Exercise 8-19 (10 minutes)

Jan. 1

Copyright ……………………………………………………….

418,000

Cash…………………………..……………………………..…….

418,000

To record purchase of copyright.

Dec. 31

Amortization Expense—Copyright ……………………….

41,800

Accumulated Amortization—Copyright …………….

41,800

To record amortization of copyright

[$418,000 / 10 years].

Exercise 8-20 (10 minutes)

1. Goodwill = $2,500,000 – $1,800,000 = $700,000

Exercise 8-21 (15 minutes)

1. $11,761,000 cash for property and equipment

Exercise 8-22 (15 minutes)

Analysis comments. Based on these calculations, Lok turned its assets over 1.23

(4.59 – 3.36) more times in 2013 than in 2012. This increase indicates that the

Exercise 8-23A (15 minutes)

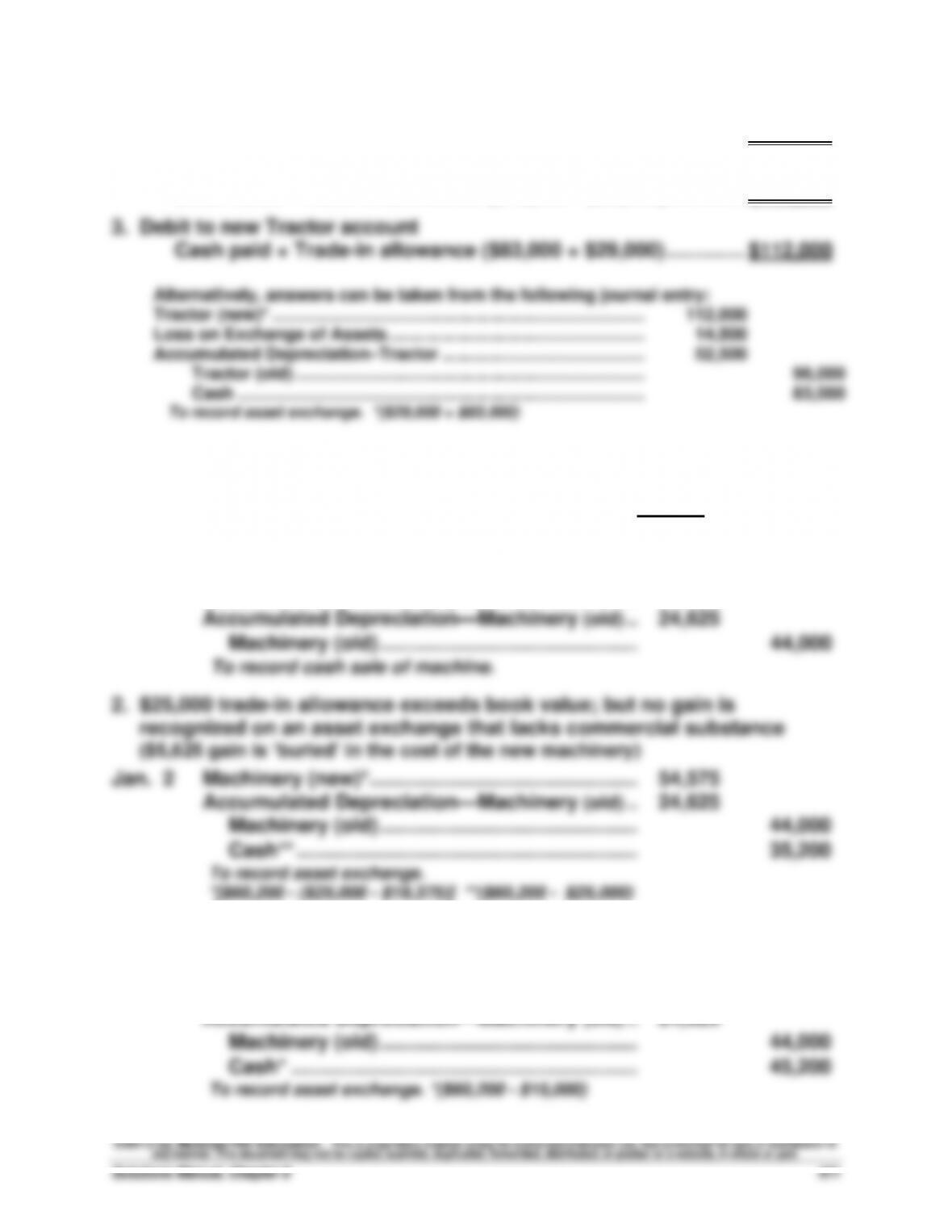

1. Book value of the old tractor ($96,000 – $52,500) …………………….. $ 43,500

2. Loss on the exchange

Book value – Trade-in allowance ($43,500 – $29,000) ………….. $ 14,500

Exercise 8-24A (25 minutes)

Note: Book value of Machine equals $44,000 – $24,625 = $19,375

1. Sold for $18,250 cash

Jan. 2

Cash …………………………………………………………..……….

18,250

Loss on Sale of Machinery …………………………..

1,125

Accumulated Depreciation—Machinery (old) ..……….

24,625

Machinery (old) ……………………………………….……….

44,000

To record cash sale of machine.

2. $25,000 trade-in allowance exceeds book value; but no gain is

recognized on an asset exchange that lacks commercial substance

($5,625 gain is ‘buried’ in the cost of the new machinery)

Jan. 2

Machinery (new)* ………………………………………………….

54,575

Accumulated Depreciation—Machinery (old) ..……….

24,625

Machinery (old) ……………………………………….……….

44,000

Cash** …………………………………………………….…

35,200

To record asset exchange.

*[$60,200 – ($25,000 – $19,375)] **($60,200 – $25,000)

3. $15,000 trade-in allowance is less than book value (yielding a loss)

Jan. 2

Machinery (new) ………………………………………….……….

60,200

Loss on Exchange of Machinery ………………….……….

4,375

Accumulated Depreciation—Machinery (old) ..……….

24,625

Machinery (old) ……………………………………….……….

44,000

Cash* ……………………………………………………....

45,200

To record asset exchange. *($60,200 – $15,000)

