Archives

Accounting Chapter 1 A cost accountant would normally occupy

ANS: F PTS: 1 DIF: Difficulty: Easy OBJ: LO: 1-1 NAT: BUSPROG: Analytic STA: AICPA: FN-Decision Modeling | IMA: Cost Management | ACBSP: APC–26-Management Functions KEY: Bloom’s: Knowledge NOT: 1 min. ANS: T PTS: 1 DIF: Difficulty: Easy OBJ: LO: […]

Accounting Chapter 1 One Company Emphasizing Low Costs And The

1-1 INTRODUCTION TO MANAGERIAL ACCOUNTING DISCUSSION QUESTIONS 1. Managerial accounting is the provision of accounting information for internal users in a firm. 2. The three broad objectives of managerial accounting are to provide information for planning, controlling, and decision making. […]

Accounting Chapter 10 Historical experience is often a poor choice

1. Standard costs are essentially budgeted amounts on a per-unit basis. Unit standards serve as inputs in building budgets. 2. Unit standards are used to build flexible budgets. Unit standards for variable costs are the variable cost component of a […]

Accounting Chapter 10 Managers develop quantity standards when they decide

Chapter 10—Standard Costing: A Managerial Control Tool TRUE/FALSE 1. Managers develop quantity standards when they decide what amount of input should be used per unit of output. 2. Managers develop price standards when they determine what amount should be paid […]

Accounting Chapter 10 Rhodes Corporation manufactures a product with

14. Rhodes Corporation manufactures a product with the following standard costs: Direct materials (20 yards @ $1.85 per yard) $37.00 Direct labor (4 hours @ $12.00 per hour) 48.00 Standards are based on normal monthly production involving 2,000 direct labor […]

Accounting Chapter 10 The Labor Rate Variance Measures The Difference

Figure 10-2. Highland Company’s standard cost is $250,000. The allowable deviation is 10%. Its actual costs for six months are January $235,000 February 220,000 March 245,000 April 265,000 May 270,000 June 280,000 30. Refer to Figure 10-2. The upper and […]

Accounting Chapter 10 There would be unfavorable labor efficiency variances

P 10-42 1. Standard Standard Usage Cost Direct materials…………………… … $ 4 25.000 $100.00 Direct labor………………………… … 15 0.768 11.52 V ariable overhead………………… 8 0.768 6.14 Fixed overhead…………………… … 12 0.768 9.22 Standard cost per unit………… … $126.88 2. There […]

Accounting Chapter 10 What is James’ materials price variance

81. Refer to Figure 10-9. What is James’ materials price variance assuming that materials purchased equals materials used? a. $750,000 F b. $700,000 F c. $700,000 U d. $750,00 U 82. Refer to Figure 10-9. What is James’ materials usage […]

Accounting Chapter 11 a favorable maintenance variance could be caused

PTS: 1 DIF: Difficulty: Moderate OBJ: LO: 11-1 NAT: BUSPROG: Analytic STA: AICPA: FN-Decision Modeling | IMA: Budget Preparation | ACBSP: APC–36-Budgeting and Responsibility KEY: Bloom’s: Application NOT: 30 min. 2. Refer to Figure 11-7. Assume that Kipling actually produced […]

Accounting Chapter 11 A flexible budget is based on a simple formula

1. A static budget is for a particular level of activity. A flexible budget is one that can be established for any level of activity. 2. For performance reporting, it is necessary to compare the actual costs for the actual […]

Accounting Chapter 11 A static budget compares actual cost

Chapter 11—Flexible Budgets and Overhead Analysis TRUE/FALSE 1. A static budget compares actual cost with budgeted costs. 2. Static budgets are the best benchmarks for preparing a performance report. ANS: F PTS: 1 DIF: Difficulty: Easy OBJ: LO: 11-1 NAT: […]

Accounting Chapter 11 Each Items Variance Should Analyzed See These

CHAPTER 11 Flexible Budget and Overhead Analysis P 11-47 (Continued) Before-the-fact flexible budgeting allows managers to assess risk and uncertainty. 3. The financial performance as revealed in Requirements 1 and 2 is not very promising. Two out of three scenarios […]

