Archives: Solution Manual

978-1259722660 Chapter 12 Solution Manual Part 7

Exercise 12–24 Requirement 1 Purchase ($ in millions) Net income Investment in VB shares (25% x $32 million) ………………………. 8 Investment revenue…………………………………………………. 8 Dividends Cash (25% x $24 million)………………………………………………… 6 Investment in VB shares………………………………………….. 6 Amortization of differential Investment revenue […]

978-1259722660 Chapter 12 Solution Manual Part 6

Exercise 12–17 (continued) Requirement 2 Need to move from a fair-value adjustment from ($145,000) to ($70,000): Fair-Value Adjustment 1/1/2018 145,000 Fair Value Adjustment Balance on 1/1/2018 ($145,000) ± Adjustment needed to update fair value ? Balance needed on 12/31/2018 ($1,275,000 […]

978-1259722660 Chapter 12 Solution Manual Part 5

Exercise 12–12 (continued) a. June 30, 2019: Recognition of interest revenue b. July 1, 2019: Any entries necessary upon sale of the Jackson bonds 1) Updating the fair-value adjustment: Need to move from a fair-value adjustment of $200,000 to ($100,000): […]

978-1259722660 Chapter 12 Solution Manual Part 4

Exercise 12–7 (continued) 2019 January 5 1) Updating the fair-value adjustment: Need to move from a fair-value adjustment of $50,000 to $45,000: Fair-Value Adjustment Change needed 5,000 1/5/2019 45,000 Unrealized holding loss—NI ($395,000 – $400,000)…………… 5,000 Fair value adjustment………………………………………………. 5,000 […]

978-1259722660 Chapter 12 Solution Manual Part 3

Brief Exercise 12–19 LED does not intend to sell the investment, and it does not believe it is more likely than not that it will have to sell the investment before fair value recovers, so Fair value adjustment…………………………………… 100,000 Reclassification […]

978-1259722660 Chapter 12 Solution Manual Part 2

Brief Exercise 12–2 Because S&L Financial is purchasing the bonds for purposes of earning profits on short-term differences in price, those bonds would be classified as trading securities. For trading securities, gains and losses from changes in fair values are […]

978-1259722660 Chapter 12 Solution Manual Part 1

Question 12–1 Question 12–2 Increases and decreases in the market value between the time a debt security is acquired and the day it matures to a prearranged maturity value are ignored for a security classified as “held-to-maturity.” These changes aren’t […]

978-1259722660 Chapter 12 Lecture Note Part 1

CHAPTER 12 INVESTMENTS Overview In this chapter we cover various approaches used to account for investments that companies make in the debt and equity securities of other companies. An investing company has the option to account for these investments at […]

978-1259722660 Chapter 11 Solution Manual Part 11

Ethics Case 11–10 Requirement 1 2018 expense using CEO’s approach: $42,000,000 Cost Depreciation to date (2016–2017) 33,600,000 Book value ÷ 3 Estimated remaining life (2018–2020) $11,200,000 New annual depreciation 2018 income would include only depreciation expense of $11,200,000. 2018 expense […]

978-1259722660 Chapter 11 Solution Manual Part 10

Problem 11–13 (concluded) 2019 Depreciation of equipment: Original cost $140,000 Less: 2018 depreciation (19 ,500) 2019 Depreciation of structures: Original cost $68,000 Less: 2018 depreciation (10 ,200) Remaining depreciable cost $57,800 Revised estimate of tons remaining (1,000,000 – 120,000) […]

978-1259722660 Chapter 11 Solution Manual Part 9

Problem 11–10 (concluded) b. This is a change in accounting principle that is accounted for as a change in estimate. SYD 2014 depreciation $ 60,000 ($330,000 × 10/55) 2015 depreciation 54,000 ($330,000 × 9/55) 2016 depreciation 48,000 ($330,000 × 8/55) […]

978-1259722660 Chapter 11 Solution Manual Part 8

Problem 11–7 Requirement 1 Cost of mineral mine: Depletion: $2,200,000 – 100,000 Depletion per ton = = $5.25 per ton 400,000 tons 2018 depletion = $5.25 × 50,000 tons = $262,500 2019 depletion: Revised depletion rate = ($2,200,000 – 262,500) […]

978-1259722660 Chapter 11 Solution Manual Part 7

Problem 11–1 Requirement 1 Determine useful life: Determine age of assets: $40,000 accumulated depreciation = 4 years old $10,000 annual depreciation Double-declining balance in 4th year of life: Year 1 (2015) $200,000 × 10% = $20,000 Year 2 (2016) 180,000 […]