Exercise 8-25 (20 minutes)

1.

Depreciation expense …………………………………………….

4,731

Accumulated depreciation—Property, plant

and equipment……………………………………………..

4,731

To record depreciation on property, plant and

equipment.

2.

Property, plant and equipment …………………………..…..

5,634

Cash ……………………………………………………………….

5,634

To record betterments (improvements) on property,

plant and equipment.

3.

Cash …………………………..…………………………………………

700

Loss on disposal of property, plant and equipment ..

500

Accumulated Depreciation—Property, plant and

equipment …………………………………………………………..

1,322

Property, plant and equipment …………………………

2,522

To record asset disposal.

4. Volkswagen would decrease its property, plant and equipment account

by €451 at December 31, 2010, for its total impairments for 2010.

PROBLEM SET A

Problem 8-1A (50 minutes)

Part 1

Estimated

Market Value

Percent

of Total

Apportioned

Cost

Building ……………………..

$508,800

53%

$477,000

Land ………………………….

297,600

31

279,000

Land improvements ……

28,800

3

27,000

Vehicles …………………….

124,800

13

117,000

Total ………………………….

$960,000

100%

$900,000

2013

Jan. 1

Building …………………………..………………………..…

477,000

Land ……………………………………………………………………..

279,000

Land Improvements …………………………………..…………..

27,000

Vehicles ……………………………………………………….

117,000

Cash …………………………..……………………….….

900,000

To record asset purchases.

Part 2

Year 2013 straight-line depreciation on building

Part 3

Year 2013 double-declining-balance depreciation on land improvements

Part 4

Accelerated depreciation does not lower the total amount of taxes paid over

the asset’s life. Instead, it defers or postpones taxes to the later years of an

Financial & Managerial Accounting, 5th Edition

474

Problem 8-2A (45 minutes)

Part 1

Land

Building

2

Building

3

Land

Improve-

ments 1

Land

Improvements

2

Purchase price* ……….………

$1,612,000

$598,000

$390,000

Demolition ………………………

328,400

Land grading …………..………

175,400

New building……………………

$2,202,000

New improvements ….………

_________

_______

_________

_______

$164,000

Totals …………………………..