Accounting Chapter 11 The two variances for fixed overhead are

36. During the year, Hawkings produced 10,000 units, used 20,000 direct labor hours, and incurred variable overhead of $90,000. Budgeted variable overhead for the year was $88,000. The hours allowed per unit are 2.1. The standard variable overhead rate is […]

Accounting Chapter 12 Centra And Mantra Agree Transfer Boxes What

35. Refer to Figure 12-2. What is the residual income for Stock Division without the additional investment? a. $40,000 b. $6,000 c. $6,600 d. $6,200 e. $7,500 ANS: E Residual income = $60,000 – (0.14)($375,000) = $7,500 PTS: 1 DIF: […]

Accounting Chapter 12 Margin reveals how much sales revenue remains

1. In centralized decision making, decisions are made at the very top level, and lower-level managers are responsible for implementing these decisions. For decentralized decision making, decisions are made and implemented by lower-level managers. 2. Decentralization is the delegation of […]

Accounting Chapter 12 The practice of delegating decision-making authority

Chapter 12—Performance Evaluation and Decentralization TRUE/FALSE 1. The practice of delegating decision-making authority to lower levels of management in a company is called centralization. 2. In a decentralized company, overall profit margins can mask inefficiencies within the various subdivisions. ANS: […]

Accounting Chapter 12 Which Division Sets The Minimum Transfer Price

Operating income $ 43,200 Beginning assets were $279,500 and ending assets were $296,500. A. Average operating assets were $__________________. B. Margin was __________________. C. Turnover was __________________. D. Return on investment was __________________%. 4. Given the following information for the […]

Accounting Chapter 13 A manager can identify alternatives by using

1. Tactical decisions are short run in nature; they involve choosing among alternatives with an immediate or limited end in view. Strategic decisions involve selecting strategies that yield a long-term competitive advantage. 5. The salary of the supervisor of an […]

Accounting Chapter 13 Clutch And The Tote With Unit Contribution margins

7. Island Princess Pineapples purchases pineapples from area farmers and processes them into rings, juice, and skins. The cost of the pineapples is a joint cost, as is the initial processing in which the fruits are skinned, cored, and sliced […]

Accounting Chapter 13 Detailing Uses Target costing What The Price They

a. $40 b. $65 c. $25.50 d. $13.33 e. $15.67 70. Refer to Figure 13-9. What is the contribution margin per hour of machine time for Test B? a. $20.50 b. $33 c. $16.25 d. $16.50 e. $18 ANS: D […]

Accounting Chapter 13 Sales Dac That Would Not Occur Action

NOT: 4 min. 26. Houston Corporation manufacturers a part for its production cycle. The costs per unit for 5,000 units of this part are as follows: Direct materials $ 32 Direct labor 40 Variable overhead 16 Fixed overhead 32 Total […]

Accounting Chapter 13 The financial manager might encounter one or more

CHAPTER 13 Short-Run Decision Making E 13-34 1. Price of Carved Bear Candle = $12.00 + (0.80 × $12) = $21.60 3. The financial manager might encounter one or more common challenges to using cost-plus (or markup) pricing. One challenge […]

Accounting Chapter 13 The first step in making a short-run decision is to

Chapter 13—Short-Run Decision Making: Relevant Costing TRUE/FALSE 1. The first step in making a short-run decision is to identify alternatives as possible solutions to the problem. 2. In making a short-run decision, all alternatives need to be considered. ANS: F […]

Accounting Chapter 14 Good projects can be rejected and bad projects accepted

1. Independent projects are such that the acceptance of one does not preclude the acceptance of another. With mutually exclusive projects, acceptance of one precludes the acceptance of others. 5. (a) A measure of risk. Roughly, projects with shorter paybacks […]

Accounting Chapter 14 Projects that do not affect the cash flows of other

Chapter 14—Capital Investment Decisions TRUE/FALSE 1. Projects that do not affect the cash flows of other projects are called mutually exclusive projects. 2. The process of planning, setting goals and priorities, arranging financing, and using certain criteria to select long-term […]

Accounting Chapter 14 The After tax Cash Flows Associated With The

72. When investing in automated systems, which of the following intangible or indirect benefits may be important? a. improved customer satisfaction b. improved market share c. reduced support labor cost d. reduced lead time e. All of these. 73. Which […]

