1. Job-order costing accumulates costs by jobs, and process costing accumulates costs by

processes. Job-order costing is suitable for operations that produce custom-made products that

receive different doses of manufacturing costs. Process costing, on the other hand, is suitable

for operations that produce homogeneous products that receive equal amounts of manufacturing

costs in each process.

4. Actual overhead rates are rarely used because managers cannot wait until the end of the year

to obtain product costs. Information on product costs is needed as the year unfolds for planning,

control, and decision making.

5. Overhead is assigned to production using the predetermined rate. The predetermined overhead

rate is equal to estimated overhead divided by estimated activity level. The predetermined

overhead rate is multiplied by the actual activity level or the cost driver on which the rate is based.

8. Unless all your jobs (lawns) are the same size and require the same services, you will need to

use a job-order costing system. At a minimum, you will need job-order cost sheets for each

customer. You will need labor time tickets to record the amount of time spent on each job, both

to cost the job and to pay the individual doing the work. A materials requisition form may be

5JOB-ORDER COSTING

DISCUSSION QUESTIONS

5-1

CHAPTER 5 Job-Order Costing

9. Multiple overhead rates often produce a more accurate assignment of overhead costs to jobs.

This can be true if the departments through which products pass have different amounts of

10. Materials requisition forms serve as the source document for posting materials usage and costs

to individual jobs. Time tickets serve a similar function for labor. Predetermined overhead rates

are used to assign overhead costs to individual jobs.

11. Because the overhead rate is based on direct labor cost, the amount of overhead applied will

increase. As a result, the total cost of each job will go up.

14. Because advertising expense is a period expense, it has no effect on overhead—either applied or

actual. Therefore, changes in advertising expense cannot affect manufacturing cost or cost of

goods sold.

15. A departmental overhead rate application can be easily converted to a plantwide rate. First, the

estimated overhead for all departments is totaled, and a single plantwide driver is chosen. The

plantwide overhead rate is simply the estimated plantwide overhead divided by the plantwide

CHAPTER 5 Job-Order Costing

18. The identification and use of causal factors ensures that support department costs are accurately

19. a. Number of employees

b. Square footage

20. The direct method allocates the direct costs of each support department directly to the producing

departments. No consideration is given to the fact that other support departments may use support

services. The sequential method allocates support department costs sequentially. First, the costs

5-3

CHAPTER 5 Job-Order Costing

5-1. d

5-2. c

5-11. c

5-12. e

5-13. d

MULTIPLE-CHOICE QUESTIONS

5-4

CHAPTER 5 Job-Order Costing

5-14. c

5-15. b

5-5

CHAPTER 5 Job-Order Costing

CE 5-22

1. Predetermined Overhead Rate =

CE 5-23

CE 5-24

1. Cutting Department Overhead Rate = $240,000/150,000 mhrs

= $1.60 per machine hour

CORNERSTONE EXERCISES

Estimated Direct Labor Cost

Estimated Overhead

CHAPTER 5 Job-Order Costing

CE 5-25

1. Predetermined Plantwide Overhead Rate = $590,000/131,200 DLH

= $4.50 per direct labor hour*

* Rounded

CE 5-26

1. Since the predetermined overhead rate is not given, it must be calculated from

BWIP amounts using either Job 44 or Job 45. Using Job 44,

2. Job 45 Job 46 Job 47

Beginning balance, June 1

…

$ 6,450 $ 0 $ 0

3. By the end of June, Jobs 44, 45, and 47 have been transferred out of Work in

Process. Thus, the ending balance in Work in Process consists of Job 46.

Work in process, June 30……

…

$3,285

4. One job, Job 45, was sold during June.

Cost of goods sold…………………

…

$24,120

$ 7,080

Job 44

CHAPTER 5 Job-Order Costing

CE 5-27

1. Allocation ratios for S1 based on number of employees:

Cutting = 63/(63 + 147) = 0.30

2.

Allocate: S1 S2 Cutting Sewing

…

CE 5-28

1. Allocation ratios for S1 based on number of employees:

S2 = 30/(30 + 63 + 147) = 0.1250

2. Support Departments Producing Departments

Allocate: S1 S2 Cutting Sewing

Direct costs…………………

…

$ 180,000 $ 150,000 $122,000 $ 90,500

Support Departments Producing Departments

5-8

CHAPTER 5 Job-Order Costing

E 5-29

a. Hospital services—job order

b. Custom cabinet making—job order

c. Toy manufacturing—process

E 5-30

a. Auto manufacturing—a shop that builds autos from scratch (the way Rolls Royce

used to build cars, or a car that can be built from kits) would use job-order costing.

