Chapter 4

Future Value, Present Value, and Interest Rates

Conceptual and Analytical Problems

1. Compute the future value of $100 at an 8 percent interest rate 5, 10, and 15 years into the

percent? (LO1)

Answer:

Future value in 5 years = $100 × (1.08)5 = $146.93

Future value in 15 years = $100 × (1.05)15 = $207.89

2. Compute the present value of a $100 investment made 6 months, 5 years, and 10 years from

now at 4 percent interest. (LO1)

Answer:6 months: Present Value = 100/(1.04)0.5 = $98.06

5 years: Present Value = 100/(1.04)5 = $82.19

Remember, you are calculating the present value of an investment to be made in the future.

3. Assuming that the current interest rate is 3 percent, compute the present value of a five-year,

to 4 percent? What happens when the interest rate goes to 2 percent? (LO2)

Answer:

Present Value for 5-year 5 percent coupon bond with face value of $1,000 (i = 3%) =

Present Value for 5-year 5 percent coupon bond with face value of $1,000 (i = 4%) =

The present value rises when the interest rate falls to 2 percent.

4. *Given a choice of two investments, would you choose one that pays a total return of 30

Answer: To compare the investments, you need to measure their returns in the same units.

One option would be to convert both these returns to annual rates. The first investment gives

0.5 percent per month for five years.

Alternatively, you could convert the first investment to a monthly return:

A third option would be to convert the monthly rate on the second investment into a 5-year

When converted to a common unit of measurement, we see that the second investment gives

5. A financial institution offers you a one-year certificate of deposit with an interest rate of 5

deposit? (LO3)

Answer: The real interest rate equals the nominal rate less the expected rate of inflation;

6. Consider two scenarios. In the first, the nominal interest rate is 6 percent and the expected

rate of inflation is 4 percent. In the second, the nominal interest rate is 5 percent and the

Answer: In the first scenario the real interest rate is 2 percent (the difference between the

real interest rate and so would rather borrow when the real rate is 2 percent (even though the

nominal interest rate is 6 percent).

7. You decide you would like to retire at age 65, and expect to live until you are 85 (assume

on $50,000 per year. (LO3)

a. Describe the calculation you need to make to determine how much you must save to

interest rate is 7 percent.

b. If you want to keep your purchasing power constant, how would your calculation change

b. If you want to have $50,000 in purchasing power for each year of your retirement,you

8. Most businesses replace their computers every two to three years. Assume that a computer

is thrown away. (LO1)

a. If the interest rate for financing the equipment is equal to i, show how to compute the

b. Suppose the computer did not fully depreciate but still had a $250 value at the time it was

c. What if financing can only be had at a 10 percent interest rate? Calculate the minimum

(a).

Answer:

a. If x = minimum annual cash flow:

$2,000 = x/(1 + i) + x/(1 + i)2 + x/(1 + i)3

b. $2,000 = x/(1 + i) + x/(1 + i)2 + x/(1 + i)3 + $250/(1 + i)3

9. Some friends of yours have just had a child. Thinking ahead, and realizing the power of

assume there is no inflation and no tax on interest income used to pay college tuition and

expenses. (LO1)

a. If the interest rate is 5 percent, how much money will your friends need to put into their

b. What if the interest rate were 10 percent?

c. The chance that the price of a college education will be the same 18 years from now as it

today’s interest rate is 8 percent, what will your friend’s investment need to be?

d. Return to part (a), the case with a 5 percent interest rate and no inflation. Assume that your

required size of the two equal investments, made five years apart.

Answer:

c. If the price rises 3 percent per year, the cost of a college education in 18 years will be:

d. If x is the size of each investment:

$125,000 = x(1.05)18 + x(1.05)13

10. You are considering buying a new house, and have found that a $100,000, 30-year fixed-rate

mortgage is available with an interest rate of 7 percent. This mortgage requires 360 monthly

with the percentage change in the interest rate. (LO1)

0.006434

Using the equation from Appendix 4A:

($714 – $651)/$651 = 9.7% and the interest rate has risen by (8% – 7%) / 7% = 14.3%.