978-1259722660 Chapter 11 Solution Manual Part 6

Exercise 11–30 Requirement 1 Determination of implied fair value of goodwill: Fair value of Centerpoint, Inc. $220 million Measurement of impairment loss: Book value of goodwill $50 million Implied fair value of goodwill 20 million Impairment loss $30 million Requirement […]

978-1259722660 Chapter 11 Solution Manual Part 5

Exercise 11–20 Adjustment of amortization expense to reflect change in useful life. ($ in millions) ……………………………………………………………………Patent ………………………………………………………………………..2.5 Calculation of annual amortization after the estimate change: $ in millions) $9 Cost $1 Previous annual amortization ($9 ÷ 9 years) × 4 […]

978-1259722660 Chapter 11 Solution Manual Part 4

Exercise 11–11 Requirement 1 To update depreciation in 2018; 2 months of service to date of disposal. Depreciation expense …………………………………………….. 2,000 ……………………………………….Accumulated depreciation …………………………………………………………………………..2,000 Requirement 2 To record the sale of the truck. Cash …………………………………………………………………….. 58,000 Loss on sale of […]

978-1259722660 Chapter 11 Solution Manual Part 3

Exercise 11–2 1. Straight-line: 2. Sum-of-the-years’ digits: Sum-of-the-digits is ([10 (10 + 1)] ÷ 2) = 55 2018 $110,000 × 10/55 = $20,000 2019 $110,000 × 9/55 = $18,000 3. Double-declining balance: Straight-line rate is 10% (1 ÷ 10 years) […]

978-1259722660 Chapter 11 Solution Manual Part 2

Brief Exercise 11–3 a. Straight-line: b. Sum-of-the-years’ digits: Sum-of-the-digits is ([4 (4 + 1)] ÷ 2) = 10 2018 $28,000 × 4/10 × 9/12 = $8,400 2019 $28,000 × 4/10 × 3/12 = $2,800 + $28,000 × 3/10 × 9/12 […]

978-1259722660 Chapter 11 Solution Manual Part 1

Question 11–1 The terms depreciation, depletion, and amortization all refer to the process of allocating the cost of property, plant, and equipment and finite-life intangible assets Question 11–2 The term depreciation often is confused with a decline in value or […]

978-1259722660 Chapter 11 Lecture Note Part 1

CHAPTER 11 PROPERTY, PLANT, AND EQUIPMENT AND INTANGIBLE ASSETS: UTILIZATION AND DISPOSITION Overview This chapter completes our discussion of accounting for property, plant, and equipment and intangible assets. We address the allocation of the cost of these assets to the […]

978-1259722660 Chapter 10 Solution Manual Part 9

Judgment Case 10–9 Requirement 1 The costs of research equipment used exclusively for Trouver would be reported as research and development expenses in the period incurred. The costs of research equipment used on both Trouver and future research Requirement 2 […]

978-1259722660 Chapter 10 Solution Manual Part 8

Judgment Case 10–1 Requirement 1 All costs necessary to bring the land to its condition for use should be capitalized as the cost of the land. This should include the following costs: Purchase price. Title insurance. Requirement 2 Assets acquired […]

978-1259722660 Chapter 10 Solution Manual Part 7

Problem 10–8 Case A. Requirement 1 Book value less fair value = loss on exchange Fair value of old tractor + cash given = Initial value of new tractor $9,000 + 20,000 = $29,000 Journal entry (not required): New tractor […]

978-1259722660 Chapter 10 Solution Manual Part 6

Exercise 10–32 Requirement 1 2018: ………………………………………………………………………..Cash ……………………………………………………………………………..2,200,000 2019: Research and development expense……………………………. 800,000 Software development costs ……………………………………… 400,000 ………………………………………………………………………..Cash ……………………………………………………………………………..1,200,000 Requirement 2 (1) Percentage-of-revenue method: $1,000,000 = 20% × $400,000 = $80,000 $5,000,000 (2) Straight-line method: 1/4 or 25% × […]

978-1259722660 Chapter 10 Solution Manual Part 5

Exercise 10–22 Average accumulated expenditures: Interest capitalized: $3,000,000 – 1 ,500,000 (construction loan) x 10% = $150,000 $1,500,000 x 7%* = 105 ,000 $255 ,000 = interest capitalized * Weighted-average rate of all other debt: $2,000,000 x 9% = $180,000 […]

