CHAPTER 13 Short-Run Decision Making

E 13-34

1. Price of Carved Bear Candle = $12.00 + (0.80 × $12) = $21.60

3. The financial manager might encounter one or more common challenges to using

cost-plus (or markup) pricing. One challenge might be identifying the most

appropriate percentage by which to markup gift shop costs. For example, if the

percentage is too high (and 80% seems high), the manager risks setting prices

too high, thereby causing some customers to decide not to buy the gift shop’s

E 13-35

1. Desired Profit = 0.20 × Target Price

E 13-36

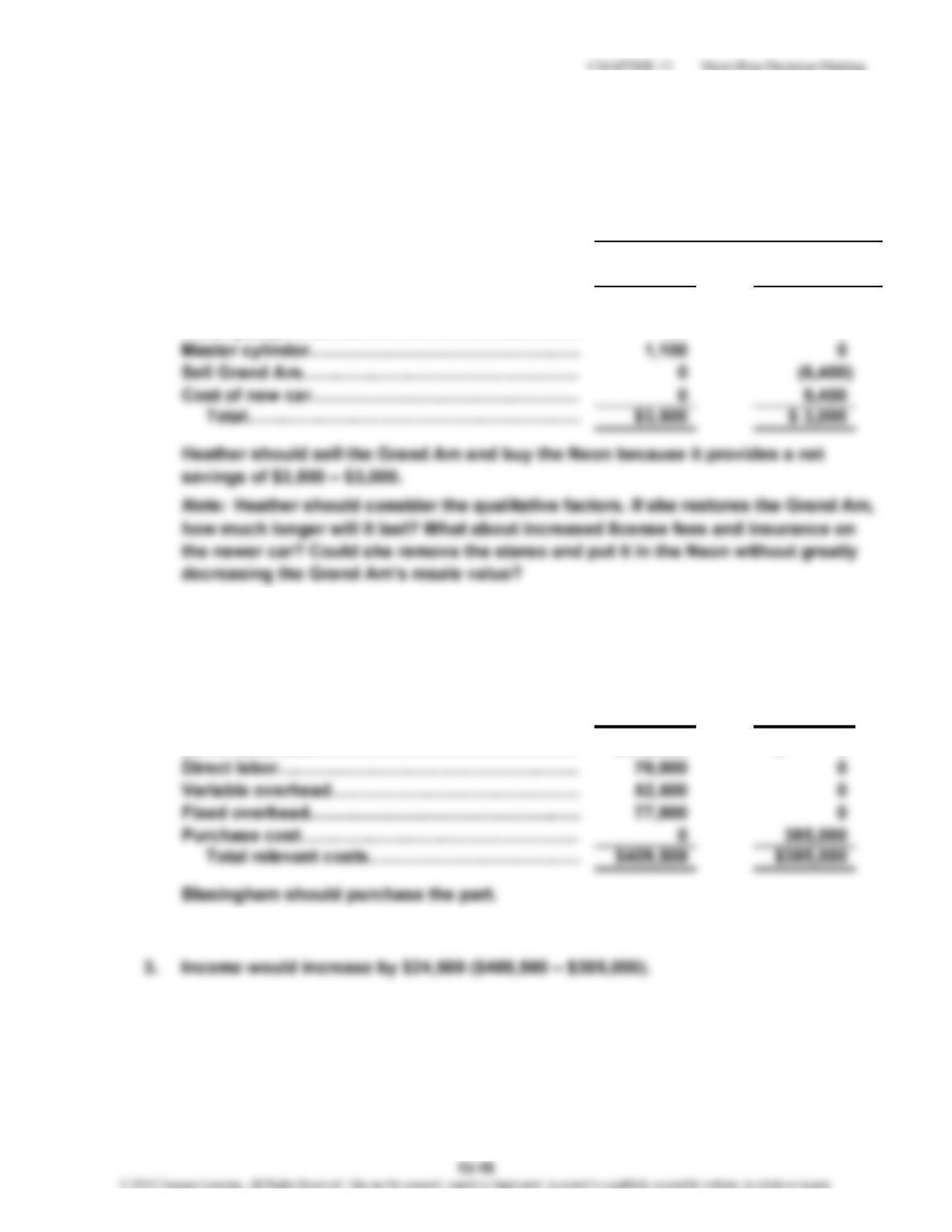

1. The amounts Heather has spent on purchasing and improving the Grand Am are

irrelevant because these are sunk costs.

2.

Restore

Cost Item Grand Am

Transmission…………………………………………

…

$2,000 $ 0

Water pump……………………………………………

…

400 0

E 13-37

1. If the analysis is done using total costs, each variable cost as well as the purchase

price will be the unit cost multiplied by 35,000 units. The direct fixed overhead of

$77,000 is avoidable if the part is purchased.

