Archives: Solution Manual

978-1259722660 Chapter 18 Solution Manual Part 9

Real World Case 18–1 Requirement 1 Assuming the shares are issued at the midpoint of the price range indicated, Requirement 2 $ in millions Cash (determined above)…………………………………………………..398.750 Common stock (27.5 million shares x $.01 par)…………………. .275 Paid-in capital—excess of par […]

978-1259722660 Chapter 18 Solution Manual Part 8

Problem 18–11 A stock dividend is the distribution of additional shares of stock to current shareholders of the corporation. The investor receives no assets, only additional shares. Because each shareholder receives the same percentage increase in To record the investment […]

978-1259722660 Chapter 18 Solution Manual Part 7

Problem 18–6 Requirement 1 2018 ($ in millions) Cash……………………………………………………………………………. 480 Preferred stock (1 million shares x $10 par per share)…………… 10 Paid-in capital—excess of par, preferred……………………… 470 Cash……………………………………………………………………………. 70 2019 ($ in millions) Common stock (3 million shares x $1 […]

978-1259722660 Chapter 18 Solution Manual Part 6

Problem 18–3 Requirement 1 February 15, 2018 (a) Retired Common stock (300,000 shares x $1 par)…………………….. 300,000 (b) Accounted for as treasury stock Treasury stock (300,000 shares x $8)………………………….. 2,400,000 Cash (300,000 shares x $8)……………………………………. 2,400,000 February 17, 2019 (a) […]

978-1259722660 Chapter 18 Solution Manual Part 5

Exercise 18–22 The FASB Accounting Standards Codification represents the single source of authoritative U.S. generally accepted accounting principles. The specific citation for each of the following items is: 1. Disclosure for the pertinent rights and privileges of the various securities […]

978-1259722660 Chapter 18 Solution Manual Part 4

Exercise 18–12 1. January 23, 2018 ($ in millions) 2. September 3, 2018 Cash (1 million shares x $21)……………………………………………… 21 Treasury stock (1 million shares x $20)…………………………….. 20 Paid-in capital—share repurchase (remainder)………………… 1 3. November 4, 2018 Cash (1 million […]

978-1259722660 Chapter 18 Solution Manual Part 3

Exercise 18–2 Requirement 1 The specific citation that describes the guidelines for presenting accumulated other comprehensive income on the statement of shareholders’ equity is FASB ASC Requirement 2 45-14 The total of other comprehensive income for a period shall be […]

978-1259722660 Chapter 18 Solution Manual Part 2

Brief Exercise 18–5 Horton’s total paid-in capital will decline by $17 million, the price paid to buy back the shares. Journal entry (not required): ($ in millions) Common stock (2 million shares x $1 par)……………………………. 2 * Paid-in capital—excess of […]

978-1259722660 Chapter 18 Solution Manual Part 1

AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty may approach assessment and its documentation differently, one approach is to provide specific questions on exams that become the basis […]

978-1259722660 Chapter 18 Lecture Note Part 2

5. Professional Skills Development Activities The following are suggested assignments from the end-of-chapter material that will help your students develop their communication, research, analysis, and judgment skills. Communication Skills. Analysis Case 18–2, Exercise 18–23, and Problem 18–6 are suitable for […]

978-1259722660 Chapter 18 Lecture Note Part 1

CHAPTER 18 SHAREHOLDERS’ EQUITY Overview We turn our attention in this chapter from liabilities, which represent the creditors’ interests in the assets of a corporation, to the shareholders’ residual interest in those assets. The discussions distinguish between the two basic […]

978-1259722660 Chapter 17 Solution Manual Part 13

Real World Case 17–7 Requirement 1 FedEx sponsors both defined benefit and defined contribution pension plans as well as a postretirement healthcare plan. These are described in disclosure note 13 (in part) for the years ended May 31, 2015 and […]

978-1259722660 Chapter 17 Solution Manual Part 12

Case 17–1 (continued) Requirement 2 The value of your plan assets as of the anticipated retirement date is $1,872,981: A B C D E End of Years to Future Value Year: Retirement Salary Contribution at Retirement 2018 39 100,000 8,000 […]