$2,115,800

$598,000

$2,202,000

$390,000

$164,000

*Allocation of purchase price

Appraised

Value

Percent

of Total

Apportioned

Cost**

Land …………………………………..

$1,736,000

62%

$1,612,000

Building 2 …………………………..

644,000

23

598,000

Land Improvements 1 ………....

420,000

15

390,000

Totals ………………………………...

$2,800,000

100%

$2,600,000

**Multiply the percentages in column 3 by the $2,600,000 purchase price.

Part 2

2013

Jan. 1

Land …………………………………………………………….

2,115,800

Building 2 …………………………………………………….

598,000

Building 3 …………………………………………………….

2,202,000

Land Improvements 1 …………………………………..

390,000

Land Improvements 2 …………………………………..

164,000

Cash ……………………………………………………….

5,469,800

To record costs of plant assets.

Part 3

2013

Dec. 31

Depreciation Expense—Building 2 …………………….…..

26,900

Accumulated Depreciation—Building 2 ………..…..

26,900

To record depreciation [($598,000 – $60,000)/20].

31

Depreciation Expense—Building 3 …………………….…..

72,400

Accumulated Depreciation—Building 3 ………..…..

72,400

To record depreciation [($2,202,000 – $392,000)/25].

31

Depreciation Expense—Land Improv. 1 ……………..…..

32,500

Accum. Depreciation—Land Improv. 1 ………….…..

32,500

To record depreciation [$390,000/12].

31

Depreciation Expense—Land Improv. 2 ……………..…..

8,200

Accum. Depreciation—Land Improv. 2 ………….…..

8,200

To record depreciation [$164,000/20].

Problem 8-3A (50 minutes)

2012

Jan. 1

Equipment ……………………………………………………....

300,600

Cash …………………………………………………………...

300,600

To record loader costs ($287,600 +$11,500 +$1,500).

Jan. 3

Equipment ……………………………………………………….

4,800

Cash ………………………………………………………….…..

4,800

To record betterment of loader.

To record depreciation.

Jan. 1

Equipment ……………………………………………………….

5,400

Cash ………………………………………………………….…..

5,400

To record extraordinary repair on loader.

Cash ………………………………………………………….…..

To record ordinary repair on loader.

Dec. 31

Depreciation Expense—Trucks …………………………..

Accumulated Depreciation—Trucks ………………..

5,200

Dec. 31

Accumulated Depreciation—Trucks ……………………..

To record sale of truck.

Problem 8-4A (40 minutes)

2012

Jan. 1

Trucks ………………………………………………………………...

22,000

Cash ……………………………………………………………...

22,000

To record cost of truck ($20,515 + $1,485).

Dec. 31

Depreciation Expense—Trucks …………………………..

4,000

Accumulated Depreciation—Trucks ………………..

4,000

To record depreciation [($22,000 – $2,000)/5].

2013

Dec. 31

Depreciation Expense—Trucks …………………………..

5,200*

Accumulated Depreciation—Trucks ………………..

5,200

To record depreciation.

Problem 8-5A (25 minutes)