Make Buy

Direct materials………………………………………

…

$210,000 $ 0

2. Maximum Price = $409,500/35,000 = $11.70 per unit

Alternatives

Buy Neon

CHAPTER 13 Short-Run Decision Making

E 13-38

Make Buy

1. Direct materialsa……………………………

…

$210,000 $ 0

Direct laborb…………………………………

…

70,000 0

2. Maximum Price = $332,500/35,000 = $9.50 per unit

3. Income would decrease by $52,500 ($332,500 – $385,000).

a$6.00 × 35,000 = $210,000

13-16

…

CHAPTER 13 Short-Run Decision Making

P 13-39

1. If the special order is accepted:

Revenues ($7 × 100,000)……………………………………….……………

…

$ 700,000

Direct materials ($2 × 100,000)………………………………….…………… (200,000)

2. The qualitative factors are those that cannot be easily quantified. The company is

faced with a problem of idle capacity. Accepting the special order would bring

production up to near capacity and allow the company to avoid laying off

P 13-40

1. Cost Item Make Buy

Raw materialsa…………………………………………………

…

$218,000 $ 0

Direct labor

b

……………………………………………………

…

70,200 0

Variable overheadc……………………………………………

…

20,800 0

d

…

PROBLEMS

CHAPTER 13 Short-Run Decision Making

P 13-40 (Continued)

2. Qualitative factors that Hetrick should consider include quality of crowns, reliability

and promptness of producer, and reduction of workforce.

3. It reduces the cost of making the crowns to $335,000, which is less than the cost

4. Cost Item Make Buy

Raw materialsa………………………………………………

…

$372,000 $ 0

Direct labor

b

…………………………………………………

…

129,600 0

…

d

…

P 13-41

Process

@ 600 lbs. Furthe

r

Sell Difference

Revenuesa…………………………………… $24,000 $7,200 $16,800

b

d

a600 × 10 × $4 = $24,000;

$12 × 600 = $7,200

b$1.30 × (600/20)

c[(10 × 600)/25] × $1.60 = $384;

