Archives: Solution Manual

978-1259746741 chapter 4 Solution Manual

Chapter 4 Future Value, Present Value, and Interest Rates Conceptual and Analytical Problems 1. Compute the future value of $100 at an 8 percent interest rate 5, 10, and 15 years into the percent? (LO1) Answer: Future value in 5 […]

978-1259746741 chapter 3 Solution Manual

Chapter 3 Financial Instruments, Financial Markets, and Financial Institutions Conceptual and Analytical Problems 1. As the end of the month approaches, you realize that you probably will not be able to pay the might use to solve your dilemma. (LO1) […]

978-1259746741 chapter 2 Solution Manual

Chapter 2 Money and the Payments System Conceptual and Analytical Problems 1. Describe at least three ways you could pay for your morning cup of coffee. What are the advantages and disadvantages of each? (LO2) Money: This is the most […]

978-1259746741 chapter 1 Solution Manual

Chapter 1 An Introduction to Money and the Financial System Problems 1. List the financial transactions you have engaged in over the past week. How might Answer: Commercial purchases that you made likely used credit cards and debit cards. Fifty […]

978-1259722660 Chapter 21 Solution Manual Part 15

Research Case 21–9 Requirement 1 The specific citation that specifies the classification of notes payable to suppliers is Requirement 2 Specifically, paragraph 45–17a states that cash outflows for operating activities include payments to acquire materials for manufacture or goods for […]

978-1259722660 Chapter 21 Solution Manual Part 14

Analysis Case 21–5 Requirement 1 (a) Cash _________________________________________________________________ Beginning balance ? Beginning cash + Net increase in cash = Ending cash Beginning cash + 183 = 360 Beginning cash = 360 – 183 Beginning cash = 177 (b) Accounts Receivable […]

978-1259722660 Chapter 21 Solution Manual Part 13

Problem 21–21 (continued) INCOME STATEMENT ACCOUNTS Sales Investment Revenue ________________________ ________________________________ Gain on Sale of Treasury Bills Cost of Goods Sold ________________________ ________________________________ 2 180 __________ 2(3) (4) 180 Salaries Expense Depreciation Expense ________________________ ________________________________ 73 12 __________ (5) 73 […]

978-1259722660 Chapter 21 Solution Manual Part 12

Problem 21–19 (continued) INCOME STATEMENT ACCOUNTS Sales Dividend Revenue ________________________ ________________________________ Cost of Goods Sold Salaries Expense ________________________ ________________________________ 120 25 __________ (3) 120 (4) 25 Depreciation Expense Bad Debt Expense ________________________ ________________________________ 5 1 __________ (5) 5(1) 1 Interest […]

978-1259722660 Chapter 21 Solution Manual Part 11

METAGROBOLIZE INDUSTRIES Spreadsheet for the Statement of Cash Flows Dec.31 Changes Dec. 31 2017 Debits Credits 2018 Balance Sheet Assets: Cash 375 (15)205 580 Accounts receivable 450 (7)150 600 6 ,880 Liabilities: Accounts payable 450 (9)300 750 Accrued expenses 225 […]

978-1259722660 Chapter 21 Solution Manual Part 10

Problem 21–14 (continued) Spreadsheet for the Statement of Cash Flows (continued) Dec.31 Changes Dec. 31 2017 Debits Credits 2018 Statement of Cash Flows Operating activities: Net income (1)50 Adjustments for noncash effects: Depreciation expense (2)22 Bad debt expense (3) 8 […]

978-1259722660 Chapter 21 Solution Manual Part 9

ARDUOUS COMPANY Spreadsheet for the Statement of Cash Flows Dec.31 Changes Dec. 31 2017 Debits Credits 2018 Balance Sheet Assets: Cash 81 (21)28 109 Accounts receivable 194 (1) 4 190 Investment rev. receivable 4 (2) 2 6 1 ,211 Liabilities: […]

