Archives: Solution Manual

978-1259722660 Chapter 8 Lecture Note Part 2

Assignment Chart Learning Est. time Questions Objective(s) Topic (min.) 8–1 3 Types of inventory for a manufacturer 5 8–2 1 Perpetual versus period inventory systems 5 8–3 1 Perpetual versus period inventory systems 5 8–4 2 f.o.b. shipping point versus […]

978-1259722660 Chapter 8 Lecture Note Part 1

CHAPTER 8 INVENTORIES: MEASUREMENT Overview The next two chapters continue our study of assets by investigating the measurement and reporting issues involving inventories and the related expense—cost of goods sold. Inventory refers to the assets a company (1) intends to […]

978-1259722660 Chapter 7 Solution Manual Part 10

Integrating Case 7–8 McLaughlin’s underestimation of bad debts is treated as a change in accounting estimate. Changes in estimates are accounted for prospectively. When a company revises a previous estimate, prior financial statements are not restated. Instead, the company merely […]

978-1259722660 Chapter 7 Solution Manual Part 9

Judgment Case 7–3 Requirement 1 a. Hogan should account for the sales discounts at the date of sale using the Revenues should be recorded at the cash equivalent price at the date of sale. Under the net method, the sale […]

978-1259722660 Chapter 7 Solution Manual Part 8

Problem 7–15 National Bank would recognize $3,359,005 of impairment, because it is not probable that a loss will occur. ANALYSIS Previous Value: New Value: Interest $500,000 x 3.99271 * =$ 1,996,355 Principal $8 million x 0.68058 ** =5 ,444,640 Present […]

978-1259722660 Chapter 7 Solution Manual Part 7

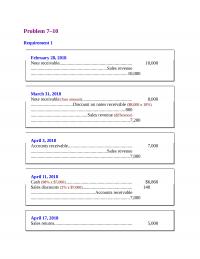

Problem 7–10 Requirement 1 February 28, 2018 Note receivable……………………………………………………… 10,000 …………………………………………………………Sales revenue …………………………………………………………………………10,000 March 31, 2018 Note receivable (face amount)……………………………………. 8,000 ………………………………Discount on notes receivable ($8,000 x 10%) ……………………………………………………………………….800 ………………………………………….Sales revenue (difference) …………………………………………………………………………..7,200 April 3, 2018 Accounts receivable……………………………………………….. 7,000 …………………………………………………………Sales […]

978-1259722660 Chapter 7 Solution Manual Part 6

Problem 7–4 Requirement 1 To record accounts receivable written off during the year 2018: ………………………………………………..Accounts receivable …………………………………………………………………………35,000 To record collection of account receivable previously written off: Accounts receivable……………………………………………….. 3,000 ………………………..Allowance for uncollectible accounts …………………………………………………………………………..3,000 Cash…………………………………………………………………….. 3,000 ………………………………………………..Accounts receivable …………………………………………………………………………..3,000 Requirement […]

978-1259722660 Chapter 7 Solution Manual Part 5

Exercise 7–30 Requirement 1 Step 1: Bank Balance to Corrected Balance Balance per bank statement $38,018 Step 2: Book Balance to Corrected Balance Balance per books $38,918 Add: Error in recording cash receipt ($2,000 – 200) 1,800 Deduct: Service charges […]

978-1259722660 Chapter 7 Solution Manual Part 4

Exercise 7–15 Requirement 1 June 30, 2018 Note receivable (face amount)……………………………………. 30,000 December 31, 2018 Discount on note receivable ……………………………………. 1,200 ………………………………………………..Interest revenue ($30,000 x 8% x 6/12) …………………………………………………………………………..1,200 March 31, 2019 Discount on note receivable ……………………………………. 600 ………………………………………………..Interest revenue […]

978-1259722660 Chapter 7 Solution Manual Part 3

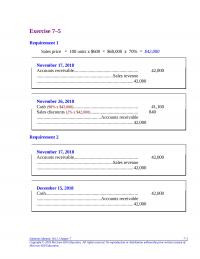

Exercise 7–5 Requirement 1 November 17, 2018 Accounts receivable……………………………………………….. 42,000 …………………………………………………………Sales revenue …………………………………………………………………………42,000 November 26, 2018 Cash (98% x $42,000)……………………………………………….. 41,160 Sales discounts (2% x $42,000)………………………………….. 840 ………………………………………………..Accounts receivable …………………………………………………………………………42,000 Requirement 2 November 17, 2018 Accounts receivable……………………………………………….. 42,000 …………………………………………………………Sales revenue […]