Accounting Chapter 14 What is the accounting rate of return for the project

Figure 14-3. Davis Company is considering the purchase of a new piece of equipment that will cost $1,600,000 and have a life of five years with no expected salvage value. The expected cash flows associated with the project are as […]

Accounting Chapter 14 the sensitivity analysis should strengthen the case

CHAPTER 14 Capital Investment Decisions P 14-37 (Continued) Revenues…………………………………………………………… … $ 1,650,000 2. Discount Facto r Present Value 1.00000 $(1,840,000) 3.60478 1,189,577 0.50663 91,193 0.45235 149,276 0.40388 133,280 0.36061 119,001 0.32197 167,424 NPV……………………………………………………… … $ 9,751 The new process should […]

Accounting Chapter 15 A statement of cash flows indicates the sources

Chapter 15—Statement of Cash Flows TRUE/FALSE 1. A statement of cash flows indicates the sources and uses of a firm’s cash during a period. 2. All SEC-registered firms must issue a statement of cash flows, in addition to the income […]

Accounting Chapter 15 Ending Accumulated Depreciation Beginning Equipment Purchases Less

CHAPTER 15 Statement of Cash Flows P 15-42 1. a. Indirect Method: Cash flows from operating activities: Net income………………………………………… … $122,400 Add (deduct) adjusting items: 15-17 © 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, […]

Accounting Chapter 15 net cash flows from investing activities

PTS: 1 DIF: Difficulty: Challenging OBJ: LO: 15-2 NAT: BUSPROG: Analytic STA: AICPA: FN-Reporting | IMA: Reporting | ACBSP: APC-24-Statement of Cash Flows KEY: Bloom’s: Application NOT: 10 min. 6. Use the following selected data and additional information to answer […]

Accounting Chapter 15 The all-financial-resources approach requires disclosure

1. Cash equivalents such as money market funds and CDs are highly liquid investments that can be readily converted into cash. They are treated as cash. 2. Operating activities are the ongoing, day-to-day, revenue-generating activities of an organization. Investing activities […]

Accounting Chapter 15 The data given below are from the accounting records

Credit balances: Accumulated Depreciation 23,000 Accounts payable (10,000) Accrued liabilities 7,000 Taxes payable 5,000 Bonds payable 40,000 Based solely on this information, the net cash flows from operating activities under the indirect method on the statement of cash flows would […]

Accounting Chapter 15 The general ledger of Lopez Company provides

Ending Beginning balance balance Accounts receivable $32,000 $40,000 Inventory 60,000 50,000 Prepaid expenses 12,000 8,000 Accumulated depreciation (40,000) (30,000) Accounts payable 30,000 45,000 Accrued liabilities 16,000 10,000 Income taxes payable 2,000 5,000 Required: Using the direct method, prepare the operating […]

Accounting Chapter 16 Inventory This Year Last Year Inventory Turnover

CHAPTER 16 Financial Statement Analysis E 16-37 = = 1.67 Total Liabilities Total Equity = =$10,250,000 $6,150,000 3. Debt-to-Equity Ratio E 16-38 = 0.1858, or 18.58% 2. The return on sales ratio illustrates the number of cents from each sales […]

Accounting Chapter 16 Return Stockholders Equity Net Income Preferred

1. The two major types of financial statement analysis discussed in this chapter are common-size analysis and ratio analysis. 2. Horizontal analysis expresses line items of financial statements as a percentage of a prior- period amount. Vertical analysis expresses the […]

Accounting Chapter 16 the base year can be the immediately preceding

Chapter 16—Financial Statement Analysis TRUE/FALSE 1. In horizontal analysis, the base year can be the immediately preceding period, or it can be a period further in the past. 2. A primary purpose of vertical analysis is to observe trends over […]

Accounting Chapter 16 The following information pertains to Barkley

41. Eagle Company has $9,000 in cash, $11,000 in marketable securities, $26,000 in current receivables, $34,000 in inventories, and $40,000 in current liabilities. The company’s quick ratio is closest to a. 1.35. b. 1.15. c. 2.00. d. 1.73. 42. Siri […]