Large automobile manufacturers use process costing. (While the customer may

EXERCISES

5-9

CHAPTER 5 Job-Order Costing

E 5-31

E 5-32

1. Predetermined Overhead Rate = $486,400/95,000 DLH

= $5.12 per direct labor hour

E 5-33

1. Assembly Department Overhead Rate = $338,000/130,000 DLH

= $2.60 per direct labor hour

3. Assembly Testing

Department Department

Actual overhead…………………………

…

$29,850 $58,000

5-10

CHAPTER 5 Job-Order Costing

E 5-34

2. Direct Materials = 3 × Direct Labor

Prime Cost = Direct Materials + Direct Labor

3. Applied Overhead = Direct Labor × Overhead Rate

E 5-35

1. Materials requisition form

E 5-36

1. Job 93 Direct Labor Hours = $2,160/$18 = 120 DLH

2. August applied overhead for:

Job 93 = 120 DLH × $8 = $960

3. Job 93 Job 94 Job 95 Job 96

Beginning balance……

…

$ 8,750 $ 7,300 $ 0 $ 0

4. Work in Process, August 31, consists of unfinished jobs:

Job 94……………………

…

$19,600

…

…

CHAPTER 5 Job-Order Costing

E 5-36 (Continued)

5. Price of Job 93 = $12,820 + (0.40 × $12,820) = $17,948

6. Jagjit could treat the acquisition and use of the bulldozer as a separate department

and create a departmental overhead rate for it based on the hours used. That is, the

E 5-37

Job 877 Job 878 Job 879 Job 880

1. Beginning balance…………

…

$18,640 $ 0 $ 0 $ 0

2. Applied overhead in October for:

Job 877 = $14,800 × 0.80 = $11,840

3. Work in Process, October 31:

Job 878*…………………………………………………………

…

$21,300

E 5-38

1. Balance in Work in Process (all incomplete jobs):

Job 303……………………………………………………………

…

$ 780

Job 306……………………………………………………………

…

350

…

…

…

CHAPTER 5 Job-Order Costing

E 5-38 (Continued)

2. Balance in Finished Goods (all jobs completed but not sold):

Beginning balance (Job 300)………………………………

…

$ 300

Job 301…………………………………………………………

…

1,600

E 5-39

1. Job 106 Job 107 Job 108

Balance, July 1……………………………… $21,310 $ 6,250 $ 0

2. Work in Process, July 31 = Job 107 = $35,550

3. Finished Goods:

Beginning balance……………………………………………

…

$ 49,000

…

5. Sales [$81,360 + (0.30 × $81,360)]…………………………

…

$105,768

Cost of goods sold………………………………………….

…

81,360

Gross margin………………………………………………

…

$ 24,408

Less:

…

…

CHAPTER 5 Job-Order Costing

E 5-40

Job 213:

1. Number of Units =

4. Overhead Applied, Department 2 = 25 machine hours × $8

= $200

Job 214:

1. Price per Unit =

= $4,375/350 units

=

Unit Cost

Total Manufacturing Cost

Total Sales Revenue

Number of Units

$12.50

5-14

CHAPTER 5 Job-Order Costing

E 5-40 (Continued)

4. Unit Cost =

= $3,073/350 units

=

Job 217:

1. Machine Hours, Department 2 =

Job 225:

1. Number of Units =

= $1,150/$5 = 230 units

Total Sales Revenue

Price per Unit

Overhead Applied, Department 2

Overhead Rate

Number of Units

Total Manufacturing Cost

$8.78

5-15

CHAPTER 5 Job-Order Costing

E 5-41

1. Direct materials……………………………..……………………

…

$12,000

Direct labor:

2. Unit Cost = $27,960/1,000 units = $27.96

3. Direct materials…………………………………………………

…

$12,000

Direct labor:

…

E 5-42

1. Job 39 Job 40 Job 41 Job 42 Job 43

Balance, April 1 $ 540 $3,400 $2,990 $ 0 $ 0

Direct materials 700 560 375 3,500 6,900

3.