11. *Use the Fisher equation to explain in detail what a borrower is compensating a lender for

when he pays her a nominal rate of interest. (LO3)

Answer: The Fisher equation illustrates that the nominal interest rate (i) can be broken down

foregoing the use of her money for the duration of the loan and so needs to be compensated

for this opportunity cost.

12. If the current interest rate increases, what would you expect to happen to bond prices?

Explain. (LO2)

Answer: Interest rates and bond prices are inversely related so bond prices will fall when

payments.

13. Which would be most affected in the event of an interest rate increase– the price of a

Explain. (LO2)

Answer: The price of the bond with the later payments will fall by relatively more. The

divided by (1 + i)5, so the impact will be bigger in the latter case.

14. Under what circumstances might you be willing to pay more than $1,000 for a coupon bond

(LO2)

Answer: If the interest rate in the market were less than 10 percent, the present value of the

(1.08)2 +100/(1.08)3 +1,000/(1.08)3 = $1,051.54.

15. *Approximately how long would it take for an investment of $100 to reach $800 if you

between doubling the interest rate and doubling the initial investment? (LO1)

Answer: Using the rule of 72, we know that if the interest rate is 5 percent, it will take 72/5 =

take 43.2 years to reach $800.

half the time.

(You can check that your calculations are approximately correct using the future value

If $200 is invested at 5 percent, it will take 72/5 = 14.4 × 2 = 28.8 years reach $800 – which

investment.

16. Rather than spending $100 today on paint today, you decide to save the money until next

expected inflation rate is 10 percent? (LO3)

Answer: Saving $100 today means forgoing 10 cans of paint. Since the funds grow in

only 10 percent more next year; because the real interest rate is 10 percent. Note that, in this

example, the Fisher equation approximation of the real interest rate (the nominal rate less

17. Recently, some lucky person won the lottery. The lottery winnings were reported to be $85.5

a. Explain briefly why winning $2.85 million per year for 30 years is not equivalent to

b. The evening news interviewed a group of people the day after the winner was announced.

When asked, most of them responded that, if they were the lucky winner, they would take

payment?

Answer:

a. $2.85 million per year is not equivalent to winning $85.5 million because of the time

value of money. If you received all the money today, you could invest it and earn

the sum of the present values of the sequence of payments.

b. I would calculate which payment option gave me the highest present value. I would look

Another factor to consider would be whether the tax treatment was the same for both

options.

18. You are considering going to graduate school for a one-year master’s program. You have

done some research and believe that the master’s degree will add $5,000 per year to your

would you decide if this investment in your education were profitable? (LO1)

Answer: You should calculate the internal rate of return from completing the master’s

program. If the IRR is greater than 6 percent, then it will be profitable. The calculation is

Using a spreadsheet or financial calculator, we find the IRR is around 7 percent. As the IRR

19. Assuming the chances of being paid back are the same, would a nominal interest rate of 10

(LO3)

Answer: Lenders are concerned with the real return they receive. If the higher nominal

interest rate represents a higher real interest rate, then the lender will find it more attractive.

expected inflation of 1 percent and a real interest rate of 4 percent. It is the real, not the

nominal, interest rate that matters.

20. *Your firm has the opportunity to buy a perpetual motion machine to use in your business.

internal rate of return? (LO2)

Answer: Using the result in the appendix equation (A5) as n becomes arbitrarily large, we

21. *Suppose two parties agree that the expected inflation rate for the next year is 3 percent.

is 7 percent. If inflation for the year turns out to be 2 percent, who gains and who loses?

(LO3)

Answer: The ex ante real interest rate is 4 percent. This is what the borrower thinks he or she

is paying and the lender thinks he or she is earning. If inflation turns out to be lower than

than he or she anticipated.

22. An unusual development in the wake of the 2007-2009 financial crisis was that nominal

examples would the nominal interest rate be negative?

a. The real interest rate is 2 percent and the expected inflation rate is 1 percent.

Explain your choice. (LO3)

Answer:

Using the Fisher equation, i = r + πe, we can calculate the associated nominal interest rate for

each of the four examples above.

a. i = 3 percent

We see that the nominal interest is negative only in c), where the rate of deflation (negative

interest rate.

23. Suppose analysts agree that the losses resulting from climate change will reach x dollars 100

(LO1)

Answer:

From the present value formula, PV = FV/(1 + i)n, we can see that the PV of a given future

get wider as n increases at specified interest rates.