Accounting Chapter 16 Using The Information Provided Above Compute The

KEY: Bloom’s: Application NOT: 5 min. 10. The following information is summarized from the balance sheets of Kress Inc. and Ross Corp. at December 31, 2013. Neither company has inventory. Kress Ross Current Assets: Cash and cash equivalents $ 340,800 […]

Accounting Chapter 2 A direct cost is one that can be traced to the cost

1. Cost is the amount of cash or cash equivalent sacrificed for goods and/or services that are expected to bring a current or future benefit to the organization. An expense is an expired cost; the benefit has been used up. […]

Accounting Chapter 2 Fidalgo Company Makes Stereos During The

KEY: Bloom’s: Application NOT: 1 min. 77. Refer to Figure 2-3. What was the gross margin percent? a. 52% b. 48% c. 17% d. 19% 78. Refer to Figure 2-3. What was the selling expense percent? a. 17% b. 19% […]

Accounting Chapter 2 Finished Goods Inventory Cog Ending Finished

CHAPTER 2 Basic Managerial Accounting Concepts E 2-42 (Concluded) So, COGM = Direct Materials Used in Production + Direct Labor Used in Production + 2-16 © 2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or […]

Accounting Chapter 2 involves the way that a cost is linked to some

7. Assigning costs a. involves the way that a cost is linked to some cost object. b. tells the company why the money was spent. c. to a cost object using a reasonable and convenient method is allocation. d. all […]

Accounting Chapter 2 It is beneficial to assign indirect costs to cost

Chapter 2—Basic Managerial Accounting Concepts TRUE/FALSE 1. It is beneficial to assign indirect costs to cost objects. 2. Price must be greater than cost in order for the firm to generate revenue. ANS: F PTS: 1 DIF: Difficulty: Easy OBJ: […]

Accounting Chapter 2 A product cost is a manufacturing cost that is

B. Compute the gross margin C. Compute the operating income D. Compute the operating income if 75,000 stereos were produced and 69,000 were sold. 14. Baleen Company supplied the following data at the end of the current year: Sales commissions […]

Accounting Chapter 3 A cost that changes in total as output changes

Chapter 3—Cost Behavior TRUE/FALSE 1. A cost that changes in total as output changes is a variable cost. 2. The cost of raw materials used is usually a fixed cost. ANS: F The cost of raw materials used is usually […]

Accounting Chapter 3 Some account categories are primarily fixed

1. Knowledge of cost behavior allows a manager to assess changes in costs that result from changes in activity. This allows a manager to examine the effects of choices that change activity. For example, if excess capacity exists, bids that […]

Accounting Chapter 3 While These Reductions Were Not Quantified Outside

CHAPTER 3 Cost Behavior E 3-39 1. SUMMARY OUTPUT Multiple R 0.917226463 R Square 0.841304384 2. Delivery Cost = $942 + ($1.79 × Number of Deliveries) 3. The R² is 0.841, or 84.1%. In other words, 84.1% of the variation […]

Accounting Chapter 4 Decrease in contribution margin for basic sleds

CHAPTER 4 Cost-Volume-Profit Analysis: A Managerial Planning Tool E 4-35 (Continued) 2. d. Both fixed cost and unit variable cost increase: E 4-36 1. Unit Contribution Margin = $791,700/54,600 = $14.50 Break-Even Units = $801,850/ $14.50 = 55,300 2. Operating […]

Accounting Chapter 4 Break-even point is the level of sales activity

1. CVP analysis allows managers to focus on selling prices, volume, costs, profits, and sales mix. Many different “what-if” questions can be asked to assess the effect of changes in key variables on profits. 4. A t the break-even point, […]

Accounting Chapter 5 Allocation ratios for Power based on number of

CHAPTER 5 Job-Order Costing E 5-43 (Continued) 4. Work in Process: Beginning balance………………………………………… … $0 Direct materials……………………………………………… 24,500 5. Finished Goods: Beginning balance………………………………………… … $ 25,600 Jobs transferred in: Job 58……………………………………………….…… … $27,440 Job 59……………………………………………………… 22,580 50,020 Jobs sold: Job […]