978-1259722660 Chapter 7 Solution Manual Part 2

Brief Exercise 7–10 (1)Allowance for uncollectible accounts: Beginning balance $ 25,000 Deduct: Write-offs (16,000) Required allowance (33 ,400)* Bad debt expense $24,400 (2) Required allowance = $334,000** x 10% = $33,400* Accounts receivable: Beginning balance $ 300,000 Add: Credit sales […]

978-1259722660 Chapter 7 Solution Manual Part 1

Question 7–1 Cash equivalents usually include negotiable instruments as well as highly Question 7–2 Internal control procedures involving accounting functions are intended to improve the accuracy and reliability of accounting information and to safeguard the company’s assets. The separation of […]

978-1259722660 Chapter 7 Lecture Note Part 2

Suggestions for Class Activities 1. Real World Scenario The following is an excerpt from a December 18, 2000, article on TheStreet.com titled “Cisco Triples Bad-Account Provision as Cash Crunch Deepens.” The article discusses an increase in bad debts for Cisco […]

978-1259722660 Chapter 7 Lecture Note Part 1

CHAPTER 7 CASH AND RECEIVABLES Overview We begin our study of assets by looking at cash and receivables—the two assets typically listed first in a balance sheet. Internal control and classification in the balance sheet are key issues we address […]

978-1259722660 Chapter 6 Solution Manual Part 6

Real World Case 6–6 Requirement 1 The maturity value (face amount) can be determined by dividing the present value by the present value of $1 factor for 8 semiannual periods (end of 2015 – beginning of 2020) at the semiannual […]

978-1259722660 Chapter 6 Solution Manual Part 5

Problem 6–14 Requirement 1 Tinkers: Present value of an ordinary annuity of $1: n = 15, i = 11% (from Table 4) PV = $143,817 x 0.81162 = $116,725 Present value of $1: n = 2, i = 11% (from […]

978-1259722660 Chapter 6 Solution Manual Part 4

Problem 6–6 1. Present value of $1: n = ?, i = 8% (from Table 2, n = approximately 9 years) 2. Annuity factor = Annuity factor = $28,700 = 4.1000 $7,000 Present value of an ordinary annuity of $1: […]

978-1259722660 Chapter 6 Solution Manual Part 3

Exercise 6–16 PV = ? x 0.90573= 1,200 annuity amount PVA = $1,325 = $88 = Payment 14.99203 Present value of an ordinary annuity of $1: n = 18, i = 2% (from Table 4) Exercise 6–17 To determine the […]

978-1259722660 Chapter 6 Solution Manual Part 2

Exercise 6–3 Present value of $1: n = 10, i = 7% (from Table 2) 2. PV = $14,000 (0.39711) = $5,560 Present value of $1: n = 12, i = 8% (from Table 2) 3. PV = $25,000 (0.10367) […]

978-1259722660 Chapter 6 Solution Manual Part 1

Question 6–1 Question 6–2 Compound interest includes interest not only on the original invested amount but also on the accumulated interest from previous periods. Question 6–3 If interest is compounded more frequently than once a year, the effective rate or […]

978-1259722660 Chapter 6 Lecture Note

CHAPTER 6 TIME VALUE OF MONEY CONCEPTS Overview Time value of money concepts, specifically future value and present value, are essential in a variety of accounting situations. These concepts and the related computational procedures are the subjects of this chapter. […]

978-1259722660 Chapter 5 Solution Manual Part 16

Target Case Requirement 1 Target reports Sales revenue of $73,785 million for the 2015 fiscal year, which ended January 30, 2016. Requirement 2 Recording revenue at the point of sale indicates that Target records revenue at the Requirement 3 Target […]

978-1259722660 Chapter 5 Solution Manual Part 15

Communication Case 5–7 The critical question that student groups should address is how to account for The preferred solution should include the idea that the sale of an ice cream cone to a person who has a card involves two […]

978-1259722660 Chapter 5 Solution Manual Part 14

Problem 5–19 Requirement 1 a. January 30, 2018 Cash ……………………………………………………………………. 200,000 1,200,000 b. September 1, 2018 Deferred franchise fee revenue………………………………… 1,200,000 Franchise fee revenue ………………………………………… 1,200,000 c. September 30, 2018 Accounts receivable ($40,000 x 3%) …………………………… 1,200 Service revenue …………………………………………………. […]

978-1259722660 Chapter 5 Solution Manual Part 13

Problem 5–15 Requirement 1 2018 cost recovery % : $180,000 2019 cost recovery %: $280,000 = 70% (gross profit % = 30%) $400,000 2018 gross profit: Cash collection from 2018 sales = $120,000 x 40% = $48,000 2019 gross profit: […]