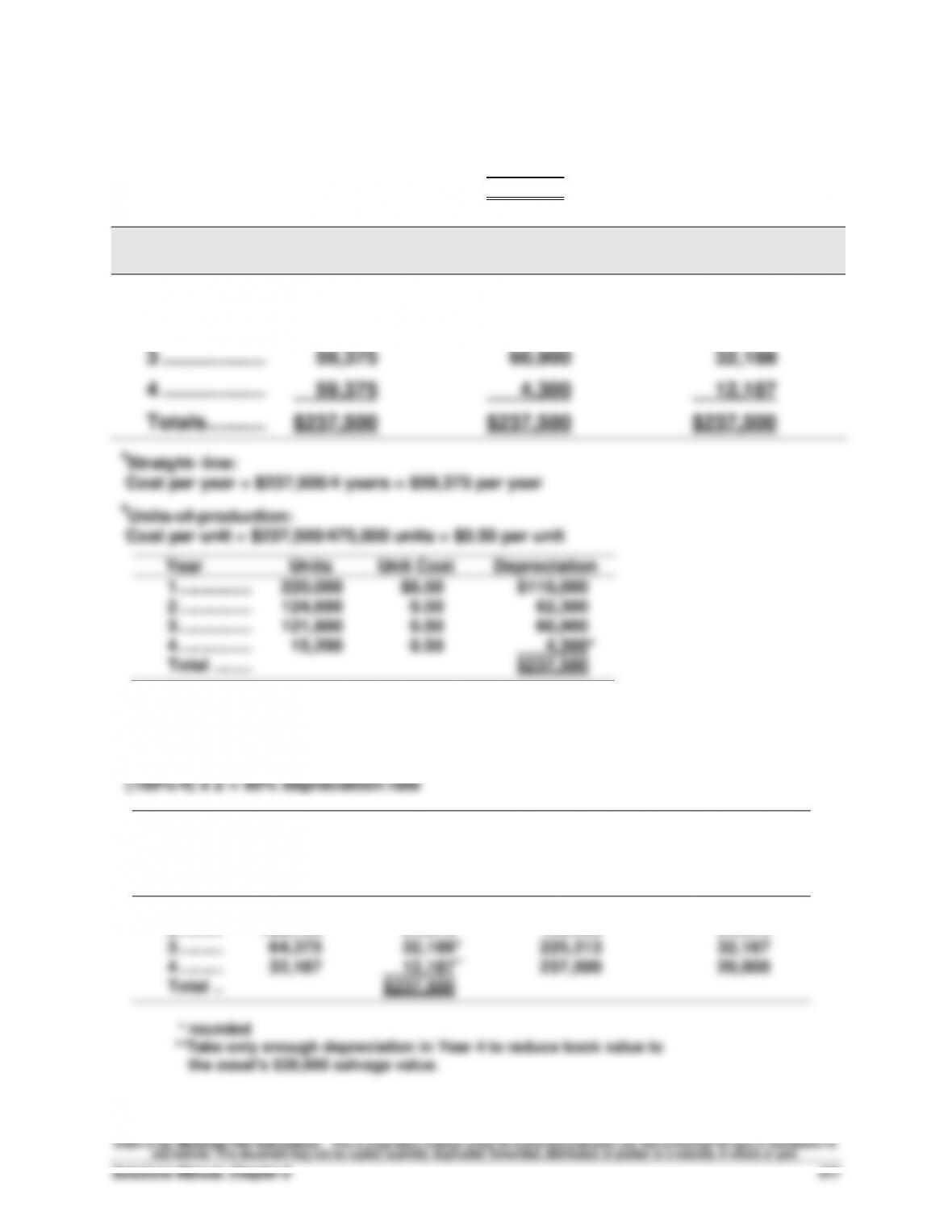

Cost of machine ……………………………….…………………….

$257,500

Less estimated salvage value …………………………..

20,000

Total depreciable cost …………………………..

$237,500

Year

Straight–Linea

Units–of-Productionb

Double-Declining-

Balancec

1 ……………….…

$ 59,375

$110,000

$128,750

2 ……………….…

59,375

62,300

64,375

3 ……………….…

59,375

60,900

32,188

4 ……………….…

59,375

4,300

12,187

Totals ………..…

$237,500

$237,500

$237,500

aStraight- line:

Cost per year = $237,500/4 years = $59,375 per year

bUnits-of-production:

Cost per unit = $237,500/475,000 units = $0.50 per unit

Year

Units

Unit Cost

Depreciation

1 …………….

220,000

$0.50

$110,000

2 …………….

124,600

0.50

62,300

3 …………….

121,800

0.50

60,900

4 …………….

15,200

0.50

4,300*

Total ……...