Data Exploration

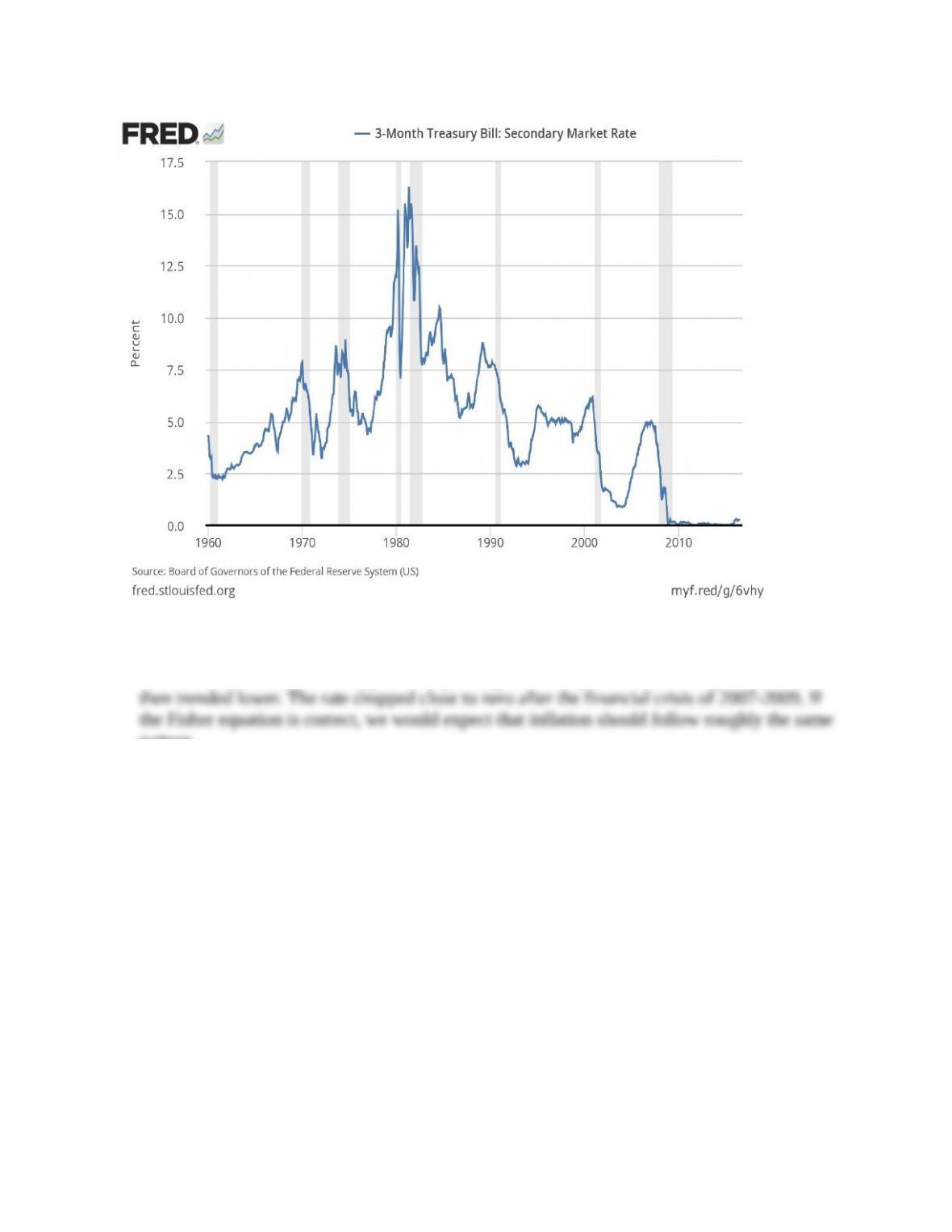

1. How does inflation affect nominal interest rates? (LO3)

a. Plot the three-month U.S. Treasury bill rate (FRED code: TB3MS) from 1960 to the

