Archives: Solution Manual

978-1259722660 Chapter 15 Solution Manual Part 10

Problem 15-4 Requirement 1 Finance lease to lessee; Sales-type lease to lessor. Since the present value of lease payments (same for both the lessor and the Calculation of the Present Value of Lease Payments Present value of periodic lease payments […]

978-1259722660 Chapter 15 Solution Manual Part 9

Exercise 15-36 Requirement 1 The specific citation that specifies when a lessee remeasures the lease payments is FASB ASC 842–10–35–4: “Leases–Overall–Subsequent Measurement–Lease Payments.” Requirement 2 A lessee shall remeasure the lease payments if any of the following occur: a. The […]

978-1259722660 Chapter 15 Solution Manual Part 8

Exercise 15-29 Requirement 1 Note: Because exercise of the option appears at the beginning of the lease to be reasonably certain, payment of the option price ($45,000) is expected to occur when the option becomes exercisable (at the end of […]

978-1259722660 Chapter 15 Solution Manual Part 7

Exercise 15-23 The lease term will be 6 years. The lease term is the contractual lease term modified by any renewal or termination options for which exercise of the options is “reasonably certain.” Requirement 1 January 1, 2018 […]

978-1259722660 Chapter 15 Solution Manual Part 6

Exercise 15-16 Present Value of Lease Payments: lease present payments value * present value of an annuity due of $1: n=8, i=2% [i = 2% (8% ÷ 4) because the lease calls for quarterly payments] January 1, 2018 Right-of-use asset […]

978-1259722660 Chapter 15 Solution Manual Part 5

Exercise 15–11 Present Value of Lease Payments: contract present payments value * Present value of an annuity due of $1: n = 20, i = 2% [i = 2% (8% ÷ 4) because the contract calls for quarterly payments] Requirement […]

978-1259722660 Chapter 15 Solution Manual Part 4

Exercise 15-5 1. Calculation of the present value of lease payments (“selling price”) 2. Receivable at December 31, 2018 Receivable Initial balance, June 30, 2018…………. $3,000,000 June 30, 2018 reduction………………… (562,907)* Dec. 31, 2018 reduction………………… (441 ,052)** December 31, 2018 […]

978-1259722660 Chapter 15 Solution Manual Part 3

Exercise 15-1 Situation 1 Since none of the criteria is met, this is an operating lease to the lessee: Lessee’s Application of Classification Criteria 1 Does the agreement specify that ownership of the asset transfers 2 Does the agreement contain […]

978-1259722660 Chapter 15 Solution Manual Part 2

Brief Exercise 15-1 The present value of the lease payments is greater than “substantially all” of the Brief Exercise 15-2 The lease is a finance lease to Athens because the present value of the lease payments is greater than “substantially […]

978-1259722660 Chapter 15 Solution Manual Part 1

QUESTIONS FOR REVIEW OF KEY TOPICS Question 15-1 Regardless of the legal form of the agreement, a lease is accounted for as either a rental agreement or a purchase/sale accompanied by debt financing depending on the Question 15-2 Periodic interest […]

978-1259722660 Chapter 15 Lecture Note Part 2

PowerPoint Slides Two PowerPoint presentations of the chapter are available in the Connect Library: 1. With “Concept Checks” useful for classroom presentation, permitting the instructor to intersperse in the presentation short exercises students can be asked to solve individually or […]

978-1259722660 Chapter 15 Lecture Note Part 1

CHAPTER 15 LEASES Overview In the previous chapter, we saw how companies account for their long-term debt. The focus of that discussion was bonds and notes. In this chapter, we continue our discussion of debt, but we now turn our […]

978-1259722660 Chapter 14 Solution Manual Part 15

Case 14–9 (continued) AGF has experienced favorable leverage, as demonstrated by calculating and comparing the return on assets and the return on shareholders’ equity for 2016: The debt to equity ratio is not used to shareholders’ advantage. The return on […]

978-1259722660 Chapter 14 Solution Manual Part 14

Case 14–3 (continued) Arguments Supporting View 1: 1. Those who favor accounting for convertible debt as entirely a liability until it is either converted or repaid argue that a convertible bond offers the holder two mutually exclusive choices. The holder […]

978-1259722615 Chapter 18 Solution Manual

Solutions to Chapter 18 Long-Term Financial Planning 1. a. False. Financial planning is a process of deciding which risks to take. b. False. Financial planning is concerned with possible surprises as well as the most likely outcomes. c. True. Financial […]