978-1259722660 Chapter 21 Solution Manual Part 8

METAGROBOLIZE INDUSTRIES Spreadsheet for the Statement of Cash Flows Dec.31 Changes Dec. 31 2017 Debits Credits 2018 Balance Sheet Assets: Cash 375 (14)205 580 Liabilities: Accounts payable 450 (4)300 750 Accrued expenses 225 (9)75 300 Lease liability—land 0 (2)20 X(2)150 […]

978-1259722660 Chapter 21 Solution Manual Part 7

WRIGHT COMPANY Spreadsheet for the Statement of Cash Flows Dec.31 Changes Dec. 31 2017 Debits Credits 2018 Balance Sheet Assets: Cash 30 (15)12 42 Accounts receivable 75 (1) 2 73 Liabilities: Accounts payable 35 (2) 7 28 Salaries payable 5 […]

978-1259722660 Chapter 21 Solution Manual Part 6

$ in millions Pension expense (given) 82 Plan assets (expected return) 90 Exercise 21–28 PBO ($112 service cost + $51 interest cost) 163 Amortization of net loss—OCI (given) 1 Amortization of prior service cost—OCI (given) 8 Plan assets 9 Gain—OCI […]

978-1259722660 Chapter 21 Solution Manual Part 5

Direct Method Cash Flows from Operating Activities: Cash received from customers $672 Cash paid to suppliers (234) The depreciation expense, patent amortization expense, and loss on sale of land are not cash flows. Indirect Method Cash Flows from Operating Activities: […]

978-1259722660 Chapter 21 Solution Manual Part 4

Exercise 21–15 Wilson would report the $3,000,000* investment in the commercial food The $391,548 ($195,774* + 195,774**) cash lease payments are divided into the interest portion and the principal portion. The interest portion, $84,127, is reported as cash outflows from […]

978-1259722660 Chapter 21 Solution Manual Part 3

Cost of Accounts Cash paid to Situation goods sold Inventory payable suppliers increase increase (decrease) (decrease) 2 200 6 0 206 2. Summary Entry Cost of goods sold 200 Inventory 6 Cash (paid to suppliers of goods) 206 3 200 […]

978-1259722660 Chapter 21 Solution Manual Part 2

($ in millions) Interest expense (10% x 1/2 x $380) 19 Agee would report the cash inflow of $380 million from the sale of the bonds as a cash inflow from financing activities in its statement of cash flows. The […]

978-1259722660 Chapter 21 Solution Manual Part 1

AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty may approach assessment and its documentation differently, one approach is to provide specific questions on exams that become the basis […]

978-1259722660 Chapter 21 Lecture Note Part 2

3. Spreadsheet Activity Have students create a functional spreadsheet in Excel or some other spreadsheet program capable of being used to help prepare a statement of cash flows. Suggest that the spreadsheet: 1. Accommodate debit and credit “explanations” for changes […]

978-1259722660 Chapter 21 Lecture Note Part 1

CHAPTER 21 THE STATEMENT OF CASH FLOWS REVISITED Overview The objective of financial reporting is to provide investors and creditors with useful information, primarily in the form of financial statements. The balance sheet and the income statement—the focus of your […]

978-1259722660 Chapter 20 Solution Manual Part 12

Judgment Case 20-10 Situation I 2.The change in estimate should be reflected in the current period and in future periods. Unlike a change in accounting principle, the change in accounting estimate should not be applied retrospectively. 3.This change in accounting […]

978-1259722660 Chapter 20 Solution Manual Part 11

Analysis Case 20-4 For changes not involving LIFO or changes from the LIFO method to another, the event is accounted for as a normal change in accounting principle. In general, we report voluntary changes in accounting principles retrospectively. This means […]

978-1259722660 Chapter 20 Solution Manual Part 10

Problem 20-16 Fair value adjustment calculation: Investment balance, December 31, 2018, as reported $250,000 Error adjustment 40,000 Corrected balance, 12/31/2018 $290,000 Fair value, 12/31/2018 (274,000) Fair value credit adjustment needed, 12/31/2018 $ 16,000 c. Loss–lawsuit……………………………………………………………. 130,000 Liability—lawsuit…………………………………………………. 130,000 d. Cost […]