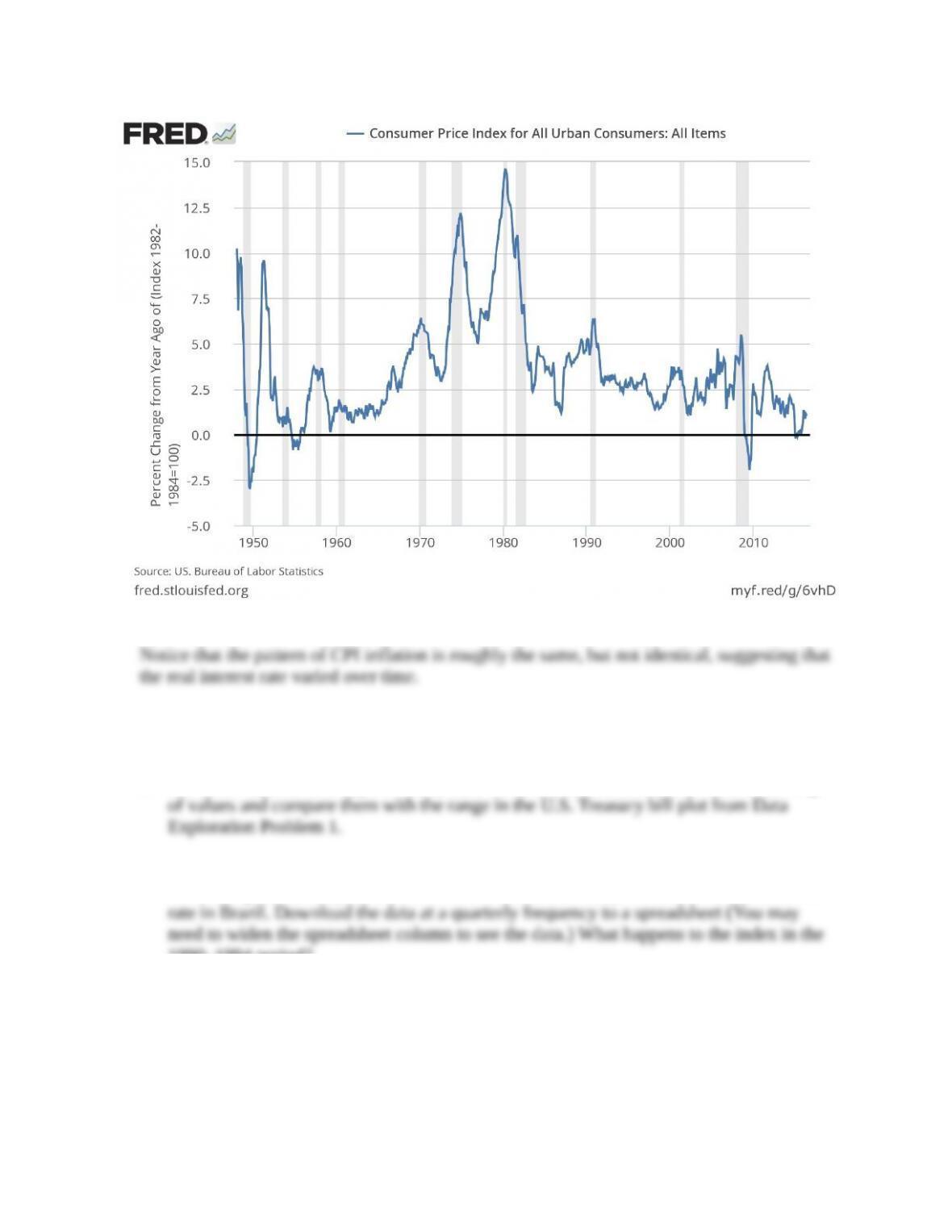

b. Plot the inflation rate based on the percent change from a year ago of the U.S.

U.S. inflation history reflect your explanation in part (a)?