978-1259722660 Chapter 17 Solution Manual Part 11

Problem 17–17 (concluded) Requirement 2 GLOBAL COMMUNICATIONS Statement of Comprehensive Income Year ended December 31, 2018 Net income $300.0 Other comprehensive income: Net unrealized holding gain on investments ($30, net of $12 tax) $ 18.0 Loss on pensions—PBO estimate ($23, […]

978-1259722660 Chapter 17 Solution Manual Part 10

Problem 17–15 ( )s indicate credits; debits otherwise ($ in 000s) PBO Plan Assets Prior Service Cost –AOCI Net Loss –AOCI Pension Expense Cash Net Pension (Liability) / Asset Balance, Jan. 1, 2018 (4100) 4530 840 477 430 Service cost2(332) […]

978-1259722660 Chapter 17 Solution Manual Part 9

Problem 17–10 (concluded) Requirement 3 ($ in millions) PBO balance, January 1 $480 Service cost 75 Plan assets balance, January 1 $300 Actual return on plan assets 20 Contributions 2018 60 Benefits paid (36 ) Plan assets balance, December 31 $344 Because […]

978-1259722660 Chapter 17 Solution Manual Part 8

Problem 17–6 1. Projected Benefit Obligation ($ in 000s) Balance, January 1, 2018 $ 0 Service cost 150 2. Plan Assets Balance, January 1, 2018 $ 0 Actual return on plan assets (10% x $0) 0 Contributions, 2018 160 Benefits […]

978-1259722660 Chapter 17 Solution Manual Part 7

Exercise 17–29 Requirement 1 ($ in millions) Service cost $34 Requirement 2 ($ in millions) Postretirement benefit expense (calculated above)…………………… 47 Amortization of prior service cost—OCI (amortization)*……. 1 APBO ($34 service cost + $12 interest cost)…………………………… 46 The amortization amount […]

978-1259722660 Chapter 17 Solution Manual Part 6

Exercise 17–21 Requirement 1 ($ in millions) Service cost $ 60 Interest cost 27 * Since the amendment was at the end of the year, there is no amortization of prior service cost in 2018. Requirement 2 ($ in millions) […]

978-1259722660 Chapter 17 Solution Manual Part 5

978-1259722660 Chapter 17 Solution Manual Part 4

Exercise 17–15 PBO Plan Assets Prior Service Cost –AOCI Net Gain –AOCI Pension Expense Cash Net Pension (Liability ) / Asset Balance, Jan. 1, 2018 (800) 600 114 80 (200) Service cost (84) 84 (84) Interest cost, 5% (40) 40 […]

978-1259722660 Chapter 17 Solution Manual Part 3

Exercise 17–4 Requirement 1 ($ in millions) Pension expense (total)…………………………………………… 14 Requirement 2 ($ in millions) Pension expense (total)…………………………………………… 10 Plan assets (expected return on assets)………………………….. 4 Amortization of net gain—OCI (current amortization)* ….. 2 PBO ($10 service cost + […]

978-1259722660 Chapter 17 Solution Manual Part 2

Brief Exercise 17–1 ($ in millions) Beginning of the year PBO $80 Service cost 10 Brief Exercise 17–2 ($ in millions) Beginning of the year PBO $80 Service cost ? Interest cost 4 (5% x $80) Loss (gain) on […]

978-1259722660 Chapter 17 Solution Manual Part 1

AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty may approach assessment and its documentation differently, one approach is to provide specific questions on exams that become the basis […]

978-1259722660 Chapter 17 Lecture Note Part 3

Assignment Chart Learning Est. time Questions Objective(s) Topic (min.) 17–1 1 Motivation to offer a pension plan 5 17–2 1 Qualified pension plans 5 17–3 1 What type of pension plan? 5 17–4 2 What is the vested benefit obligation? […]

978-1259722660 Chapter 17 Lecture Note Part 2

PowerPoint Slides Two PowerPoint presentations of the chapter are available in the Connect Library: 1. With “Concept Checks” useful for classroom presentation, permitting the instructor to intersperse in the presentation short exercises students can be asked to solve individually or […]

978-1259722660 Chapter 17 Lecture Note Part 1

CHAPTER 17 PENSIONS AND OTHER POSTRETIREMENT BENEFITS Overview Employee compensation comes in many forms. Salaries and wages, of course, provide direct and current payment for services provided. However, it’s commonplace for compensation also to include benefits payable after retirement. We […]