978-1259722660 Chapter 14 Solution Manual Part 13

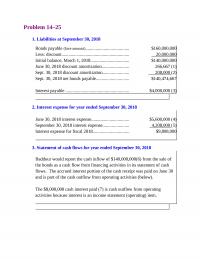

Problem 14–25 1. Liabilities at September 30, 2018 Bonds payable (face amount)……………………………….. $160,000,000 Less: discount………………………………………………….. 20 ,000,000 2. Interest expense for year ended September 30, 2018 June 30, 2018 interest expense…………………………… $5,600,000 (4) September 30, 2018 interest expense………………….. 4 ,208,000 […]

978-1259722660 Chapter 14 Solution Manual Part 12

Problem 14–23 (continued) Requirement 4 If the fair value on December 31 is $342,000, Appling needs to compare that amount with the amortized initial measurement on that date. That amount was increased when Appling recorded interest on December 31: Interest […]

978-1259722660 Chapter 14 Solution Manual Part 11

Problem 14–19 Requirement 1 Convertible Bonds—2005 issue Cash (97.5% x $200 million)……………………………………………….. 195 Bonds with Warrants—2009 issue Cash (102% x $50 million)………………………………………………….. 51 Discount on bonds payable (difference)………………………………. 3 Bonds payable (face amount)………………………………………….. 50 Equity—stock warrants (given)……………………………………… 4 Requirement 2 […]

978-1259722660 Chapter 14 Solution Manual Part 10

Problem 14–11 Requirement 1 *Present value of an ordinary annuity of $1: n = 5, i = 10% (Table 4) ** Present value of $1: n = 5, i = 10% (Table 2) Equipment (fair value)……………………………………………. 115,883 Discount on notes […]

978-1259722660 Chapter 14 Solution Manual Part 9

Problem 14–6 (concluded) February 28, 2021 (Western) Interest expense ($1,800,000 + 40,000 – 1,200,000). 640,000 Interest payable (from adjusting entry)……………….. 1,200,000 February 28, 2021 (Stillworth) Cash ($30,000 x 12% x 6/12)……………………………… 1,800 Discount on bond investment ($20 x 2 months)…… […]

978-1259722660 Chapter 14 Solution Manual Part 8

Problem 14–3 (continued) Requirement 3 (effective interest) (straight-line) Interest expense ($4,500 + 404)…………………………………. 4,904 Discount on bonds payable ($3,232 ÷ 8)…………….. 404 Cash (4.5% x $100,000)…………………………………….. 4,500 Requirement 4 By the straight-line method, a company determines interest indirectly by allocating […]

978-1259722660 Chapter 14 Solution Manual Part 7

Exercise 14–30 (concluded Rapid will report the loss from the change in the fair value of the bonds in net income if the entire change is due to the change in general interest rates. But any change in the fair […]

978-1259722660 Chapter 14 Solution Manual Part 6

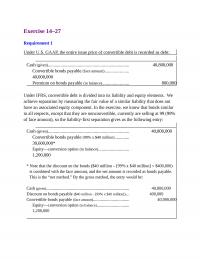

Exercise 14–27 Requirement 1 Under U.S. GAAP, the entire issue price of convertible debt is recorded as debt: Under IFRS, convertible debt is divided into its liability and equity elements. We achieve separation by measuring the fair value of a […]

978-1259722660 Chapter 14 Solution Manual Part 5

Exercise 14–19 1. January 1, 2018 Cash ……………………………………………………………………….. 8,000,000 2. Amortization schedule $8,000,000 ÷ 2.67301 = $2,992,881 amount (from Table 4) of loan n = 3, i = 6% Cash Effective Decrease in Outstanding Dec.31 Payment Interest Balance Balance 6% […]

978-1259722660 Chapter 14 Solution Manual Part 4

Exercise 14–11 1. February 1, 2018 2. July 31, 2018 Interest expense (5% x $731,364)…………………… 36,568 Discount on bonds payable (difference)…… 568 Cash (4.5% x $800,000)………………………….. 36,000 3. December 31, 2018 Interest expense (5/6 x 5% x [$731,364 + 568]). […]

978-1259722660 Chapter 14 Solution Manual Part 3

Exercise 14–3 1. Price of the bonds at January 1, 2018 2. January 1, 2018 Cash (price determined above)……………………………….. 70,823,680 Discount on bonds payable (difference)………………… 9,176,320 Bonds payable (face amount)……………………………. 80,000,000 3. June 30, 2018 Interest expense (6% x $70,823,680)………………………….. […]