Answer:

a. The data plot for the U.S. three- month Treasury bill is:

Notice that this rate trended higher until peaking above 15 percent in the early 1980s and

pattern.

b. The CPI plot is:

2. In Data Exploration Problem 1, you saw the impact of inflation in the U.S. on short-term

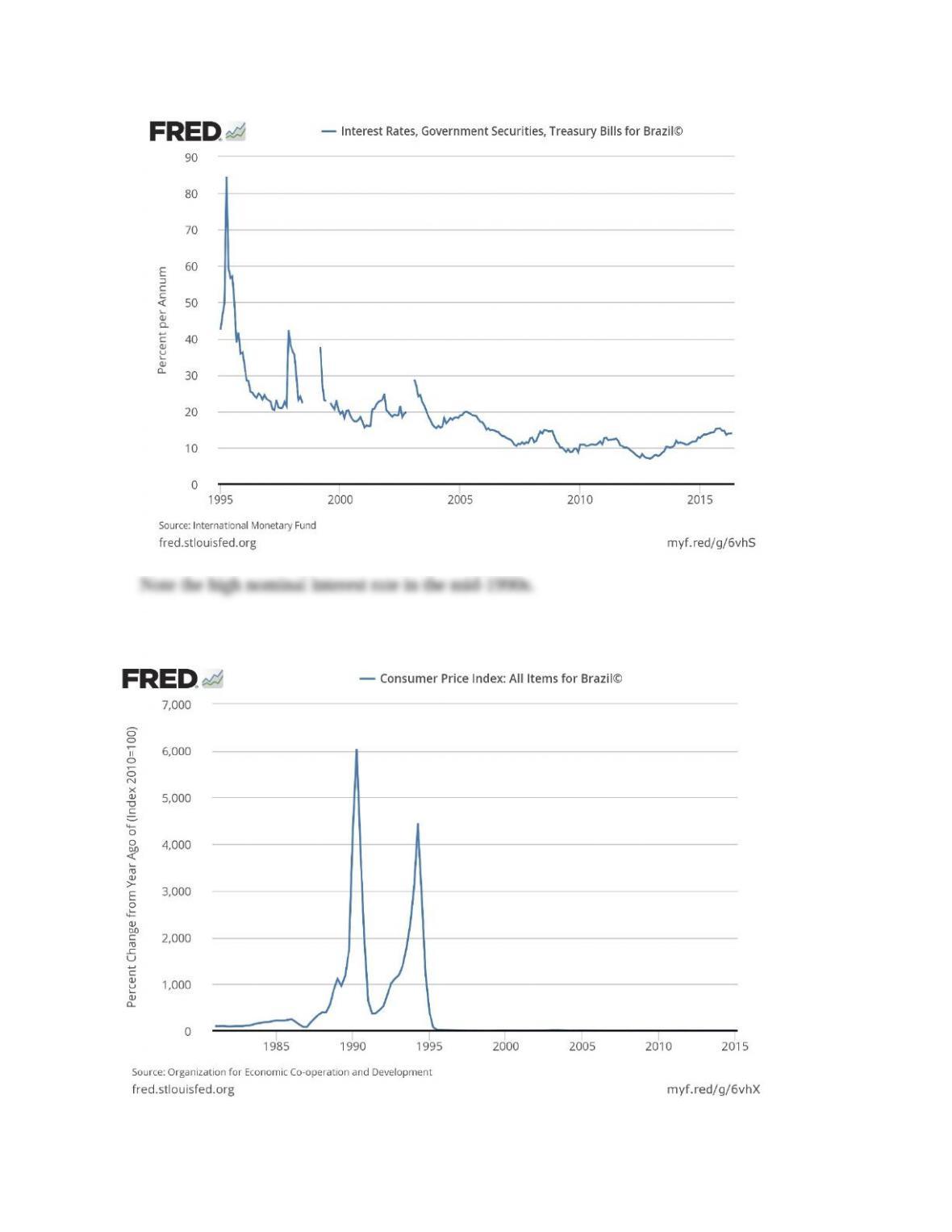

U.S. Treasury bill rates. Now examine similar data for Brazil. (LO3)

a. Plot the Brazilian Treasury bill rate (FRED code: INTGSTBRM193N). Notice the range

b. Plot the inflation rate based on the percent change from a year ago of the Brazilian

consumer price index (FRED code: BRACPIALLMINMEI). Comment on the inflation

1990–1994 period?

Answer:

a. The plot for the Brazilian interest rate is:

b. The plot for Brazilian inflation is:

Note the inflation in the mid-1990s approached 5,000 percent per year (following even

1990-01-01 0.000345

1990-04-01 0.000703

1990-07-01 0.000996

1994-04-01 19.719672

1994-07-01 29.926005

1994-10-01 31.978231

As the inflation plot implies, the values of the price index show explosive growth.