978-1259722660 Chapter 16 Solution Manual Part 11

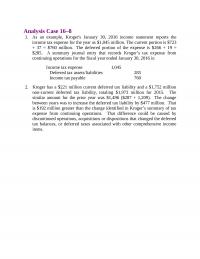

Analysis Case 16–8 1. As an example, Kroger’s January 30, 2016 income statement reports the income tax expense for the year as $1,045 million. The current portion is $723 Income tax expense 1,045 Deferred tax assets/liabilities 285 Income tax payable […]

978-1259722660 Chapter 16 Solution Manual Part 10

Analysis Case 16–1 Requirement 1 Temporary differences originate in one or more years and reverse in one or more future years. Differing depreciation methods are a common example of a Requirement 2 Intraperiod tax allocation allocates the total income tax […]

978-1259722660 Chapter 16 Solution Manual Part 9

Problem 16–11 Requirement 1 Deferred tax assets are recognized for all deductible temporary differences and operating loss carryforwards. Deferred tax assets are then reduced by a valuation allowance if it is “more likely than not” that some portion or all […]

978-1259722660 Chapter 16 Solution Manual Part 8

Problem 16–8 (continued) Journal entry at the end of 2018 Income tax expense (to balance) 52 * Temporary difference for subscriptions: 2017 2018 2019 Earned in current yr. (reported on income statement) $25 $33 Collected in prior yr., recognized in […]

978-1259722660 Chapter 16 Solution Manual Part 7

Problem 16–4 2018 2019 2020 2021 Pretax accounting income $60,000 $80,000 $70,000 $70,000 Cumulative Temporary 2018 2019 2020 2021 Difference Straight-line 30,000 30,000 30,000 30,000 Tax depreciation (39 ,600) (52 ,800) (18 ,000) (9 ,600) Temporary differences: (9,600) (22,800) 12,000 […]

978-1259722660 Chapter 16 Solution Manual Part 6

Exercise 16–30 Income Statement For the fiscal year ended March 31, 2018 ($ in millions) Revenues $ 830 Cost of goods sold (350 ) The FASB Accounting Standards Codification represents the single source of authoritative U.S. generally accepted accounting principles. […]

978-1259722660 Chapter 16 Solution Manual Part 5

Exercise 16–22 Requirement 1 ($ in thousands) Current Future Prior Years Year Deductible 2016 2017 2018 Amounts [total] Net operating loss (160) Deferred Tax Asset Deferred Tax Asset: 0 Ending balance (balance currently needed) $ 8 8Less: beginning balance […]

978-1259722660 Chapter 16 Solution Manual Part 4

Exercise 16–15 Requirement 1 ($ in millions) Current Future Year Deductible Amounts Total 2018 2019 2020 2021 2022 Pretax accounting income 14 Temporary difference: Deferred Tax Asset Deferred Tax Asset: 0 Ending balance (balance currently needed) $ 1.7 1.7 […]

978-1259722660 Chapter 16 Solution Manual Part 3

Exercise 16–7 1. Liability—loss contingency 2. Liability—deferred subscription revenue 3. Prepaid rent 4. Accrued bond interest payable 5. Prepaid insurance 6. Unrealized loss on investments (shareholders’ equity account) 7. Warranty liability 8. Liability—deferred rent revenue 9. Accumulated depreciation; and thus […]

978-1259722660 Chapter 16 Solution Manual Part 2

Brief Exercise 16–9 Current year Future taxable amount Pretax accounting income $ 900,000 Permanent difference: Taxable income (tax return) $ 760,000 Enacted tax rate 40% 40% Tax payable currently $ 304 ,000 Deferred tax liability $ 48,000 Journal entry Income […]

978-1259722660 Chapter 16 Solution Manual Part 1

_____________________________________________________________________________ Question 16–1 Income tax expense is comprised of both the current and the deferred tax consequences of events and transactions already recognized. Specifically, the $12.3 Question 16–2 Temporary differences between the reported amount of an asset or liability in […]

978-1259722660 Chapter 16 Lecture Note Part 2

Suggestions for Class Activities 1. Target Analysis Have students, individually or in groups, go to Target’s most recent annual report at Target’s website. Ask them to: 1. Determine the temporary difference that for Target creates the largest deferred assets and […]

