solution.

The check figure for total estimated uncollectibles is $41,650.

Adjusting entry

Dec. 31

Bad Debts Expense ……………………………………....

27,150

Allowance for Doubtful Accounts …………....

27,150

To record estimated bad debts.*

* Req. allowance balance ………………..

$41,650 credit

Unadjusted balance ………………………

14,500 credit

Adj. to the allowance …………………….

$27,150 credit

December 31, 2013, Balance Sheet Presentation

Accounts Receivable …………………………………….. $1,220,000*

Less Allowance for Doubtful Accounts ………….. 41,650 1,178,350**

* Total of each age category.

** Net Realizable Accounts Receivable.

Entrepreneurial Decision — BTN 7-7

1. Computation of added annual net income or loss

a.

Added Monthly Net Income or Loss under Plan A

Increased sales ……………………………………………………… $250,000

Cost of sales …………………………………………………………. (135,500)

Entrepreneurial Decision — BTN 7-7 continued

2. Plan (A) provides a slightly higher income, so if the company can only

pursue one plan now, based purely on the financial aspect, it should

choose Plan (A).

Plan (A) might expand its product into new markets, and could increase

sales over time. However, this is a new distribution method for the

company, and it might lack the expertise to do it well. It will need to

further assess whether the benefit of additional expansion of online

sales over time will be more/less than the cost of lost sales through

normal channels.

Taking credit cards for these online sales reduces its risk of

uncollectible accounts. The credit card company takes the risk of the

customer not paying.

Plan (B) is a way to expand sales, possibly into more locations. This is

an expansion of a distribution method now employed.

The company does run some unknown risk associated with having new

customers. While the company may understand its current customers,

it will need to monitor the new customers to make sure that the

uncollectible accounts do not rise beyond acceptable levels.

Hitting the Road — BTN 7-8

Telephone calls to VISA and American Express are the source of

information for this solution. VISA reports that the average transaction fee

it charges merchants is 3%. American Express has a range, depending on

volume of business and average price of merchandise sold, which ranges

from 2.95% to 4.5%.

Some merchants often choose not to accept certain cards because the

credit card fees are higher than others. In the case of VISA, compared to

American Express, a merchant might have to pay as much as 1.5% more on

its American Express transactions. This can be a major part of its net

profit margin, especially for businesses such as grocery and hardware

stores.

Global Decision — BTN 7-9

1. Accounts Receivable Turnover (Euro in thousands)

2. Average Collection Period (or “Average Days’ Sales Uncollected”)

3. Piaggio is in between Polaris and Arctic Cat in terms of its turnover and

collection periods. Its collection period is relatively low however,