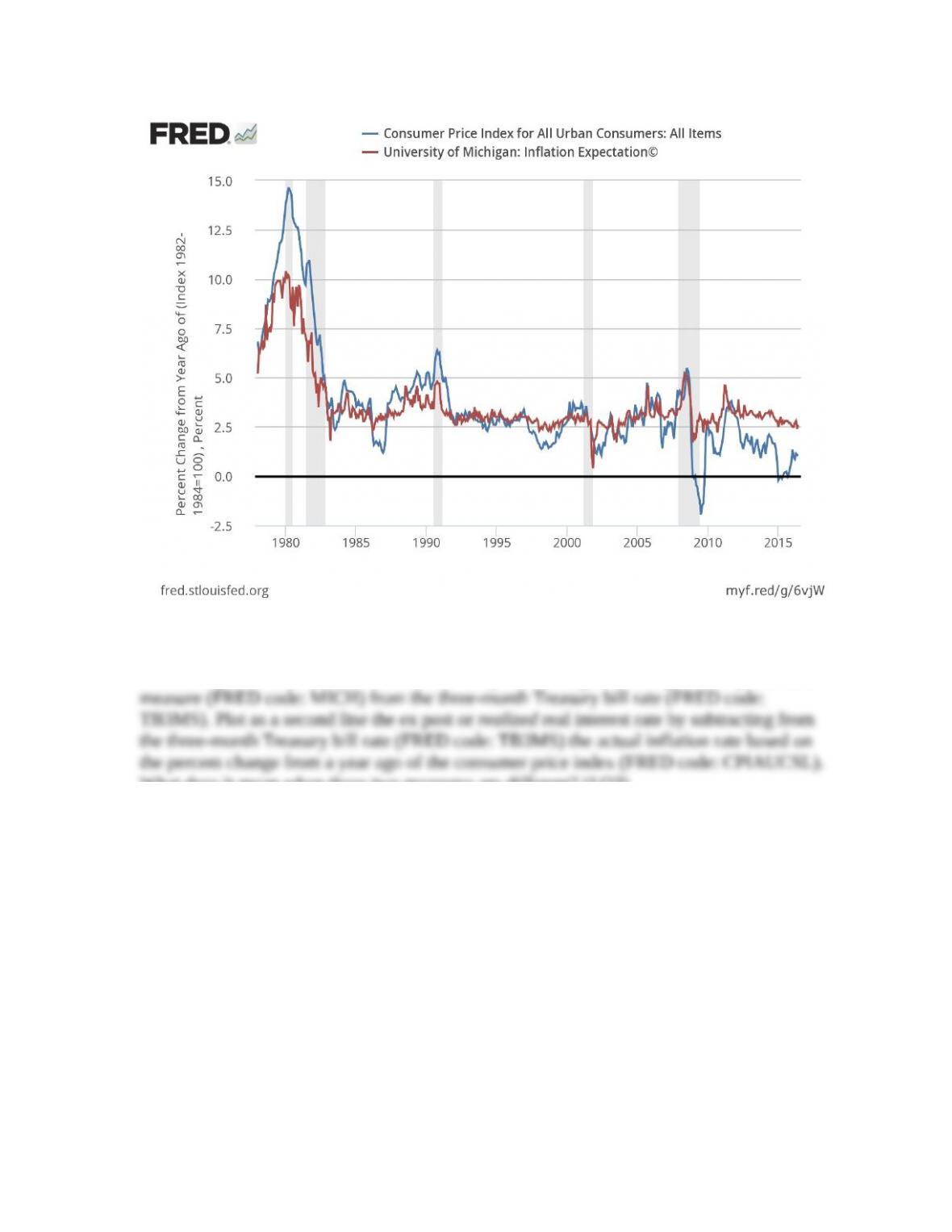

3. The expected real interest rate is the rate which people use in making decisions about the

future. It is the difference between the nominal interest rate and the expected inflation rate,

survey of consumers (FRED code: MICH). Is expected inflation always in line with actual

inflation? Which is more stable? (LO3)

Answer: Expected inflation tends to move with actual inflation but varies somewhat less.