$237,500

* Take only enough depreciation in Year 4 to reduce book

value to the asset’s $20,000 salvage value.

cDouble-declining-balance:

Year

Beginning

Book

Value

Annual

Depreciation

(50% of

Book Value)

Accumulated

Depreciation

at the End of

the Year

Ending Book Value

($257,500 Cost Less

Accumulated

Depreciation)

1 ………

$257,500

$128,750

$128,750

$128,750

2 ………

128,750

64,375

193,125

64,375

3 ………

64,375

32,188*

225,313

32,187

4 ………

32,187

12,187**

237,500

20,000

Total ..

$237,500

* rounded

**Take only enough depreciation in Year 4 to reduce book value to

the asset’s $20,000 salvage value.

Financial & Managerial Accounting, 5th Edition

478

Problem 8-6A (20 minutes)

1.

Jan. 2

Machinery ……………………………………………………….

178,000

Cash …………………………..……………………………...

178,000

To record machinery purchase.

Jan. 3

Machinery ……………………………………………………….

2,840

Cash …………………………..……………………………...

2,840

To record machinery costs.

Jan. 3

Machinery ……………………………………………………….

1,160

Cash …………………………..……………………………...

1,160

To record machinery costs.

2. a. First year

Dec. 31

Depreciation Expense—Machinery ………………….……

28,000

Accumulated Depreciation—Machinery ……..……

28,000

To record depreciation [($182,000 – $14,000)/6].

b. Fifth year

Dec. 31

Depreciation Expense—Machinery ………………….……

28,000

Accumulated Depreciation—Machinery ……..……

28,000

To record year’s depreciation.

3. Accumulated depreciation at the date of disposal

Five years’ depreciation (5 x $28,000) …………………....

$140,000

Book value at the date of disposal

Original total cost ………………………………………………...

$182,000

Accumulated depreciation …………………………………....

(140,000)

Book value …………………………………………………………..

$ 42,000

a. Sold for $15,000 cash

Dec. 31

Cash ……………………………………………………………..…….

15,000

Loss on Sale of Machinery …………………………....…….

27,000

Accumulated Depreciation—Machinery ………….…….

140,000

Machinery ……………………………………………………….

182,000

Dec. 31

Cash ……………………………………………………………..…….

50,000

Accumulated Depreciation—Machinery ………….…….

140,000

Machinery ……………………………………………………….

182,000

Gain on Sale of Machinery …………………………..

8,000

Dec. 31

Cash ……………………………………………………………..…….

30,000

Accumulated Depreciation—Machinery ………….…….

140,000

Loss from Fire ……………………………………………….…….

12,000

Machinery ……………………………………………………….

182,000

Problem 8-7A (20 minutes)

a.

July 23

Mineral Deposit ……………………………………………………

4,715,000

Cash ……………………………………………………….

4,715,000

To record purchase of mineral deposit.

b.

July 25

Machinery ……………………………………………………….

410,000

Cash ……………………………………………………….

410,000

To record costs of machinery.

c.

Dec. 31

Depletion Expense—Mineral Deposit ……………………

441,600

Accum. Depletion—Mineral Deposit ……..…………

441,600

To record depletion [$4,715,000/

5,125,000 tons = $0.92 per ton.

480,000 tons x $0.92 = $441,600].

d.

Dec. 31

Depreciation Expense—Machinery …………….…………

38,400

Accum. Depreciation—Machinery ………..…………

38,400

To record depreciation [$410,000/

5,125,000 tons = $0.08 per ton.

480,000 tons x $0.08 = $38,400].

Analysis Component

Financial & Managerial Accounting, 5th Edition

480

Problem 8-8A (20 minutes)

1.

2013

(a)

June 25

Leasehold ……………………………………………………....

200,000

Cash ………………………………………………………..…….

200,000

To record payment for sublease.

(b)

July 1

Prepaid Rent………………………………………………….……

80,000

Cash ………………………………………………………..…….

80,000

To record prepaid annual lease rental.