978-1259722660 Chapter 14 Solution Manual Part 2

Brief Exercise 14–1 face annual fraction of the cash amount rate annual period interest Brief Exercise 14–2 Interest $ 2,000,000 ¥ x 23.11477* =$46,229,540 Principal $80,000,000 x 0.30656** = 24,524,800 Present value (price) of the bonds $70,754,340 ¥ [5 ÷ […]

978-1259722660 Chapter 14 Solution Manual Part 1

QUESTIONS FOR REVIEW OF KEY TOPICS Question 14–1 Periodic interest is calculated as the effective interest rate times the amount of the debt outstanding during the period. This same principle applies to the flip side of the Question 14–2 Long-term […]

978-1259722660 Chapter 14 Lecture Note Part 2

Suggestions for Class Activities 1. Real World Scenario An article in Barron’s, titled “Wall Street’s Latest Illusion,” reported that “Goldman Sachs, Morgan Stanley and other firms are booking profits from the falling value of their own debt.” The article asserts […]

978-1259722660 Chapter 14 Lecture Note Part 1

CHAPTER 14 BONDS AND LONG-TERM NOTES Overview This chapter continues the presentation of liabilities. While the discussion focuses on the accounting treatment of long-term liabilities, the borrowers’ side of the same transactions is presented as well. Long-term notes and bonds […]

978-1259722660 Chapter 13 Solution Manual Part 10

TARGET CASE Requirement 1 a. The four components of current liabilities are: ($ in millions) 1/30/2016 1/31/2015 Current Liabilities: Accounts payable $ 7,418 $ 7,759 b. Current assets are sufficient to cover current liabilities in both the fiscal years ended […]

978-1259722660 Chapter 13 Solution Manual Part 9

IFRS Case 13–15 Under IFRS, the $70 million environmental contingency would be accrued and included in Fizer’s liabilities. The associated loss would be reported in the income statement. Accounting for contingencies is covered under IAS No. 37, “Provisions, Contingent Liabilities, […]

978-1259722660 Chapter 13 Solution Manual Part 8

Communication Case 13–7 Assumptions students make will determine the correct answer to some classifications. Depending on the assumptions made, different views can be convincingly defended. The process of developing and synthesizing the arguments will likely be more beneficial than any […]

978-1259722660 Chapter 13 Solution Manual Part 7

Problem 13–13 Salaries and wages expense (total amount earned)……….. 2,000,000 Withholding taxes payable (federal income tax)………. 400,000 Withholding taxes payable (local income tax)…………. 53,000 Payroll tax expense (total)……………………………………. 273,000 Social security taxes payable (employer’s matching amount) 124,000 Medicare taxes payable […]

978-1259722660 Chapter 13 Solution Manual Part 6

Problem 13–7 Requirement 1 Item (a): Because the loss is probable and can be reasonably estimated, HW would be required to accrue a liability under both U.S. GAAP and Item (b): Under IFRS, present values would be used, so the […]

978-1259722660 Chapter 13 Solution Manual Part 5

Problem 13–1 Requirement 1 Blanton Plastics L & T Bank Notes receivable………………………………………………. 14,000,000 Cash …………………………………………………………… 14,000,000 Requirement 2 Adjusting entries (December 31, 2018) Blanton Plastics Interest expense ($14,000,000 x 12% x 3/12)…………….. 420,000 Interest payable…………………………………………….. 420,000 L & T Bank […]

978-1259722660 Chapter 13 Solution Manual Part 4

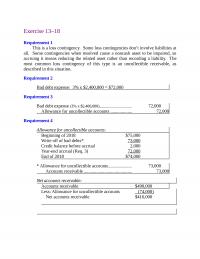

Exercise 13–18 Requirement 1 This is a loss contingency. Some loss contingencies don’t involve liabilities at all. Some contingencies when resolved cause a noncash asset to be impaired, so Requirement 2 Bad debt expense: 3% x $2,400,000 = $72,000 Requirement […]

978-1259722660 Chapter 13 Solution Manual Part 3

Exercise 13–7 Requirement 1 Deposits Collected Containers Returned Liability—refundable deposits …………………… 790,000 Cash…………………………………………………….. 790,000 Deposits Forfeited Liability—refundable deposits …………………… 35,000 Revenue—sale of containers…………………… 35,000 Cost of goods sold…………………………………….. 35,000 Inventory of containers ………………………….. 35,000 Requirement 2 Balance on January 1 […]