978-1259722660 Chapter 10 Solution Manual Part 4

Exercise 10–18 Requirement 1 Fair value of old land + Cash given = Fair value of new land Requirement 2 Land—new ($72,000 + 14,000)…………………………………… 86,000 ……………………………………………………………………..Cash …………………………………………………………………………14,000 ……………………………………………..Land—old (book value) …………………………………………………………………………30,000 ……………………………………………………………….Gain ($72,000 – 30,000) …………………………………………………………………………42,000 Requirement 3 Land—new ($30,000 […]

978-1259722660 Chapter 10 Solution Manual Part 3

Exercise 10–5 Patent ($200,000 + 10,000)…………………………………………. 210,000 ……………………………………………………………………..Cash ……………………………………………………………………….935,000 *The ongoing expense each month of operating as a franchise would be expensed as incurred. Exercise 10–6 Calculation of goodwill: Consideration exchanged $17,000,000 Less fair value of net assets: Assets $23,000,000 […]

978-1259722660 Chapter 10 Solution Manual Part 2

Brief Exercise 10–4 Cost of silver mine: Acquisition, exploration, and development $5,600,000 *Present value of $1, n = 5, i = 6% (from Table 2) Brief Exercise 10–5 After one year, the liability will increase to $455,456. ($429,675† + ($429,675 […]

978-1259722660 Chapter 10 Solution Manual Part 1

Question 10–1 The difference between tangible and intangible long-lived, revenue-producing Question 10–2 The cost of property, plant, and equipment and intangible assets includes the purchase price (less any discounts received from the seller); transportation costs paid by the buyer to […]

978-1259722660 Chapter 10 Lecture Note Part 2

Suggestions for Class Activities 1. Guest Speaker The assigning of fair value to assets acquired in an acquisition is an interesting topic for students. The accounting issues are interesting, as are the valuation issues. Through your contacts at local CPA […]

978-1259722660 Chapter 10 Lecture Note Part 1

CHAPTER 10 PROPERTY, PLANT, AND EQUIPMENT AND INTANGIBLE ASSETS: ACQUISITION Overview This chapter and the one that follows address the measurement and reporting issues involving property, plant, and equipment and intangible assets, the tangible and intangible long-lived assets that are […]

978-1259722660 Chapter 9 Solution Manual Part 10

Real World Case 9–8 Requirement 1 Inventories are valued using the retail first-in, first-out method for goods in Requirement 2 The company uses the Producer Price Index in applying the dollar-value LIFO retail method to its pharmacy department inventories. Requirement […]

978-1259722660 Chapter 9 Solution Manual Part 9

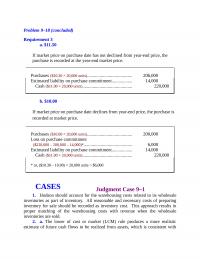

Problem 9–18 (concluded) Requirement 3 a. $11.50 If market price on purchase date has not declined from year-end price, the purchase is recorded at the year-end market price. b. $10.00 If market price on purchase date declines from year-end price, […]

978-1259722660 Chapter 9 Solution Manual Part 8

Problem 9–13 (continued) 2018 Step 1 Step 2 Step 3 Ending Ending Inventory Inventory Inventory Inventory Layers Layers at Year-End at Base Year at Base Year Converted to Retail Prices Retail Prices Retail Prices Cost $206,000 $206,000 = $200,000 $150,000 […]

978-1259722660 Chapter 9 Solution Manual Part 7

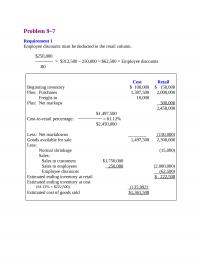

Problem 9–7 Requirement 1 Employee discounts must be deducted in the retail column. Cost Retail Beginning inventory $ 100,000 $ 150,000 Plus: Purchases 1,387,500 2,000,000 Freight-in 10,000 Plus: Net markups 300 ,000 2,450,000 $1,497,500 Cost-to-retail percentage: = 61.12% $2,450,000 Less: […]

978-1259722660 Chapter 9 Solution Manual Part 6

Exercise 9–31 If market price is less than the contract price, the purchase is recorded at the market price. June 15, 2018 Purchases (market price)………………………………………………… 85,000 If market price at year-end is less than contract price for outstanding purchase commitments, […]

978-1259722660 Chapter 9 Solution Manual Part 5

Exercise 9–24 Requirement 1 Requirement 2 Effect on cost of goods sold: Decrease in beginning inventory ($78,000 – 71,000) – $7,000 Decrease in ending inventory ($83,000 – 78,000) + 5 ,000 Decrease in cost of goods sold $2 ,000 Cost […]