Accounting Chapter 5 Normal costing defines product cost as the sum

1. Job-order costing accumulates costs by jobs, and process costing accumulates costs by processes. Job-order costing is suitable for operations that produce custom-made products that receive different doses of manufacturing costs. Process costing, on the other hand, is suitable for […]

Accounting Chapter 6 conversion materials cost total beginning work

A. Units completed 65,000 Units in ending work in process (7,000 x 80%) 3,200 Total equivalent units 68,200 B. Costs to account for: Conversion Materials Cost Total Beginning work in process $23,000 $52,000 $75,000 Incurred during the period $115,000 $195,000 […]

Accounting Chapter 6 The cost flows for process-costing and job-order

1. Process costing collects costs by process (department) for a given period of time. Unit costs are computed by dividing these costs by the department’s output measured for the same period of time. Job-order costing collects costs by job. Unit […]

Accounting Chapter 6 The Martin Company uses the weighted average

Figure 6-6. The Martin Company uses the weighted average method. The beginning work in process consists of 6,000 units (100% completed as to materials and 50% complete as to conversion costs). The number of units completed was 120,000. The ending […]

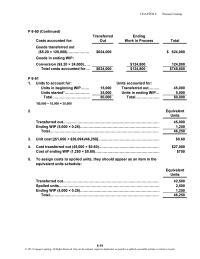

Accounting Chapter 6 they should appear as an item in the equivalent units

CHAPTER 6 Process Costing P 6-50 (Continued) Transferred Costs accounted for: Out Total Goods transferred out P 6-51 1. Units to account for: Units accounted for: Units in beginning WIP…… … 15,000 Transferred out……… 45,000 Units started*……………… … 35,000 Units […]

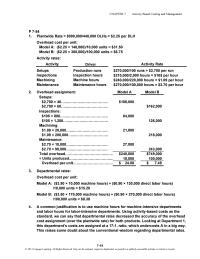

Accounting Chapter 7 Activity Rates Ordering Rate Selling Rate Service

1. For plantwide rates, overhead is first collected in a plantwide pool, using direct tracing. Next, an overhead rate is computed and used to assign overhead to products. 2. First stage: Overhead is assigned to production department pools using direct tracing, […]

Accounting Chapter 7 For Category That Means The Range Difference

CHAPTER 7 Activity Based Costing and Management P 7-54 1. Plantwide Rate = $990,000/440,000 DLHs = $2.25 per DLH Overhead cost per unit: Model A: ($2.25 × 140,000)/10,000 units = $31.50 Model B: ($2.25 × 300,000)/100,000 units = $6.75 Activity […]

Accounting Chapter 7 Rollo Company has developed cost formulas

28. Rollo Company has developed cost formulas for the drivers of the following production activities: Driver Activity Fixed Variable Labor hours Materials -0- 20 Labor hours Labor -0- 10 Machine hours Maintenance 10,000 8 Machine hours Machining 50,000 2 Number […]

Accounting Chapter 7 What is the plantwide overhead rate based on

3. Refer to Figure 7-6. A. What is the plantwide overhead rate based on machine hours? B. Assuming a plantwide overhead rate, what is the unit cost of the basic model? C. Assuming a plantwide overhead rate, what is the […]

Accounting Chapter 8 Laird Company uses 405 units of a part each

Indirect materials (variable) 30,000 Other variable overhead 90,000 Fixed manufacturing overhead 180,000 Fixed administrative expenses 150,000 Fixed selling expenses 120,000 Variable selling expenses, per unit 40 Direct labor, per unit 80 Direct materials, per unit 20 Required: Compute the dollar […]

Accounting Chapter 8 Unit Direct Labor Cost Unit Variable Overhead

1. The only difference between absorption costing and variable costing is the way in which fixed overhead costs are assigned. Under variable costing, fixed overhead is a period cost; under absorption costing, it is a product cost. 2. A bsorption-costing […]

Accounting Chapter 8 Variable costing and absorption costing income

Chapter 8—Absorption and Variable Costing, and Inventory Management TRUE/FALSE 1. Variable costing and absorption costing income statements may differ because of their treatment of fixed factory overhead. 2. Inventory costs under variable costing include only direct materials, direct labor, and […]