978-1259722660 Chapter 20 Solution Manual Part 9

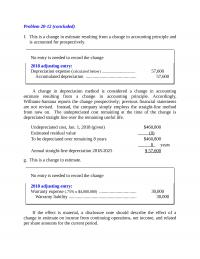

Problem 20-12 (concluded) f. This is a change in estimate resulting from a change in accounting principle and is accounted for prospectively. No entry is needed to record the change 2018 adjusting entry: A change in depreciation method is considered […]

978-1259722660 Chapter 20 Solution Manual Part 8

Problem 20-8 (concluded) A change in depreciation method is considered a change in accounting estimate resulting from a change in accounting principle. Accordingly, the Hoffman Group reports the change prospectively; previous financial statements are not revised. Instead, the company simply […]

978-1259722660 Chapter 20 Solution Manual Part 7

Problem 20-4 Requirement 1 To record the change: Retained earnings (net effect) ………………………………………….. 12,000 Note: For financial reporting purposes, but not for tax, the company is retrospectively decreasing accounting income, but not taxable income. This creates a temporary difference between […]

978-1259722660 Chapter 20 Solution Manual Part 6

Exercise 20-21 Requirement 1 The error caused both 2016 net income and 2017 net income to be overstated, so retained earnings is overstated by a total of $85,000. Also, the note payable would be understated by the same amount. Remember, […]

978-1259722660 Chapter 20 Solution Manual Part 5

Exercise 20-15 Requirement 1 A deferred tax liability is established using the currently enacted tax rate for the year(s) a temporary difference is expected to reverse. In this case that rate was ($ in millions) Income tax expense (to balance)………………………………………… […]

978-1259722660 Chapter 20 Solution Manual Part 4

Exercise 20-6 The FASB Accounting Standards Codification® represents the single source of authoritative U.S. generally accepted accounting principles. The specific citation for each of the following items is: 1. Reporting most changes in accounting principle: 2. Disclosure requirements for a […]

978-1259722660 Chapter 20 Solution Manual Part 3

Brief Exercise 20-12 (concluded) Error b 1. To include the $3 million in year 2018 purchases and increase retained earnings to what it would have been if 2017 cost of goods sold had not included the $3 million purchases. Analysis: […]

978-1259722660 Chapter 20 Solution Manual Part 2

Brief Exercise 20-1 To record the change: ($ in millions) Retained earnings ……………………………………………………………………………. 8.2 Inventory ($32 million – 23.8 million)………………………………. 8.2 B & B applies the average cost method retrospectively; that is, to all prior Then, the cumulative effects of […]

978-1259722660 Chapter 20 Solution Manual Part 1

AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty may approach assessment and its documentation differently, one approach is to provide specific questions on exams that become the basis […]

978-1259722660 Chapter 20 Lecture Note Part 2

3. Professional Skills Development Activities The following are suggested assignments from the end-of-chapter material that will help your students develop their communication, research, analysis, and judgment skills. Communication Skills. Ethics Case 20–3, Research Case 20–7, and Problem 20–10 are suitable […]

978-1259722660 Chapter 20 Lecture Note Part 1

CHAPTER 20 ACCOUNTING CHANGES AND ERROR CORRECTIONS Overview Chapter 4 provided a brief overview of accounting changes and error correction. Later, we discussed changes encountered in connection with specific assets and liabilities as we dealt with those topics in subsequent […]

978-1259722660 Chapter 19 Solution Manual Part 11

Case 19–12 (concluded) Requirement 2 Sometimes, the effect of potential common shares would be to increase, rather than decrease, EPS. These we refer to as “antidilutive” securities. Such securities are ignored when calculating both basic and diluted EPS. For example, […]

978-1259722660 Chapter 19 Solution Manual Part 10

Real World Case 19–7 Requirement 1 The note indicates that Best Buy does not include potentially dilutive shares of common stock when calculating EPS for the twelve months ended March 3, 2012. Requirement 2 Best Buy’s diluted earnings per share […]