(c)

July 5

Leasehold Improvements …………………………………….

130,000

Cash ………………………………………………………..…….

130,000

To record costs of leasehold improvements.

2.

2013

(a)

Dec. 31

Rent Expense ………………………………………………..…….

10,000

Accumulated Amortization—Leasehold …….…….

10,000

To record leasehold amortization ($200,000/10 x 6/12).

(b)

Dec. 31

Amortization Expense—Leasehold Improvements ….…….

6,500

Accumulated Amortization—Leasehold

Improvements …………………………………………….……..

6,500

To record leasehold improvement amortization

($130,000/10 years remaining on lease x 6/12).

(c)

Dec. 31

Rent Expense ………………………………………………..…….

40,000

Prepaid Rent ………………………………………………….

40,000

To record one-half year lease rental ($80,000 x 6/12).

PROBLEM SET B

Problem 8-1B (50 minutes)

Part 1

Estimated

Market Value

Percent

of Total

Apportioned

Cost

Building ……………………..

$ 890,000

50%

$ 900,000

Land …………………………..

427,200

24

432,000

Land improvements ……

249,200

14

252,000

Trucks ………………………..

213,600

12

216,000

Total …………………………..

$1,780,000

100%

$1,800,000

2013

Jan. 1

Buildings ……………………………………………..………..

900,000

Land …………………………………………………….…

432,000

Land Improvements ……………………………..……………….

252,000

Trucks ………………………………………………….……

216,000

Cash ……………………………………………….………

1,800,000

To record asset purchases.

Part 2

Year 2013 straight-line depreciation on building

Part 3

Year 2013 double-declining-balance depreciation on land improvements

Part 4

Accelerated depreciation does not increase the total amount of taxes paid

over the asset’s life. Instead, it defers or postpones taxes to the later years of