Accounting Chapter 8 Variable Costing Should Used Since The Fixed

CHAPTER 8 Absorption and Variable Costing, and Inventory Management E 8-32 3. Total Ordering Cost = Number of Orders × Cost per Order = 72 orders × $10 = 4. Total Carrying Cost = Average Number of Units in Inventory […]

Accounting Chapter 8 What is the value of ending inventory using

33. Refer to Figure 8-8. What is the January ending inventory for Steele Corporation using the variable costing method? a. $260,000 b. $78,000 c. $108,000 d. $90,000 34. Refer to Figure 8-8. What is the March ending inventory for Steele […]

Accounting Chapter 9 A master budget is the collection of all individual

1. Budgets are the quantitative expressions of plans. Budgets are used to translate the goals and strategies of an organization into operational terms. 2. Control is the process of setting standards, receiving feedback on actual performance, and taking corrective action […]

Accounting Chapter 9 Bright Lamp Company Manufactures Lamps The

Chapter 9—Profit Planning TRUE/FALSE 1. A strategic plan identifies strategies for future activities and operations, generally covering at least five years. 2. Budgets are financial plans for the future. ANS: T PTS: 1 DIF: Difficulty: Easy OBJ: LO: 9-1 NAT: […]

Accounting Chapter 9 Other Expenses That Will Likely Increase With

CHAPTER 9 Profit Planning P 9-51 (Continued) 7. Schedule 7: Ending Finished Goods Inventory Budget Unit cost computation: Direct materials (3 units @ $80)…………………………………………… … $ 240.00 8. Schedule 8: Cost of Goods Sold Budget Direct materials used (Schedule 3)…………………………………………… […]

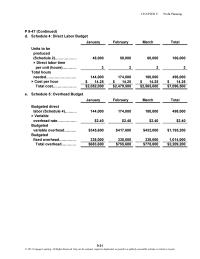

Accounting Chapter 9 This schedule will also be used to build the cash budget

CHAPTER 9 Profit Planning P 9-47 (Continued) d. Schedule 4: Direct Labor Budget January February March Total Units to be produced e. Schedule 5: Overhead Budget January February March Total Budgeted direct labor (Schedule 4)……… … 144,000 174,000 180,000 498,000 […]

Accounting Chapter 9 What is the ending cash balance for October

15. Quillin Company had the following budgeted information for October: 1. October 1 cash balance $3,500 2. Expected sales 2,500 units at $25 each (half in cash, remainder on credit due in November) 3. Inventory purchases 3,000 units at $14 […]

Accounting Chapter 9 Which The Following Not Advantage Participative

36. In going from the sales budget to the production budget, adjustments to the sales budget need to be made for a. finished goods inventories. b. cash receipts. c. factory overhead costs. d. selling expenses. ANS: A PTS: 1 DIF: […]

Accounting Chapter 9 Which of the following is an example of myopic

e. It fosters a sense of managerial responsibility. 86. Which of the following is an advantage of participative budgeting? a. It fosters pseudoparticipation. b. It encourages budgetary slack. c. It tends to discourage goal congruence. d. It fosters a sense […]

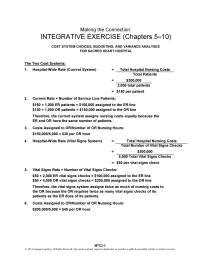

Accounting Integrative Exercise Managers And Employees Third While The

The Two Cost Systems: 1. Hospital-Wide Rate (Current System) = 3. Costs Assigned to OR/Number of OR Nursing Hours: $150,000/5,000 = $30 per OR hour 4. Hospital-Wide Rate (Vital Signs System) = = = $50 per vital signs check Total […]

Accounting Integrative Exercise Relevant revenues from the special sales offer

Special Sales Offer Relevant Analysis: 1. Note: Sales commission costs and advertising costs are irrelevant because they are marketing in nature. Similarly, customer hotline service costs are irrelevant because they are customer service in nature (see bulleted points in exercise). […]

Accounting Integrative Exercise The manufacturing and marketing total fixed

1. The variable and fixed costs for each product line—canoes and paddles— possess both a manufacturing and a marketing component. However, the manufacturing and marketing data are recorded separately, which means that a. Canoe: High-Low (Manufacturing costs): ($140,000 – $108,000)/(400 […]