978-1259722660 Chapter 16 Lecture Note Part 1

CHAPTER 16 ACCOUNTING FOR INCOME TAXES Overview In this chapter we explore financial accounting and reporting for the effects of income taxes. The discussion defines and illustrates temporary differences, which are the basis for recognizing deferred tax assets and deferred […]

978-1259722660 Chapter 15 Solution Manual Part 20

Communication Case 15-2 First, this case has no single right answer. The process of developing the proposed solutions will likely be more beneficial than the solutions themselves. Students should benefit from participating in the process, interacting first with other group […]

978-1259722660 Chapter 15 Solution Manual Part 19

Problem 15-29 (concluded) Calculations: September 30, 2018* Lease receivable (present value calculated above)…………. 6,000,000 December 31, 2018** Cash (lease payment)……………………………………………….. 391,548 Lease receivable (difference)………………………………… 223,294 Interest revenue (3% x [$6,000,000 – 391,548])………… 168,254 Equipment (lessor’s cost)……………………………………… 6,000,000 Cash (lease payment)……………………………………………….. […]

978-1259722660 Chapter 15 Solution Manual Part 18

Problem 15–26 Requirement 1 $5,000 .86384*** = $4,319 * Present value of $1: n = 1, i = 5%. ** Present value of $1: n = 2, i = 5%. *** Present value of $1: n = 3, i […]

978-1259722660 Chapter 15 Solution Manual Part 17

Problem 15-23 (connued) (a) by Western Soya Co. (the lessee) Since at least one (two in this case) classification criterion is met, this is a finance lease to the lessee. Western Soya records the present value of lease payments as […]

978-1259722660 Chapter 15 Solution Manual Part 16

Problem 15-22 Requirement 1 Lessor’s Calculation of Lease payments Amount to be recovered (fair value) $365,760 Less: Present value of the residual value ($25,000 x .68301*) (17 ,075) * present value of $1: n=4, i=10% ** present value of an […]

978-1259722660 Chapter 15 Solution Manual Part 15

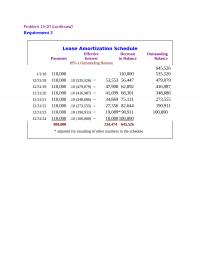

Problem 15-20 (connued) Requirement 3 Lease Amortization Schedule Effective Decrease Outstanding Payments Interest in Balance Balance 10% x Outstanding Balance 645,526 1/1/18 110,000 110,000 535,526 12/31/18 110,000 .10 (535,526) = 53,553 56,447 479,079 12/31/19 110,000 .10 (479,079) = 47,908 62,092 […]

978-1259722660 Chapter 15 Solution Manual Part 14

Problem 15-18 (connued) Requirement 10 December 31, 2021 Yard Art Landscaping (Lessee) Maintenance expense (2021 fee)……………………………………… 1,000 ………………….Prepaid maintenance expense (paid in 2020) …………………………………………………………………………..1,000 Branch Motors (Lessor) Cash (lease payment)…………………………………………………. 11,000 …..Maintenance fee payable [or prepaid maintenance*] …………………………………………………………………………..1,000 ……………Lease receivable […]

978-1259722660 Chapter 15 Solution Manual Part 13

Problem 15-17 (connued) Requirement 2 Branson Construction (Lessee) Interest expense (10% x [$936,492* – 100,000])………………… 83,649 ** present value of an annuity due of $1: n=20, i=10% Amortization expense ($936,492 ÷ 20 years)…………………….. 46,825 …………………………………………………..Right-of-use asset …………………………………………………………………………46,825 *** This debit […]

978-1259722660 Chapter 15 Solution Manual Part 12

Problem 15–13 Requirement 1 January 1, 2018 Present Value of Lease Payments for Lessee Present value of periodic lease payments Plus: Present value of the excess lessee-guaranteed residual value ($40,000 x .82270*) 32 ,908 Present value of lease payments $742 […]

978-1259722660 Chapter 15 Solution Manual Part 11

Problem 15-9 Situation 1 2 3 4 A. The lessor’s: 1. Lease payments1$40,000 $40,000 $40,000 $33,000 B. The lessee’s: 4. Lease payments440,000 40,000 40,000 33,000 5. Right-of-use asset534,437 34,437 34,437 29,319 6. Lease payable634,437 34,437 34,437 29,319 1 ($10,000 x […]