978-1259722660 Chapter 9 Solution Manual Part 4

Exercise 9–15 Cost Retail Beginning inventory $160 ,000 $ 280 ,000 Plus: Net purchases 607,760 840,000 Estimated ending inventory at cost: Retail Cost Beginning inventory $280,000 $160,000 Current period’s layer 56 ,000 × 71% = 39,760 Total $336 ,000 $199,760 […]

978-1259722660 Chapter 9 Solution Manual Part 3

Exercise 9–3 Requirement 1 (1) (2) Product Cost NRV Inventory Value [Lower of (1) and (2)] 101 $120,000 $100,000 $100,000 The inventory value is $270,000. Requirement 2 Write-down of inventory: $300,000 – 270,000 = $30,000 Cost of Goods Sold* 30,000 […]

978-1259722660 Chapter 9 Solution Manual Part 2

Brief Exercise 9–8 Cost Retail Beginning inventory $ 300 ,000 $ 450 ,000 Estimated ending inventory at cost: Retail Cost Beginning inventory $ 450,000 $ 300,000 Current period’s layer 40 ,000 × 71.21 % = 28,484 Total $ 490 ,000 […]

978-1259722660 Chapter 9 Solution Manual Part 1

978-1259722660 Chapter 9 Lecture Note Part 1

CHAPTER 9 INVENTORIES: ADDITIONAL ISSUES Overview We covered most of the principal measurement and reporting issues involving the asset inventory and the corresponding expense cost of goods sold in the previous chapter. In this chapter, we complete our discussion of […]

978-1259722660 Chapter 8 Solution Manual Part 8

Communication Case 8–4 Suggested Grading Concepts and Grading Scheme: Content (70%) _______ Prices are increasing. _______ Prices are decreasing. ________ 25 Discusses the various motivating factors that might influence the choice of inventory method. _______ The actual physical flow of […]

978-1259722660 Chapter 8 Solution Manual Part 7

Problem 8–9 Requirement 1 Beginning inventory $ 450,000 Purchases: Cost of ending inventory: Date of purchase UnitsUnit cost Total cost Beg. Inv. 10,000 $15 $150,000 Beg. Inv. 5,000 20 100,000 Totals 15,000 $250,000 Requirement 2 Cost of goods sold assuming […]

978-1259722660 Chapter 8 Solution Manual Part 6

Problem 8–4 Requirement 1 Beginning inventory (10,000 x $8.00) $ 80,000 Net purchases: * The 5,000 units purchased on December 28 are not included. The merchandise was shipped f.o.b. destination and did not arrive at Johnson’s warehouse until 2019. Cost […]

978-1259722660 Chapter 8 Solution Manual Part 5

Exercise 8–24 Ending Ending Inventory Inventory Layers Inventory Layers Inventory Date at Base Year Cost at Base Year Cost Converted to Cost DVL Cost 12/31/2018 $200,000 = $200,000 $200,000 (base) $200,000 x 1.00 = $200,000 $200,000 1.00 12/31/2019 $231,000 = […]

978-1259722660 Chapter 8 Solution Manual Part 4

Exercise 8–14 First-in, first-out (FIFO) Cost of goods sold: Date of Cost of Sale Units Sold Units Sold Total Cost Aug. 14 2,000 (from Beg. Inv.) $6.10 $12,200 Last-in, first-out (LIFO) Date Purchased Sold Balance Beginning inventory 2,000 @ $6.10 […]

978-1259722660 Chapter 8 Solution Manual Part 3

Air France–KLM Case Per note 4.16, AF uses the weighted-average method to value its inventory. Under IFRS, the FIFO (first-in, first-out) method also can be used. However, the LIFO (last-in, first-out) method, which can be used under U.S. GAAP in […]

978-1259722660 Chapter 8 Solution Manual Part 2

Brief Exercise 8–7 First-in, first-out (FIFO) Cost of goods sold: Date of Cost of Sale Units Sold Units Sold Total Cost January 10 125 (from Beg. Inv.) $25 $3,125 Ending inventory: Date of Purchase Units Unit Cost Total Cost January […]

978-1259722660 Chapter 8 Solution Manual Part 1

Question 8–1 Question 8–2 Question 8–3 Perpetual System Periodic System (1) Purchase of merchandise debit inventory debit purchases Solutions Manual, Vol.1, Chapter 8 8–1 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written […]