an asset’s useful life. This is because accelerated methods charge a higher

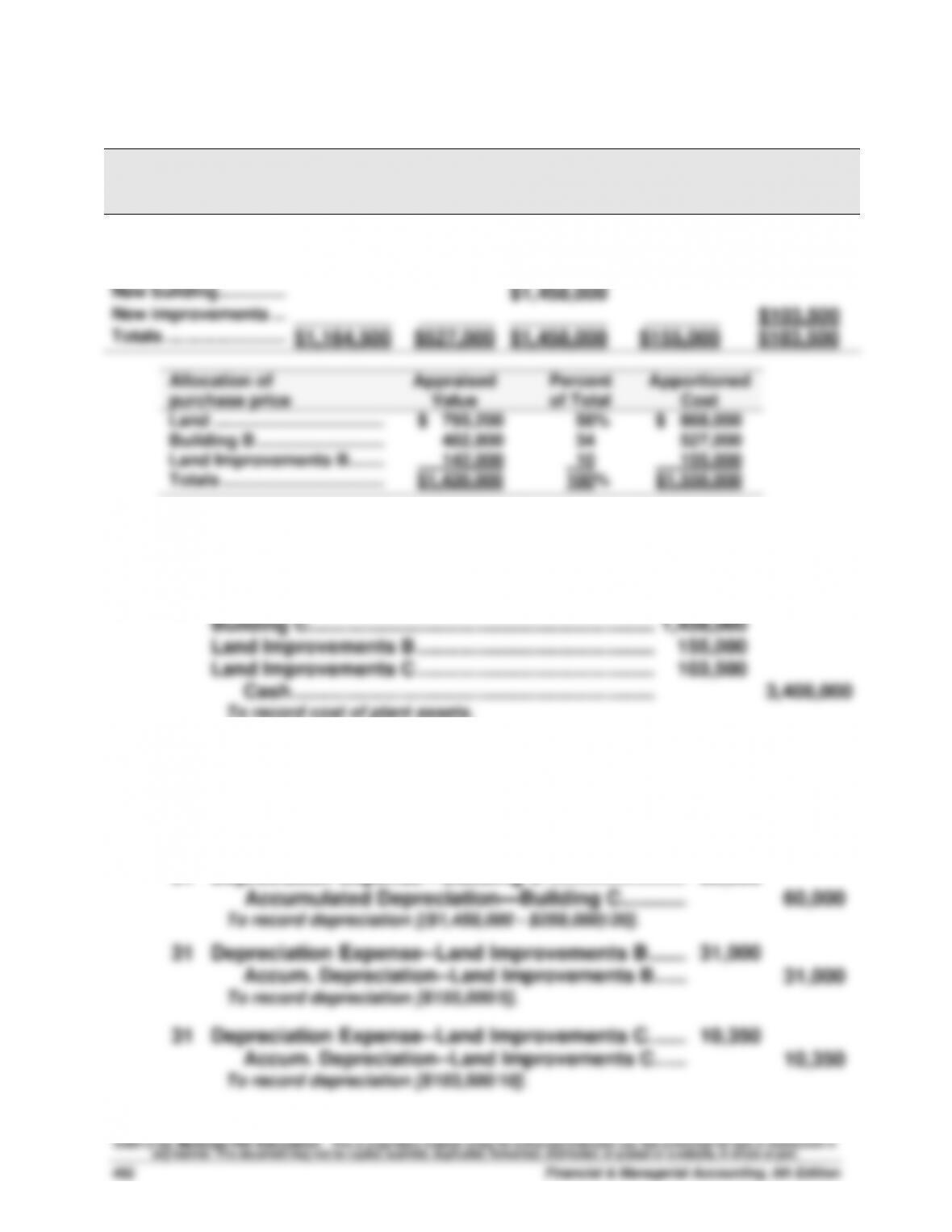

Problem 8-2B (45 minutes)

Part 1

Land

Building

B

Building

C

Land

Improve-

ments B

Land

Improve-

ments C

Purchase price* ……….

$ 868,000

$527,000

$155,000

Demolition ………………

122,000

Land grading …………..

174,500

New building……………

$1,458,000

New improvements ….

_________

_______

_________

_______

$103,500

Totals ……………………..

$1,164,500

$527,000

$1,458,000

$155,000

$103,500

Allocation of

purchase price

Appraised

Value

Percent

of Total

Apportioned

Cost

Land …………………………………..

$ 795,200

56%

$ 868,000

Building B …………………………..

482,800

34

527,000

Land Improvements B ……..…..

142,000

10

155,000

Totals …………………………….…..

$1,420,000

100%

$1,550,000

Part 2

2013

Jan. 1

Land ……………………………………………………………….

1,164,500

Building B……………………………………………………….

527,000

Building C……………………………………………………….

1,458,000

Land Improvements B ……………………………………..

155,000

Land Improvements C ……………………………………..

103,500

Cash ………………………………………………………….

3,408,000

To record cost of plant assets.

Part 3

2013

Dec. 31

Depreciation Expense—Building B …………………….…….

28,500

Accumulated Depreciation—Building B ……………………..

28,500

To record depreciation [($527,000 – $99,500)/15].

31

Depreciation Expense—Building C ……………………...

60,000

Accumulated Depreciation—Building C …………..

60,000

To record depreciation [($1,458,000 – $258,000)/20].

31

Depreciation Expense—Land Improvements B ……...

31,000

Accum. Depreciation—Land Improvements B ……..

31,000

To record depreciation [$155,000/5].

31

Depreciation Expense—Land Improvements C. ……..

10,350

Accum. Depreciation—Land Improvements C ……..

10,350

To record depreciation [$103,500/10].

Problem 8-3B (50 minutes)

2012

Jan. 1

Equipment …………………………………………………………..

27,670

Cash ……………………………………………………………...

27,670

To record costs of van ($25,860 + $1,810).

Jan. 3

Equipment …………………………………………………………..

1,850

Cash ……………………………………………………………...

1,850

To record betterment of van.

5,124

To record depreciation.

Jan. 1

Equipment …………………………………………………………..

2,064

Cash ……………………………………………………………...

2,064

To record extraordinary repair on van.

Cash ……………………………………………………………...

To record ordinary repair on van.

3,760