13-18

CHAPTER 13 Short-Run Decision Making

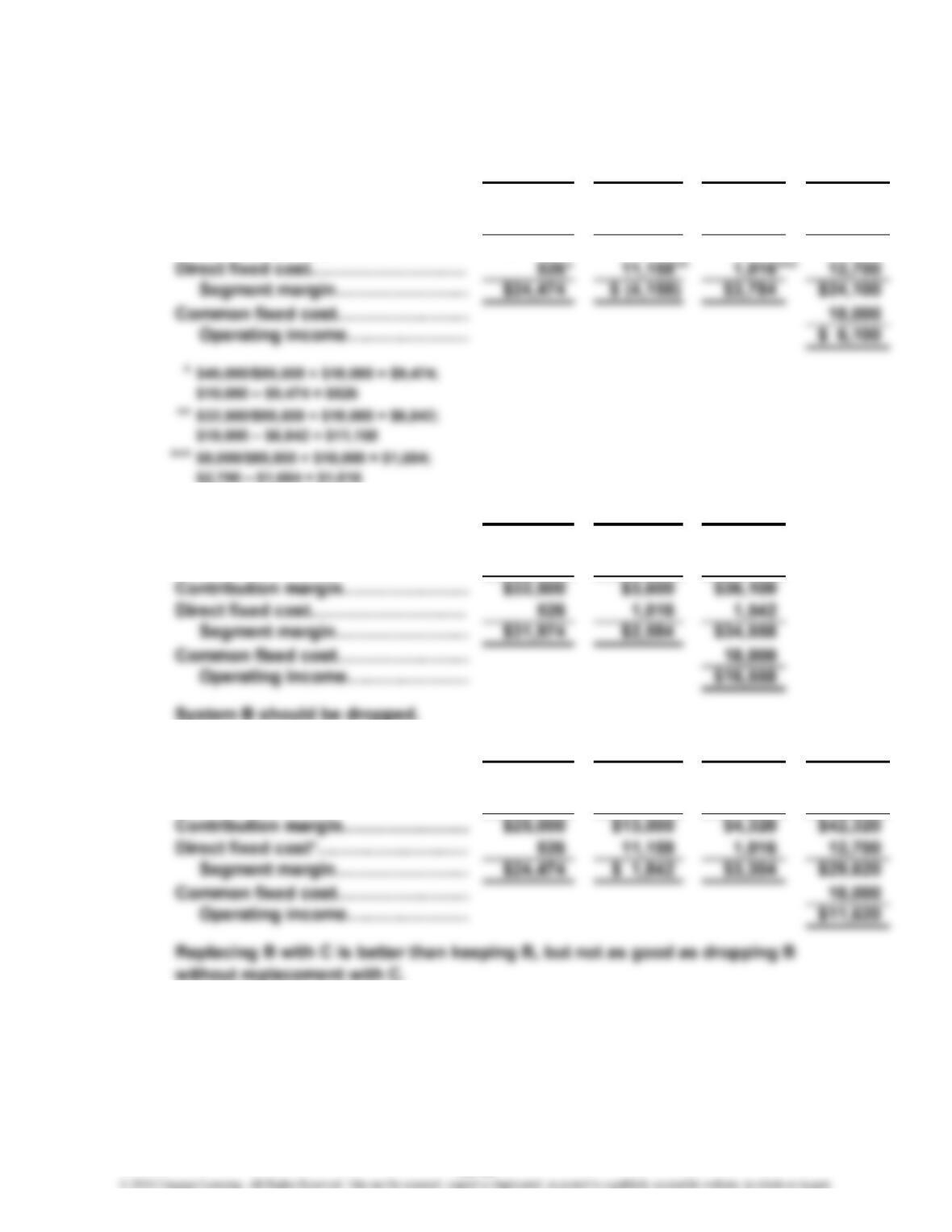

P 13-42

1. System

A

System B Headset Total

Sales……………………………………

…

$45,000 $32,500 $8,000 $85,500

V

ariable expenses……………………

…

20,000 25,500 3,200 48,700

Contribution margin…………………

…

$25,000 $ 7,000 $4,800 $36,800

2. System

A

Headset Total

Sales……………………………………

…

$58,500 $6,000 $64,500

V

ariable expenses……………………

…

26,000 2,400 28,400

…

3. System

A

System C Headset Total

Sales……………………………………

…

$45,000 $26,000 $7,200 $78,200

V

ariable expenses……………………

…

20,000 13,000 2,880 35,880

…

13-19

CHAPTER 13 Short-Run Decision Making

P 13-43

1. Steve should consider selling the part for $1.85 because his division’s profits would

increase $12,800:

A

ccept Reject

Revenues (2 × $1.85 × 8,000)…………………………………

…

$29,600 $0

2. Pat should accept the $2 price. This price will increase the cost of the component

from $29,600 to $32,000 (2 × $2 × 8,000) and yield an incremental benefit of $16,000

3. Yes. At full price, the total cost of the component is $36,800 (2 × $2.30 × 8,000), an

P 13-44

1. Markup = ($46,300 + $35,600)/$130,000 = 0.63, or 63%

2. Direct materials………………………………

…

$1,800

Direct labor……………………………………

…

1,600

V

…

A

CHAPTER 13 Short-Run Decision Making

P 13-45

Basic Standard Deluxe

1. Price………………………………………………

…

$ 9.00 $30.00 $35.00

V

ariable cost……………………………………

…

6.00 20.00 10.00

Contribution margin……………………………

…

$ 3.00 $10.00 $25.00

2. First, produce and sell 12,000 deluxe units, which would use 9,000 machine

hours. Then, produce and sell 50,000 basic units, which would use 5,000

P 13-46

1. The company should not accept the offer because the additional revenue is

less than the additional costs (assuming fixed overhead is allocated and will

2. Costs associated with the layoff:

Increase state UI premiums (0.01 × $1,460,000)…………………………

…

$14,600

13-21

CHAPTER 13 Short-Run Decision Making

P 13-47

1. Sales………………………………………………………………………………… $263,000

Process

2. Sell Furthe

r

Difference

Revenues…………………………………

…

$40,000 $75,000 $35,000

P 13-48

1. ($30 × 2,000) + ($60 × 4,000) = $300,000

2. Juno Hera

Contribution margin…………………………………………

…

$30 $60

÷ Pounds of material………………………………………… 25

P 13-49

1. Process

Sell Furthe

r

Revenues…………………

…

$24,000 $33,000 $ 9,000

…

2. Process

Sell Furthe

r

Revenues…………………

…

$24,000 $33,000 $ 9,000

Processing cost…………

…

— (4,100) (4,100)

P 13-50

1. Monthly cost for FirstBank:

Checking accounts:

Maintenance fees ($5 × 6)………………………….…… $ 30

Differential Amount

to Process Furthe

r

Differential Amount

to Process Furthe

r

13-23

CHAPTER 13 Short-Run Decision Making

P 13-50 (Continued)

Monthly cost for Community Bank:

Checking accounts: Returned checks ($2 × 25)…….…………

…

$50

Credit card fees

Per item ($0.50 × 4,000)…………………………………………… $2,000

Batch processing ($7 × 20)………………………………………

…

140 2,140

Wire transfers ($30 × 100)…….……………………………………… 3,000

2. If the full online banking access were crucial, Community Bank would be eliminated

immediately. This leaves FirstBank and RegionalOne Bank. The two sets of monthly

13-24

…

CHAPTER 13 Short-Run Decision Making

Case 13-51

1. Pamela should not have told Roger about the deliberations concerning the power

department because this is confidential information. She had been explicitly told

2. The romantic relationship between Pamela and Roger sets up a conflict of interest

for this particular decision. Pamela should have withdrawn from any active role in it.

(Standard III: 1) However, she should definitely provide the information she currently

has about the cost of eliminating the power department. To not do so would be active

CASES

13-25

CHAPTER 13 Short-Run Decision Making

Case 13-52

1. Salesa………………………………………………………

…

$3,751,500

Less: Variable expenses

b

……………………………… 2,004,900

Contribution margin……………………………………

…

$1,746,600

aBased on sales of 41,000 units

Let X = Units sold

$83X/2 + $100X/2 = $3,751,500

$183X = $7,503,000

X = 41,000 units

b$83X/125.0% $66.40 Manufacturing cost

2. Keep Drop

Sales………………………………………………………

…

$ 3,751,500 $—

V

ariable costs……………………………………………

…

(2,004,900) (2,050,000)

Case 13-53

Answers will vary.

*