978-1259722660 Chapter 19 Solution Manual Part 9

Problem 19–19 (continued) Requirement 2 (amounts in millions, except per share amount) 2019 Basic EPS net income shares at Jan. 1 2019 Diluted EPS net income $160 $160 —————————————————————————— = —— = $.50 300 + (30 – 20*) + (15 […]

978-1259722660 Chapter 19 Solution Manual Part 8

(amounts in millions, except per share amounts) Basic EPS net preferred income dividends shares at Jan. 1 The incremental effect of the conversion of the preferred stock is: preferred dividends +120* ————————————— = $3.75 +32 conversion of preferred stock The […]

978-1259722660 Chapter 19 Solution Manual Part 7

Problem 19–7 Requirement 1 No entry until the end of the reporting period, but compensation must be estimated at the grant date: options fair estimated expected value total to vest per option compensation Requirement 2 December 31, 2018, 2019, 2020, […]

978-1259722660 Chapter 19 Solution Manual Part 6

Requirement 1 We treat each individual vesting date as a separate award and allocate the compensation cost for each of the four groups (tranches) evenly over its individual vesting (service) period: Vesting Amount Fair Value Date Vesting per Option The […]

978-1259722660 Chapter 19 Solution Manual Part 5

Requirement 1 three-year vesting period, reducing earnings by $30 million each year. 2017 Compensation expense………………………………………………………….. 30 Paid-in capital—restricted stock………………………………………….. 30 2018 Compensation expense………………………………………………………….. 30 Paid-in capital—restricted stock………………………………………….. 30 Requirement 2 The total compensation for the award is $90 million ($5 […]

978-1259722660 Chapter 19 Solution Manual Part 4

1. EPS in 2018 (amounts in thousands, except per share amount) net Earnings income Per Share $400 $400 —————————————————————————— –––– = 2. EPS in 2019 (amounts in thousands, except per share amount) net Earnings income Per Share $400 $400 —————————————————————————— […]

978-1259722660 Chapter 19 Solution Manual Part 3

Exercise 19–2 Requirement 1 Requirement 2 no entry Requirement 3 ($ in millions) Compensation expense ($30 million ÷ 3 years)… 10 Paid-in capital—restricted stock…………….. 10 Requirement 4 Compensation expense ($30 million ÷ 3 years)… 10 Paid-in capital—restricted stock…………….. 10 Requirement […]

978-1259722660 Chapter 19 Solution Manual Part 2

Question 19–20 The accounting treatment of SARs depends on whether the award is considered an equity instrument or a liability. If the employer can choose to settle in shares rather than cash, the award is considered to be equity. If […]

978-1259722660 Chapter 19 Solution Manual Part 1

AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty may approach assessment and its documentation differently, one approach is to provide specific questions on exams that become the basis […]

978-1259722660 Chapter 19 Lecture Note Part 2

Suggestions for Class Activities 1. Research Activity Microsoft reported the following in a recent annual report: Employee Stock Purchase Plan. We have an employee stock purchase plan for all eligible employees. Compensation expense for the employee stock purchase plan is […]

978-1259722660 Chapter 19 Lecture Note Part 1

CHAPTER 19 SHARE-BASED COMPENSATION AND EARNINGS PER SHARE Overview We’ve discussed a variety of employee compensation plans in prior chapters, including pension and other postretirement benefits in Chapter 17. In this chapter we look at some common forms of compensation […]

978-1259722660 Chapter 18 Solution Manual Part 11

Research Case 18–9 The results students report will vary depending on the companies chosen. It Typical items that affect retained earnings are dividends (cash, property, or stock) and net income or loss. Treasury stock or retired stock transactions also affect […]

978-1259722660 Chapter 18 Solution Manual Part 10

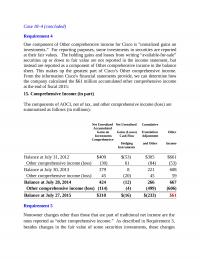

Case 18–4 (concluded) Requirement 4 One component of Other comprehensive income for Cisco is “unrealized gains on investments.” For reporting purposes, some investments in securities are reported at their fair values. The holding gains and losses from writing “available-for-sale” 15. […]