978-1259722660 Chapter 13 Solution Manual Part 2

Brief Exercise 13–6 December 12 January 16 Cash…………………………………………………………….. 216,000 Deferred sales revenue……………………………………. 24,000 Sales revenue…………………………………………….. 240,000 Brief Exercise 13–7 In 2018 Lizzie would recognize $11,500 of revenue ($4,000 + 3,000 + 2,500 + 2,000). In 2019 Lizzie would recognize the […]

978-1259722660 Chapter 13 Solution Manual Part 1

A liability involves the past, the present, and the future. It is a present responsibility, to sacrifice assets in the future, caused by a transaction or other event 1. are probable, future sacrifices of economic benefits 2. that arise from […]

978-1259722660 Chapter 13 Lecture Note Part 2

5. Ethical Dilemma Consider the following ethical dilemma: ETHICAL DILEMMA You are chief financial officer of Camp Industries. Camp is the defendant in a $44 million class-action suit. The company’s legal counsel informally advises you that chances are remote that […]

978-1259722660 Chapter 13 Lecture Note Part 1

CHAPTER 13 CURRENT LIABILITIES AND CONTINGENCIES Overview Chapter 13 is the first of five chapters devoted to liabilities. In Part A of this chapter, we discuss liabilities that are classified appropriately as current. In Part B, we turn our attention […]

978-1259722660 Chapter 12 Solution Manual Part 15

International Case 12–4 Requirement 1 P. 140 of the 10K includes the following note: “Interests in other companies Interests in other companies are measured at fair value. Investments in equity investments that do not have a quoted market price in […]

978-1259722660 Chapter 12 Solution Manual Part 14

Problem 12–16 (continued) Need to move from a fair-value adjustment from $0 to ($9,420): Fair-Value Adjustment 1/1/2018 0 December 31, 2018 Cash ($150,000 x 6%) ÷ 2……………………………….. 4,500 Discount on bond investment (difference)…………. 390 Interest revenue [{$150,000 – ($10,658 – […]

978-1259722660 Chapter 12 Solution Manual Part 13

Problem 12–11 Note: the answer to P12-11 is the same as the answer to Requirement 2 of P12-10. Purchase ($ in millions) Net income No entry Dividends Cash (10 million shares x $2)……………………………………………………. 20 Dividend revenue……………………………………………………………. 20 Adjusting entry Need […]

978-1259722660 Chapter 12 Solution Manual Part 12

Problem 12–9 2018 ($ in millions) October 18 October 31 Cash…………………………………………………………………………………. 1.5 Interest revenue………………………………………………………………. 1.5 November 1 Investment in Holistic Entertainment bonds (HTM)……………….. 18 Cash……………………………………………………………………………… 18 November 1 1) Updating the fair-value adjustment: Need to move from a fair-value adjustment […]

978-1259722660 Chapter 12 Solution Manual Part 11

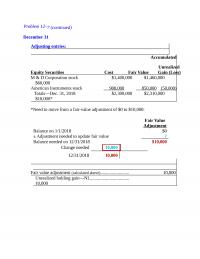

Problem 12–7 (continued) December 31 Adjusting entries: Accumulated Unrealized Equity Securities Cost Fair Value Gain (Loss) $10,000* *Need to move from a fair-value adjustment of $0 to $10,000: Fair-Value Adjustment 1/1/2018 0 Change needed 10,000 12/31/2018 10,000 Fair value adjustment […]

978-1259722660 Chapter 12 Solution Manual Part 10

Problem 12–5 (continued) 2) Recording the sale transaction: Cash (proceeds)…………………………………………………….. 425,000 November 1 Investment in M&D Corporation bonds ………………… 1,400,000 Cash……………………………………………………………….. 1,400,000 Investment in Distribution Transformers bonds (cost) 400,000 Fair-value adjustment (account balance)…………………. 25,000 Problem 12–5 (continued) December 31 Adjusting […]

978-1259722660 Chapter 12 Solution Manual Part 9

Problem 12–2 Requirement 1 ($ in millions) Requirement 2 Cash (4% x $80 million)…………………………………… 3.20 Discount on bond investment (difference)…………. .10 Interest revenue (5% x $66)……………………………… 3.30 Requirement 3 Cash (4% x $80 million)…………………………………… 3.20 Discount on bond investment (difference)…………. […]

978-1259722660 Chapter 12 Solution Manual Part 8

Exercise 12–29 Requirement 1 Requirement 2 Cash (death benefit)………………………………………………… 250,000 Cash surrender value of life insurance (account balance) 16,000 Gain on life insurance settlement (to balance)………… 234,000 Insurance expense (difference)………………………………… 22,900 Cash surrender value of life insurance ($4,600 – 2,500).. […]