energy price changes) that are not expected to persist. Here is the figure:

Plot the expected real interest rate since 1979 by subtracting the Michigan survey inflation

What does it mean when these two measures are different? (LO3)

Answer: The data plots are:

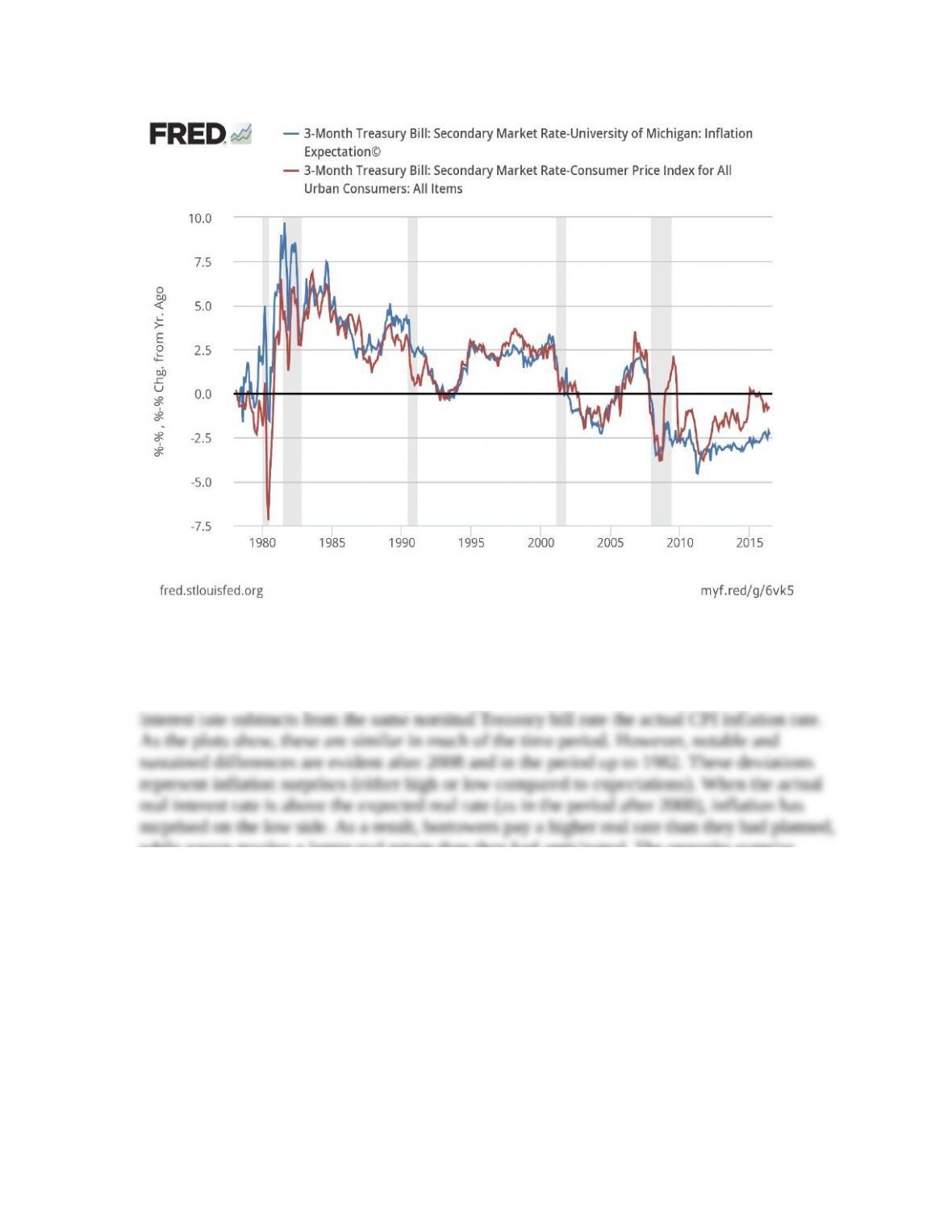

The expected real interest rate is computed by subtracting from the nominal three-month

Treasury bill interest rate the Michigan survey expectations. The actual or ex post real

while savers receive a larger real return than they had anticipated. The opposite surprise

occurred in the late 1970s.

* indicates more difficult problems