978-1259722660 Chapter 5 Solution Manual Part 12

Requirement 5 2018 2019 2020 Costs incurred during the year $2,400,000 $3,800,000 $3,900,000 2018 2019 2020 Contract price $10 ,000,000 $10 ,000,000 $10,000,000 Actual costs to date 2,400,000 6,200,000 10,100,000 Estimated costs to complete 5 ,600,000 4 ,100,000 – 0 […]

978-1259722660 Chapter 5 Solution Manual Part 11

Problem 5–6 Requirement 1 Cash 80,000 Deferred revenue 80,000 $80,000 is recognized as deferred revenue. Requirement 2 Deferred revenue ($80,000 ÷ 10) Bonus receivable ($40,000 ÷ 10) 8,000 4,000 Service revenue 12,000 Super Rise earns revenue of $12,000 associated in […]

978-1259722660 Chapter 5 Solution Manual Part 10

Problem 5-1 (concluded) Requirement 2 a. Number of performance obligations in the contract: 1. The access to the gym for 50 visits is one performance obligation. The option to is not a performance obligation in the contract. (Note: It could […]

978-1259722660 Chapter 5 Solution Manual Part 9

Exercise 5–29 (concluded) When payments are received, gain on sale of land is recognized, calculated by April 1, 2018 Cash…………………………………………………………………….. 120,000 Installment receivables……………………………………….. 120,000 To record cash collection from installment sale Deferred gain………………………………………………………… 96,000 Gain on sale of land (80% […]

978-1259722660 Chapter 5 Solution Manual Part 8

SUPPLEMENT EXERCISES Exercise 5–23 Requirement 1 2018 cost recovery %: $234,000 2019 cost recovery %: $245,000 = 70% (gross profit % = 30%) $350,000 2018 gross profit: Cash collection from 2018 sales of $150,000 x 35% = $52 ,500 2019 […]

978-1259722660 Chapter 5 Solution Manual Part 7

Exercise 5–21 SUMMARY Gr. Profit Recognized Over Time Gr. Profit Recognized Upon Completion Situation 2018 2019 2020 2018 2019 2020 1$166,667 $233,333 $100,000 $0 $0 $500,000 6$(100,000) $(100,000) $(100,000) $(100,000) $(100,000) $(100,000) Situation 1 – Revenue Recognized Over Time 2018 […]

978-1259722660 Chapter 5 Solution Manual Part 6

Exercise 5–16 The FASB Accounting Standards Codification® represents the single source of authoritative U.S. generally accepted accounting principles. Requirement 1 Regarding disclosures that are required with respect to performance the appropriate citation is: FASB ASC 606–10–50–12: “Revenue from Contracts with […]

978-1259722660 Chapter 5 Solution Manual Part 5

Exercise 5-8 Requirement 1 Number of performance obligations in the contract: 2. Delivery of keyboards is one performance obligation. The special discount being distinct, as it could be sold or provided separately, and it is separately identifiable, as it is […]

978-1259722660 Chapter 5 Solution Manual Part 4

Brief Exercise 5–40 Orange has separate sales prices for the two parts of LearnIt-Plus, so the that revenue will be deferred and recognized over the life of the one-year period in which the Office Hours are delivered. If LearnIt were […]

978-1259722660 Chapter 5 Solution Manual Part 3

Brief Exercise 5-11 Number of performance obligations in the contract: 1. The separate goods and services that Precision Equipment has agreed to provide each other. The contractor’s role is to integrate and customize them to create one automated assembly line. […]

978-1259722660 Chapter 5 Solution Manual Part 2

Question 5–21 Sometimes a company arranges for another company to sell its product under consignment. The “consignor” physically transfers the goods to the other company commission and approved expenses) to the consignor. Because the consignor retains the risks and rewards […]

978-1259722660 Chapter 5 Solution Manual Part 1

Chapter 5 Revenue Recognition and Profitability Analysis QUESTIONS FOR REVIEW OF KEY TOPICS Question 5–1 The five key steps in applying the core revenue recognition principle are: 1. Identify the contract with a customer. 5. Recognize revenue when (or as) […]

978-1259722660 Chapter 5 Lecture Note Part 2

Supplement: GAAP in Effect Prior to ASU No. 2014-09 I. Summary of GAAP Changes A. ASU No. 2014-09 replaced over 200 specific items of revenue recognition guidance. Illustration 5–S1 summarizes some important changes in GAAP that occurred. II. The Realization […]