Sales [$22,814 + (0.30 × $22,814)]……..………..……….………………….…

…

$29,658

Income Statement

For the Month Ended April 30

Ensign Landscape Design

CHAPTER 5 Job-Order Costing

E 5-43

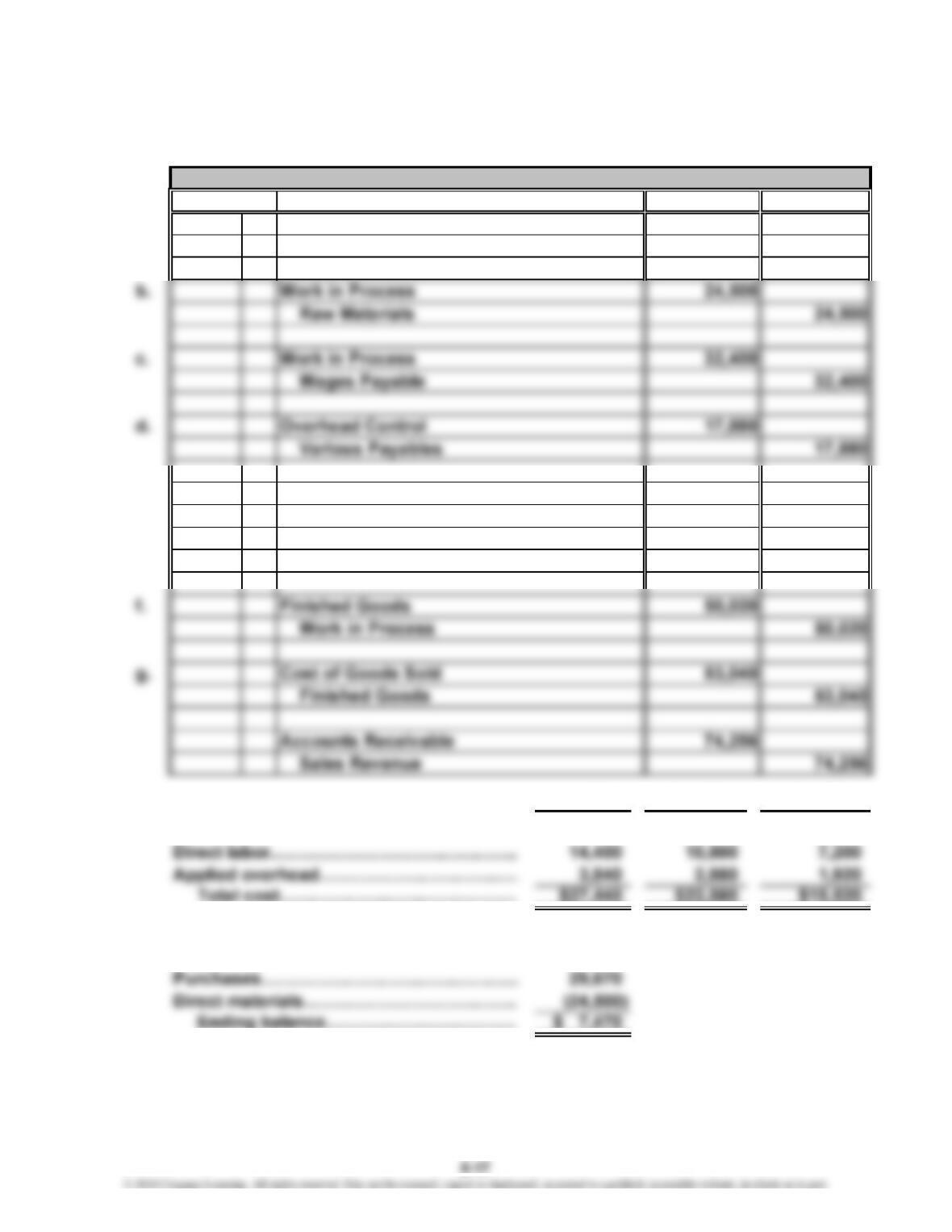

1.

Credit

a. Raw Materials

Accounts Payable 29,670

e. Work in Process

Overhead Control 8,640

Total Direct Labor Hours = $32,400/$18 = 1,800 DLH

Applied Overhead = 1,800 DLH × $4.80 = $8,640

2. Job 58 Job 59 Job 60

Direct materials………………………………

…

$ 9,200 $ 8,900 $ 6,400

3. Raw Materials:

Beginning balance…………………………… $ 2,300

29,670

8,640

Journal

Account & ExplanationDate Debit