978-1259722660 Chapter 5 Lecture Note Part 1

CHAPTER 5 REVENUE RECOGNITION Overview In Chapter 4, we discussed net income and its presentation in the income statement. In Chapter 5, we focus on revenue recognition, which determines when and how much revenue appears in the income statement. In […]

978-1259722660 Chapter 4 Solution Manual Part 12

Case 4–15 (concluded) 1. The company could have chosen to present the information in the two statements in a single, continuous statement of comprehensive income. 2. The company reported the following other comprehensive income items: a. Foreign currency translation adjustments. […]

978-1259722660 Chapter 4 Solution Manual Part 11

Judgment Case 4–6 Financial Statement Presentation Situation Treatment (a–g) (CO, BC, or RE) 1. a. CO 2. b. RE 3. e. CO 4. f. CO 5. a. CO 6. d. BC 7. c. RE Judgment Case 4–7 1. The loss […]

978-1259722660 Chapter 4 Solution Manual Part 10

Requirement 5 The current ratios of the two firms are comparable and within the range of the Current ratio = Current assets Current liabilities Metropolitan = $1,203.0 = 0.94 $1,280.2 Republic = $1,478.7 =0.83 $1,787.1 Acid-test ratio = Quick assets […]

978-1259722660 Chapter 4 Solution Manual Part 9

Requirement 2 The return on assets indicates a company’s overall J&J’s profitability is significantly higher than that of Pfizer. Rate of return on assets = Net income Total assets profitability, ignoring specific sources of financing. In this regard, J&J = […]

978-1259722660 Chapter 4 Solution Manual Part 8

Problem 4–8 DUKE COMPANY Statement of Comprehensive Income For the Year Ended December 31, 2018 Sales revenue ………………………………………………………… $15,000,000 Operating expenses: General and administrative …………………………………… $1,000,000 Selling ………………………………………………………………. 500,000 Restructuring costs ………………………………………………. 300,000 Loss from write-down of obsolete inventory …………… […]

978-1259722660 Chapter 4 Solution Manual Part 7

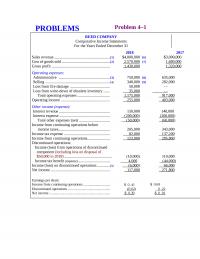

Problem 4–1 REED COMPANY Comparative Income Statements For the Years Ended December 31 2018 2017 Sales revenue …………………………………………………[1] $4,000,000 [6] $3,000,000 Operating expenses: Administrative …………………………………………….[3] 750,000 [8] 635,000 Selling ………………………………………………………..[4] 340,000 [9] 282,000 Loss from fire damage ………………………………….. 50,000 – […]

978-1259722660 Chapter 4 Solution Manual Part 6

Exercise 4–23 The FASB Accounting Standards Codification® represents the single source of authoritative U.S. generally accepted accounting principles. The specific citation for each of the following items is: 1. The calculation of the weighted average number of shares for basic […]

978-1259722660 Chapter 4 Solution Manual Part 5

Exercise 4–16 (concluded) Requirement 2 WAINWRIGHT CORPORATION Statement of Cash Flows For the Month Ended March 31, 2018 Cash flows from operating activities: Collections from customers $ 55,000 Cash flows from investing activities: Purchase of equipment (10 ,000) Net cash […]

978-1259722660 Chapter 4 Solution Manual Part 4

Exercise 4–5 AXEL CORPORATION Income Statement For the Year Ended December 31, 2018 Sales revenue ………………………………………………. $ 592,000 Operating expenses: Selling …………………………………………………….. $67,000 Administrative …………………………………………. 87,000 Restructuring costs ……………………………………. 55 ,000 Total operating expenses …………………………. 209 ,000 Operating income ………………………………………… […]

978-1259722660 Chapter 4 Solution Manual Part 3

Brief Exercise 4–15 Receivables turnover ratio = Net sales Average accounts receivable (net) Receivables turnover ratio = $600,000 [$100,000 + 120,000] ÷ 2 Inventory turnover ratio = $400,000* [$80,000 + 60,000] ÷ 2 =5.45 times =5.71 times Inventory turnover ratio […]

978-1259722660 Chapter 4 Solution Manual Part 2

Brief Exercise 4–3 PACIFIC SCIENTIFIC CORPORATION Income Statement For the Year Ended December 31, 2018 ($ in millions) Operating expenses: Selling………………………………………………………. $126 General and administrative………………………….. 105 Total operating expenses …………………………. 231 Operating income ………………………………………… 635 Other income (expense): Gain on […]